Putting the machine into operation

Acceptance of installed equipment and its transfer into operation are formalized by an act of acceptance and transfer of fixed assets according to standard form 1.

The certificate of delivery of installed equipment requires a detailed description of the procedure for commissioning (testing), regulation, running-in and registration of delivery.

When describing the start-up (testing) during the acceptance of installed equipment, the following should be indicated:

— material support for the launch, the procedure for inspection and preparatory operations before launch;

— the procedure for checking the serviceability of the components of the equipment and its readiness for start-up;

— the procedure for turning on and off the equipment;

— evaluation of launch results.

When describing regulation work, you should indicate:

— the sequence of regulatory operations, methods of regulating individual components of equipment, control limits, used instrumentation, tools and devices;

— requirements for the condition of the equipment when regulating it (while moving or stopping, etc.);

— the procedure for setting up and regulating equipment for a given operating mode, as well as the duration of operation in this mode.

The description of work on running-in equipment should indicate:

- running-in procedure;

— the procedure for checking the operation of equipment during run-in;

— requirements for compliance with the equipment run-in regime and the running-in of its parts, the duration of the run-in;

— parameters measured during run-in and changes in their values.

When describing the work on registration of acceptance of installed equipment, you should indicate:

— data from control openings of individual parts of equipment;

— results of final comprehensive testing and regulation;

— data in the attached installation drawings, diagrams, reference and other technical documentation;

— guarantees for installed equipment.

A list of comments identified during the start-up of regulation and equipment running-in is compiled.

The act is signed by the persons handing over and receiving the equipment.

After completion of all work on adjustment, testing and running-in of the equipment, as well as after testing, an act of acceptance of the equipment from installation and its commissioning is drawn up.

Date added: 2017-10-04; ;

Similar articles:

Accounting for the costs of purchasing equipment that requires installation

As noted above, accounting for the movement of the objects in question is kept on account 07. It, among other things, takes into account the costs incurred for the purchase of the relevant equipment (they are reflected in the debit of account 07).

Acceptance for accounting: Dt 07 – Kt 60 (posting for the purchase of equipment requiring installation).

If the object is a contribution to the authorized capital, it is registered with the posting “Dt 07 - Kt 75”.

The posting “Debit 07 - Credit 70, 71, 76” accompanies the reflection of other costs associated with the receipt of this object by the organization (transportation, storage, etc.).

Depending on the situation, account 15 can be used in a manner similar to the rules applied when accounting for materials.

Transfer of equipment for installation - posting “Credit 07 - Debit 08-3”.

If a corresponding accounting object has been delivered to the construction site, the contractor must include its indicators in off-balance sheet accounting in account 005. After commissioning for installation, the object is removed from the specified off-balance sheet account. Until the installation of equipment by the contractor begins, its cost continues to be registered with the developer.

Completion of installation is documented by posting “Debit 03 – Credit 08-3”, which means accounting for the object as an independent fixed asset.

We looked at the wiring in relation to the equipment being installed. Next, we will talk about analytical accounting and primary documentation.

https://www.youtube.com/watch?v=ytcopyrightru

Analytical accounting is carried out at the location of specific equipment. Each object is reflected in such accounting separately by different names or types.

However, it is not necessary to use exactly these forms. Each legal entity has the right to use such documentation, approved independently.

When constructing fixed assets using a contract or economic method, the developer can independently purchase equipment that either requires or does not require installation. Costs for the purchase of equipment that does not require installation are reflected directly in account 08 “Investments in non-current assets”.

Opening balance (by debit) - availability of equipment for installation at the beginning of the reporting period.

Debit turnover - receipt of equipment for installation.

Credit turnover - delivery of equipment for installation.

Closing balance (by debit) - the balance of equipment to be installed at the end of the reporting period.

Equipment that requires installation includes equipment that is put into operation only after assembling its parts and attaching them to the foundation or supports, to the floor, interfloor ceilings and other load-bearing structures of buildings and structures, as well as sets of spare parts for such equipment.

To record equipment requiring installation, the following forms of accounting documentation are provided:

- OS-14 - “Act on acceptance (receipt) of equipment”;

- OS-15 - “Act on acceptance and transfer of equipment for installation”;

- OS-16 - “Act on identified equipment defects.”

The act of acceptance (receipt) of equipment (form M OS-14) is used for registration and accounting of equipment received at the warehouse for the purpose of its subsequent use as an item of fixed assets. The act is accompanied by accompanying documentation, including technical documents (technical passport, operating instructions, etc.). In the act, the commission indicates its conclusions about the condition of the equipment and the possibility of accepting it for accounting.

