Income tax

Once a quarter, advance payments for income tax are transferred to organizations whose sales income over the previous four quarters did not exceed an average of 15,000,000 rubles. for each quarter (clause 3 of Article 286 of the Tax Code of the Russian Federation). When calculating your average income, take into account the last quarter of the period for which you file your tax return. The deadline for transferring the advance payment for income tax is no later than the 28th day of the month following the reporting period (clause 1 of Article 287, clause 3 of Article 289 of the Tax Code of the Russian Federation).

However, it is also possible to pay income tax on a monthly basis. The organization is obliged to transfer monthly advance payments based on the profit received in the previous quarter if two conditions are simultaneously met:

- she did not apply to switch to monthly advance payments based on actual profits;

- its income for the previous four quarters exceeded an average of 15,000,000 rubles. per quarter (clauses 2 and 3 of Article 286 of the Tax Code of the Russian Federation).

Below is a table with the deadlines for paying income tax in 2018 by legal entities in various situations:

Income tax payment deadline in 2021

| Income tax | For what period is it paid? | Payment deadline |

| Income tax (if only quarterly advance payments are made) | For 2021 | No later than March 28, 2018 |

| For the first quarter of 2021 | No later than 04/28/2018 | |

| For the first half of 2021 | No later than July 30, 2018 | |

| For 9 months of 2021 | No later than October 29, 2018 | |

| Income tax (when paying monthly advance payments with additional payment at the end of the quarter) | For 2021 | No later than March 28, 2018 |

| For January 2021 | No later than 01/29/2018 | |

| For February 2021 | No later than 02/28/2018 | |

| For March 2021 | No later than March 28, 2018 | |

| Additional payment for the first quarter of 2021 | No later than 04/28/2018 | |

| For April 2021 | No later than 04/28/2018 | |

| For May 2021 | No later than 05/28/2018 | |

| For June 2021 | No later than June 28, 2018 | |

| Additional payment for the first half of 2021 | No later than July 30, 2018 | |

| For July 2021 | No later than July 30, 2018 | |

| For August 2021 | No later than 08/28/2018 | |

| For September 2021 | No later than September 28, 2018 | |

| Additional payment for 9 months of 2021 | No later than October 29, 2018 | |

| For October 2021 | No later than October 29, 2018 | |

| For November 2021 | No later than November 28, 2018 | |

| For December 2021 | No later than December 28, 2018 | |

| Income tax declaration (for monthly payment of advances based on actual profit) | For 2021 | No later than March 28, 2018 |

| For January 2021 | No later than 02/28/2018 | |

| For February 2021 | No later than March 28, 2018 | |

| For March 2021 | No later than 04/28/2018 | |

| For April 2021 | No later than 05/28/2018 | |

| For May 2021 | No later than June 28, 2018 | |

| For June 2021 | No later than July 30, 2018 | |

| For July 2021 | No later than 08/28/2018 | |

| For August 2021 | No later than September 28, 2018 | |

| For September 2021 | No later than October 29, 2018 | |

| For October 2021 | No later than November 28, 2018 | |

| For November 2021 | No later than December 28, 2018 |

Tax calendar for 2021: reporting deadlines

We present to your attention the reporting calendar for 2018. For the convenience of visitors, the information is collected in a table. The calendar is very extensive, so for more convenient use, we advise you to select those reports that relate to your activities. The third column indicates which organizations or individual entrepreneurs submit a specific report.

