Depreciation groups of fixed assets: how to determine in 2021

Express courses Intensive on hot topics at Kontur.School Fixed assets (FPE) of an organization, depending on their useful life (SPI) for profit tax purposes, are assigned to one or another depreciation group (clause.

1 tbsp. 258 of the Tax Code of the Russian Federation). The organization determines the useful life of the OS itself, taking into account the classification approved (Resolution No. 1). In 2021, all depreciation classification groups have changed, except the first. The changes apply to legal relations arising from January 1, 2021.

Most of the amendments are in the subsection “Structures and transmission devices” of the second to tenth groups. The list of fixed assets in the “Machinery and Equipment” subsection of the second and ninth groups has been expanded.

Classifier of fixed assets by depreciation groups with examples of fixed assets: Number of depreciation group Useful life of fixed assets Example of fixed assets belonging to depreciation group 1 From 1 year to 2 years inclusive General purpose machinery and equipment 2 Over 2 years up to 3 years inclusive Pumps for pumping liquids 3 Over 3 years up to 5 years inclusive Radio-electronic communications 4 Over 5 years up to 7 years inclusive Fences (fences) and reinforced concrete barriers 5 Over 7 years up to 10 years inclusive Timber industry structures 6 Over 10 years up to 15 years inclusive Water intake well 7 Over 15 years up to 20 years inclusive Sewerage 8 Over 20 years up to 25 years inclusive Condensate pipeline and main product pipeline 9 Over 25 years up to 30 years inclusive Buildings (except residential) 10 Over 30 years Residential buildings and structures All-Russian Classifier of Fixed Assets (OKOF), which is used to determine depreciation OS group - no changes.

Since January 1, 2021, OKOF has been in effect, approved by order of Rosstandart dated December 12, 2014 No. 2021-st. The same classifier will be in effect in 2021. The classification of fixed assets is a table in which, for each depreciation group, the names of the fixed assets included in it and the corresponding codes of the All-Russian Classifier of Fixed Assets are listed.

For tax accounting purposes, according to the classification of fixed assets, the following is determined:

- depreciation group to which the fixed asset belongs. All depreciable property is combined into 10 depreciation groups depending on the useful life of the property (clause 3 of Article 258 of the Tax Code of the Russian Federation). Depreciation groups are also important in determining the amount of depreciation bonus that can be applied to a specific asset; the useful life must be within the limits established for each depreciation group (Letter of the Ministry of Finance of Russia dated July 6, 2016 No. 03-05-05-01/39563). Choose any period within the SPI, for example the shortest, in order to quickly write off the cost of the fixed assets as expenses (Letter of the Ministry of Finance of the Russian Federation dated July 6, 2016 No. 03-05-05-01/39563).

You can set an entire OS group in the classification. A transcript of the group is presented in OKOF.

Determine the depreciation group of the fixed asset as follows: In the first column of OKOF, find the type of property to which it belongs

Classification of fixed assets. Types (groups) of fixed assets

Home » Accounting » Fixed assets » Classification of fixed assets is an integral element of organizing property accounting at an enterprise. It helps to specify information about certain objects and solves certain problems of the accounting process and management.

Classification of fixed assets involves their grouping according to certain characteristics.

For the purposes of accounting, evaluation, and analysis of property objects, six main criteria for classification can be distinguished. according to natural composition and functions performed (by type) - standard classification.

In accordance with the All-Russian Classifier of Fixed Assets (OK 013-94), approved by Decree of the State Standard of Russia dated December 26, 1994 No. 359 (hereinafter referred to as OKOF), fixed assets are accounted for in the following groups (Table 1).

Table 1 – Classification of fixed assets by type Name of group Code Group composition Buildings (except residential) 11 0000000 Buildings of workshops, plant management, workshops, etc.

The object of classification in this group is considered to be each separate building or extension if it has independent economic significance (warehouse, garage) along with all communications (lighting, heating, ventilation, water and gas supply, elevator facilities, internal telephones, etc.), ensuring normal operation of Structures 12 0000000 Oil and gas wells, bridges, overpasses, roads, mines, sewers, gates, cylinders and tanks, etc. are engineering and construction facilities designed to create the conditions necessary for the performance of certain functions in the production process.