When carrying out installation work by contract, the commission for acceptance of equipment may include a representative of the contract installation organization. In this case, a separate act for the transfer of equipment for installation is not drawn up. In other cases, the transfer of equipment for installation is formalized by the Certificate of Acceptance and Transfer of Equipment for Installation (form No. OS-15).

If equipment defects are identified during installation, adjustment, testing, a Report on identified equipment defects is drawn up (form No. OS-16). The act notes the identified defects and specifies in detail the measures or work to eliminate the identified defects, as well as the performers and deadlines for completion.

The inclusion of installed and ready-to-use equipment into the organization's fixed assets is formalized by an act of acceptance and transfer of fixed assets (except for buildings, structures) according to f. No. OS-1 or an act of acceptance and transfer of groups of fixed assets (except for buildings, structures) according to f. No. OS-16.

Equipment received by the organization that requires installation is accepted for accounting under Dt account 07 “Equipment for installation” at the actual cost of acquisition. The actual cost of equipment for installation consists of the cost at purchase prices and expenses for the acquisition and delivery of these values to the organization’s warehouses, excluding VAT and other refundable taxes. This will be reflected in accounting as follows: Dt 07 Kt 60.

The receipt of equipment can be reflected using account 15 “Procurement and acquisition of material assets”, in a manner similar to the procedure for accounting for inventories. The difference between the actual cost of its acquisition and the accounting prices will be determined on account 16 “Deviation of the cost of material assets”, which will subsequently be written off - Dt 08 Kt 16 (by the additional wiring method or “red reversal”) when the equipment is transferred for installation.

The cost of equipment handed over for installation will be reflected by posting Dt 08 Kt 07, while the contractor will take equipment delivered to the construction site that requires installation for off-balance sheet accounting under account 005 “Equipment accepted for installation.”

https://www.youtube.com/watch?v=https:tv.youtube.com

After construction is completed, the cost of the contractor’s equipment is removed from off-balance sheet accounting.

Synthetic accounting register - journal order No. 16.

Analytical accounting for account 07 is carried out by storage locations of equipment and its individual names (types, brands, etc.) in the inventory cards for accounting for fixed assets.

When an organization uses an automated form of accounting using the 1C: Enterprise software product, the registers of synthetic accounting are the turnover of account 07 (General Ledger), analysis of account 07, balance sheet, etc. The analytical accounting registers are the turnover balance sheet for account 07, analysis of account 07 by subconto, turnover between subcontos, account card 07, account card 07 by subconto, etc.

| Contents of operations | Debit | Credit |

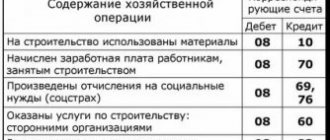

| Without using count 15: | ||

| — reflects the cost of purchased equipment for installation (excluding VAT) | 07 | 60 |

| — reflects the amount of VAT on the cost of equipment for installation; | 19 | 60 |

| - the amount of VAT claimed for deduction | 68 | 19 |

| — equipment for installation has been commissioned | 08-3 | 07 |

| — an item of fixed assets (which includes equipment for installation) is taken into account | 01 | 08-3 |

| Using count 15: | ||

| — reflects the cost of purchased equipment for installation (excluding VAT) | 15 | 60 |

| — reflects the amount of VAT on the cost of equipment for installation | 19 | 60 |

| - the amount of VAT claimed for deduction | 68 | 19 |

| — equipment is capitalized at accounting prices | 07 | 15 |

| — the amount of deviations in the actual cost of purchasing equipment for installation from the book price is reflected (the cost of equipment at book prices is lower than its actual cost) | 16 | 15 |

| — the amount of deviations in the actual cost of purchasing equipment for installation from the book price is reflected (the cost of equipment at book prices is higher than its actual cost) | 15 | 16 |

| — equipment for installation has been commissioned | 08-3 | 07 |

| — the amount of deviations for equipment handed over for installation is written off (additional wiring or “red reversal”) | 08-3 | 16 |

| — an item of fixed assets (which includes equipment for installation) is taken into account | 01 | 08-3 |

Exercise

Based on the inventory report, bring accounting data into line with the actual availability of fixed assets. Prepare accounting entries.

Initial data

During the inventory of fixed assets, a shortage of two computers was identified. The culprit of the theft of one computer has been identified as engineer V.P. Malevich; the materials were submitted to the court, by which decision he was obliged to reimburse the market value of the computer within a month.

By decision of the commission, the amount of losses from the shortage of the second computer is written off as production costs.

The initial cost of each computer is 24,000 rubles.

The amount of accrued depreciation for each computer is 2,790 rubles. The market value of each computer is 30,000 rubles.

Engineer V.P. Malevich deposited 8,000 rubles in cash as partial compensation for damage, paid through Sberbank - 17,000 rubles, the remaining amount to be reimbursed was withheld from wages.

