If the inventory results differ from the data reflected in the accounting documents, it is necessary to draw up a so-called matching statement. Usually a special form INV-19 is used, which is quite convenient and simple. A form and a ready-made example of document design, features that are important to pay attention to - talk about all this right now.

Blank form INV-19 (excel)

Sample of filling out a matching sheet (excel)

Main purpose

Carrying out accounting is a mandatory procedure, during which discrepancies are almost always inevitably discovered:

- surplus;

- shortage.

All these discrepancies must be recorded in writing. The reporting procedure is necessary, first of all, for the company itself, because:

- Thanks to detailed accounting, you can correctly draw up accounting documents.

- It is possible to analyze the causes of shortages and reduce their volumes.

- You can see weaknesses in the storage system, transportation of goods within the enterprise, and in the work of employees, which leads to discrepancies in results.

NOTE. The statement is filled out in all cases during accounting - both scheduled and extraordinary (for example, after the dismissal of one financially responsible person and the transfer of his powers to a new employee).

Why do the results differ?

It is obvious that the results of counting commodity units, materials, raw materials, products and other material assets may differ from those presented in accounting documents due to inattention. Moreover, an error can occur at several stages at once or at one of them:

- Errors during counting are the most likely and real reason.

- Errors when drawing up a particular document with balances.

Along with this, the reasons for the discrepancies may be related to the following factors:

- re-grading;

- theft;

- loss of an item (due to inattention);

- cashier error (the item was not punched and was simply “handed over” at the checkout).

Analyzing specific causes is always a complex process. As a rule, the results of only one inventory, presented in the reconciliation sheet, are not enough. It will be necessary to conduct a series of inspections (including unscheduled ones) to establish the specific reasons for the discrepancies.

Comment on the rating

Thank you, your rating has been taken into account. You can also leave a comment on your rating.

Is the sample document useful?

If the document “Sample.

Comparison statement of the results of inventory of fixed assets. Form No. inv-18 (order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49)” was useful for you, we ask you to leave a review about it. Remember just 2 words:

Contract-Lawyer

And add Contract-Yurist.Ru to your bookmarks (Ctrl+D).

You will still need it!

Filling procedure

Results with discrepancies are not immediately entered into the form. Typically, the procedure looks like this:

- Workers participating in the inventory commission discover shortages and/or surpluses.

- They immediately record this information in their personal papers (draft).

- Then the data is re-checked to exclude the possibility of an error due to inattention (usually another employee recalculates it for greater reliability).

- If it is confirmed that the fact of a shortage or surplus actually exists, the inventory result is transferred to the final version - i.e. on the matching sheet.

Leave a comment on the document

Do you think the document is incorrect? Leave a comment and we will correct the shortcomings. Without a comment, the rating will not be taken into account!

Thank you, your rating has been taken into account. The quality of documents will increase from your activity.

| Here you can leave a comment on the document “Sample. Comparison statement of the results of inventory of fixed assets. Form No. inv-18 (order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49)”, as well as ask questions associated with it. If you would like to leave a comment with a rating , then you need to rate the document at the top of the page Reply for |

Form and sample document

If you use the most common form INV-19, you just need to fill out all the fields correctly. If you develop and use your own sample, then when drawing it up, it is important to take into account that the document contains the following information:

- Name of the organization, type of its activity, OKUD and OKPO codes.

- A link to the document that regulated the start of the inventory - usually a corresponding order is issued, which stipulates the timing of the procedure, the responsible persons and the chairman of the commission.

- The timing of the inventory is the start and end dates (sometimes they may coincide).

- Document number (consecutive numbering is used throughout the year or for other periods - at the discretion of the administration).

- Full name, full title of the position of the responsible person. This could be a warehouse manager, department manager, senior cashier/salesperson, administrator, etc.

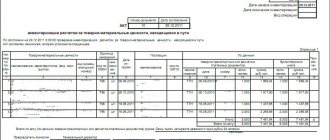

- The main part of the comparison sheet is presented in the form of a table in which the inventory results are recorded. It is necessary to indicate only those groups of goods for which a shortage and/or surplus was detected (including as a result of misgrading). The INV-19 form contains 32 columns, including:

- name of the product (or other value), its grade, type;

- labeling of goods in the form of a code that is accepted in the nomenclature system in a warehouse or store;

- accounting results - with discrepancies in quantities and in rubles (both in surplus and shortage);

- discrepancies in regrading;

- finally calculated discrepancies (taking into account additional final checks).

