“Our organization uses the simplified tax system. In 2021, we plan to open an additional branch - a branch or just an additional office (not decided yet). In this case, will we lose the right to use the simplified tax system? Does it matter where the new division of the organization will be located: in the same subject of the Russian Federation with the head office or in different subjects? Will I need to register with the tax authority again? What tax reports will need to be submitted and where?” These are the questions our reader asked us. The answers are in the material provided.

HOW TO RETAIN THE RIGHT TO APPLY SYSTEM WHEN OPENING A DIVISION OF AN ORGANIZATION?

The use of a special tax regime - the simplified tax system - has a number of undeniable advantages that attract taxpayers, but there are also restrictions established by Chapter. 26.2 Tax Code of the Russian Federation. One of them is a ban on the use of the simplified tax system by organizations that have branches (clause 1, clause 3, article 346.12 of the Tax Code of the Russian Federation).

The Tax Code does not contain the concepts of “branch”, “representative office”, “additional office” (or similar). Article 11 of the Tax Code of the Russian Federation defines one general concept - “a separate division of an organization.”

The main features of a separate division of an organization are:

- territorial isolation from the organization;

- equipment of stationary workplaces at the location of this unit;

- independence from reflecting the fact of creating a separate division in the constituent or other documents of the organization;

- independence from the amount of authority vested in this unit.

Let's talk separately about the workplaces of a separate unit. To be recognized as a separate division of an organization, workplaces must be stationary. Based on Art. 209 of the Labor Code of the Russian Federation, a workplace is a place where an employee must be or where he needs to arrive in connection with his work and which is directly or indirectly under the control of the employer. For these purposes, a workplace is considered stationary if it is created for a period of more than one month.

The equipment of the workplace means the creation of all the conditions necessary for the performance of work duties, as well as the very performance of these duties.

Let us note that the legislation does not specify the exact territorial location of the division and the location of the head office of this division (Letter of the Ministry of Finance of Russia dated October 29, 2015 No. 03-11-06/62392). In this case, the territorial isolation of the unit from the organization is determined by an address different from the address of the specified organization (Letter of the Ministry of Finance of Russia dated August 18, 2015 No. 03-02-07/1/47702). Accordingly, for the purposes of applying the simplified tax system, it does not matter where the separate division of the organization is located: in the same subject of the Russian Federation with the parent organization or in different ones.

Thus, an organization that opens a separate division has the right to continue to use the simplified tax system only if this separate division is not a branch. Tax legislation does not contain a separate concept of “branch”, and therefore, on the basis of clause 1 of Art. 11 of the Tax Code of the Russian Federation, the designated concept is applied in the meaning in which it is used in the norms of civil law.

The concept of “branch” is given in Art. 55 Civil Code of the Russian Federation. Main features of a branch:

- this is a separate division of a legal entity located outside its location;

- the branch carries out all the functions of a legal entity or part thereof, including the functions of a representative office;

- it is not a legal entity;

- the branch is endowed with the property of the legal entity that created it;

- he acts on the basis of provisions approved by the legal entity;

- the head of the branch is appointed by a legal entity and acts on the basis of his power of attorney;

- The branch is listed in the Unified State Register of Legal Entities.

It follows from these rules that if the creation of a separate division of an organization is not properly formalized as a branch of a legal entity, including if the branch is not indicated in the constituent documents of the organization and in the Unified State Register of Legal Entities, then this organization has the right to continue to apply the simplified tax system subject to compliance with the norms established by Chapter . 26.2 of the Tax Code of the Russian Federation (letters of the Ministry of Finance of Russia dated October 29, 2015 No. 03-11-06/62392, dated October 14, 2015 No. 03-11-06/2/58685).

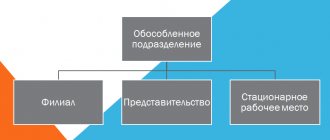

What applies to separate divisions of the organization

The concept of separate divisions is formulated in civil and tax legislation (Article 55 of the Civil Code of the Russian Federation, paragraph 2 of Article 11 of the Tax Code of the Russian Federation). Only a legal entity can create them, and for recognition of a division as such, it does not matter whether its creation is enshrined in the constituent documents of the company or not. For each division, a regulation is drawn up and an order is issued on its creation, as well as on the appointment of its leader.