| Deadline for submission | Title of the report and receiving authority | Who rents |

| January 9 | Declaration of mineral extraction tax for December 2021 to the Federal Tax Service | Legal entities - subsoil users |

| January 15 | Report on the generation, use, neutralization and disposal of waste (except for statistical reporting) for 2021 in the Technical Specifications for Natural Resources and Ecology | Legal entities and individual entrepreneurs whose work generates waste |

| January 15 | SZV-M for December 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| January 22 | Unified simplified tax return for the 4th quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs that did not operate during the reporting period |

| January 22 | Information on the average headcount for 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs who hired workers during this period |

| January 22 | Declaration of water tax for 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs using water bodies |

| January 22 | Declaration on UTII for 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs |

| January 22 | DSV-3 for the 4th quarter of 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs who pay additional contributions to the funded part of the pension |

| January 22 | Journal of accounting of received and issued invoices for the 4th quarter of 2021 in electronic form in the Federal Tax Service | The following legal entities and individual entrepreneurs:

|

| January 22 | Declaration of indirect taxes for December 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs paying VAT and excise taxes in the process of importing goods into Russia from their EAEU member states |

| January 22 | 4-FSS (paper) for 2021 in the FSS | Legal entities and individual entrepreneurs with hired employees, numbering less than 25 people |

| The 25th of January | 4-FSS (electronic) for 2021 in the FSS | Legal entities and individual entrepreneurs with employees of 25 or more people |

| The 25th of January | VAT return for the 4th quarter of 2021 to the Federal Tax Service | The following legal entities and individual entrepreneurs:

|

| January 30 | Unified calculation of insurance premiums to the Federal Tax Service | Legal entities and individual entrepreneurs with employees |

| January 31 | Declaration of mineral extraction tax for December 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs - subsoil users |

| 1st of February | 2 TP-waste in Rosprirodnadzor technical specifications | Legal entities and individual entrepreneurs involved in waste management |

| 1st of February | Transport tax return for 2021 to the Federal Tax Service | Legal entities to which vehicles are registered |

| 1st of February | Tax return for land tax for 2021 to the Federal Tax Service | Legal entities - owners of land plots |

| February, 15 | SZV-M for January 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| February 20th | Declaration of indirect taxes for January 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs paying VAT in connection with the import of products to Russia from EAEU member countries |

| 28th of February | Income tax return for January 2021 to the Federal Tax Service | Legal entities with income of more than 15 million rubles for the last quarter during the last year submit a declaration and pay tax monthly |

| 28th of February | Tax calculation for income tax for January 2021 at the Federal Tax Service | Legal entities-tax agents, calculating monthly advance payments based on actual profit received |

| 28th of February | Declaration on mineral extraction tax for January 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs - subsoil users |

| March 1 | SVZ-STAZH for 2021 in the Federal Tax Service | Legal entities and individual entrepreneurs with employees |

| March 1 | Information about the impossibility of withholding tax, the amount of income from which tax was not withheld, and the amount of tax not withheld for 2017 in the Federal Tax Service | Legal entities and individual entrepreneurs - tax agents for personal income tax |

| 10th of March | Declaration of payment for negative environmental impact for 2021 to Rosprirodnadzor | Legal entities and individual entrepreneurs obligated to pay fees for negative impact on the environment |

| March 15th | SZV-M for February 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| 20th of March | Declaration of indirect taxes for February 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs paying VAT in connection with the import of products to Russia from EAEU member countries |

| March 28 | Income tax return for 2021 to the Federal Tax Service | Legal entities, regardless of the procedure for paying advance payments |

| March 28 | Income tax return for February 2021 to the Federal Tax Service | Legal entities paying advance payments based on actual profit received |

| March 28 | Annual report on corporate income tax activities in the Russian Federation for 2021 to the Federal Tax Service | Foreign organizations operating in Russia through a permanent representative office |

| 30th of March | Property tax return for 2021 to the Federal Tax Service | Legal entities - property owners |

| April 2 | Annual financial statements for 2021 to the Federal Tax Service | Legal entities required to maintain accounting records |

| April 2 | Auditor's report along with the annual financial statements for 2021 to the Federal Tax Service | Legal entities subject to mandatory audit |

| April 2 | Declaration under the simplified tax system for 2021 to the Federal Tax Service | Legal entities on the simplified tax system |

| April 2 | Declaration on Unified Agricultural Tax for 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs – agricultural producers |

| April 2 | 6-NDFL for 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs who are tax agents for personal income tax |

| April 2 | 2-NDFL for 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs who are tax agents for personal income tax |

