Inventory is represented by a special procedure for reconciling the company’s existing valuables, goods, money or fixed assets with those values that are available in the official documents of the enterprise. It can be carried out mandatory or on the initiative of the company management. Carrying out an inventory is mandatory for some companies, and this process is certainly carried out every year in all companies. The main purpose of this procedure is to identify various inconsistencies and shortages. Many firms do not realize the value of this process, so it is used only as a formality. Although, if you approach inventory wisely, then with its help you can identify all shortages or surpluses.

Purpose of the process

You may be interested in: Which bank is better to invest money in? Review of rates on bank deposits

Many novice entrepreneurs wonder whether it is necessary to carry out an inventory and what goals can be achieved through this process. The procedure is represented by a systematic accounting of material assets and assets, for which actual indicators are compared with data from official documents.

You may be interested in: Aroon indicator: description of the indicator, application in trading

The main purpose of inventory is to identify discrepancies. They can appear for various reasons:

- impact on values of factors of a natural nature, therefore this includes shrinkage, damage due to improper storage, evaporation or loss occurring during the transportation of goods;

- illegal actions on the part of company employees, for example, taking incorrect measurements, allowing body kits, or even stealing valuables;

- problems that arise during accounting, therefore, after the inventory, various errors, corrections, inaccuracies, clerical errors or other ambiguities in documents are often identified.

Channel PROGRAMMER'S DIARY

The life of a programmer and interesting reviews of everything. Subscribe so you don't miss new videos.

Based on this, a systematic audit allows any company manager to promptly identify various violations and problems.

Verification functions

You may be interested in:Engineering preparation of a construction site: basic rules

Carrying out an inventory of goods necessarily involves the use of various functions of the procedure:

- The conditions under which various goods are stored are objectively assessed, and such an assessment is objective.

- It is determined how correctly and competently the maintenance of various documents is carried out in the company.

- The features of warehouse management in the company are reflected.

- The completeness and accuracy of accounting is assessed.

- Grants are provided for the prevention of various abuses and violations on the part of hired specialists.

Due to such numerous functions, inventory is considered an important process in any company.

Cases of mandatory inventory

Some companies are required to carry out the procedure based on legal requirements. Information on in which cases an inventory is mandatory is contained in the following regulations:

The check must be carried out in the following situations:

- when providing property for rent;

- sale or repurchase of assets owned by the company;

- transformation of a state or municipal enterprise;

- before preparing annual reports;

- when appointing a new financially responsible person in the company;

- upon detection of damage to valuables or theft of property;

- after natural disasters or other emergencies;

- during company reorganization;

- before the liquidation of the organization;

- in other situations provided for by law.

Carrying out an inventory is mandatory before preparing annual reports. This process allows not only to take into account legal requirements, but also to prevent various errors or shortcomings in accounting papers. Typically, companies perform the review annually before the end of the calendar year.

Inventory of fixed assets is carried out every three years. Every manager should know all cases of mandatory inventory. Additionally, he can independently order an inspection if there are doubts about the integrity of the work of certain hired specialists.

You may be interested in: Residential complex "Peredelkino Blizhnoe": reviews, advantages and disadvantages

Other grounds

Please note that in relation to fixed assets, mandatory inventory is carried out once every 3 years. And in organizations of the Far North and equivalent to them, inventory of goods, raw materials and supplies can be carried out during the period of their smallest balances.

As you can see, in some cases an inventory is required - there is a non-exhaustive list of reasons. Therefore, here are examples when there is still an obligation to conduct an inventory:

- to determine in the contract for the sale of an enterprise its composition and value (clause 1 of Article 561 of the Civil Code of the Russian Federation);

- upon receipt by an external manager for management of the debtor’s property (clause 2 of Article 99 of the Law of October 26, 2002 No. 127-FZ “On Insolvency (Bankruptcy)”;

- monthly in relation to narcotic drugs, psychotropic substances and their precursors at the disposal of legal entities - holders of licenses for their circulation (Clause 1, Article 38 of the Law of 01/08/1998 No. 3-FZ “On Narcotic Drugs and Psychotropic Substances”).

Also, conducting an inventory is mandatory in cases established by the head of the organization (Part 3 of Article 11 of the Law on Accounting dated December 6, 2011 No. 402-FZ). In particular, such cases can be specified in the inventory regulations.

Also see Inventory Matching Statements.