There are the following types of separate divisions:

- branches - structures endowed with the greatest independence and scope of powers, have the right to conduct business activities, which are carried out by the parent company;

- representative offices are less independent units engaged in representing and protecting the interests of the parent company, while being deprived of the right to do business;

- other OPs, as a rule, are remote workplaces for specialists, fully managed by the head office.

All separate divisions must be located at an address different from the location of the organization itself and have stationary workplaces. Such places are recognized as places created for a period of at least 1 month.

Branches and representative offices must be included in the Unified State Register of Legal Entities, and there is no requirement to notify the Federal Tax Service about their creation. These divisions can be allocated to a separate balance sheet and have the right to open bank accounts on behalf of the organization.

The tax office must be notified of the organization’s opening of other separate divisions, but no changes are made to the Unified State Register of Legal Entities. They do not have separate bank accounts and do not do their own accounting.

DO I NEED TO REGISTER WITH THE TAX AUTHORITY WHEN CREATING A SEPARATE DIVISION?

If an organization using the simplified tax system has decided to create a separate division (in any form, except for a branch), then it is obliged to register for taxation at the location of this separate division (clause 1 of article 83 of the Tax Code of the Russian Federation).

Let us immediately make a reservation that the organization that opened a representative office has the right to continue to use the simplified tax system. A representative office is a separate division of a legal entity located outside its location, which represents the interests of the legal entity and protects them. The remaining criteria for a representative office coincide with the criteria for a branch. Accordingly, the registration authority has information about the opening of a representative office, since it must be indicated in the Unified State Register of Legal Entities. Therefore, registration with the tax authorities of a Russian organization at the location of the representative office is carried out on the basis of information contained in the Unified State Register of Legal Entities. A legal entity, within three working days from the moment of creation of a representative office, is obliged to inform the registration authority at its location about this (Clause 5, Article 5 of the Federal Law of 08.08.2001 No. 129-FZ “On State Registration of Legal Entities and Individual Entrepreneurs”) . There is no need to register a representative office of the organization separately for tax purposes.

Since the vast majority of organizations open separate divisions that are not a representative office (hereinafter referred to as a separate division), we will consider their features of tax registration.

Firstly, since data on the creation of the named separate division is not submitted to the registration authority and is not entered either into the constituent documents or into the Unified State Register of Legal Entities, the organization is obliged to register for tax purposes at the location of this separate division.

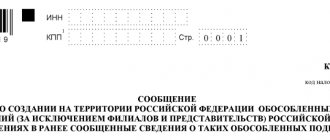

Secondly, registration with the tax authorities of a Russian organization at the location of its separate divisions is carried out by tax authorities on the basis of messages submitted (sent) by this organization in accordance with clause 2 of Art. 23 Tax Code of the Russian Federation. The organization submits a notification on the creation of a separate division in the form S-09-3-1 “Notification on the creation on the territory of the Russian Federation of separate divisions (except for branches and representative offices) of a Russian organization and on changes to previously reported information about such separate divisions”, approved by the Order Federal Tax Service of Russia dated 06/09/2011 No. ММВ-7-6/ [email protected]

Note:

As a general rule, a notification about the creation of a separate division is submitted to the tax authority at the location of the separate division.

Only if several separate divisions of an organization are located in one municipality, the federal cities of Moscow, St. Petersburg and Sevastopol in territories under the jurisdiction of different tax authorities, the organization can be registered by the tax authority at the location of one of its separate divisions . The organization determines this independently. The organization indicates information about the choice of tax authority in a notification, the form of which is approved by Order of the Federal Tax Service of Russia dated August 11, 2011 No. YAK-7-6 / [email protected] and which is submitted to the tax authority at its location.

According to paragraph 9 of Art. 83 of the Tax Code of the Russian Federation, if a taxpayer has difficulty determining the place of registration with the tax authority, a decision based on the data submitted by him (including documents, information about the activities of the organization through a separate division) is made by the tax authority.

