The expansion of the organization indicates business development, the need to cover new territories, clients and market segments. When another retail outlet, hotel premises or bakery opens, it means a separate division is opening.

In the legislation, many aspects of working with EP are not fully disclosed; taxpayers often have to rely on arbitration practice. I would like to focus on the analysis of practical situations.

Pay in order!

There are three types of separate divisions:

- Branch.

- Representation.

- Others.

The characteristics that unite all three types are territorial isolation and the presence of jobs created for more than a month. This is the general definition of an OP given by the Tax Code of the Russian Federation in Article 11. The Tax Code does not define the concepts of “branch” and “representative office”. Their definition will have to be sought in civil legislation.

Article 55 of the Civil Code of the Russian Federation indicates that the representative office represents the interests of the legal entity and also protects them. A branch has broader rights: it carries out all or part of the functions of a legal entity, including those of a representative office. Simply put, if an organization opens an office where a client can seek advice, conclude an agreement, write a complaint, place an order, then this is a representative office; if this office supplies the client with goods under a concluded agreement, then this is already a branch.

Other divisions fall into the “other” category. It is important to correctly determine what type of OP is opening. This matters not only from a legal point of view, but also from the point of view of the Tax Code.

Should - don't: don't guess with a daisy

If you are in doubt whether you need to open the OP or not, most likely the answer is yes, it is necessary. Please note that neither the Tax Code nor the Civil Code contain any restrictions on the number of employees of a separate division, as well as the absence of an order for its creation in internal documents.

There are difficult situations when it is really difficult to understand whether an OP occurs or not:

- We hire an employee in another city to provide services or perform work on the territory of clients (customers). Let's say a company provides cleaning services in another city and hires cleaners. In this case, there is no separate division, because there are no stationary jobs. A similar approach is applied to the situation when a worker (electrician, finisher) goes to the customer’s site. Depending on the position and type of occupation, the employee is drawn up with both a regular employment contract and an agreement on home-based or remote work.

- Construction work is underway. Here you need to consider each specific situation individually.

- Road works are being carried out. In this case, the Federal Tax Service believes that there is no need to create an OP. The work is being carried out “in the field”; there is no talk of any permanent location.

- Storage space is rented or purchased. This is one of the frequent subjects of controversy. There are permanent employees at the warehouse: storekeeper, watchman, loaders, which means that you will definitely need to register an OP.

- Premises in the same building. The company rents an office in a business center and decides to open a cafe on another floor. On the one hand, both premises are located in the same building and, naturally, belong to the same tax office, so it is logical to assume that there is no need to open an OP. The judges confirm this point of view, since they consider one of the signs of territorial isolation to be assigned to a tax inspectorate different from the parent enterprise. On the other hand, tax authorities do not always agree with arbitration practice. Their position is that even if in fact the legal address of the organization and the cafe differ slightly, for example, in the number of the premises, then formally such a difference is already a reason for registering the separate entity. The conclusion is drawn from the definition of OP in Article 11 of the Tax Code, the concepts established by Article 55 of the Civil Code of the Russian Federation and the determination of the location of a legal entity (according to paragraph 2 of Article 54 of the Civil Code, this is the place of state registration). You will either have to contact the Federal Tax Service for clarification, or act at your own peril and risk.

- The employee works in coworking mode. A popular way to work outside the home. Freelancers usually resort to it. The point is to engage in some kind of activity in a room where fellow “free artists” gather, perhaps in the process exchanging opinions, achievements and experiences, or simply working in a calm environment. Let’s imagine that a space is rented for an employee under a coworking agreement, is this equivalent to renting an office, is it necessary to organize an OP? In reality, this option involves a short-term rental, usually for a few hours a day, and the employer has no control over such a workplace. This means that it cannot be recognized as stationary and the creation of a separate unit is not required.

Note! Homeworkers and remote workers clearly do not have workplaces controlled by the employer.

Example No. 1: the construction site where the workers are sent is equipped with cabins owned by the organization, the workers are given tools by the employer, and he also controls the progress of the work - there is an OP.

Example No. 2: workers come to the construction site every day from home, safety at the site is monitored not by the employer (subcontractor), but by the general contractor, who also controls the progress of construction. Based on the definition of jobs (Article 209 of the Labor Code), there are none in this case, since construction is not under the control of the employer.