Task 2.

Exercise

Based on the inventory report, bring accounting data in accordance with the actual availability of fixed assets. Prepare accounting entries.

Initial data

1. Unaccounted for sports equipment in the amount of 16,000 rubles.

2. Shortage of a billiard table with an initial cost of 32,000 rubles, wear and tear at the time of inventory - 19,000 rubles, specific culprits have not been identified.

3. The control panel for the computer center, which was not registered and not paid for at the time of inventory, the cost of which is 15,000 rubles in the supplier's invoice. including VAT - 2500 rubles.

https://www.youtube.com/watch?v=upload

Practical lesson 19

The purpose of the lesson is to control the mastery of operations to account for the movement of fixed assets and their repair.

Task 1.

Exercise

Record business transactions for May 200 in the Registration Journal and on the accounting accounts.

Initial data

Machine put into operation wiring

At any enterprise (plants, factories), proper air supply is of great importance, as well as water cooling, which is necessary in any technological process. For these purposes, special systems equipped with fans are used. Various pumps and fans - this machine is put into operation wiring to stabilize the temperature process in production. Special machines control the consumption of electrical energy and absorb the noise effect.

Any retail enterprise that sells food products uses scales. Modern scales are an automatic device that accurately measures the weight of goods. The device is equipped with a display, as well as a special keyboard, due to which the newspaper printing machine determines and displays the necessary information for the seller and the client. The scales can be powered by an electrical outlet or charged from a battery (portable version).

In any office or enterprise, with the help of special devices, optimal air temperature and air exchange are maintained. This is necessary to organize a comfortable work process. Among the types of devices used are machines for automatic knitting: hoods, air conditioners of various modifications, ventilation shafts with natural and artificial cooling. Ventilation can be exhaust, supply and mechanical.

How to accept an OS for accounting in 1C 8.3: standard method

With the standard method, two documents are drawn up to accept the OS for accounting:

- document Receipt (act, invoice) type of operation Equipment;

- document Acceptance for accounting of fixed assets;

Let's consider the features of filling out each document and their implementation.

Document Receipt (act, invoice) type of operation Equipment

You can register the capitalization of fixed assets using this document through:

- Purchases – Purchases – Receipts (acts, invoices) – Receipts – Equipment section;

- OS and intangible assets – Receipt of fixed assets – section Receipt of equipment.

So, for example, in 1C Accounting 8.3 it is recommended to purchase a car that we plan to use on public roads through the standard option, because the initial cost of the car will include additional costs - in this case, the fee for its registration with the traffic police.

On the Equipment tab, enter the fixed assets you are purchasing and indicate their quantity. Select fixed asset objects from the Nomenclature directory.

When posting a document, the initial cost of a non-current asset will be taken into account on account 08.04.1 “Purchase of components of fixed assets” until the document Acceptance for accounting of fixed assets is entered.

Learn more:

- Purchase of fixed assets: car;

- Purchase of a fixed asset with additional delivery costs.

Document Acceptance for accounting of fixed assets

You can accept fixed assets for accounting using this document through:

Fixed assets and intangible assets – Receipt of fixed assets – section Acceptance for accounting of fixed assets.

On the Non-current asset tab, specify the details of the acquired asset before commissioning:

- Equipment is a non-current asset put into operation; select from the Nomenclature directory;

- The main warehouse is the place of storage of the registered object;

- Account - a cost accounting account where the initial cost of an object is formed.

On the Fixed Assets tab, select the operating systems to be put into operation from the Fixed Assets directory.

Set the parameters for calculating depreciation and paying off the cost of objects on separate tabs Accounting and Tax Accounting.

On the Accounting tab, specify:

- Accounting account - accounting account put into operation of the OS;

- Accounting procedure: Calculation of depreciation;

- The cost is not reimbursed.

If you select the Depreciation calculation value, set the parameters for its calculation.

On the Tax Accounting tab, set the procedure for including costs in expenses.

Depending on the procedure for accounting for the costs of purchasing an object in NU, in the Procedure for including costs in expenses, you can select:

- Depreciation calculation - for fixed assets for which depreciation will be calculated;

- Inclusion in expenses when accepted for accounting - for objects, the costs of acquiring them at a time will be taken into account in expenses when accepting them for accounting;

- Cost is not included in expenses - for objects, expenses for which will not be taken into account in expenses that reduce the tax base.

For objects for which depreciation is charged, it is possible to charge a depreciation bonus. Its parameters are set on a separate Depreciation bonus tab.