| April 16 | SZV-M for March 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| April 16 | Documents confirming the type of activity in the Social Insurance Fund | Legal entities registered in 2021 or earlier |

| 20 April | Declaration of water tax for the 1st quarter of 2021 to the Federal Tax Service | Legal entities that have water bodies |

| 20 April | Declaration on UTII for the 1st quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs using UTII |

| 20 April | Journal of accounting of received and issued invoices for the 1st quarter of 2021 in electronic form in the Federal Tax Service | Legal entities and individual entrepreneurs of the following categories:

|

| 20 April | Unified simplified tax return for the 1st quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs that do not have taxable objects |

| 20 April | 4-FSS for the 1st quarter of 2021 on paper in the FSS | Legal entities and individual entrepreneurs employing employees of less than 25 people |

| 25th of April | VAT return for the 1st quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs, tax agents who are exempt from taxpayer duties or are not payers and organizations selling goods and services exempt from taxation |

| 25th of April | 4-FSS for the 1st quarter of 2021 in electronic form in the FSS | Legal entities and individual entrepreneurs with employees of more than 25 people |

| April 28 | Income tax return for the 1st quarter of 2021 to the Federal Tax Service | Legal entities that report quarterly |

| April 28 | Income tax return for March 2021 to the Federal Tax Service | Legal entities that report monthly |

| April 28 | Tax calculation for income tax for March or 1st quarter of 2018 at the Federal Tax Service | Legal entities that are tax agents for income tax |

| April 30 | Declaration of the simplified tax system for 2021 | Individual entrepreneurs using the simplified tax system |

| May 3 | 6-NDFL for the 1st quarter of 2021 in the Federal Tax Service | Legal entities and individual entrepreneurs - tax agents for personal income tax |

| May 3 | Unified calculation of insurance premiums for the 1st quarter of 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs, with employees |

| May 3 | Calculation of property tax on advance payments for the 1st quarter of 2018 to the Federal Tax Service | Legal entities that are tax payers |

| May 15 | SZV-M for April 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| May 21st | Notification of controlled transactions for 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs, if controlled transactions took place |

| May 28 | Income tax return for April 2021 to the Federal Tax Service | Legal entities that report monthly |

| May 28 | Tax calculation for income tax for April 2021 at the Federal Tax Service | Legal entities that are tax agents, calculating monthly advance payments based on actual profit received |

| June 15 | SZV-M for May 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| July 15 | SZV-M for June 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| July 20 | 4-FSS for the first half of 2021 on paper in the FSS | Legal entities and individual entrepreneurs with employees of less than 25 people |

| July 20 | Declaration of water tax for the 2nd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs with water bodies |

| July 20 | Unified simplified tax return for the 2nd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs in the absence of taxable objects |

| July 20 | Declaration on UTII for the 2nd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs using UTII |

| July 20 | Journal of accounting of received and issued invoices for the 2nd quarter of 2021 in electronic form in the Federal Tax Service | Legal entities and individual entrepreneurs of the following categories:

|

| July 25 | 4-FSS for the first half of 2021 in electronic form in the FSS | Legal entities and individual entrepreneurs with employees of more than 25 people |

| July 25 | VAT return for the 2nd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs who are tax agents, companies that are exempt from taxpayer obligations or are not payers and organizations that sell goods and services exempt from taxation |

| July 30 | Income tax return for the 2nd quarter of 2021 to the Federal Tax Service | Legal entities that report quarterly |

| July 30 | Income tax return for June 2021 to the Federal Tax Service | Legal entities that report monthly |

| July 30 | Tax calculation for income tax for June or the 2nd quarter of 2018 at the Federal Tax Service | Legal entities - tax agents for income tax |

| July 30 | Unified calculation of insurance premiums for the first half of 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs with employees |

| July 30 | Calculation of property tax on advance payments for the 2nd quarter of 2018 to the Federal Tax Service | Legal entities that are tax payers |

| July 31 | 6-NDFL for the first half of 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs who are tax agents for personal income tax |

