Organizations periodically conduct inventories. They are needed in order to obtain the current balances of a particular product. Inventory also allows you to compare actual data with accounting data in the program.

There are cases when such a reconciliation of balances makes it possible to identify thefts among financially responsible persons.

After conducting an inventory in 1C 8.3, the shortage can be written off and the surplus can be capitalized. For this entire sequence of actions and its reflection in accounting, there are special documents, the completion of which we will consider below.

Inventory of goods

Let's start with the inventory itself. To do this, use the document of the same name in the “Warehouse” section of the program.

Our team provides consulting, configuration and implementation services for 1C. You can contact us by phone +7 499 350 29 00 . Services and prices can be seen at the link. We will be happy to help you!

The document is quite simple to fill out. First of all, we will indicate all the necessary header details.

Let's assume that an inventory was carried out at the retail warehouse of store No. 23 on March 31, 2016. You don’t have to indicate the responsible person, as we did, but fill it out if necessary.

For the convenience of filling out the list of goods, you can use the “Fill in by warehouse balances” item from the “Fill” menu, as shown in the image below. In any case, you can fill out the tabular part manually if, for example, during an inventory check in a warehouse, a product is found that is not on stock at all.

We did not complicate the example and used only automatic completion. The program “found” only 127 units of 95% Chocolate in the warehouse. Let's assume that this number does not coincide with reality, and we are missing seven tiles.

In the “Fact” column we will add that in fact there are only 120 units of 95% chocolate in the warehouse. Now some recalculation has been automatically carried out in the tabular part.

The “Deviation” column displays the quantity “-7”, which is highlighted in red. This color means there is a shortage of goods. Also, depending on the quantity taken into account in the program and the actual quantity, the corresponding amounts of goods were calculated taking into account the price.

When carried out, this document does not create any accounting movements. From it you can print out all the necessary reports, for example, on forms INV-3, 22, 19. Reflection in accounting of the fact of deviation can be done by writing off and capitalizing goods, depending on whether it is a shortage or a surplus. These documents are created both independently and based on the inventory.

Video on filling out an inventory card:

Shortages, surpluses, re-grading in 1C: Accounting ed. 3.0

Published 03/24/2020 23:16 Author: Administrator For the reliability of annual reporting, it is necessary that the balances of all accounts reflect reality and not erroneous data. In this regard, one of the main preparatory stages is the inventory of inventory items in warehouses. We recently wrote about how to correctly fill out an order to conduct an inventory and how to enter its results into the program. And today we’ll talk in more detail about the reflection of identified shortages, surpluses and mis-gradings both in accounting and tax accounting.

Reflecting the shortage

In the 1C program: Accounting ed. 3.0 write-off of shortages of goods is entered using the document “Write-off of goods” in the “Warehouse” section. When posting this document, the program generates a posting to the debit of account 94 and the credit of the account for recording written off inventory items, for example, 10, 41, 43.

At the same time, account 94 is not an account for reflecting the organization’s expenses and losses; it accumulates all discrepancies between the accounting quantity of inventory items and the actual one.

For further movement of written-off goods, it is necessary to determine the possible cause of the shortage. This may be loss or damage to goods due to the fault of the employee, or natural loss. Let's consider the nuances of reflecting all of the above situations in the program.

In the first case, in the “Operations” section, using the document “Operations entered manually,” the transfer of the cost of inventory items to the guilty party is recorded. Subsequently, he can pay off the cost of the damage through the company’s cash desk, deposit funds into a current account, or write a statement to deduct this amount from his salary.

According to tax accounting, in this case there are no differences in the reflection of the transaction.

But with regards to the previously accepted VAT deduction, opinions differ. On the one hand, paragraph 3 of Article 170 of the Tax Code of the Russian Federation establishes a closed list of cases of VAT recovery, and there is no such item as writing off inventory and materials when shortages are identified. The courts adhere to the same position, as evidenced by the decision of the Supreme Arbitration Court of the Russian Federation dated May 19, 2011 No. 3943/11. At the same time, the Russian Ministry of Finance has repeatedly issued letters of explanation in which it recommended that these amounts be restored - No. 03-07-11/15015 dated March 19, 2015. Therefore, this decision remains with the organization.