The classification object is a separate structure with all devices Dwellings 13 0000000 Panel houses, buildings and other premises used for housing, historical monuments related to residential buildings Machinery and equipment 14 0000000 - Energy equipment (nuclear reactors, steam engines, turbines, internal combustion engines etc.), which either produce electricity or thermal energy, or convert it into mechanical energy of movement. The object of classification is each individual machine (if it is not part of another object), including its constituent fixtures, accessories, instruments, individual fencing, foundation; — Working machines and equipment (machines, machines, devices) for mechanical, thermal and chemical effects on the object being processed. The object of classification of working machines and equipment is each individual machine, apparatus, unit, installation, etc., including their included accessories, instruments, tools, electrical equipment, individual fencing, foundation; — Measurement and control equipment (scales, pressure gauges, equipment for remote control, alarms, instruments and laboratory equipment, etc., which are intended

Which depreciation group does the computer belong to?

Today, the vast majority of modern entrepreneurs from large and small businesses use computers, laptops, and other means for printing and transmitting information through high-tech communicators.

When purchasing such equipment, the accountant must capitalize them properly and determine the balance group.

We must not forget that the instructional materials on accounting very precisely define what the category of fixed assets is, which also includes computers, both separately and in combination with other technical devices - scanners, printers, modems and other equipment.

What are the fixed assets of a legal entity?

The same Regulations on maintaining primary records contain the following wording:

- The category of fixed assets or the main composition of the main balance sheet items includes a group of assets used for certain purposes of industrial or other production for the production of certain products.

- Providing household services or industrial work.

- Carrying out highly specialized processes, exchanging information and working in a certain direction.

- A category of assets that can be used as an object for lease for a short period with a strictly fixed payment under the contract.

Thus, computers are designed to perform specific work and provide services, both for internal use and as core production activities.

Therefore, it is extremely important to accurately determine the group in which fixed assets of this type should be capitalized and depreciation charges and depreciation amounts should be calculated for certain calendar periods.

How to determine depreciation group?

Initially, in order to accurately determine the depreciation group, it is necessary to consider what depreciation itself is as an accounting and economic category of a legal and accounting nature.

As important as it is to determine which group the fixed asset will be assigned to, depreciation charges will be calculated correctly.

They, in turn, allow the formation of a depreciation fund, where certain funds are accumulated, which are subsequently used to restore certain funds, mechanisms and devices that are intended for carrying out industrial production and services associated with the main activity.

Distribution into groups is carried out in a manner determined by the Accounting Regulations, which is quite simply and clearly stated in the articles and subparagraphs.

Today, there are several accounting groups of fixed assets in accounting. They are defined through the following principles:

- The length of time during which equipment or property can properly serve to achieve the goals of the company, which is determined separately or jointly with the interests of the taxation system. It directly distributes the property complex into depreciation groups, according to the classifier of the type and type of fixed asset.

- Tax legislation includes ten groups of depreciable property . This approach forms the percentages and amount of deductions for the reconstruction and improvement of assets of the depreciation type of property:

- from 1 year to 2 years;

- two or three years;

- from three to five years;

- from five to seven years;

- the fifth from seven to ten years;

- ten - fifteen years;

- fifteen - twenty years;

- from 25 to 30 years;

- tenth – more than 30 years.

The distribution into depreciation groups was carried out clearly and in full accordance with the criteria of moral and material aging of the fixed assets used.

- The period of effective use of a particular enterprise facility can be established within the framework defined by federal laws for the commissioning of fixed assets , their types of reconstruction, moderation and other methods for assessing the need for comprehensive technical re-equipment. This is especially important when there is a possibility of increasing the service life or useful technical use of an object or mechanism.

- According to the conditions for the capitalization of intangible assets, the useful life periods are determined based on the periods of validity of the registered patent or the implementation of a license for the rights to use a particular object. When useful life cannot be determined in this way, depreciation standards are set for an average period of ten years.