Read also

25.07.2019

How the order of the process is established

Carrying out an inventory necessarily involves taking into account the requirements contained in the Methodological Recommendations. Numerous nuances are determined by the immediate managers of the companies. For this purpose, the rules are fixed in the constituent documentation.

The director of the company can determine some important points:

- when the process needs to be executed;

- how many times a year can inventory be taken;

- at what time the process takes place;

- how long does it last;

- what assets are necessarily checked;

- who is a member or chairman of the inventory commission.

The answers to all these questions are fixed in the constituent documentation. Carrying out an inventory is mandatory when changing financially responsible persons. Under such conditions, a new hired specialist can be sure that the shortcomings that arose under his predecessor will in no way be transferred to him.

What is being checked?

Inventory can be carried out in relation to different property, so checking of cash, fixed assets, materials or other items is highlighted. During the procedure, all assets and liabilities existing in the company and its divisions are assessed. The following elements are checked:

- fixed assets of the company used to conduct business;

- intangible assets of the company;

- various financial investments;

- goods and materials;

- unfinished production;

- money in accounts and in the cash register;

- securities and BSO;

- settlements with counterparties, buyers, the Federal Tax Service, various funds and other debtors or creditors;

- reserves;

- assets and liabilities of the enterprise.

In what cases is it necessary to conduct an inventory of materials? Such a check is carried out when there are suspicions that hired specialists in the company are abusing their powers, so theft or shortage is detected.

Not only the property owned by the company is subject to inspection, but also the assets located on off-balance sheet accounts. The enterprise does not have ownership rights to them, but they are used in the process of work on the basis of a lease agreement or other agreements.

Process steps

Carrying out an inventory of property necessarily involves performing sequential actions. Therefore, the process is divided into stages:

The inventory must be completed before the actual preparation, signing and submission of annual reports to the Federal Tax Service. The inventory procedure necessarily ends with the preparation of a special report.

What are the consequences of lack of inventory?

Inventory is the main way to control the activities of any organization. A kind of “medical examination” for the company. The ability to control property values and the economic condition of the enterprise. But what happens if you neglect inventory and don’t carry it out at all? Could this turn into a problem for the company? And how significant will these problems be?

When is inventory required?

Carrying out an inventory in our country is mandatory in several cases (Regulations on accounting and reporting in the Russian Federation):

- when transferring the organization’s property for rent, redemption, sale;

- before drawing up annual financial statements, except for property, the inventory of which

- was carried out no earlier than October 1 of the reporting year;

- when there is a change of financially responsible persons or owner;

- when establishing facts of theft or abuse, as well as damage to valuables;

- in case of natural disasters, fire, accidents or other emergencies;

- when preparing documentation for property write-off;

- upon liquidation (reorganization) of the organization.

An inventory of fixed assets can be carried out once every three years, and of library collections - once every five years.

Inventory helps to identify shortages, surpluses, re-sorting, find lost items or even compensate for damage. During an inventory, property is checked, its condition is determined and revalued.

But what happens if the organization does not conduct an inventory at all? Is this prosecuted by law at the state level, are fines and sanctions imposed?

Is not keeping an inventory a criminal violation?

Let us say right away that there is no fine as such for lack of inventory. But this does not mean that there will be no problems.

There are cases when tax authorities try to fine an organization under Art. 120 of the Tax Code of the Russian Federation, citing the fact that the absence of inventory acts is a violation of the rules for accounting for income/expenses and taxable items.

Visitors to one of the forums on the Internet, discussing possible problems in the absence of inventory check reports, suggested that in some cases this could entail administrative and sometimes even criminal liability. In defense, they gave the following arguments: “When preparing annual reports, an inventory of liabilities and assets was not carried out, but in accounting, on the contrary, property or liabilities were carried out, which results in unreliable reporting. Here it would be appropriate to recall such a concept as “official forgery” (the entry by an official of knowingly false information into official documents, other forgery of documents, as well as the preparation and issuance of deliberately untrue documents). This, according to law enforcement agencies, may lead to criminal liability.”

“Criminal liability arises in the event of proof of fictitious (falsified) accounting statements. This may be the case if any assets and liabilities are misrepresented. The reliability of the financial statements is confirmed by a timely inventory. That is, there is no responsibility for the very fact of lack of inventory. But in this case, the accounting statements may be considered fictitious and questioned.”

“The onset of criminal liability due to failure to carry out an inventory is only an assumption of what may happen. The respondents presented arguments for criminal liability. As for the very fact of lack of inventory, there is no responsibility for this.”