The second reason for writing off goods, as we said earlier, may be the natural loss of certain types of goods, for example, bottling, shrinkage, leakage, etc. Ministries and departments for sectors of the economy establish norms of natural loss used to determine the permissible amount of attributing shortage amounts to production costs.

Based on this, the write-off of shortages can be both within the established standards and in excess of them.

In the first case, the reflection of losses within the normal limits is entered by the document “Operations entered manually” and generates a posting to the debit of the expense account (20, 25, 26, 44) and credit 94.

In cases where losses of goods and materials exceed the norm of natural loss or the persons responsible for the damage or loss of goods and materials could not be identified, the costs of the identified shortage are attributed to non-operating expenses (clause 5 of clause 2 of Article 265 of the Tax Code of the Russian Federation). In this case, the fact that there are no perpetrators must be documented by an authorized government body.

Reflection of surplus

According to paragraph 28 of the Regulations on accounting and financial reporting in the Russian Federation (approved by order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n), surpluses are accounted for at market value, increasing the financial results of the organization.

In tax accounting, they relate to non-operating income of the organization in the reporting period in which they were identified (clause 20, article 250, clause 1, article 271 of the Tax Code of the Russian Federation).

In the program, information about identified surplus inventory items is entered using the document “Receipt of Goods” in the “Warehouse” section. It can be entered both on the basis of the “Inventory of goods” document, and independently of it.

The posted document generates postings: by debit - a reflection of capitalized inventory items, and by credit - a reflection of non-operating income.

Reflection of misgrading

Regrading is an offset of identified shortages and surpluses among themselves for homogeneous inventory items, if the discrepancy between items is of equal quantity and they were identified in the same period. Simply put, during the inventory period you discovered a shortage of the product “Light Wood Table” in the amount of 1 piece, and a surplus of “Mahogany Table” in the amount of 1 piece.

The decision to count a regraded student is always made only by the head of the organization, which is confirmed by a corresponding order.

If the cost of surplus goods is greater than that of lost goods, then such a difference in accounting is attributed to an increase in the financial results of the organization.

In the opposite situation, the difference in cost is written off either according to the norms of natural loss, in the case of commodity items that meet the standard, or to the account of the guilty parties, or if the perpetrators were not identified or the court refused to recover damages from them, then it is written off as a decrease in the financial results of the organization .

In tax accounting, regrading is not provided for by Chapter 25 of the Tax Code of the Russian Federation, therefore the identified discrepancies will be reflected as writing off shortages and capitalizing surpluses. Accordingly, since the capitalization of surpluses in tax accounting is carried out at market value, and the offset of re-grading in accounting is defined as the difference between the values of the offset positions, constant differences arise in accounting.

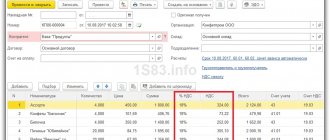

Let’s assume that the cost of the position “Light wood table” is 5,000 rubles, and “Mahogany table” is 6,000 rubles. Let’s carry out the document “Inventory of goods” in the “Warehouse” section.

Then we need to offset the regrading in accounting and reflect the write-off of the shortage and capitalization of the surplus in tax accounting.

To do this, go to the “Warehouse” section and select the “Item assemblage” item. Products with a positive deviation must be indicated in the “Set” field, and those with a negative deviation – in the “Accessories” field. In this case, the program will generate a posting for the debit and credit of account 41, but with different analytics.

The transaction amount will be determined from the cost of the component. Accordingly, we need to make another entry for the amount of differences in the cost of goods.

To do this, go to the “Operations” section and select the “Operations entered manually” item. Let us reflect non-operating income, which for accounting purposes will be calculated as the difference in the value of the written-off and received goods, and in tax accounting - as the value of the capitalized surplus. In the line reflecting permanent differences, it is necessary to indicate a negative deviation between the accounting and tax accounting amounts.

We will create a balance sheet for 41 accounts and check the balances of goods.

If the value of the incoming surplus goods is less than the value of the written-off shortages, then the documents will look like this.

Depending on whether you can apply standards for natural loss of goods or not, you should make another entry to attribute the shortage to expense accounts or to non-operating expenses. Also, the amount of the shortage can be attributed to the guilty person, if one is identified and the fact is confirmed by authorized state bodies

Author of the article: Alina Kalendzhan

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

JComments

Write-off of goods

Let's continue with the previous example. During the inventory, it was found that in the sales area of store No. 23 there was a shortage of 7 chocolate bars (95%). This quantity must be written off from the warehouse, because it simply does not exist.

