What is considered the object of taxation on the simplified tax system

The current law assumes that the simplified taxation system in 2021 for individual entrepreneurs and LLCs, depending on the characteristics of the activity, will be divided into two types.

According to the Tax Code, the tax can be calculated based on a base formed only from income, or a base consisting of income reduced by expenses incurred.

In each of these cases, business entities will be required to generate a declaration once a year, and pay the tax throughout the year in advance installments.

By Income

The system for calculating taxes of the simplified tax system of 6 percent in 2021 for LLCs and entrepreneurs establishes that the amount of tax must be determined based on the amount of funds received at the cash desk and into the bank account, which are income for the entity. The current law sets the tax calculation rate for this system at 6%. But the authorities operating in the regions are given the right to reduce it in certain cases.

A business entity must record all receipts in a special journal, which is called a book of income and expenses. In this case, information is entered in the journal only in the section intended for incoming income, and the part for expenses is not filled out.

The simplified tax system of 6 percent in 2021 for individual entrepreneurs and organizations is the most optimal for small businesses. It is beneficial if the amount of costs is less than 70% of incoming income.

Income minus expenses

The simplified taxation system in 2021 for LLCs and entrepreneurs determines that in the case of using the “Income reduced by expenses” system, the base also includes cash receipts and bank accounts, but they must additionally be reduced by the amount of expenses incurred during this period . The latter must be paid to suppliers, and also be included in the closed list established by the Tax Code.

When calculating the amount of tax payable, a rate of 15% must be used. However, regional authorities can also change it at will - the law allows you to reduce the rate down to 0% both for the entire system and for specific areas of activity.

A special feature of this system is the fact that the tax will have to be paid even if the business entity has a tax period with a loss. In this case, it is important that he has receipts that are recognized as income.

Then it is necessary to calculate and pay a payment, which is called the minimum tax according to the simplified tax system, income minus expenses. Its rate is 1% of the entire income for a given period.

When applying this system, a business entity must also use a journal - a ledger of income and expenses.

However, now it is necessary to fill out both parts, both income and expenses. Attention: for business entities that are engaged in production and have a serious cost component, the use of this system is more profitable.

Limit on the simplified tax system for 2018-2019 for those planning to switch to a special regime

If an organization plans to switch to the simplified tax system from next year, it needs to take into account that its revenue for 9 months of the current year is also regulated. The limit on the simplified tax system for 2021, exceeding which will not allow switching to a special regime from 2021, is 112.5 million rubles.

NOTE! The limit established for the transition to the simplified simplified tax system 2018-2019 is valid only for organizations. If an individual entrepreneur decides to switch to the simplified tax system, there is no limit on the amount of revenue for 9 months of the year preceding the transition to the simplified tax system.

Both limits (for income for 9 months and for the entire annual income) under the simplified tax system in 2018-2019 do not provide for changes in the income limit depending on the value of the deflator coefficient. The above values of the general income limit under the simplified tax system in 2018-2019 and the limit established for 9 months of 2018-2019 have been introduced since 2017.

Despite the fact that their indexing is provided for in the text of Art. 346.12 and 346.13 of the Tax Code of the Russian Federation, the application of the deflator coefficient to the values of the simplified tax system limit for 2018-2019 is not carried out, because indexation is frozen for the period until 2021 (Law “On Amendments...” dated 07/03/2016 No. 243-FZ).

Find out about the size of the deflator coefficient under the simplified tax system for 2021 from the publication “Deflator coefficients for 2021 have been approved.”

Find the odds sizes planned for 2021.

Features of taxation on the simplified tax system

When using the simplification, a business entity has the opportunity not only to significantly reduce the amount of tax payments, but also to replace several taxes with a single one.