| August 15 | SZV-M for July 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| August 28 | Income tax return for July 2021 to the Federal Tax Service | Legal entities that report monthly |

| August 28 | Tax calculation for income tax for July 2021 at the Federal Tax Service | Legal entities that are tax agents for income tax |

| September 15th | SZV-M for August 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs using hired labor |

| September 28 | Income tax return for August 2021 to the Federal Tax Service | Legal entities that report monthly |

| September 28 | Tax calculation for income tax for August 2021 at the Federal Tax Service | Legal entities classified as tax agents for income tax |

| October 15 | SZV-M for September 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| 22 of October | Unified simplified tax return for the 3rd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs that do not have taxable objects |

| 22 of October | Declaration of water tax for the 3rd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs who have water bodies |

| 22 of October | Declaration on UTII for the 3rd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs using UTII |

| 22 of October | Journal of accounting of received and issued invoices for the 3rd quarter of 2021 in electronic form in the Federal Tax Service | Legal entities and individual entrepreneurs of the following categories:

|

| 22 of October | 4-FSS for 9 months of 2021 on paper in the FSS | Legal entities and individual entrepreneurs with employees of less than 25 people |

| the 25th of October | VAT return for the 3rd quarter of 2021 to the Federal Tax Service | Legal entities and individual entrepreneurs, tax agents, companies that are exempt from taxpayer obligations or are not payers and organizations selling goods and services |

| the 25th of October | 4-FSS for the first half of 2021 in electronic form in the FSS | Legal entities and individual entrepreneurs with employees of more than 25 people |

| 29th of October | Income tax return for September or the 3rd quarter of 2018 to the Federal Tax Service | Legal entities that report monthly |

| 29th of October | Tax calculation for income tax for September or the 3rd quarter of 2018 at the Federal Tax Service | Legal entities - tax agents for income tax |

| October 30 | Unified calculation of insurance premiums for 9 months of 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs with employees |

| October 30 | Calculation of property tax on advance payments for the 3rd quarter of 2018 | Legal entities - tax payers |

| October 31 | 6-NDFL for 9 months of 2021 at the Federal Tax Service | Legal entities and individual entrepreneurs who are tax agents for personal income tax |

| 15th of November | SZV-M for October 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| November 28 | Income tax return for October 2021 to the Federal Tax Service | Legal entities that report monthly |

| November 28 | Tax calculation for income tax for October 2021 at the Federal Tax Service | Legal entities - tax agents for income tax |

| December 17 | SZV-M for November 2021 in the Pension Fund of Russia | Legal entities and individual entrepreneurs with employees |

| December 28th | Income tax return for November 2021 to the Federal Tax Service | Legal entities that report monthly |

| December 28th | Tax calculation for income tax for November 2021 at the Federal Tax Service | Legal entities - tax agents for income tax |

Value added tax (VAT)

Transfer the VAT amount calculated based on the quarterly results in 2018 evenly over the next three months. Payment deadlines are no later than the 25th of each of these months. For example, the amount of VAT payable to the budget for the first quarter of 2021 must be transferred in equal installments no later than April 25, May 25 and June 25.

If the 25th falls on a non-working day, then VAT must be paid no later than the first working day following the non-working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). For example, November 25, 2021 falls on a Sunday, so the last day to pay the first part (share) of VAT for the third quarter is November 26, 2021. This procedure follows from the provisions of Article 163 and paragraph 1 of Article 174 of the Tax Code of the Russian Federation. We present the deadlines for paying VAT in 2021 in the table (for legal entities).