To do this, we will use the document “Write-off of goods”. We created it based on the previously entered inventory.

Please note that the document is completely filled out automatically. Despite the fact that the program gives us the opportunity to edit it, we will not do this.

After the document was completed, two movements were created: to write off seven chocolate bars 95% and to write off the trade margin. The second posting was created due to the fact that the warehouse with the detected shortage is a sales area and the prices are accordingly different.

Write-off of goods in 1C from the warehouse

In order to write off goods based on inventory, you need to create a new write-off document.

In “Inventory”, click the “Create based on” - “Write-off of goods” button:

The 1C Accounting 8.3 program will automatically generate a write-off for items that had a shortage:

If everything is correct, just click the “Pass” button. Let's check the postings for writing off goods:

Posting of goods

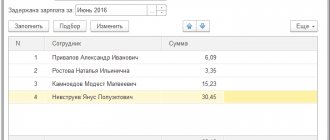

Now let's look at the second example. During the inventory, it was found that instead of the 110 kilograms of “Assorted (commission)” candies reflected in the program, there are actually 150 of them in the warehouse. In this case, the deviation in the inventory will be 40 kilograms.

Since the deviation occurred in a positive direction, to take it into account it is necessary to capitalize the surplus. Capitalization, just like write-off, can be created from the goods inventory document itself.

The program filled out all the necessary fields automatically, and all we had to do was post the document. After it is carried out, the number of “Assorted (commission)” candies in the program will coincide with the actual quantity in the warehouse.

Video on capitalization and write-off of goods in 1C 8.3 based on inventory:

Surplus inventory items during inventory in 1C 8.3

Capitalization of surplus inventory items discovered as a result of inventory:

- In accounting, surplus inventory items are accounted for at current market value. Posting Dt accounting account – Kt account 91.1 as other income;

- In NU, surplus inventory items found during inventory are taken into account as non-operating income by virtue of clause 20 of Article 250 of the Tax Code of the Russian Federation.

Step 1. Creating the Goods Receipt document and filling it out

To capitalize surplus inventory items discovered as a result of inventory, use the Create based button - then Capitalize goods:

Filling out the title of the Goods Receipt document:

- In the Number field – the document number automatically generated by 1C 8.3;

- In the From field – day, month, year of the document;

- In the Organization field – filled in automatically from the Goods Inventory document;

- In the Warehouse field – the warehouse where the detected inventory items will be taken into account;

- In the Income Item field – the item of other income and expenses; income in accounting and accounting records will be attributed to it:

The tabular form of the Goods Receipt document is filled in automatically from the Goods Inventory document. All inventory items for which surpluses have been identified are transferred to a tabular form:

Step 2. Posting the document Receipt of goods

Clicking the Post button will create the following transactions:

Step 3. Printing the Goods Receipt document

We print the invoice by clicking on the Invoice for goods receipt button:

Transfer of inventory items into operation

For the transfer of goods into operation, the same ERP document of the 1C system is intended - “Internal consumption of goods”, but with a different type of operation - “Transfer for operation”.

The scheme for working with a document (creation, filling out) is similar to that discussed above, with the exception that when you select the business transaction “Transfer into operation”, additional fields become available for filling - category of operation and financially responsible person. After the document is reflected in accounting, inventory items are written off and further accounting of such materials is carried out in the off-balance sheet account MTs.04.

Document “Conversion of goods” in the 1C program Trade Management (UT 11) 11.2

Let's move on to "Recalculations of goods" . At the top of this journal, you must select the warehouse for which recalculations will be processed. Let's select the main warehouse.

Also, if the use of recalculation status is set for a warehouse, you can additionally select the corresponding warehouses. This is configured in the card of each warehouse. On the “Order scheme and structure” there is a flag “States of goods recounts” . These statuses are required for an order warehouse, for which an order scheme is used to reflect surpluses and shortages, and this option allows you to further detail the process of recounting goods.