Let's consider what taxes need to be paid, and from which the subject will be exempt:

| Must be paid if simplified payment is used | Exempt from payment when using simplification |

| Single tax, which is calculated when using a simplified tax | – |

| VAT, but only if the subject acts as an agent or accrues VAT on its own initiative | VAT |

| – | Income tax |

| Property tax, but only for those objects that are recorded at cadastral value | Property tax |

| Personal income tax | Personal income tax for individual entrepreneurs regarding types of activities under a simplified regime |

| Transport tax (when there is a base) | – |

| Land tax (when there is a base) | – |

| Water tax (when there is a base) | – |

In addition, for some types of activities reduced rates for payment of social contributions are established. Also, for some types of insurance (usually health insurance and social insurance), 0% rates apply. At this point in time, this reduction is valid until the end of 2018.

When not to use simplification

The law establishes several criteria under which an entity cannot use the simplified system. Thus, a company will not be able to switch to a simplified system if its founders include another company, and its share is 25% or more.

In addition, it is impossible to start using the simplified tax system when a company has branches and representative offices.

Important: types of activities that cannot be performed while on a simplified regime are also defined. These include pawnshops, insurance or lending activities, gambling, production of excise goods and others.

Finally, you cannot be on simplified employment if you do not meet the criteria specified in the Tax Code (number of employees, amount of income, etc.).

The procedure for switching to the simplified tax system

The law specifies several ways to begin using the simplified tax regime.

When registering an LLC or individual entrepreneur

If a future business entity is only collecting all the necessary documents for registering an individual entrepreneur or opening an LLC, then he can submit an application to start using the simplified regime in a general package.

In this situation, along with forms confirming completion of the registration procedure, he will also be given a notice of application of the simplified tax system.

Attention: if at the time of opening a business there are still doubts about choosing a system, then this can be done within 30 days from the moment you receive the forms for registering an LLC or individual entrepreneur.

Transition from other modes

The Tax Code allows existing business entities to change the current tax regime to a simplified system.

But such a step is allowed only from January 1 of the calendar year. Therefore, in order to make the transition, you must complete and submit an application to the tax authority before December 31 of the current year. In it, the business entity indicates that it meets the criteria defined in the Tax Code for the application of the simplified tax system. The latter are calculated based on October 1 of the current year.

So, in order to start applying the simplified regime from January 1, 2019, it is necessary that as of October 1, 2021, the income received does not exceed 112.5 million rubles.

Another opportunity to start using a simplified version is not provided for by law.

The current value of the maximum income of simplifiers

In order to switch to the simplified tax system from January 2021, organizations had to comply with an income limit of 112,500,000 rubles for the first 9 months of 2021. Since the same year, this limit has been frozen: the deflator coefficient will also temporarily not be applied to it.

If the revenue limit under the simplified tax system 2021 at the end of the tax period is exceeded, the business entity is transferred to the general taxation regime.

For organizations that have lost the right to apply the simplified tax system, the opportunity to return to the simplified tax system does not appear immediately. Those who lost their simplified status at the end of 2021 can apply for a second transition to this special regime in 2021, and the transfer to the simplified tax system will take place from the beginning of 2021. This algorithm of actions is enshrined in clause 7 of Art. 346.13 Tax Code of the Russian Federation.

For those who already apply the simplified tax system, the income limit for 2021 to maintain simplified status is at the level of 150 million rubles. This amount is calculated for the entire year from January to December.

If a company is just about to submit a petition to the tax office to switch to a simplified special regime, then another scheme applies:

- it calculates income receipts based on the results of the first 9 months of the current year;

- the result is compared with the legally approved limit for this period - 112.5 million rubles;

- If as of October 1 the limits are met, you can submit an application to the Federal Tax Service to switch to a simplified tax system from January next year.

Please note that the amount of 112.5 million rubles is fixed for the period until 2020. Until this moment it is not subject to revision.

For those planning to change the taxation system, a limit on the amount of income received at the end of 9 months is provided only for legal entities. This rule does not apply to individual entrepreneurs. Letters issued by the Ministry of Finance (for example, No. 03-11-11/47084 dated 05.11.2013) serve as confirmation of the fact that individual entrepreneurs are exempt from fulfilling the requirement to comply with the 9-month income limit.

Income receipts to check compliance with the simplified tax system criteria must be calculated using the cash method (Article 346.17 of the Tax Code of the Russian Federation). Take into account:

- the amount of all payments received into the company’s accounts in the analyzed period;

- the amount of advance payments received;

- posting money through the cash register;

- income not related to sales;

- refunds of funds through bank accounts or cash desks (amounts returned by counterparties).