It should be noted that in most cases, tax authorities, regardless of the circumstances, believe that a construction site requires the creation of a separate division.

What if it’s just a room where goods or materials are delivered, unloaded, and picked up, if necessary, by visiting drivers and forwarders? Despite the fact that employees are not constantly in the warehouse, it is considered that there are jobs, and the time spent on them does not matter.

By the way! A similar approach is valid in a situation where an organization has rented or purchased an office, but the employee uses it occasionally.

After the company has decided to create an OP, it is necessary to prepare documents regulating its activities and register it with the Federal Tax Service.

"Separate" accounting

The business of any successful company sooner or later goes beyond the boundaries of its home office - the company opens first one, then a second separate division... The management of the organization may plan to create, for example, points of sale of products, purchase of raw materials, or a department of the main office that will engage in the same or different activities .

Therefore, all accounting specialists need to clearly understand how to set up and maintain records in company branches. After all, even if an accountant does not yet face such a problem, tomorrow he can get a job in a company that has departments. Therefore, firstly, he needs to find out what is hidden behind the concepts of a separate division, branch and representative office and whether there are differences between them. And secondly, it is important to understand the peculiarities of accounting and reporting of “isolated”. This article is devoted to these issues.

Civil division...

You can find out which units should be called separate from Article 55 of the Civil Code. Its first paragraph explains what a representative office is, and the second talks about branches.

What these concepts have in common is that they are both types of separate divisions and should be located outside the location where the main company is located. There is also a difference: representative offices can only act in the interests of the main office. Branches are already capable of performing all or some of its functions, as well as doing purely “representative” work.

Representative offices and branches are not legally independent. They are endowed with property by the parent organization, and they act on the basis of regulations approved by it. This is stated in paragraph 3 of Article 55 of the Civil Code.

The management of separate divisions operates on the basis of powers of attorney issued to them by the main company. The Code puts forward another mandatory condition for legitimate “isolation” - branches and representative offices must be indicated in the constituent documents of the company that created them.

As already about the property, in any case, it will be the property of the main company. Therefore, if the main company or branch is in debt to someone, valuables located both in the “main” and in the “separate” territories can be seized in court.

...and “tax-wise”

The Tax Code interprets “separateness” in its own way. The concept is disclosed in paragraph 2 of Article 11 of the Tax Code - this is any unit outside the territory of the company where the company has equipped permanent workplaces, that is, where personnel work for at least one month.

Note that for tax purposes, a separate division will be any department that meets the criteria of Article 11. Therefore, in this case, it does not matter at all whether the main company indicated the newly created branch in its constituent documents, whether there is a corresponding provision and whether the department has any official powers. The main thing is that a “big” company conducts its business activities through it.

Many accountants are concerned about the question of what is a territory outside the company. After all, the answer to it depends on whether the newly formed unit will be separate.

Let us turn to the concept of “location of the organization”, which is given in paragraph 2 of Article 54 of the Civil Code - this is the place of its state registration. The boundaries of the administrative territory, departments outside of which will be considered separate, can most easily be identified by the OKATO code (“All-Russian Classifier of Objects of Administrative-Territorial Division OK 019-95” approved by Gosstandart Resolution No. 413 of July 31, 1995). It is different for each area.

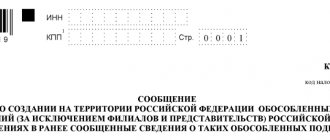

If a company has created, reorganized or closed a separate division, it is obliged to report this to the tax office at its location within one month from the start of its operation. Such requirements for companies are put forward by paragraph 4 of Article 83 of the Tax Code. The application must be submitted to the tax office using form No. 09-1-1 (approved by order of the Ministry of Taxation dated March 3, 2004 No. BG-3-09/178).

If the “separate” is lucky enough to gain a foothold in the territory of the same tax office as the parent company, the branch does not need to be registered. This conclusion is suggested not only by common sense, but also by the opinion of tax workers (for example, letter of the Ministry of Taxes dated August 8, 2001 No. ШС-6-14/613(a)). The inspectors indicated that taxpayers should be registered, and not their property in the area controlled by one inspection.