Let's create the first recount of goods. The 1C Trade Management program (UT 11) 11.2 automatically filled out the warehouse for which we will carry out recalculation. I indicated the responsible administrator. You can specify the executor - this can be the financially responsible person or someone else. The inventory is carried out for the warehouse as a whole, without breakdown by organization, so there are no organizational details here.

On the “Products” , you can use the selection settings, set some parameters - for example, by item groups, by selection characteristics, and then click the “fill in by selection” to fill out the tabular part with the goods that are listed in our accounting.

Next, you will need to fill out the “Actually” . “Accounting” column corresponds to accounting data, and it will be refilled when posting the document. You can automatically refill this column “according to the fact” by clicking the “fill in the accounting fact” . In this case, the button for the actual availability of goods corresponds to the accounting one, and the deviation is equal to zero.

Let's assume that in our case excess shortages were identified. For example, for a Sony TV, 2 units were found to be in stock, and for a Samsung refrigerator, the actual quantity was 8 units. Accordingly, the 1C Trade Management (UT 11) 11.2 program immediately identified deviations, namely, an excess on TV and a shortage on the refrigerator.

Such a document can be written down and posted.

Program 1C Trade Management (UT 11) 11.2 warns that when posting a document, the accounting quantity will be refilled. Let's confirm this. The document was passed.

Based on this document, you can print an inventory list. In this case, the inventory list was not printed because the corresponding document was not generated. We'll come back to this a little later. You can print the recalculation results.

The inventory sheet and the matching sheet are printed on the basis of the document of the same name “inventory list”. We have it in the “Warehouse acts” group. This document does not have any additional meaning other than to draw up a regulated document with the ability to print a regulated form.

Inventory of funds in the current account (surpluses identified)

Current accounts are intended for the storage and movement of funds in the currency of the Russian Federation. A foreign currency account stores funds in foreign currencies.

According to Part 1 of Art. 11 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” (hereinafter referred to as the Accounting Law), the assets and liabilities of an economic entity are subject to inventory.

An inventory of the relevant objects is carried out in order to identify discrepancies between the actual availability of such objects and the data of the accounting registers (Part 2 of Article 11 of the Accounting Law).

In a number of cases, conducting an inventory is mandatory and is established by the legislation of the Russian Federation, federal and industry standards (Part 3 of Article 11 of the Accounting Law). However, there is no list of cases of mandatory inventory in the new Accounting Law.

Inventory of funds held in banks in settlement (current), foreign currency and special accounts is carried out by reconciling the balances of amounts listed in the corresponding accounts according to the organization’s accounting department with data from bank statements (closing balance according to bank statements) (clause 3.43 of the Methodological Instructions on inventory of property and financial obligations, approved by order of the Ministry of Finance of Russia dated June 13, 1995 No. 49).

Also, when taking inventory of funds in a current account, the identity of the debit and credit turnovers of the accounts is checked to the data contained in the statements of credit institutions. The balance at the end of the period in the previous bank statement of the account must be equal to the balance at the beginning of the period in the next statement.

Example

The organization Sewing Factory LLC carries out an inventory of funds in the current account. During the inventory, a discrepancy was revealed: the account balance according to the accounting data was 60.00 rubles. less than the balance according to the bank statement.

The shortage is attributed to the person at fault

To perform an operation, you must create an Operation

.

Creating and filling out the “Operation” document (Fig. 3):

1. Menu: Transactions - Accounting - Transactions entered manually

.

2. “Create” button

3. Select the document type “Operation”.

4. In the “from” field, enter the inventory date.

5. In the “Content” field, enter the content of the operation.

6. To create a new transaction in the tabular section, click the “Add” button.

7. In the “Debit” field, select account 73.02 “Calculations for compensation of material damage.” Next, fill out the “Subconto1 Debit” field by selecting from the “Individuals” directory the person found guilty of the shortage.

8. In the “Credit” field, select account, select account 94 “Shortages and losses from damage to valuables.”

9. In the “Amount” field, you must fill in the amount of the shortfall attributed to the guilty party.

10. In the “Content” field, indicate the content of the operation.

11. The fields “Amount Dt” and “Amount Kt” in the “NU” line are automatically filled in with the value specified in the “Amount” column.

12. “Record” button.

13. To call up a printed form of an accounting certificate, use the “Accounting certificate” button.

Rice. 3