With regard to the valuation of fixed assets, it is necessary to check the compliance of current accounting data with legislative standards for the simplified tax system only as of the end of the year. That is, during the reporting period, fluctuations in the value of fixed assets can lead to exceeding the limit. But the main thing is that by the end of the year the numbers fit into the standard of 150,000 rubles.

Also see “Conditions for transition to the simplified tax system in 2021: criteria.”

The fact of a significant increase in the limit in 2021 allowed more business entities to take advantage of the opportunity to switch to the simplified tax system. To implement the change of OSNO to this special regime, you must notify the tax authority of your intention in writing this year. If all requirements are met, it will be possible to apply the new tax rules from January next year.

Also see “Changes to the simplified tax system in 2021”.

Read also

14.03.2018

Tax and reporting period

The concepts of what is considered a tax period and what is a reporting period are enshrined in the Tax Code.

Taxable period

For simplicity, the tax period is taken as a calendar year. It is at the end of this period of time that the business entity must make the final tax calculation. Moreover, several reporting periods are included in one tax period.

If a business entity violates the rules for applying the simplified regime, the tax period for it will take less than a year.

Attention: information in the tax return is indicated in cumulative form from the beginning of the tax period.

Reporting period

The following time periods are established as reporting periods: 1st quarter, six months, 9 months. Upon completion of each of them, the advance payment according to the simplified tax system must be calculated.

Turnover restrictions for individual entrepreneurs

The turnover limit is the establishment of a specific profit figure, exceeding which the entrepreneur loses the right to apply preferential tax treatment.

This rule applies to two types of taxes:

- USN.

- Patent.

Each system has its own nuances that you should be aware of.

On the simplified tax system

Under the simplified system, the restriction is strictly regulated by tax legislation, namely Article 346.12 of the Tax Code of the Russian Federation. According to it, businessmen have the right to receive no more than 150 million rubles per year under the simplified tax system. This limit is usually sufficient.

Calculating annual revenue is simple. Cash transactions, both cash and non-cash, are taken into account.

According to a simplified version, businessmen pay 6% if they choose the “income” scheme and 15% if they choose the “income with deduction of expenses” scheme, for example, the purchase of equipment, real estate, transport for work, and obtaining a mortgage are taken into account. Which one to choose is up to the entrepreneur himself.

On UTII

With UTII, the turnover of individual entrepreneurs does not have strict restrictions, but such a regime cannot be used by large businessmen with large incomes. The authorities even planned to abolish this type of tax, but now it remains in force.

On patent

For entrepreneurs working in the patent system, the restrictions are strict and there are no changes today. They are allowed to make a profit of no more than 60 million per year.

Note! In 2021, small business representatives have the opportunity to apply for one patent for several types of work at once. In this case, you will have to control the annual turnover taking into account all types of activities.

Taxes and reporting on the simplified tax system

Tax payment procedure

Tax Returns

Tax payments to the budget must be made by transferring advance payments. Next, at the end of the calendar year, you must make a full tax calculation and pay the remaining amount.

The dates before which the advance amounts must be transferred are determined in the Tax Code. It establishes that this must be done before the 25th day of the month following the end of the next quarter.

Thus, the advance payment must be made before the following dates:

- For the 1st quarter - until April 25;

- Six months before July 25;

- 9 months before October 25th.

But the day of payment of the final payment differs for entrepreneurs and firms. Companies do this first - they need to transfer the tax by March 31, following the reporting period. Then it’s the turn of entrepreneurs - they send taxes to the budget by April 30.

Attention: if the specified deadlines are violated, then the business entity will be subject to liability as specified in the Tax Code.

Taxes and reporting on a simplified system for individual entrepreneurs

For an individual entrepreneur, the number of tax payments and mandatory reports will depend on whether he has hired employees.

In the case where the individual entrepreneur did not hire employees and operates alone:

- Single tax due to the application of simplification.