With a separate balance...

In order to properly conduct accounting in a company burdened with divisions, it is important for an accounting specialist to determine whether the “separate divisions” will have separate balance sheets.

In the current accounting legislation, the concept of a separate balance sheet is not disclosed. The Ministry of Finance shed light on the problem in its letter dated March 29, 2004 No. 04-05-06/27. Chief financiers noticed that such a concept as a “separate balance sheet” was excluded from PBU 4/99 “Accounting statements of an organization.” Therefore, according to the Ministry of Finance, organizations can independently determine the composition of information for management purposes. In the letter, the controllers defined a separate balance sheet - this is a list of information established by the company for its divisions. On their basis, the chief accountant will draw up financial statements for the entire organization.

Let's consider a situation where the parent company transferred the branch to a separate balance sheet. In this case, the division will maintain accounting records on its own.

It should be borne in mind that, according to paragraph 11 of PBU 1/98, the company’s accounting policies will also be valid for its “stand-alone” companies. For example, for the entire company, the methods of organizing accounting and tax accounting should be uniform. As well as methods for calculating depreciation, for example, of fixed assets.

As you know, an integral part of the accounting policy is the working chart of accounts. This is the only way the division's accounting methodology may differ from the main company. In fact, such accounting accounts as, for example, 80 “Authorized capital”, 75 “Settlements with founders” and 04 “Intangible assets” are of no use to the branch. The chief accountant must register the working charts of accounts of the “parent” and all “side” departments in the order on the accounting policies of the main company.

To reflect the calculations of the main company and division in accounting, the accountant should use account 79 “Intra-business calculations”. And to control the values that the main representative office has, it is best for him to use subaccount 79-1 “Calculations for allocated property.” The “flow” of values in the opposite direction is shown in the same subaccount by reverse posting.

Meanwhile, with such “circulation” implementation does not occur. After all, this concept is defined in paragraph 1 of Article 39 of the Tax Code. And there it is clearly stated that the implementation must be paid.

The “circulation” of property between the main accountant must be shown in the accounts of both, while for the division the posting must be reversed.

In addition, departments with an independent balance sheet, despite the fact that they prepare reports, should not submit them to the tax office (clause 8 of PBU 4/99). And the accounting information of the divisions should be included in the reporting of the main company.

Accounting will be correct if the balances on the debit of account 79-1 of the main company and the credit of the same division account are the same. When preparing reports for the company, the debit and credit of account 79 will cancel each other out and therefore will not be shown in the balance sheet.

What should the accounting specialist do with the rest of the accounts? When an accountant prepares the Income Statement and Capital Flow Statement, as well as the Balance Sheet and Cash Flow Statement, he needs to summarize the accounts of the division and the main company. In the last form, the accounting specialist does not need to show the “migration” of funds between the main and subordinate companies - turnover on accounts 50, 51, etc. in correspondence with 79 will be absent in the accounting reports.

The capital's controllers require departments to submit accounting reports to tax authorities throughout the company. They expressed this opinion in a letter from the Department of Tax Administration for Moscow dated January 27, 2004 No. 26-12/05494. In their reasoning, the inspectors referred to paragraph 1 of Article 83 of the Tax Code, which states that companies must register both at the location of the main company and its divisions. And from this they concluded that to all inspections where the organization itself or its branches are registered, it needs to submit a full set of reporting forms. After all, according to the controllers, it is not a separate division that is registered with the tax authorities, but the head office itself.

However, inspectors often require departments to report only on themselves. Therefore, what an accountant should come to the inspectorate with, he needs to find out in each specific tax office.

...and without

The above applies to the case where the main division has a separate balance sheet. What if the head office decided not to allocate a branch or representative office?

In this case, all accounting will be carried out by the accounting department of the main company. The facts of the economic life of a branch can be shown, for example, in the analytics of accounts in its accounting. Or on separate sub-accounts - depending on the accounting methodology adopted by the company and the preferences of the chief accountant. In this case, no accounting statements will exist separately for the division.

Opinion

Marat Smirnov, leading tax lawyer in the capital: “Accounting specialists often ask me what can be considered a stationary workplace. I will say right away that this concept is not clearly defined in the Tax Code. Therefore, let us turn to the Federal Law of July 17, 1999 No. 181-FZ “On the Fundamentals of Labor Safety”. Article 1 of the law states that a workplace is a territory where an employee needs to be or where he needs to arrive to work. However, it must be under the control of the company.