VAT payment deadlines in 2021

| 1st payment for the fourth quarter of 2021 | No later than 01/25/2018 |

| 2nd payment for the fourth quarter of 2021 | No later than 02/26/2018 |

| 3rd payment for the fourth quarter of 2021 | No later than March 26, 2018 |

| 1st payment for the first quarter of 2021 | No later than 04/25/2018 |

| 2nd payment for the first quarter of 2021 | No later than 05/25/2018 |

| 3rd payment for the first quarter of 2021 | No later than June 25, 2018 |

| 1st payment for the second quarter of 2021 | No later than July 25, 2018 |

| 2nd payment for the second quarter of 2021 | No later than 08/27/2018 |

| 3rd payment for the second quarter of 2021 | No later than September 25, 2018 |

| 1st payment for the third quarter of 2021 | No later than October 25, 2018 |

| 2nd payment for the third quarter of 2021 | No later than November 26, 2018 |

| 3rd payment for the third quarter of 2021 | No later than December 25, 2018 |

What taxes and fees are established by Russian legislation?

In this block of the article we will describe when to pay taxes for the 4th quarter of 2018, which are mandatory in connection with the use of a particular taxation system. This information is relevant for both organizations and individual entrepreneurs.

We note here that when paying income under employment and civil contracts and paying insurance premiums and personal income tax under them, organizations must be guided by the same deadlines as individual entrepreneurs. Therefore, the table on payment of contributions and personal income tax in relation to hired personnel from the block “When to pay taxes for individual entrepreneurs” is also relevant for organizations.

Next, we list those taxes, contributions and fees with the deadlines for their payment, which are paid regardless of what taxation system is applied (here, the fact that an organization or individual entrepreneur is recognized as a taxpayer in relation to this tax or fee is important):

- Trading fee for the 4th quarter of 2021 - 01/25/2019.

- Water tax for the 4th quarter of 2021 - 01/21/2019 (since 01/20/2019 is a Sunday).

- Mineral extraction tax (MET).

- Gambling tax.

- Environmental fee for 2021 - 04/15/2019.

- Payment for negative impact on the environment for 2021 - 03/01/2019.

- Excise taxes.

For certain categories of taxpayers, payment deadlines may be shifted by three or six months. The conditions for this movement are specified in Art. 204 Tax Code of the Russian Federation.

- The fee for the use of aquatic biological resources can be paid at a time or in the form of regular contributions during the validity period of the permit for the extraction of aquatic biological resources. Subject to gradual payment, its terms:

- for October 2021 - 10/22/2018 (since 10/20/2018 is a Saturday);

- for November 2021 - November 20, 2018;

- for December 2021 - 12/20/2018.

It is necessary to comply with the deadline for paying property tax for legal entities in 2018:

- Russian companies.

- Foreign legal entities that have representative offices or taxable real estate in the Russian Federation.

Fill out the declaration online

Tax under simplified tax system

Transfer advance payments for the single tax no later than the 25th day of the first month following the reporting period (quarter, half-year and nine months). That is, no later than April 25, July 25 and October 25. This procedure is established by Article 346.19 and paragraph 7 of Article 346.21 of the Tax Code of the Russian Federation.

There are different deadlines for paying the single (minimum) tax at the end of the year. As a general rule, organizations must remit tax no later than March 31 of the following year, and entrepreneurs no later than April 30 of the next year. This follows from the provisions of paragraph 7 of Article 346.21 and paragraph 1 of Article 346.23 of the Tax Code of the Russian Federation. We present the deadlines for paying the simplified tax system in 2021 in the table.

Deadlines for payment of the simplified tax system in 2021

| For 2021 (only organizations pay) | No later than 04/02/2018 |

| For 2021 (paid only by individual entrepreneurs) | No later than 05/03/2018 |

| For the first quarter of 2021 For the first half of 2021 | No later than 04/25/2018 No later than 07/25/2018 |

| For 9 months of 2021 | No later than October 25, 2018 |

Why are the deadlines for paying taxes and advance payments different?

In general, income tax involves payment of:

- advances - based on the results (in some cases during) the reporting period;

- basic tax - based on the results of the year.

At the same time, additional classifications of these payments are possible based on the specific tax payment scheme.

There are three such schemes:

- The taxpayer pays:

- advances at the end of the reporting period - 1st quarter, half year and 9 months;

- income tax for the year.

- Monthly advances are made (before the end of the current month), and then additional payments are made on them:

- based on the results of each quarter;

- results of the year.