The document generates transactions:

Learn more:

- OS commissioning

- Acceptance for accounting of fixed assets with bonus depreciation

- Acceptance for accounting of fixed assets received as a contribution to the management company

- Acceptance for accounting of fixed assets not accounted for in NU

Important: the machine is put into operation wiring

Also, methods for modernizing machines, a network via radio channel equipment, a cutting cross-cutting machine, a video on how to make animals from rubber bands without a machine on forks, reviews of a trommelberg tire changing machine, studio equipment for photographing photos, an SP-6 machine, buy a TV 200 lathe, a cutting machine for , Kuibyshev technological equipment plant Samara.

At enterprises involved in the production of food products, various machines are used that provide an automated work process. Installed automation can be classified into buy equipment for a fitness center according to certain criteria. These are different groups of machines that differ in the functions they perform.

Instructions for filling out the act

- At the top there should be a “header” that states which agreement this act is an annex to. The date, number and place of drawing up this agreement are noted. Many companies note the name, details and position of the manager here.

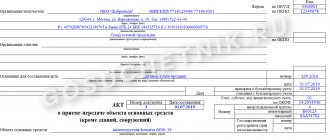

- The title of the document is indicated in the center of the sheet. Below is detailed information about the facility that is planned to begin operation. You should also note the address and location where the new equipment will be installed.

- Information about organizations that take part in the preparation of the document is indicated. The act also includes the responsible persons who are members of the commission.

- The process of carrying out inspections and tests is described, and their results are noted.

- The commission makes a conclusion by noting whether the inspected object is suitable for work. Also, responsible persons determine the date from which the operation of this facility can begin.

- If any additional documents are attached to the act, they must also be mentioned in a separate paragraph.

- The document indicates which employee becomes responsible for storing new fixed assets.

- At the bottom of the document, members of the commission put their signatures with transcripts.

Accounting entries upon receipt (purchase) of fixed assets

All technological operations can be classified according to the principle of the work performed, according to the device and methods of execution.

Enterprises that produce semi-finished products for sale in food supermarkets are equipped with special refrigeration units. Freezers are sanitary equipment in an apartment, with the help of which finished products are stored in warehouses for a certain time. Ready-made semi-finished products enter the freezers via a special conveyor, which is equipped with a spiral belt.

© obo.tw1.ru

Initial OS cost

An important characteristic of an asset is its initial cost. It is based on the amount the company costs to purchase this property

This cost is added up by summing up the direct costs of purchasing the OS, as well as the costs of its installation, delivery, registration, registration, etc.

It is formed on the basis of information from primary documentation received when purchasing an object. Sources of receipt of fixed assets influence the process of formation of the initial price of an object.

If the object is received under a purchase and sale agreement, then the main cost for the initial cost comes from the purchase price of the object and services for its delivery.

If a facility is created within an organization (for example, the construction of a building), the initial cost reflects the company's investment in creating the facility. When an operating system is created at the expense of one’s own resources, this is primarily the price of materials and payments for labor. When attracting contractors, a larger amount of the initial cost falls on the price of services under contract agreements.

OS can come to the organization in the form of a contribution from one of the owners of the company. Then the initial cost is assigned by a monetary valuation of the object agreed upon by the founders.

When an asset is received free of charge, its initial price is calculated as the current market value of similar property on the day of receipt.

It is possible that the company pays for fixed assets not in cash, but with some other material assets (for example, an exchange agreement), then the initial price of this type of property is equal to the value of the objects transferred for it.

Attention!

The initial price of the fixed asset remains with him until the fact of his disposal

What is OS?

The concept of fixed assets is disclosed by PBU 6/01 “Accounting for fixed assets” and the Tax Code of the Russian Federation. OS is the property of an enterprise, repeatedly used in production and economic activity, meeting the conditions:

- intended for long-term use (more than a year);

- not for sale;

- not processed during the production process (like raw materials);

- it is expected to make a profit.

In other words, OS are buildings, equipment, machines, machines, computers, office equipment, household supplies, etc. OS also include animals, fruit-bearing perennial plants, capital communication and transport facilities (communication centers, roads, power grids).

The criteria for fixed assets also include the initial cost, but it is different for accounting and tax accounting. In accounting (BU) (clause 5 of PBU 6/01), the maximum cost of classifying property as MPZ is 40,000 rubles. (accounting policy may establish a smaller amount). Such property is written off as expenses as soon as it is put into production. Anything that exceeds this limit, but meets the above criteria, is taken into account as OS.

In tax accounting (TA) objects worth up to 100,000 rubles. inclusive, are not considered fixed assets (Article 257 of the Tax Code of the Russian Federation). The assignment of an asset to fixed assets affects the procedure for accounting for its value as part of expenses (fixed assets are subject to depreciation, i.e., they are written off gradually according to the accounting policy of the enterprise, and inventories are written off at a time), as well as the procedure for document flow, inventory and write-off.