- The largest and requiring special attention and accounting is the fifth depreciation group , which includes buildings other than residential buildings, industrial sites without ceilings, thermal and other communications for highways, various types of photographic equipment and other equipment.

- When fixed assets are difficult to attribute to one or another depreciation group , then the useful life is determined based on the technical conditions or recommendations of the manufacturer.

Therefore, a professional accountant must accurately determine all the parameters of the object that needs to be included in the balance sheet.

Accounting for receipt of fixed assets

The receipt of fixed assets in the segment of private businesses or public associations can occur through several methods.

Experts have developed several solutions defined by federal law, and they have combined them into several groups:

- Contributions to the formation of the management company.

- Property purchased from third party companies and other manufacturers.

- Property and equipment manufactured, constructed, and constructed.

- Exchanged, donated for other types of fixed assets.

- Receipt for free use . The main basis and form of receipt are specified in the paragraphs of the donation agreement.

Thus, any type of receipt of funds is an object in order to put it on primary accounting in accordance with the standards of domestic law.

Accelerated depreciation

The accelerated depreciation method can represent an accelerated transfer of the price factor of an object of fixed capital to the cost items of products produced using their assistance.

In the overwhelming majority of cases, domestic instructional materials and literature devoted to tax, economic and accounting systems exclude the presence of clearly defined boundaries in deciphering the concepts of accelerated depreciation mechanisms and numerous ways of its possible calculation.

The essence of the mechanisms is as follows:

- When the accrual of amounts begins to apply, they will be significantly larger than similar amounts for depreciation, which are traditionally accrued at the end of periods of effective operation of objects constituting items from fixed capital.

The section in which you want to enter your personal computer

According to the current federal legislation, namely the Regulations - Resolution of the Cabinet of Ministers of the Russian Federation dated 01.01.2002 N 1, as amended on July 6, 2015 “On the Classification of fixed assets included in depreciation groups”, computer equipment belongs to the third group of the technical-electronic group, including customized personal gadgets.

At the same time, during the process of capitalization, at least ten percent of the original cost of the object is written off simultaneously.

Industrial and household equipment

Industrial equipment are items for special technical purposes. They are used in the implementation of the production process. However, this equipment cannot be classified as equipment or structures.

For example, it can be vacuum cleaners, floor polishers, floor scrubbers, air conditioners and other technical equipment.

In this case, household equipment includes carpet runners, a tape recorder, sports equipment and other items.

- 14 3020000 6 Electronic computer technology

This includes analog and computer systems, computer technology complexes, various complexes of computer technology devices, electronic communication technology and specialized analytical machines.

- 14 3020215 5 Specialized computers

Today they can be keyboard - industrial, and push-button - for the production of calculated and written volumes for management purposes.

- 14 3020216 8 Control computers

A computer complex for remote control of technology systems and remote access to certain controlling technological associations of equipment fragments.

Source: https://pozvoniuristu.ru/business/amortizacionnaya-gruppa-kompyutera.html

Features of depreciation of office equipment

1949 Page Contents One of the key issues that an accountant needs to resolve when registering depreciable equipment is determining the useful life of the object.

In 2021, an updated OS classifier is in effect, according to which the depreciation group of equipment, including office equipment, is determined.

Despite the fact that the new classification rules are as close as possible to the realities of today, accountants still have many questions about which depreciation group to include this or that equipment purchased for the office.

Of great practical importance is the choice of the method of depreciation of equipment for accounting and accounting purposes, as well as the possibility of classifying this or that office equipment as inventory. Classification by depreciation groups is necessary for tax purposes and is associated with the process of accounting for costs included in tax calculations under the appropriate taxation system.

We recommend reading: Registry office to submit an application for divorce in St. Petersburg

In accounting, depreciation can be set arbitrarily, but in practice they are guided by the same standards as for NU. It is known that for the purposes of NU, equipment that is used in the production process for more than a year and has a cost of more than 100 thousand is considered depreciable.

rub., in BU the cost limit is 40 thousand rubles. and the same period of use. In tax and accounting, various methods of depreciation are defined.