- Deductions for compulsory types of insurance for yourself;

- Personal property tax;

- If there are appropriate bases - land, transport taxes;

- VAT, if the subject makes allocations in some shipping documents;

- If the legislation of the region provides for the payment of a trade tax.

If the individual entrepreneur hired at least one person:

- Personal income tax on employee remuneration

- Deductions for compulsory types of insurance for payments in favor of individuals.

Individual entrepreneurs without employees send the following reports:

- Single tax declaration due to the application of the simplified tax system (annually).

- VAT declaration (quarterly when this tax is highlighted in the shipping documents).

- Declarations on transport, land, water taxes (quarterly).

- Statistical reporting to the extent required by law.

If the individual entrepreneur has employees, then you also need to register:

- 2 personal income tax (annually).

- 6 personal income tax (quarterly).

- Calculation of insurance premiums (quarterly).

- Payroll in form 4FSS (quarterly).

- SZV-M report (monthly).

- SZV-experience report (annually).

- Information on the average number of employees.

Taxes and reporting on a simplified system for LLC

When applying the simplified tax system, a legal entity must make the following mandatory payments:

- Single tax due to the application of simplification.

- Personal income tax on remuneration of employees and other individuals engaged under civil contracts.

- Deductions for compulsory types of insurance for payments in favor of individuals.

- Property tax (if the region is based on its cadastral value).

- If appropriate bases are available - land, transport and water taxes.

- VAT, if the subject makes allocations in some shipping documents.

- If the legislation of the region provides for the payment of a trade tax.

Also, a legal entity must submit the following reports to the simplified tax system:

- Single tax declaration due to the application of the simplified tax system (annually).

- 2 personal income tax (annually).

- 6 personal income tax (quarterly).

- VAT declaration (quarterly when this tax is highlighted in the shipping documents).

- Declarations on transport, land, water taxes (quarterly).

- Calculation of insurance premiums (quarterly).

- Payroll in form 4FSS (quarterly).

- SZV-M report (monthly).

- SZV-experience report (annually).

- Information on the average number of employees.

- Statistical reporting to the extent required by law.

- Small businesses submit accounting reports in a simplified form (balance sheet, profit and loss statement, report on the intended use of funds). For all other companies, reporting must be submitted in full.

Maximum income under the simplified tax system in 2021

Organizations using the simplified tax system must organize revenue control to ensure that the amount of revenue corresponds to the limit value under the simplified tax system: 150 million in 2021.

Such control is easily implemented in the tax register “Book of Income and Expenses (KUDiR) under a simplified taxation system,” which is filled in with a cumulative total. To carry out control, KUDiR should be generated and archived in digital or paper form on a monthly basis.

At borderline profit levels, when the amount begins to approach the limit value for this tax regime, monitoring of the revenue indicator should be organized on a daily basis. This is due to the fact that the loss of the right to apply the simplification applies from the beginning of the quarter in which the indicator was exceeded. An organization that has lost the right to use the simplified tax system in the middle and at the end of the quarter is considered to be using the simplified tax system from the 1st day of the current quarter with all the ensuing consequences, including the preparation of primary documents. According to the law, invoices must be issued within 5 days from the date of shipment. This means that for the entire VAT tax period, which includes the loss of the right to the simplified tax system, it will not be possible to issue invoices. And the organization will have to pay VAT from its own funds.

The Resolution of the FAS of the Volga District dated May 30, 2007 No. A12-14123/06-C29 and the Supreme Arbitration Court of the Russian Federation dated August 6, 2007 No. 9478/07 contains an opinion and raises the question of the organization’s right to issue invoices for the entire period in which the accident occurred. loss of the right to simplification, but you will have to defend this position before the tax authorities yourself.

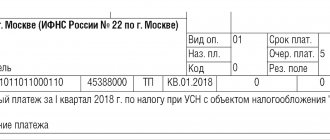

Minimum tax according to the simplified tax system: income minus expenses (1%)

Tax legislation establishes the obligation of a business entity using the simplified tax system “Income minus expenses”, when receiving insignificant income or with negative performance indicators, to calculate and pay the minimum tax, which is 1% of the amount of income received.