Thirdly, specific deadlines have been established for reporting to the tax authority:

- on the creation of a separate division - within one month from the date of creation of a separate division of the Russian organization. The specified period is calculated from the beginning of the organization’s activities through the corresponding separate division (Letter of the Ministry of Finance of Russia dated February 19, 2016 No. 03-02-07/1/9377);

- on changes in information about a separate division - within three days from the date of change in the relevant information;

- on termination of the activities of a separate division - within three days from the date of termination of said activities.

The process of tax registration of a separate division is completed by the fact that the tax authority carries out registration within five days from the date of receipt of the message from this organization and, at the same time, issues (or sends electronically) a notice of registration with the tax authority, which indicates the checkpoint of a separate unit.

Thus, if an organization using the simplified tax system has decided to create a separate division, then it is obliged to register for taxation at the location of this division. To do this, you need to submit a message in form C-09‑3‑1 within one month from the date of creation of a separate unit.

Since today there is no single position under which article of the Tax Code of the Russian Federation to hold accountable for violating the deadline for registering a separate division - under Art. 126 (fine 200 rubles) or according to paragraph 2 of Art. 116 of the Tax Code of the Russian Federation (fine in the amount of 10% of income received during work without tax registration, but not less than 40,000 rubles) - we recommend compliance with the law (letter of the Ministry of Finance of Russia dated 09/03/2012 No. 03‑02‑07/ 1‑211, dated 04/17/2013 No. 03‑02‑07/1/12946).

Notification of the Federal Tax Service on the opening of an OP

It is mandatory to notify the Federal Tax Service at the place of registration of the legal entity about each created OP. faces. This is necessary in order to register the unit with the Federal Tax Service office at its actual location.

To do this, a message informing about this fact must be sent to the tax office where the company is registered within a month from the date of opening of a separate division. No other documents are required to be provided. After receiving the notification, within 5 days the local Tax Service will itself register the above-mentioned division (Articles 83, 84 of the Tax Code of the Russian Federation).

A notification about the creation of a unit is provided to the Federal Tax Service in one of three possible ways: transmitted during a personal visit, sent to the inspection address by mail with notification, or via telecommunication channels (electronic version).

Failure to comply with the established deadline for filing a notification (a month from the date of opening of the unit) entails the application of punitive measures to the violating organization, namely, a fine in the amount of 10 thousand rubles. In addition to the Federal Tax Service, other funds must be notified about the creation of a separate division: the Social Insurance Fund, the Pension Fund of the Russian Federation at the place of registration of the company. The notification is drawn up in any form, and exactly one month is allotted for its submission.

Similar articles

- Registration of a separate subdivision 2021: step-by-step instructions

- How to create a separate division of an LLC?

- Order on the creation of a separate division

- Order to close a separate division: sample

- 6 Personal income tax for separate divisions

DECLARATION OF TAX PAYABLE UNDER SUMMARY.

We are considering a case where an organization using the simplified tax system has created a separate division. In this situation, she continues to use the “simplified approach” while fulfilling all the restrictions established by Chapter. 26.2 Tax Code of the Russian Federation.

Note that the simplified tax system is applied by the entire organization as a whole, including a separate division. Chapter 26.2 of the Tax Code of the Russian Federation does not contain requirements for separate accounting of goods sold, work performed or services provided in the parent organization and separate divisions.

Thus, an organization using the simplified taxation system keeps tax records of its activity indicators necessary to calculate the tax base and the amount of tax paid under the simplified taxation system for the organization as a whole, taking into account all income received and expenses incurred, regardless of where exactly these incomes were received and expenses were incurred: in the parent organization or a separate division.

In accordance with paragraph 6 of Art. 346.21 of the Tax Code of the Russian Federation, payment of tax and advance payments for tax under the simplified tax system is made at the location of the organization. When calculating the “simplified” tax, it does not matter in which city (region) of the Russian Federation the separate division was created.

Based on the results of the tax period, taxpayers submit a tax return to the tax authority at the location of the organization (Article 346.23 of the Tax Code of the Russian Federation).

Accordingly, at the location of the separate division, tax under the simplified tax system is not paid and a tax return is not submitted (letters from the Federal Tax Service for Moscow dated 08/31/2010 No. 16‑15/ [email protected] , dated 06/22/2011 No. 16‑15/ [email protected ] ).