There are only two of them in NU - linear and nonlinear. In accounting, in addition to the linear method, reducing balance methods are used, based on the sum of the number of years of use, in proportion to the volume of production. In practice, when depreciating office equipment, the same method is often adopted for NU and BU - linear, so as not to account for additional differences that arise.

Office equipment's cost often falls in the range of 40-100 thousand rubles, and the question arises of how best to take it into account for the purposes of accounting and accounting.

There are two ways out of this situation:

- Write off such office equipment immediately upon commissioning in the NU and charge depreciation on it after registration in the BU. The method is not very convenient and involves the occurrence of temporary differences that are subject to additional accounting.

- Write off as expenses in NU, but not at once, but in parts (this opportunity is provided to the taxpayer by Article 254 of the Tax Code of the Russian Federation, clause 1, clause 3). At the same time, accrue depreciation for accounting purposes. Equipment that costs less than 40 thousand rubles can be written off as expenses immediately, without depreciation, both in tax and accounting.

When choosing a code according to OKOF and a depreciation group of equipment according to the OS Classifier, it is important to remember that the equipment must be a single system, a single device that collectively performs certain office functions. A depreciation group is selected in which the component parts of the device are included by the legislator to the maximum extent possible.

The depreciation policy, due to its heterogeneity and many nuances, must be spelled out in the accounting policy as its important component. It is impossible to imagine a modern office without a computer.

The cost of modern PCs of various modifications can reach the marginal cost of classifying an object as fixed assets, and, therefore, such office equipment is depreciated.

New and old! Classifier of fixed assets (OKOF) 2021

See also: .

Attention! Since 2021, a new Classifier of Fixed Assets (OKOF) has appeared, with new codes - OK 013-2014 (SNA 2008)!

For fixed assets put into operation from 2021, useful lives will have to be determined using new codes OK 013-2014 (SNA 2008) and depreciation groups. The deadlines for OS adopted before 2021 will remain in accordance with the old classifier and, if according to the new classifier the OS belongs to another group of the organization, then the deadlines will not have to be changed.

Download for free: Word (318kb) Download for free: Word (389kb) Download for free: Excel xls (2.7 mb) - old and new codes in one file.

The fixed asset classifier is used to assign a depreciation period for material assets and uses the All-Russian Classifier of Fixed Assets (OK 013-94) (OKOF) codes.

From January 1, 2021, the limit on the value of fixed assets in tax accounting has been increased to 100,000 rubles (from 40,000 rubles). For accounting, the limit remains 40,000 rubles. In accordance with the law, movable property registered as fixed assets from January 1, 2013 is not recognized as an object of taxation by the corporate property tax.

However, from 2021, regional authorities themselves will regulate this by local laws and, if the benefit is not spelled out, then it will not exist. (Clause

58 Art. 2 of the Law of November 30, 2021 No. 401-FZ). Individual entrepreneurs and organizations using the simplified tax system, UTII, PSN, Unified Agricultural Tax will continue to be exempt from movable property tax (, ,). Below you can compare the new and old classifier.

If you purchased an OS from another company, then the depreciation period should be calculated taking into account the period that it served there (letter of the Ministry of Finance of Russia dated August 11, 2021 No. 03-03-06/1/51573). You can immediately write off as expenses: For depreciation groups 1,2,8,9,10 - 10%, depreciation groups 3-7 - up to 30% of the original cost () It is often more profitable to use non-linear depreciation () Attention, since 2017 a new Classifier of basic funds (OKOF), with new codes - OK 013-2014 (SNA 2008)!

For fixed assets put into operation from 2021, useful lives will have to be determined using new codes OK 013-2014 (SNA 2008) and depreciation groups. The deadlines for OS adopted before 2021 will remain in accordance with the old classifier and, if according to the new classifier the OS belongs to another group of the organization, then the deadlines will not have to be changed.