In addition to administrative or criminal liability, a company may encounter other types of problems. For example, the refusal to deduct VAT and the inability to take into account expenses within the limits of natural loss norms as expenses. As well as the possibility of writing off bad debts.

Who is responsible?

You can talk about the consequences of lack of inventory for a long time: you can argue both in favor of impunity for such business conduct and the threat of criminal liability. However, Article 11 of the Law on Accounting in the Russian Federation “Inventory of assets and liabilities” provides for the direct obligation of organizations to conduct an inventory at least once a year before drawing up annual financial statements.

In addition, inventory, as a control mechanism, can help avoid violations for which responsibility is clearly established. This applies to situations where, during an audit, tax authorities identify excess inventories that are not accounted for in the accounting documentation. It is considered that such property was received free of charge. And if this leads to a distortion of the financial statements by 10% or more, or an understatement of the amounts of accrued taxes and fees by at least 10%, then the organization’s officials may be brought to administrative liability under Art. 15.11 of the Code of Administrative Offenses of the Russian Federation for gross violation of the rules of accounting and presentation of financial statements. And this will entail fines, prosecution and all related problems.

But most importantly, the manager himself should be interested, first of all, in conducting an inventory. After all, it is he who is responsible for the accounting of his large or small organization. And all the problems about not carrying out an inventory will fall on his shoulders.

And in addition to responsibility, such a manager also incurs financial losses: how much money can be lost due to the carelessness and negligent attitude of employees? How much profit was lost, how much was sold “outside” and “taken out” of the company? After all, no one except the owner cares about income.

Fear of ruining relationships with your team or finding out the truth about the real state of affairs in the company can prevent your company from growing, taking a step and moving to a new level of income and profit.

Report writing rules

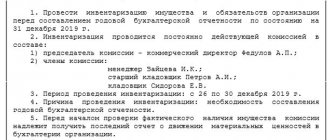

Based on the results of the inspection, a report is generated. It includes the following information:

- date of inventory;

- information about the members of the inventory commission;

- the period during which the procedure was performed;

- the company's property being inspected;

- identified problems and shortcomings;

- signatures of all inspectors.

Although conducting an inventory is mandatory before preparing annual reports, any company manager can begin the process without good reason. To do this, an appropriate order is issued, after which the company’s employees are required to follow the procedure.

Responsibilities of the inventory commission

You may be interested in: A loan secured by real estate is... Definition, types of loans, registration stages, expert advice

Carrying out an inventory is mandatory by law, so every company must create a special body responsible for inspection and accounting. It is called the liquidation commission. She has some responsibilities:

- the use of various preventive measures aimed at preserving the property of the enterprise;

- participation in various disputes related to the storage or damage of property values;

- control over the correctness of drawing up various documents relating to the company’s property;

- Carrying out an inventory based on the order of the company management;

- preparation of a report on the results of the inspection;

- conducting an investigation aimed at identifying the culprit of various violations and problems.

All these actions should be performed exclusively by company employees who are not interested in the results of the audit.

Participation of financially responsible employees

Financially responsible employees are required to be present during inventory and other similar audits, during which the safety and condition of the property entrusted to them is checked. Representatives of the Russian Ministry of Finance have long been convinced of this (letter dated July 15, 2008 No. 07-05-12/16). The obligation of the financially responsible person to be present during the inventory is also provided for by the terms of the agreement on full individual financial responsibility (Appendix 2 to Resolution of the Ministry of Labor of Russia dated December 31, 2002 No. 85).

Advice: If an organization has signed an agreement on collective financial responsibility, then it should explicitly state the condition that employees are required to be present during the inventory of the property entrusted to them.

This recommendation was given by representatives of the Russian Ministry of Finance in a letter dated July 15, 2008 No. 07-05-12/16. In the standard form, such participation in inventory is classified as a collective right (Appendix 4 to Resolution of the Ministry of Labor of Russia dated December 31, 2002 No. 85). However, experts from the Russian Ministry of Finance advise to write this down as a duty by changing the provisions of the contract. After all, the rules oblige employees to be present during the inventory of the property for which they are responsible. This is directly stated in paragraph 2.8 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated June 13, 1995 No. 49.

Who is on the commission

When forming a commission, the following specialists are usually involved:

- administrative workers;

- accounting department specialists;

- internal auditors;

- often even independent experts are involved;

- representatives of various positions available in the organization’s staffing table.