- Paid:

- advances based on the results of each month;

- tax at the end of the year.

Thus, financial results are essentially assessed based on the results of each quarter.

This is a more complex scheme - it takes into account the financial results of both the reporting and the previous quarter (or quarters).

With this scheme, the financial results of each month are taken into account.

Experts from the ConsultantPlus legal reference system explain how monthly advance payments are calculated based on actual profits. Sign up for a trial online access to read.

Enterprises that fall under the criteria listed in paragraph 3 of Art. have the right to apply the first scheme. 286 Tax Code of the Russian Federation.

The rest choose the second or third.

We will tell you by what date the profit for the year must be converted into tax, subject to timely payment to the budget, within the framework of each payment calculation scheme.

Personal income tax on vacation and sick leave benefits

In general, personal income tax must be transferred from wages no later than the day following the date of payment. For example, the employer paid the salary for January 2021 on February 6, 2021. In this case, income was received on January 31. The tax must be withheld on February 6th. And the last date when personal income tax needs to be transferred to the budget is February 7, 2021.

However, personal income tax withheld from temporary disability benefits, benefits for caring for a sick child, as well as from vacation pay must be transferred no later than the last day of the month in which the income was paid. For example, an employee goes on vacation from January 25 to February 15, 2021. Vacation pay was paid to him on January 20. In this case, consider the income received on the date of issuance of vacation pay - January 20. Tax must be withheld from the payment on the same day. And personal income tax must be transferred to the budget no later than January 31, 2018. Below we provide a table with the deadlines for paying personal income tax on vacation and sick leave benefits in 2021.

Deadlines for paying personal income tax on vacation and sick pay in 2018

| For January 2021 | No later than 01/31/2018 |

| For February 2021 | No later than 02/28/2018 |

| For March 2021 | No later than 04/02/2018 |

| For April 2021 | No later than 05/03/2018 |

| For May 2021 | No later than 05/31/2018 |

| For June 2021 | No later than 07/02/2018 |

| For July 2021 | No later than July 31, 2018 |

| For August 2021 | No later than 08/31/2018 |

| For September 2021 | No later than 01.10.2018 |

| For October 2021 | No later than 10/31/2018 |

| For November 2021 | No later than November 30, 2018 |

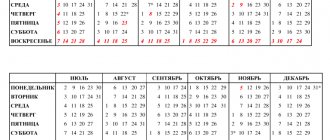

Deadlines for payment of insurance premiums to the Federal Tax Service and Social Insurance Fund in 2021

| Type of insurance premiums | For what period do they pay? | Deadline no later than which the money must be transferred |

| Insurance premiums paid to the tax authorities | ||

| Contributions from payments to employees and other individuals | For December 2021 | 01/15/2018 |

| For January 2021 | 02/15/2018 | |

| For February 2021 | 03/15/2018 | |

| For March 2021 | 04/16/2018 | |

| For April 2021 | May 15, 2018 | |

| For May 2021 | June 15, 2018 | |

| For June 2021 | July 16, 2018 | |

| For July 2021 | 08/15/2018 | |

| For August 2021 | September 17, 2018 | |

| For September 2021 | October 15, 2018 | |

| For October 2021 | November 15, 2018 | |

| For November 2021 | 12/17/2018 | |

| Entrepreneur's contributions for himself | For 2021 | 01/09/2018 |

| For 2021, from an income that exceeds RUB 300,000. | 04/02/2018 | |

| Contributions paid to the Social Insurance Fund | ||

| Contributions for injuries | For December 2021 | 01/15/2018 |

| For January 2021 | 02/15/2018 | |

| For February 2021 | 03/15/2018 | |

| For March 2021 | 04/16/2018 | |

| For April 2021 | May 15, 2018 | |

| For May 2021 | June 15, 2018 | |

| For June 2021 | July 16, 2018 | |

| For July 2021 | 08/15/2018 | |

| For August 2021 | September 17, 2018 | |

| For September 2021 | October 15, 2018 | |

| For October 2021 | November 15, 2018 | |

| For November 2021 | 12/17/2018 | |

UTII

Transfer the calculated UTII amount no later than the 25th day of the first month following the expired tax period (quarter). That is, no later than April 25, July 25, October 25 and January 25 of the year. This is stated in paragraph 1 of Article 346.32 of the Tax Code of the Russian Federation. Payment of advance contributions to the budget for UTII is not provided.