GOVERNMENT OF THE RUSSIAN FEDERATION DECISION of January 1, 2002

N 1 ON THE CLASSIFICATION OF FIXED ASSETS INCLUDED IN DEPRECIATION GROUPS List of amending documents (as amended.

Decrees of the Government of the Russian Federation dated 07/09/2003 N 415, dated 08/08/2003 N 476, dated 11/18/2006 N 697, dated 09/12/2008 N 676, dated 02/24/2009 N 165, dated 12/10/2010 N 1011, dated 06.0 7.2015 N 674, dated 07/07/2016 N 640) In accordance with Article 258 of the Tax Code of the Russian Federation, the Government of the Russian Federation decides: 1. Approve the attached Classification of fixed assets included in depreciation groups.

The paragraph is no longer valid as of January 1, 2021.

Office equipment and what it includes

› However, when mentioning all equipment of the organization that does not relate to machines, machines, mechanisms, etc. and is intended for use in the process of administrative management or in the process of engineering work, it is customary to use the term “office equipment”.

This concept includes computers, printers, scanners, telephones, calculators, shredders, copying equipment, fax machines, projectors and other office tools. Equipment for drawing work, plotters, laminators, hole punchers, mechanical pencil sharpeners, stamps, brochure makers and others are added to the list, calling it “small office equipment.” This situation arose due to the obsolescence of the specified classifier.

But an accountant, when deciding what applies to office equipment in accounting, must be guided by regulatory documents. Therefore, until 2021, the following should be classified as office equipment:

- conference equipment (microphones, projectors, screens, etc.),

- shredders,

- typewriters,

- automated telephone exchanges ensuring the operation of offices,

- banknote counters and detectors,

- copying equipment (not connected to the computer),

- duplicating equipment (not connected to the computer),

- calculators,

- pneumatic delivery device, etc. autonomous office equipment.

- telephones (wired and cellular),

According to the same standards, the following cannot be classified as office equipment:

- communicators,

- printers and MFPs connected to a computer,

- smartphones, etc.

- tablets,

Its standards also contain a subsection that includes information equipment. But the term “office equipment” is excluded from it, and computers and peripheral devices for them are separated into a separate subsection.

However, the list of what previously belonged to office equipment remains.

It has been added to the group in edited form

“Other machinery and equipment, including household equipment, and other objects”

under code 330.28.23. Therefore, starting from 2021, the answer to questions about what office equipment is and what belongs to it is mainly determined by the list in the classifier of fixed assets, marked with this code. Internal documents To minimize the likelihood of claims from tax authorities, establish the obligation to ensure normal working conditions for employees, in particular, equipping premises with an air conditioning system in: - internal labor regulations; — regulations on labor protection; -instructions on labor protection and safety precautions; - collective agreement.

The documents must refer to the norms of the Labor Code and SanPiN discussed above. Insuring yourself to the maximum If you want to insure yourself to the maximum, you can measure the temperature in the office premises.

To do this, go through the following steps: 1. Issue an order to create a commission to measure temperature and draw up a protocol on the measurement results.

2. Select a day for measurements. In fact, each of them can be used independently, without connecting to computer technology.

Classifier of fixed assets by depreciation groups 2021

→ → Current as of: April 22, 2021

To calculate the amount of depreciation of fixed assets (FPE), it is necessary to establish not only the depreciation method, but also to determine the useful life of a particular object. This period, as a general rule, is determined by the Government-approved Classification of fixed assets included in depreciation groups.

We will tell you more about the Classifier in our consultation.

The classification of fixed assets included in depreciation groups has been approved.

From 01/01/2017, the updated Classifier () is in effect. The need to change it was caused by the entry into force on 01/01/2017. Let us recall that in the Tax Classifier, types of fixed assets are classified into depreciation groups in accordance with their OKOF codes. Then changes were made to the Classifier. And although they were approved only in April, they apply to legal relations that arose from 01/01/2018.

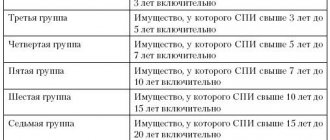

The current Classification of fixed assets by depreciation groups also provides for the distribution of fixed assets into 10 groups. We present these groups with an indication of their corresponding useful life and examples of OS objects belonging to such groups.