The minimum tax must be calculated based on the results for the reporting year.

It is always necessary to calculate the minimum tax, even if the profit is received by a company or individual entrepreneur. This calculated amount is compared with the estimated tax amount. Anything more must be transferred to the budget.

Attention: if the minimum tax is lower than the calculated tax according to the simplified tax system, then you need to transfer a single tax, calculated from the difference in income received and expenses incurred. Otherwise, you need to pay the minimum - 1%.

Previously, the minimum tax and the single tax under the simplified tax system of 15% had different BCCs, and business entities had to send letters to the tax office about the offset. Currently, these payments are united by one KBK and inspectors at the Federal Tax Service independently make offsets based on these declarations.

Maximum turnover of individual entrepreneurs under the simplified tax system

The turnover limit under the simplified tax system in 2021 was 150 million rubles. This change is reflected in Article 346.12 of the Tax Code of the Russian Federation.

Under the simplified regime, you can choose one of two options: payments from income (6%) or payments from income reduced by expenses.

If everything is clear with the first scheme, then when paying taxes according to the “income minus expenses” scheme, you need to figure it out. When applying the income-expenses scheme, you must subtract the amount of costs from the enterprise's revenue and multiply this difference by 15%. However, in some regions this rate is lower; in St. Petersburg, for example, it is 10%.

In addition, if your company has zero profit (that is, the difference between income and expenses is zero), then you will still have to pay tax. It will be equal to 1% of the income.

“Simplified” was created to support small and medium-sized businesses, so the presence of a limit on it is not surprising.

If you received more than 150 million rubles in income per year, then you will automatically be transferred to the main taxation system or to the single tax regime on temporary income if you are engaged in retail trade, provide repair, washing and servicing services for cars, are involved in veterinary medicine, advertising, transporting people and goods, providing accommodation services, providing retail space or parking space.

Please note that if you want to switch to the single tax regime, you need to fill out an application for the tax office, and this must be done within five days after the end of the quarter of work under the simplified tax system. Otherwise, you will be automatically transferred to OSN.

The transfer will be made on the first day of the quarter in which the income limit was exceeded.

If you are planning to switch to a simplified regime, you should track the residual value of your fixed assets. This figure will also be useful to you if you are already using the simplified tax system. The fact is that the amount of your funds also has a limit and for applying the simplified tax system it is 150 million rubles in 2021, it cannot be exceeded.

If you decide to switch to the simplified tax system in the new year, then the cost of fixed assets as of December 31 of last year should not exceed this limit.

Tax reduction due to contributions to the Pension Fund and compulsory medical insurance (according to the 6% and 15% systems)

LLC and individual entrepreneur with employees

Legislation establishes the right of organizations and entrepreneurs acting as employers to take into account, when determining tax under the simplified tax system, the amount of contributions calculated and transferred to the budget for their employees.

However, the amount that can be taken as a deduction depends on the type of simplified tax system used:

- If a business entity applies the simplified tax system of 6 percent, then it has the right to reduce the amount of calculated tax by 50%, but no more. Individual entrepreneurs are given the opportunity to use as a deduction not only contributions for employees, but fixed contributions to extra-budgetary funds transferred by them to themselves.

- When the simplified tax system is used for income minus expenses, then all payments transferred to the budget can be taken into account as expenses, thereby reducing the tax base for the single tax.

Attention: you can take into account social contributions that were transferred to the budget in the current period. What is important here is the fact of payment, and not the period for which it was made.

Individual entrepreneur without employees

When an entrepreneur does not involve hired personnel in his activities, the law gives him the right to reduce the amount of tax by the entire amount of compulsory insurance contributions paid to extra-budgetary funds.

At the same time, the provisions of the regulations make it possible to reduce taxes not only by the amount of the above contributions, but also by the amount of contributions that the subject pays to the Pension Fund in the amount of 1% from the excess of income of 300,000 rubles.

There is a rule according to which contributions can be deducted only if the business entity actually paid them in the period under review. If in this period contributions were paid not only for the reporting period, you can claim a deduction for the full amount of the payment made.