- At the end of the statement, the financially responsible person once again puts his signature, which means that he has become familiar with the results.

NOTE. Amounts are indicated to the nearest kopeck. If the value does not contain kopecks, you can specify it in a simple format, for example, 1000 (rubles), rather than 1000.00 (rubles).

The INV-19 form is shown below.

Here's a finished example:

Digital library

Finance and credit / Control and audit / 9.4 matching statements compiled based on the results of the work of inventory commissions

Matching statements are one of the most important final inventory documents. They reflect the final results, which represent the discrepancy between accounting indicators and data from inventory records and acts. To compile matching statements, the balances in the accounting data must be derived from all submitted receipts (expenses) documents as of the inventory date. Persons who carried out the actual inventory must confirm the assessment of the final actual balances with their signatures. If, at the same time, errors in prices, taxation and calculations are found in the primary inventory documents, inventories and acts, they must be corrected, agreed upon and certified by the signatures of all members of the commission and financially responsible persons. On the last page of the inventory and act, a special note is made about checking prices, taxation and calculation of results.

Comparison statements are prepared by the organization's accounting department employees. In the matching statements, the value of surpluses and shortages of inventory items is given in the valuation at which they are listed in the accounting registers.

Fixed assets.

The actual data of the inventory list of fixed assets in form No. INV-1 are entered

into the matching statement

in form No. INV-18. The beginning of the comparison sheet contains the same details as in the primary inventory document: references to the date and number of the administrative document, the actual start and end dates of the inventory. The statement is signed by the accountant and the financially responsible person. It contains a table with the following columns:

1) name of the fixed asset;

2) year of release of the fixed asset;

3) inventory, serial and passport numbers of the fixed asset;

4) surplus or shortage in quantity and amount.

Inventory

.

Actual data from the inventory list of inventory items in form No. INV-3, the act of inventory of goods shipped in form No. INV-4, the act of inventory of materials and goods in transit in form No. INV-6 are entered into the inventory

results inventory items according to form No. INV-19.

The beginning of the comparison sheet contains the same details as in the primary inventory document: references to the date and number of the administrative document, the actual start and end dates of the inventory.

The matching statement is signed by the accountant and the financially responsible person. It contains a table with the following columns:

1) name, nomenclature number of inventory items;

2) name and code of the unit of measurement according to SOI;

3) surplus, shortage in quantity and amount according to primary inventory documents;

1) surplus, shortage in quantity and amount, adjusted by clarifying accounting entries;

2) surpluses in quantity and amount included in covering shortages as a result of misgrading;

3) shortages in quantity and amount, covered by surpluses as a result of misgrading;

4) receipt of final surplus in quantity and amount;

5) final shortages in quantity and amount.

Trade.

Factual information from the inventory list of goods, materials, containers, funds in trade in form No. INV-12 is entered into the

matching list of goods, materials and containers in trade organizations that carry out quantitative and cost accounting of valuables,

in form No. INV-20.

Factual information from the inventory list of goods, materials, containers, funds in trade in form No. INV-13 is entered into the matching list of goods, materials and containers in retail organizations that carry out cost accounting of valuables,

according to form No. INV-2L

Shortages

. Based on the results of the inventory, the organization compiles a statement of the results identified during the inventory.

The statement records the total amount of shortages and surpluses, as well as the amount of shortages associated, respectively, with damage to property, offset by regrading, within the limits of natural loss rates attributed to the perpetrators, written off to the financial results of the organization.

Simpler form

Each company has the right to decide for itself which form to use. At the same time, the INV-19 form is used very often - on the one hand, it is convenient, on the other, many companies continue to use it out of business habit. However, in some cases, a simpler version of the form may be useful, in which you can indicate a minimum of data:

- name of the company and warehouse, date of compilation;

- Name of product;

- its quantity (in fact);

- its quantity (according to documents);

- identified deviation;

- units;

- unit price;

- the sum of all goods by actual quantity;

- the sum of all goods according to the data in the accounting documents;

- signatures, positions of responsible persons, transcripts of signatures.

This option allows you to save significant time. It is used when carrying out accounting in small warehouses, when counting individual items (sections), as well as when re-counting if deviations are found that raise doubts (i.e. there is reason to think that the cause of the error is inattention).