Depreciation group Useful life Examples of fixed assets 1 >1 year, but ≤ 2 years - hand and mechanized construction and installation tools; — drilling machines; — pneumatic motors, rotary pneumatic motors, pneumatic turbines 2 >2 years, but ≤ 3 years — other office machines, including personal computers and printing devices for them; servers of various performance; network equipment of local computer networks; data storage systems; modems for local networks; modems for backbone networks; — cargo-passenger lifts; — facilities for sports and recreation 3 >3 years, but ≤ 5 years — sheet-fed offset copying machines for offices; — gas well for production drilling; - especially small and small buses up to 7.5 m long inclusive 4 >5 years, but ≤ 7 years - buildings made of film materials (air-supported, pneumatic frame, tent, etc.); mobile all-metal; mobile wood-metal; kiosks and stalls made of metal structures, fiberglass, pressed plates and wood; — trucks, road tractors for semi-trailers (general purpose vehicles: flatbeds, vans, tractors; dump trucks); - horses and other live equine animals 5 >7 years, but ≤ 10 years - production areas with coatings; — gas turbines, except turbojet and turboprop; - large class passenger cars (with an engine displacement of over 3.5 l) and high class 6 >10 years, but ≤ 15 years - gas distribution network; — fishing vessels, fishery ships and other vessels for processing or preserving fish products; — passenger hydrofoil sea and sea hovercraft 7 >15 years, but ≤ 20 years — wooden, frame and panel buildings, container, wood-metal, frame-cladding and panel buildings,

We recommend reading: Contract between individuals when hiring

Mobile phone OKOF 2021 depreciation group

- railway flat cars 10 >30 years - buildings, except those included in other groups (with reinforced concrete and metal frames, with walls made of stone materials, large blocks and panels, with reinforced concrete, metal and other durable coatings);

We recommend reading: Who is entitled to a social package for pensioners in 2020

The most widespread practice is to use a general standard based on dividing fixed assets into single depreciation groups. The most detailed classification, logically related to grouping by age, by natural material, is called the OKOF classification.

Depreciation groups of fixed assets – 2021

→ → Current as of: January 31, 2021 Fixed assets of an organization, depending on their useful life, belong to one or another depreciation group for profit tax purposes (). The useful life of the asset is determined by the organization itself, taking into account the special classification approved by the Government of the Russian Federation.

In 2021, the Classification approved by .

In accordance with this Classification, all fixed assets are divided into 10 depreciation groups. Please note that the latest amendments to the Classification came into force retroactively and apply to legal relations that arose from 01/01/2018. The 2021 classification of fixed assets by depreciation groups is as follows: Number of depreciation group Useful life of fixed assets Example of fixed assets belonging to the depreciation group First group From 1 year to 2 years inclusive General purpose machinery and equipment Second group Over 2 years to 3 years inclusive Pumps for pumping liquids Third group Over 3 years up to 5 years inclusive Radio-electronic communications equipment Fourth group Over 5 years up to 7 years inclusive Fences (fences) and reinforced concrete fences Fifth group Over 7 years up to 10 years inclusive Timber industry structures Sixth group Over 10 years up to 15 years inclusive Water intake well Seventh group Over 15 years up to 20 years inclusive Sewerage Group Eight Over 20 years up to 25 years inclusive Condensate pipeline and main product pipeline Ninth group Over 25 years up to 30 years inclusive Buildings (except residential) Tenth group Over 30 years Residential buildings and structures To understand which depreciation group your fixed asset belongs to, you need to find it in the Classification.

Having found it, you will see which group this OS belongs to. If your OS is not named in the Classification, then you have the right to independently determine the useful life of this property, focusing on the service life specified in the technical documentation or the manufacturer’s recommendations. The established SPI will tell you which depreciation group your OS falls into.