Application of the simplified tax system in the presence of a separate division

There are no special rules for maintaining tax records and accounting under the simplified tax system for organizations with separate divisions, since the responsibility for maintaining records is assigned to the parent organization. The presence or absence of separate divisions in an organization does not affect the accounting procedure. Reporting according to the simplified tax system (KUDIR, declaration) is maintained by the head office; there is no need to separately generate reports on the income of separate divisions.

It is necessary to submit a tax return, as well as pay tax and advance tax payments at the place of registration of the main organization. If an organization has separate divisions, unified financial statements are also submitted. Reports must be submitted at the end of the year to the tax office and Rosstat at the place of registration of the parent organization. But do not forget that personal income tax for department employees is paid locally.

Please note that for a separate division you do not need to open a separate current account, since if you have a current account different from the parent organization, the division is considered a branch, and your organization will lose the right to apply the simplified tax system.

Important!

For information

09/01/2011Moscow Tax Courier magazine

An organization has the right to apply the simplified tax system when creating a separate division, if it is not a branch (representative office), and the average number of employees of the organization, taking into account the employees of the separate division, does not exceed 100 people.

In this case, the company submits a declaration at the place of its state registration.

Tax accounting of performance indicators is carried out for the organization as a whole, taking into account all income received and expenses incurred, regardless of where exactly these incomes were received and expenses were incurred: in the parent organization or a separate division.

In accordance with subparagraph 1 of paragraph 3 of Article 346.12 of the Tax Code of the Russian Federation, organizations with branches and (or) representative offices do not have the right to apply the simplified tax system. A separate division of an organization is any division territorially isolated from it, at the location of which stationary workplaces are equipped (Article 11 of the Tax Code of the Russian Federation).

A separate division is recognized as such regardless of whether its creation is reflected or not reflected in the constituent or other organizational and administrative documents of the organization, and on the powers vested in the specified division.

A workplace is considered stationary if it is created for a period of more than one month.

Representative offices and branches are endowed with property by the legal entity that created them and act on the basis of the provisions approved by it. Representative offices and branches must be indicated in the constituent documents of the legal entity that created them.

Thus, if an organization has created a separate division that is not a branch or representative office, and is not indicated as such in the organization’s constituent documents, it has the right to continue to apply the simplified taxation system.

At the same time, it should be noted that, according to paragraph 1 of Article 346.12 of the Tax Code of the Russian Federation, taxpayers are organizations that have switched to a simplified taxation system and apply it in the manner established in Chapter 26.2 of the Tax Code of the Russian Federation.

According to paragraph 6 of Article 346.21 of the Tax Code of the Russian Federation, payment of the single tax and advance payments is made at the location of the organization, that is, at the place of its state registration. In accordance with paragraph 1 of Article 346.23 of the Tax Code of the Russian Federation, an organization submits a tax return at the place of its state registration.

At the location of the separate division, the single tax is not paid and the tax return is not submitted.

Thus, an organization applying the simplified tax system keeps tax records of its activity indicators necessary for calculating the tax base and the amount of a single tax for the organization as a whole, taking into account all income received and expenses incurred, regardless of where exactly these incomes were received and expenses incurred : in the parent organization or a separate division.

When calculating the single tax when applying the simplified tax system, it does not matter in which city (region) of Russia the separate division was created.

— for compulsory pension insurance;

— compulsory social insurance in case of temporary disability and in connection with maternity;

— compulsory health insurance;

— compulsory social insurance against industrial accidents and occupational diseases.

FIRST CAPITAL LEGAL CENTER. Moscow, Georgievsky per., 1, building 1, 2nd floor; (495) 649-11-65

The organization applies the simplified tax system with the object of taxation being income reduced by the amount of expenses.

It creates a separate division that is not a branch or representative office, is not indicated as such in the organization’s constituent documents, and does not have a separate balance sheet or current account.

Can an organization continue to use the simplified tax system? Where is the tax calculated in connection with the application of the simplified tax system paid? How can an organization keep tax records of its activity indicators necessary for calculating the tax base and the amount of a single tax on the basis of a unified Book of Income and Expenses, regardless of where they were received:

In this case, the company submits a declaration at the place of its state registration.

Tax accounting of performance indicators is carried out for the organization as a whole, taking into account all income received and expenses incurred, regardless of where exactly these incomes were received and expenses were incurred: in the parent organization or a separate division.