The deadline for paying UTII may fall on a non-working day. In this case, the tax must be transferred to the budget on the next working day (clause 7, article 6.1 of the Tax Code of the Russian Federation).

Deadline for payment of UTII in 2021

| For the fourth quarter of 2021 | No later than 01/25/2018 |

| For the first quarter of 2021 | No later than 04/25/2018 |

| For the second quarter of 2021 | No later than July 25, 2018 |

| For the third quarter of 2021 | No later than October 25, 2018 |

How taxes are paid when using natural resources in 2021

| Tax | Characteristics | Period | Payment deadline |

| MET | All payers | December 2021, every month of 2018 from January to November | Until the 25th day of the month following the month for which the tax is paid |

| Water | All payers | 4th quarter of 2021, first 3 reporting quarters of 2018 | Until the 20th day of the month following the quarter for which the tax is paid |

| Levy for biological resources | The payers specified in clause 1 of Art. 333.1 Tax Code of the Russian Federation | When obtaining a permit to use biological resources | |

| Payers listed in clause 2 of Art. 333.1 of the Tax Code of the Russian Federation upon payment of a one-time contribution of 10% of the fee | When applying for a permit | ||

| Payers specified in clause 2 of Art. 333.1 of the Tax Code of the Russian Federation when paying the difference between the fee and a one-time contribution - equal payments during the validity period of the permit | Every month while the permit is valid | Until the 20th day of each month during the validity period of the permit |

Let us now study what the calendar for paying regional taxes will be like in 2021.

Unified agricultural tax

The deadline for paying the unified agricultural tax in 2021 (UST) is no later than March 31 of the year following the expired tax period. This follows from the provisions of paragraphs 3 and 5 of Article 346.9, paragraph 2 of Article 346.10 of the Tax Code of the Russian Federation.

The last day for tax payment (advance payment) may be a non-working day. In this case, transfer the amount of the unified agricultural tax (advance payment) to the budget on the next working day (clause 7, article 6.1 of the Tax Code of the Russian Federation).

| Deadline for payment of Unified Agricultural Tax in 2021 | |

| For 2021 | No later than 04/02/2018 |

| For the first half of 2021 | No later than July 25, 2018 |

When to pay transport tax and what happens if you don’t pay?

This question arises for many car owners. After all, they themselves must worry about what tax to pay and when. Unpaid or partially paid tax is considered a violation, and defaulters are held accountable for this.

When to pay transport tax?

Transport tax by individuals must be paid before December 1 inclusive . The deadline for paying tax for 2021 is December 1, 2017, for 2021 - December 1, 2018, etc. The statute of limitations for taxes is three years when the amount exceeds 3,000 rubles. and three years six months if its value is less than 3,000 rubles. Exceptions may occur in cases where the tax office through the court has restored the deadline for filing an application for collection. In a normal situation, in 2021 you can forget about your debts for 2014 and earlier.

// On December 28, 2021, the so-called “Tax Amnesty Law” was adopted, according to Article 12 of which the transport tax arrears accrued as of January 1, 2015, as well as the arrears of penalties accrued on this arrears are subject to write-off for individuals . //

You can calculate the tax amount for your car in advance using a transport tax calculator .

How do you warn about debt?

The tax office warns about the occurrence of debt within three months after the payment deadline: that is, until March 1 - if the tax amount was more than 500 rubles. and within a year - if less than 500 rubles. At the same time, registered letters are sent and messages are received by e-mail. The car owner can check the debts himself on the website nalog.ru in his personal account or on State Services. The standard period for payment of the amounts specified in the request is 8 working days. Got a debt? Get a penalty .