Also read:

Accountant forum: Share:

Subscribe to our channel at

Office equipment: shock-absorbing group

→ → Current as of: July 27, 2021

Along with office equipment, it is one of the most common groups of fixed assets for many organizations. We will tell you about the depreciation groups of equipment and their useful life in accounting in our material.

For income tax payers, a fixed asset item falls into one or another depreciation group depending on its useful life. This period is established by the organization on the date of commissioning of the fixed asset object.

In this case, it is necessary to be guided by the Classification of fixed assets included in depreciation groups (,). The Tax Classification lists, in particular, the following types of fixed assets that relate to office equipment: Name of fixed assets Depreciation group Useful life Personal computers and printing devices for them; servers of various performance; network equipment of local computer networks; data storage systems; modems for local networks; modems for backbone networks II Over 2 years up to 3 years inclusive Machines for sorting and counting coins, banknotes and lottery tickets; sheet-fed offset copying machines for offices III Over 3 years up to 5 years inclusive Office machines and equipment, except computers and peripheral equipment IV Over 5 years up to 7 years inclusive The organization establishes the useful life of office equipment in accounting independently.

To do this, it takes into account both the expected physical wear and tear and the expected period of use. An organization may provide for the use of tax classification when determining the useful life of fixed assets, incl. and office equipment, in accounting.

Also read:

Accountant forum: Share:

Subscribe to our channel at

New okof year for an office chair shock-absorbing group

In grouping 330.00.00.00.000 “Other machinery and equipment, including household equipment, and other objects,” codes have appeared that can be used to classify rafts, furniture for offices and retail establishments, as well as other metal furniture, musical instruments, sports equipment, equipment and other equipment, swimming pools. Separately, please note that now the issue of classifying office furniture and other metal furniture with the OKOF code is closed.

We recommend reading: Tax on the Sale of an Apartment Received by Inheritance for Pensioners in 2021

Articles, comments, answers to questions: OKOF furniture Answer Office furniture belongs to the Fourth depreciation group. Accordingly, the useful life of furniture can be set in the range from 5 years and 1 month to 7 years.

Office equipment: what applies to it

→ → Update: June 26, 2021

One of the areas of application of the All-Russian Classifier of Fixed Assets is accounting in institutions. According to OKOF, the accountant must determine the asset code and reflect it on the appropriate account.

Contained the term “office equipment”. What relates to it was deciphered in the grouping with codes 14 301 0000 – 14 301 0440. We will consider further what the situation is after the new classifier comes into force.

In the OK 013-94 classifier, the concepts of computer and office equipment are separated. They are both included in the “Machinery and Equipment” section, but each has its own subsection.

However, when referring to all equipment of the organization that does not relate to machines, machine tools, mechanisms, etc. and is intended for use in the process of administrative management or in the process of engineering work, it is customary to use the term “office equipment”.

This concept includes computers, printers, scanners, telephones, calculators, shredders, copying equipment, fax machines, projectors and other office tools. Equipment for drawing work, plotters, laminators, hole punchers, mechanical pencil sharpeners, stamps, brochure makers and others are added to the list, calling it “small office equipment.”

The confusion of the two concepts occurs due to the fact that auxiliary equipment for computer technology, such as a scanner, barcode reader, printer, display, electronic graphic board, drawing machine, etc., according to the rules of the OK 013-94 classifier, are taken into account together with the computer as a single object of classification. In fact, each of them can be used independently, without connecting to computer technology. This situation arose due to the obsolescence of the specified classifier.

But an accountant, when deciding what applies to office equipment in accounting, must be guided by regulatory documents.

Therefore, until 2021, the following should be classified as office equipment:

- pneumatic delivery device, etc. autonomous office equipment.

- telephones (wired and cellular),

- banknote counters and detectors,

- shredders,

- conference equipment (microphones, projectors, screens, etc.),

- calculators,

- automated telephone exchanges ensuring the operation of offices,

- typewriters,

- duplicating equipment (not connected to the computer),

- copying equipment (not connected to the computer),

According to the same standards, the following cannot be classified as office equipment:

- printers and MFPs connected to a computer,

- tablets,

- communicators,

- smartphones, etc.