In accordance with subparagraph 1 of paragraph 3 of Article 346.12 of the Tax Code of the Russian Federation, organizations with branches and (or) representative offices do not have the right to apply the simplified tax system. A separate division of an organization is any division territorially isolated from it, at the location of which stationary workplaces are equipped (Article 11 of the Tax Code of the Russian Federation).

A separate division is recognized as such regardless of whether its creation is reflected or not reflected in the constituent or other organizational and administrative documents of the organization, and on the powers vested in the specified division.

According to Article 55 of the Civil Code of the Russian Federation, a representative office is a separate division of a legal entity, which is located outside its location, represents the interests of the legal entity and protects it.

A branch is a separate division of a legal entity located outside its location and performing all or part of its functions, including the functions of a representative office.

Representative offices and branches are endowed with property by the legal entity that created them and act on the basis of the provisions approved by it. Representative offices and branches must be indicated in the constituent documents of the legal entity that created them.

Thus, if an organization has created a separate division that is not a branch or representative office, and is not indicated as such in the organization’s constituent documents, it has the right to continue to apply the simplified taxation system.

At the same time, it should be noted that, according to paragraph 1 of Article 346.12 of the Tax Code of the Russian Federation, taxpayers are organizations that have switched to a simplified taxation system and apply it in the manner established in Chapter 26.2 of the Tax Code of the Russian Federation.

According to paragraph 6 of Article 346.21 of the Tax Code of the Russian Federation, payment of the single tax and advance payments is made at the location of the organization, that is, at the place of its state registration. In accordance with paragraph 1 of Article 346.23 of the Tax Code of the Russian Federation, an organization submits a tax return at the place of its state registration.

At the location of the separate division, the single tax is not paid and the tax return is not submitted.

Thus, an organization applying the simplified tax system keeps tax records of its activity indicators necessary for calculating the tax base and the amount of a single tax for the organization as a whole, taking into account all income received and expenses incurred, regardless of where exactly these incomes were received and expenses incurred : in the parent organization or a separate division.

REPORTING ON NDFL.

If an organization using the simplified tax system opens a separate division, then it, being a tax agent for personal income tax, must be ready to pay tax and submit reports for personal income tax (f. 2-NDFL and 6-NDFL) both at its location and at the location the location of each of its own separate divisions (clause 7 of article 226, clause 2 of article 230 of the Tax Code of the Russian Federation). At the location of the separate division, personal income tax is paid and personal income tax reporting is submitted in relation to the employees of these separate divisions, as well as in relation to individuals who received income under civil contracts concluded by the separate division.

Note that if an organization has several separate divisions, then the payment of personal income tax and the submission of personal income tax reporting must be made both at the location of the parent organization and at the location of each division. In Letter No. 03‑04‑06/77778 dated December 23, 2016, representatives of the Ministry of Finance recalled that Ch. 23 of the Tax Code of the Russian Federation does not contain rules granting tax agents with separate divisions the right to independently choose a separate division through which tax transfers and, accordingly, personal income tax reporting would be submitted.

Representatives of the Federal Tax Service adhere to a similar opinion: the obligation of tax agents to submit calculations in Form 6-NDFL to the tax authority at the place of their registration corresponds with the obligation of tax agents to pay the total amount of tax calculated and withheld by the tax agent from the taxpayer in respect of whom he is recognized as the source of payment of income, to the budget at the place of registration of the tax agent with the tax authority (letters dated 10/05/2016 No. BS-4-11/ [email protected] , dated 11/09/2016 No. BS-4-11/ [email protected] , dated 11/25/2016 No. BS -4-11/22430).

CALCULATION OF INSURANCE PREMIUMS.

The procedure for paying insurance premiums, as well as submitting reports - calculating insurance premiums - does not depend on the applied tax regime, but is associated with the presence or absence of separate divisions of the organization (Article 431 of the Tax Code of the Russian Federation).

The legislator directly stated that the payment of insurance premiums and the submission of calculations for insurance premiums are carried out by the following organizations:

- at their location;

- at the location of the separate units.