Therefore, individual entrepreneurs under this system have the right to choose - pay payments immediately and claim a deduction in full, or transfer money in quarterly or monthly installments and set them to be reduced in installments.

Fixed assets and simplification

For entrepreneurs working on the simplified tax system, there is also a limitation on the value (residual value) of their fixed assets. Thus, the limit of the simplified tax system 2021 in relation to fixed assets is set at 150 million rubles. But it only affects the right to continue to use the simplified tax system, and not to work on it for the first time.

Exemption from the obligation to maintain full accounting does not give the right to business entities to stop tracking the value of the total valuation of objects from among the fixed assets. Compliance with the boundary values must be checked at the reporting date.

Please note that the simplified tax system limit for 2021 for LLCs and other business entities for fixed assets must be met as of the last day of the current year. If the limit has been exceeded during the year, this does not affect the possibility of applying this special regime.

If a small business uses the simplified tax system to calculate depreciation once a year at the end of the year, this cannot be a reason for not conducting quarterly reconciliations of the residual value of fixed assets. When you apply the simplified tax system, the income limit for 2021 and the limitation on fixed assets must be observed at all times, so as not to unexpectedly fall out of the special regime. If a violation of one or more requirements is detected, the right to use the simplified tax system is lost.

Also see “Depreciation under the simplified tax system “Income minus Expenses” in 2021” (relevant in 2018).

Repeated transition to simplification is acceptable. The chance to notify the tax authorities of such an intention appears only a full year after the loss of the grounds for having the status of a simplified person.

Finally, let us remind you that for the simplified tax system the revenue limit for 2021 and other amount restrictions are fixed until the beginning of 2021. You must adhere to them constantly.

Read also

14.03.2018

Combining the simplified tax system with other tax regimes

An economic entity can carry out several types of activities at once. Some of them may be on the simplified tax system, and some on other preferential systems.

It is allowed to combine simplification with systems such as UTII and PSN. That is, the subject generally applies the simplified tax system, but for a certain type of activity is a UTII payer or has acquired a patent.

The main requirement when implementing a combination of modes is the organization and maintenance of separate records of the company’s performance indicators, as well as the property used. This must be done to avoid double taxation. When UTII or a patent is closed for this type of activity, a simplification should be applied in the future.

STS criteria in 2021: table

It is important to take into account that the transition to “simplified” is only possible if all requirements are met at the same time. For convenience, we have collected all the conditions for the transition and work to the simplified tax system that are in force in 2018-2019. in one table:

| Transition criteria and conditions for applying the simplified tax system in 2018-2019 | Current condition or limit | Who does it apply to? | Norm of the Tax Code of the Russian Federation |

| By type of activity | The entities listed in paragraph 3 of Art. 346.12 of the Tax Code of the Russian Federation, including foreign companies, institutions (state-owned and budgetary) | Individual entrepreneur and legal entity | pp. 2-10, 17, 18, 20, 21 p. 3 art. 346.12 |

| Compatible with other modes | Not compatible with:

| Individual entrepreneur and legal entity | pp. 13, 11 clause 3 art. 346.12 |

| Availability of branches | Unacceptable | legal entity | pp. 1 clause 3 art. 346.12 |

| Management structure | Participation of other organizations no more than 25% | legal entity | pp. 14 clause 3 art. 346.12 |

| Residual value of fixed assets | No more than 150 million rubles. (for an LLC to switch to the simplified tax system from 2021, compliance with the limit as of 10/01/2018 is required) | legal entity | pp. 16 clause 3 art. 346.12 |

| Average number | No more than 100 people. | Individual entrepreneur and legal entity | pp. 15 clause 3 art. 346.12 |

| “Transitional” revenue limit (STS 2018-2019) | No more than 112.5 million rubles. for 9 months of the year preceding the transition to “simplified” | legal entity | clause 2 art. 346.12 |

| Maximum revenue under the simplified tax system 2018-2019, allowing the use of the regime | No more than 150 million rubles. in a year | Individual entrepreneurs and legal entities working on simplified terms | clause 4 art. 346.13 |