If the company has a small amount of different property, then often the responsibility for conducting an inventory is transferred to the audit commission, if the company has one.

If during the inspection it is revealed that even one member of the commission is absent, then the results of the procedure are considered invalid.

The procedure for taking inventory of property and liabilities

The inventory procedure is entrusted to either permanent or working inventory commissions. They are created by order of the leader. The order is drawn up in any form. It also determines the composition of the commissions.

A working inventory commission is created when the volume of necessary work exceeds the capabilities of a permanent commission. Working commissions are also formed by order of the manager. One order may approve the composition of one or several working commissions. The order can be drawn up in both free and unified form INV-22.

If the planned volume of work is small, you can not create a commission at all, but involve an audit commission (if the company has one) for verification.

The responsibilities of the permanent and working inventory commissions must be enshrined in the regulations.

The algorithm for implementing the procedure is as follows. Before it starts, the commissions are obliged to:

1. Receive from financially responsible persons:

- incoming and outgoing documents not submitted to the accounting department. This is necessary for the accounting department to determine the balances at the beginning of the inventory;

- receipts confirming that all incoming and outgoing documents for property have been submitted to the accounting department or commission, stating that all incoming assets have been capitalized by financially responsible persons, and those that have been disposed of have been written off.

2. Prepare inventory forms (acts) of inventory items in two copies. It is allowed to use both arbitrary and unified forms INV-1, INV-3, INV-4. Inventories (acts) are compiled for financially responsible persons and storage locations.

During the inventory, the commissions are obliged to:

1. Inspect the property and assess the possibility of its subsequent use.

2. Determine the actual availability of property.

3. Confirm the presence of non-material property (cash, intangible assets, financial investments).

4. Establish the correctness and validity of the amounts of obligations.

5. Check the book value of the property and the correctness of the calculation of valuation reserves.

6. Check the validity of recognition and the amount of estimated liabilities.

7. Analyze the reasons for premature write-off of property (physical and moral wear and tear, violation of operating and storage conditions).

8. Find the culprits.

9. Reflect in the inventories information about the actual availability of accounting objects, document the results of the inspection.

10. Prepare proposals to eliminate detected discrepancies with accounting data.

Permanent commissions are required to perform additional tasks that are assigned to them during the inter-inventory period:

- drawing up documents for writing off unusable property;

- control and disposal of unusable property;

- control over the withdrawal of parts, assemblies, assemblies, materials, and waste remaining from disposal of property suitable for use or sale;

- determining the value of material assets suitable for use or sale remaining from the disposal of property;

- acceptance of material assets when their quantity, quality or assortment does not correspond to contractual conditions.

If the organization has both a permanent inventory commission and a working commission, their functions need to be separated.

The standing commission is responsible for:

- determining the number of working inventory commissions;

- instructing commission chairmen and members;

- distribution of work between them;

- monitoring the correctness of the inventory, timeliness and correctness of registration of inspection results;

- generalization of the results.

Working commissions are directly involved in the inventory process.

Recommendations from experts

When conducting an inventory in a company, it is advisable to use certain recommendations. These include the following:

- 10 days before the inspection, the manager issues a corresponding order, which is recorded in the journal.

- It is allowed to form a commission not only permanent, but also one-time or working.

- If an organization uses a lot of inventory items, then the decision on the need to conduct a random inventory is made by the manager based on the current situation in the company.

- All members of the commission must be involved in the verification, otherwise the results are easily invalidated.

- During the process, financially responsible persons are involved.

- The company's management must provide conditions for the process to be completed quickly and easily.

- Verification often takes quite a long time, and this is especially true for companies that use a large number of materials or ship and receive many goods.

During the inventory, commission members must take into account legal requirements.

10.1.2. Creation of an inventory commission

To carry out an inventory, a permanent inventory commission is created in the organization. When the volume of work is large, working inventory commissions are created to simultaneously carry out an inventory of property and financial obligations. If the amount of work is small and the organization has an audit commission, it can be entrusted with carrying out inventories.

The personnel of permanent and working inventory commissions is approved by the head of the organization. The document on the composition of the commission (order, resolution, instruction) is registered in the book of control over the implementation of orders to conduct an inventory (form N INV-23). The commission includes representatives of the organization’s administration, accounting service employees, other specialists (engineers, economists, technicians, etc.), as well as representatives of the organization’s internal audit service and independent audit organizations.

The absence of at least one member of the commission during the inventory serves as grounds for declaring its results invalid.