But in this case we are not talking about all separate divisions of the organization, but only about those that accrue payments and other remuneration in favor of individuals (with the exception of separate divisions located outside the Russian Federation). The decision to vest a separate division established on the territory of the Russian Federation with the authority to accrue payments and rewards in favor of individuals is made by the payer of insurance premiums independently (letters of the Federal Tax Service of Russia dated December 28, 2016 No. AS-4-11/25226, dated February 3, 2017 No. BS -4-11/ [email protected] ).

Accordingly, if a separate division of an organization does not independently calculate salaries and other payments to its employees, this is done centrally, then insurance premiums are paid and reporting on them is submitted only at the location of the parent organization.

If, according to the regulations on a separate division, payments to employees of this division are accrued by a separate division, then it independently pays insurance premiums and submits a calculation of insurance premiums at its location. The parent organization separately performs these responsibilities.

LAND TAX DECLARATION.

Since “simplified people” are payers of land tax on a general basis, we note that, according to clause 3 of Art. 397 and paragraph 1 of Art. 398 of the Tax Code of the Russian Federation, tax and advance payments for land tax are paid by taxpayer organizations to the budget at the location of land plots recognized as the object of taxation (Letter of the Ministry of Finance of Russia dated October 17, 2016 No. 03‑05‑06‑02/60364).

At the end of the tax period, taxpayers-organizations submit a land tax declaration to the tax authority also at the location of the land plot.

Thus, the presence of a separate division does not affect the procedure for paying land tax and submitting a declaration on it.

Branch as a constraint

In fact, whether a separate unit can use the simplified tax system directly depends on the type of this OP. According to one of the criteria, the fact of creation:

- is reflected in the Unified State Register of Legal Entities (branches and representative offices);

- does not appear in this state register in any way.

As a result, of all possible types of “separate structures” for the simplified tax system, only the creation of a branch imposes a restriction (subclause 1, clause 3, article 346.12 of the Tax Code of the Russian Federation). Then there can be no talk of any simplified taxation system. The right to the simplified tax system will be lost from the quarter in which information about the branch will be reflected in the Unified State Register of Legal Entities (clause 4 of article 346.13 of the Tax Code of the Russian Federation).

PROPERTY TAX DECLARATION.

Since “simplified” organizations, as a general rule, are not payers of corporate property tax, we will consider only one case when they pay property tax - when they are the owners (or have the right of economic management) of real estate, in respect of which the tax base is determined as cadastral value and which is included in the corresponding list (Article 378.2 of the Tax Code of the Russian Federation).

Based on Art. 384, 385 and 385.2 of the Tax Code of the Russian Federation, payment of the property tax of organizations is carried out at the location of the organization, at the location of a separate division of the organization that has a separate balance sheet, as well as at the location of other real estate objects located outside the location of the organization or its separate division (Letter from the Ministry of Finance of Russia No. 03‑05‑06‑02/60364).

Taking into account the features established by clause 13 of Art. 378.2 of the Tax Code of the Russian Federation, an organization that uses the simplified tax system and has a separate division regarding real estate objects, the tax base for which is determined as the cadastral value, pays tax (advance tax payments) to the budget at the location of each of the specified real estate objects.

Calculations for advance tax payments and tax returns are submitted in a similar manner (Article 386 of the Tax Code of the Russian Federation).

TRANSPORT TAX DECLARATION.

If an organization that uses the simplified tax system and has a separate division has a vehicle registered as an object of taxation, then it is a payer of transport tax.

Payment of transport tax and advance payments of tax is made by taxpayers to the budget at the location of the vehicles; The tax return is also submitted to the tax authority at the location of the vehicles (Articles 363, 363.1 of the Tax Code of the Russian Federation). The location of the vehicle is determined in Art. 83 Tax Code of the Russian Federation.

A vehicle can be registered with the State Traffic Safety Inspectorate either at the location of the parent organization (at the place of state registration) or at the location of a separate unit (clause 24.3 of Appendix 1 to Order of the Ministry of Internal Affairs of Russia dated November 24, 2008 No. 1001 “On the procedure for registering vehicles ").

Consequently, if, for example, a car is registered with the traffic police at the location of a separate unit, then the tax must be paid to the budget at the location (registration) of this separate unit and a transport tax declaration must be submitted there.