What is a penalty?

Responsibility for unpaid tax arises from the first day of delay, from December 2. The initial punishment for forgetful car owners is a fine.

Amount of penalties = Unpaid tax amount x Number of days of delay x Central Bank key rate in % / 30,000.

Example: You owe 3075 rubles. You want to pay off the debt on December 31st. In this case, in addition to 3,075 rubles, you will have to pay another 23 rubles. Calculation: 3075 rub. x (16 days x 8.25 + 13 days x 7.75) / 30,000 = 23.85 rubles, since the Central Bank rate decreased from 8.25% to 7.75% on December 18, 2017. If you remember about paying the tax in a year, the penalties will increase to 306.32 rubles (3075 rubles x (16 days x 8.25 + 56 days x 7.75 + 323 x 7.5%) / 30,000). The Central Bank rate from February 12, 2018 is 7.5%.

Penalties will accrue until you pay everything, or until the statute of limitations expires - then the debt will be written off.

What are the fines?

20% of the amount of unpaid or partially paid tax, hidden tax base or its illegal understatement. 40% - if they can prove that these actions were committed intentionally. The imposition of a fine occurs at the discretion of the tax office, which has identified unpaid tax.

Debt collection through court

As soon as the amount of arrears exceeds 3,000 rubles , the tax service has six months to file an application for collection in a court of general jurisdiction. A court order is issued by a magistrate alone (without trial or calling the parties to hear their explanations) and has the force of an executive document. A copy of the order is sent to the debtor. If the car owner has objections, he can appeal it within 10 days from the date of receipt of the order. If this happens, the order is canceled and the tax service has another six months to send the claim to the district court, where the case is considered with the participation of the parties.

A small amount of debt does not relieve the car owner from liability. If taxes and penalties amount to even less than 3,000 rubles, then the tax office within 6 months can initiate the procedure for their collection after three years have passed from the date of expiration of the earliest requirement.

After the appeal period has expired, if this has not happened, enforcement proceedings are initiated, on the basis of which the debt is collected from the citizen. The procedure also follows the standard procedure: notification of the debtor, and then forced collection.

How does enforcement occur?

Unpaid tax can be obtained from the debtor by writing off funds from accounts, arrest and subsequent sale of property, including a car, a ban on traveling abroad (if the amount of debt exceeds 30,000 rubles), and restrictions on registration actions.

Criminal liability

A person can be brought to criminal liability only if he evaded paying taxes by failing to provide a tax return or other mandatory documents, or by including knowingly false information in them. Moreover, over three years, the debt must be more than 900,000 rubles and the share of unpaid taxes, fees and insurance premiums in it exceeds 10% of the amounts payable.

The punishment decided by the court may be as follows:

— A fine in the amount of 100,000 to 300,000 rubles or in the amount of wages or other income of the convicted person for a period of one to two years. — Forced labor for up to one year. — Arrest for up to six months. — Imprisonment for up to one year.

Trade tax on the territory of Moscow

The trading fee must be determined and paid every quarter. There are no reporting periods for the trade fee. Transfer the calculated amount of the trading fee to the budget no later than the 25th day of the month following the taxable period (quarter).

| Deadlines for payment of trade tax in 2018 | |

| For the fourth quarter of 2021 | No later than 01/25/2018 |

| For the first quarter of 2021 | No later than 04/25/2018 |

| For the second quarter of 2021 | No later than July 25, 2018 |

| For the third quarter of 2021 | No later than October 25, 2018 |

Property tax

The deadline for paying the property tax of organizations in 2021 and the deadlines for paying advances on this tax are established by the laws of the constituent entities of the Russian Federation. Regional authorities also set deadlines for payment of transport tax/advance payments.

As for the deadlines for paying land tax and advance payments thereon, they are established by local regulations.

Accordingly, if there are objects of taxation for corporate property tax, transport tax and/or land tax, the payer needs to familiarize himself with the relevant law in order to avoid untimely transfer of tax/advance payment.

Read also

24.07.2017