A large number of accountants have a logical question: if a company sent one employee to work in another municipality, can we talk about the emergence of a separate division there? For example, a company rented a small part of the space in a shopping center for a counter for one seller.

The inspectors answer this question in the affirmative. Thus, in a letter from the Ministry of Taxes and Taxes dated April 29, 2004 No. 09-3-02/1912, they noted that one employee is enough to talk about “isolation.”

By the way

“Osobeltsy”, who have a separate balance and current account, who independently pay their employees, are not enough to register only with the tax office. They also need to “register” with the Social Insurance Fund and the Pension Fund at the location of each department.

Such requirements for companies are spelled out in paragraph 3 of section I of the Procedure for registering legal entities as insurers at the location of separate divisions (approved by Resolution of the Federal Insurance Fund of March 23, 2004 No. 27) and paragraph 6 of section II of the Procedure for registering insurers making payments with the territorial bodies of the Pension Fund of the Russian Federation individuals (approved by Resolution of the Pension Fund Board of July 19, 2004 No. 97p).

Example

Two capital companies and Tkannon LLC simultaneously opened a separate division in the Moscow region. However, the first society “granted” him a separate balance, while the second did not.

The accountant of Dulip CJSC was faced with the task of recording in accounting the transfer of a batch of materials from the main company to the division in the amount of 10 thousand rubles. He made the following entries:

in the head office accounting

Debit 79-2 Credit 10

– 10,000 rub. – shows the transfer of materials to the warehouse of a remote department.

for department:

Debit 10 Credit 79-2

– 10,000 rub. – a batch of materials from the “parent” office was capitalized.

Then the general director of Dulip CJSC decided to organize another division in St. Petersburg. For ease of accounting, the company’s accountant created the following analytics on account 79 “Intra-business settlements”:

79-1 subaccount “Settlements for allocated property with a division in the Moscow region”;

79-1 subaccount “Settlements for allocated property with a division in St. Petersburg”;

79-2 subaccount “Settlements for current operations with the department in the Moscow region”;

79-2 subaccount “Settlements for current operations with the department in St. Petersburg”

.

In turn, the accounting specialist of Tkannon LLC, whose division does not have a separate balance sheet, created the following analytical subaccounts in accounting to control the movement of materials in the organization:

10-1 subaccount “Main company materials”;

10-1 subaccount “Materials of a separate division”;

90-1 subaccount “Revenue of the main company”;

90-1 subaccount “Revenue of the representative office in the Moscow region.”

For information

Branches and representative offices can issue a primary registration only with the details of the main company.

The requirements for setting up accounting in a separate division are listed in paragraph 3 of Article 6 of the Federal Law of November 21, 1996 No. 129-FZ “On Accounting”. In general, they are the same as for other companies, with the exception that the general director of the head office is responsible for the accounting policies and development of rules for document flow between the main organization and the “stand-alone” companies.

Danil POPOV

PRACTICAL ENCYCLOPEDIA OF AN ACCOUNTANT

Complete information about accounting rules and taxes for an accountant. Only a specific algorithm of actions, practical examples and expert advice. Nothing extra. Always up-to-date information.

Connect berator

Vesting and registration

I’ll make a reservation that if we are talking about the third type of units (others), then you just need to submit an application in form C-09-3-1. The decision to create a representative office or branch is made by a meeting of participants (Clause 1, Article 5 of Federal Law No. 14-FZ “On Limited Liability Companies”) with at least 2/3 votes, unless otherwise specified in the company’s charter. At the meeting, the position is adopted, a leader is elected, and the director of the organization issues an order.

The provision must include the following points:

- Location and name.

- Functions, rights and responsibilities.

- Functions of the manager, powers (it is worth indicating to whom the manager directly reports - the meeting of participants, the director, the general director, another official).

- Property information.

- The presence or absence of your own account, balance.

- Where payroll is calculated, at the head office or in a division.

You can also specify other points: internal reporting, rules for moving inventory, cash flow, etc.