This division is determined by information from the subsection “Means of mechanization and automation of managerial and engineering labor,” which allows us to determine what belongs to office equipment. The list of what should be considered computer technology is given in the subsection “Electronic computing technology.” According to the OK 013-94 classifier, both of these types of equipment belong to information equipment.

Meaning of the OKOF code for the printer

When purchasing a new office printing device, the question of how to place it on the balance sheet of the enterprise certainly arises. Confusion often arises regarding MFPs, since these devices simultaneously include a printing device, a fax machine, and a scanner.

The OKOF code for a printer and scanner within one device is selected according to the maximum depreciation group of individual components, in this case we are talking about blueprinting equipment.

Next, we describe in detail how OKOF is selected for new multifunctional office equipment, including the 2021 version of the classifier.

Okof - features and principles of code selection

OKOF is an all-Russian classifier of fixed assets, which is used to account for fixed assets of an enterprise. Taken together, the use of certain codes helps government statisticians assess the nature and quality of enterprise property.

Laser printer

Laser printers and MFPs are classified as office equipment; their service life is 3-5 years.

Timely write-off of depreciation cost allows the company to timely generate funds for the purchase of new equipment.

The nature of the decrease in the value of fixed assets is described using the rules by which depreciation is carried out, where OKOF is the normative source.

Computers and printers - second depreciation group

According to the classifier of fixed assets, any digital printing devices that are computer peripherals can be classified into the following categories:

- OKOF code for a laser printer (from January 1, 2021) is 320.26.2, the category “Computers and peripheral equipment” includes personal computers, various peripheral devices, including printers. Code 320.26.20.13 is used if the printer has a central processor (by default on all modern models).

- OKOF code until January 1, 2021 – 14 3020000, category “Electronic computing equipment”.

On January 1, 2021, a new classifier of fixed assets came into force, it is also known as OKOF-2.

Accordingly, new coding for fixed assets should be used, while the old classifiers continue to be valid. For quick translation, the OKOF-2 converter is used.

At the same time, the new version also lacks the concept of a multifunctional device, and difficulties arise with coding the equipment.

MFU - third depreciation group

To register an MFI on its balance sheet, the tax regulator recommends using one of the options of the third depreciation group. The device is evaluated as a whole and individually, so that the maximum amount of depreciation is selected as a result.

Due to the lack of multifunctional devices in the classifier of fixed assets (2021 inclusive), to select OKOF its components are used: printer, scanner, copier and fax, if available, which subcategory should be selected:

- Printing devices belong to depreciation group II - 320.26.20.13;

- If a specialized device is installed that does not have a processor or other features, it may be classified as 330.28.99 “Special-purpose equipment not included in other groups” or 330.28.23.2 “Office equipment” not related to computer peripherals;

- Copiers and blueprinting equipment are classified in depreciation group III - 330.28.23.21, this subcategory includes contact copiers, including thermal copiers;

- Faxes also belong to the office equipment of the second group - 320.26.30.23 “Other telephone devices.”

Accordingly, the resulting OKOF code for the printer and MFP is 330.28.23.21. The depreciation life of a copier is 2-3 years.

Conclusion

Why is correct group selection required, and what coding should be done if not explicitly stated? We are talking about writing off depreciation value. According to the third category, equipment is written off within 2-3 years.

On the one hand, this is true in large companies. On the other hand, modern peripherals are designed to operate for at least 3 years.

The manager of the enterprise will not encourage the write-off of expensive color laser printing equipment with a scanner from fixed assets. What conclusion can be drawn from this?

The fact is that a multifunctional device can be classified as a computer peripheral and be operated according to the classifier for 3-5 years.

With high work intensity in large offices, you can completely use the third category and write off a multifunctional black-and-white laser printing device with a copier within 2 years, otherwise you need to use subcategory 320.26.20.

13 and write off, for example, an infrequently used color printing device within 5 years. There is no further clarification in the new 2021 version.

Source: https://printergid.ru/expluataciya/kod-okof