Note! The registration period is one month from the date of creation (clause 1 of Order of the Ministry of Finance No. 114n dated November 5, 2009). A branch or representative office is reflected in the Unified State Register of Legal Entities after state registration.

For late registration of a company's division, fines may apply: 200 rubles – clause 1 of Art. 126 of the Tax Code of the Russian Federation for failure to submit information on time and 10% of income received (minimum 40,000 rubles) - clause 2 of Article 126 of the Tax Code of the Russian Federation for activities without registration with the tax authority.

In 2021, a bill was considered to increase liability for failure to submit (late submission) to the Federal Tax Service of information on opening an OP and increasing it to the level specified in paragraph 2 of Art. 126 of the Tax Code, but in November 2021 it was rejected during consideration by the State Duma.

Property Relocation: Accounting

When moving inventory, fixed assets and money between the head office and other departments, the method of accounting depends on whether the OP has a dedicated balance sheet.

Important! All divisions maintain accounting records in accordance with the accounting policies of the “head”.

There is no separate balance

In this case, when moving, for example, equipment (OS), an internal transfer should be carried out in analytics.

Example No. 3: transfers to division “A-1” a lathe with an initial cost of 150,000 and depreciation accrued at the time of transfer in the amount of 54,000:

- D 01 "A-1" K 01 "A" - 150000, movement carried out.

- D 02 “A” D 02 “A-1” – 54000, depreciation on the transferred machine was transferred.

The same should be done with other inventory items. When a division does not have a separate balance sheet, cash is handled by the central accounting department, and settlements with suppliers and contractors are carried out through it. In this case, normal postings are performed.

Example No. 4: Organization “B” transfers to division “B-2” materials intended for the repair of the premises in which the OP is located, costing 20,000 rubles. To transport them, “B” hires a transport company (TC), its services cost 3,000 rubles:

- D 10.8 materials in the warehouse in “B-2” K 10.8 materials in the warehouse “B” - 20,000, materials were transferred to OP “B-2”.

- D 23 (23, 25, 20, 44) K 76 – 3000, reflects the costs of transporting materials for repairs.

- D 76 K 51 – 3000, paid for TK services.

There is a separate balance

In this case, account 79 “Intra-business settlements” is used to move property and funds.

When transferring fixed assets in the accounting of the head office, it is necessary to make the following entries (we use the data from example No. 3):

- D 79-1 “A-1” K 01 “A” - 150000, the transfer of equipment is reflected.

- D 02 “A” D 79-1 “A-1” – 54000, depreciation on the machine was transferred.

Postings when transferring inventory items and paying the costs of their delivery (we use the data from example No. 4): D 79-1 “B-2” K 10-8 – 20000, materials for repairs were transferred. Further postings depend on whether the department has a current account.

No invoice (services ordered and paid for by central accounting):

- D 23 (...) K 76 – 3000, transportation costs.

- D 76 K 51 – 3000, payment to the transport company.

There is no invoice (the order for services is made by the OP, and payment is made by the parent organization):

- D 79-2 K 76 - the unit transferred the debt to the TC to the “head”. In accounting for the separation itself, the postings will be as follows: D 23 (...) K 76 - 3000, transportation costs, D 76 K 79-2 - the TC debt was transferred to the head office.

- D 76 K 51 – paid for TC services

No invoice (OP independently ordered and paid for the services):

- For division “B-2”: D 23 (...) K 76 - 3000, transportation costs are reflected, D 76 K 51 - payment to TC is transferred.

- The OP can first receive funds for expenses, then in postings “B-2” there will be posting D 51 K 79-2 - funds have been received from the central accounting department for settlements. In this case, wiring D 79-2 K 51 will be reflected in the “head” control unit.

In most cases, the wiring looks like a mirror image, as you've probably noticed. Costs incurred are transferred to the central office by posting D 79-2 K 20, 25, 23, 44. Reverse posting, respectively, is from the head accounting department.

You can read more about taxation in a separate division here.

Tax accounting in organizations with separate divisions

Branches, representative offices and other separate divisions are not independent taxpayers. They only fulfill the duties of parent organizations for the payment of taxes and fees at their location (Article 19 of the Tax Code of the Russian Federation). For some taxes, separate divisions also submit reports to the tax authorities at the place of their registration.