A newly created LLC quite often does not have its own or rented office and is listed only at its legal address. This may be the home address of the manager (founder) or an address with postal and secretarial services. While no real activity is being carried out yet, and correspondence intended for the LLC, especially from official bodies, arrives in a timely manner, this situation is normal. But, sooner or later, the LLC begins to work, which means it must “materialize” somewhere in space.

You can get answers to any questions about registering LLCs and individual entrepreneurs using the free business registration consultation :

Free consultation on business registration

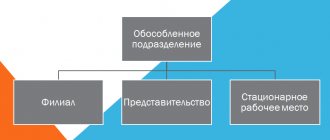

Sometimes the nature of the activity allows you to conduct business from home or with the help of remote workers, but if an LLC opens a store, warehouse, office, production facility, or in some other way begins to operate at an address other than its legal address, then it is necessary to create and register a separate division .

There is an important condition here - the criterion for creating a separate unit is the presence of at least one stationary workplace , and it is recognized as such if it is created for a period of more than one month. The concept of a workplace is in the Labor Code (Article 209), from which we can conclude that:

- an employment contract must be concluded with the employee;

- the workplace is under the control of the employer;

- the employee is constantly in this place in accordance with his job duties.

Based on this, a storage warehouse that does not have a permanent employee will not be considered a separate unit. Vending machines, payment terminals, ATMs, etc. are not considered as such. Remote (remote) workers also do not fall under the concept of a “stationary workplace”, therefore concluding employment contracts with them does not require the creation of a separate unit.

Please note that individual entrepreneurs should not create and register separate divisions . Individual entrepreneurs can operate throughout the Russian Federation, regardless of the place of state registration. If they work under the UTII regime or have purchased a patent, they only have to additionally register for taxation at the place of business.

What should a separate division be like for an organization to have the right to the simplified tax system?

Article 346.12 of the Tax Code of the Russian Federation prohibits the use of a preferential simplified taxation system for organizations that have branches (the requirement for the absence of a representative office has already been abolished). Of course, the question arises - how to register a separate division so that it is not recognized as a branch, and at the same time the organization retains the right to the simplified tax system? To understand this, you will have to refer to the provisions of three codes: Tax, Civil and Labor:

- The Tax Code (Article 11) gives the concept of a separate division of an organization as “... any territorially separate division from it, at the location of which stationary workplaces are equipped.” However, the Tax Code of the Russian Federation does not provide a description of the types of separate divisions.

- The Civil Code (Article 55) characterizes a separate division only in the form of a representative office and a branch . That is, from these provisions it is also unclear what other separate divisions, besides a representative office and a branch, can be.

- The Labor Code (Article 40) indicates that “... a collective agreement can be concluded in the organization as a whole, in its branches, representative offices and other separate structural units .” Thus, only here can one see that separate divisions can be something other than a branch and representative office.

As a result, we are dealing with some elusive concept of another separate division, therefore, when creating such a division, we must simply avoid the criteria that characterize it as a branch or representative office. These characteristics in the law are more than meager:

- a representative office is a separate division of a legal entity located outside its location, which represents the interests of the legal entity and protects them;

- a branch is a separate division of a legal entity located outside its location and performing all or part of its functions, including the functions of representative offices;

- representative offices and branches are not legal entities, and information about them must be indicated in the Unified State Register of Legal Entities, and therefore in the organization’s charter.

It is no coincidence that we understand this issue in such detail, because non-compliance with these requirements (sometimes implicit) can deprive an organization of the opportunity to work on the simplified tax system, and unexpectedly. For example, the manager believes that the created separate division is not a branch, so the organization continues to work on a simplified system, although it no longer has the right to do so.

In such cases, the organization will be recognized as operating under the general taxation system from the beginning of the quarter in which a separate division with the characteristics of a branch was created. And the loss of the right to simplification leads to the need to charge all general taxes: profit tax, property tax, VAT, and it is with the latter that the most problems can arise. VAT must be charged on the cost of all goods, works and services sold for the current quarter, and if the buyer or customer refuses to pay it additionally, then the tax will have to be paid at their own expense.

Entrepreneur and separate division

Entrepreneurs, wondering whether an individual entrepreneur can have a separate division (hereinafter also referred to as an OP), often do not proceed from the legally established concept of an OP, but are based on some idea of a form of entrepreneurial activity with an extensive network, carried out on behalf of one person.

Therefore, in order to dispel illusions and eliminate misunderstandings in this matter, it is necessary to refer to the definition of the concept of “separate division”, which is established by the legislation of the Russian Federation.

From paragraphs 1, 2 of Article 11 of the Tax Code of the Russian Federation and Article 55 of the Civil Code of the Russian Federation, it follows that a separate division of a legal entity is understood as a branch, representative office or other division of an organization, the location of which does not coincide with the parent organization.

Thus, the creation of a separate division in the sense given to it by civil and tax legislation is the prerogative of legal entities, not individuals.

It should also be taken into account that, on the basis of paragraphs 1, 3 of Article 23 of the Civil Code of the Russian Federation, from the moment of appropriate registration as an individual entrepreneur, an individual has the right to carry out commercial activities and is subject to part of the norms of civil legislation regulating the activities of organizations. However, based on the essence of legal relations for the creation of an OP, the corresponding rules are not applicable to individual entrepreneurs.

Signs of a branch and representative office

Considering what unpleasant consequences recognition of a separate division as a branch can lead to for the simplified tax system payer, you need to know what its signs may be:

- The fact of the creation and commencement of activities of a branch or representative office is reflected in the charter of the LLC (from 2021 this is not necessary).

- The parent organization approved the regulations on the branch or representative office.

- A head of a separate division has been appointed, who acts by proxy.

- Internal regulatory documents have been developed to regulate the activities of a separate division, as a branch or representative office.

- A branch or representative office represents the interests of the parent organization before third parties and protects its interests, for example, in court.

Thus, in order to retain the right to the simplified tax system, it is necessary to ensure that the created separate division does not have the indicated characteristics of a branch. In addition, it is necessary to indicate in the Regulations on a separate division that it does not have the status of a branch or representative office and does not conduct the business activities of the organization in full (for example, a store is engaged only in the storage, sale and delivery of goods). The creation of a separate division is within the competence of the head of the LLC; it is not necessary to include information about this in the charter.

We inform the tax office about the opening of a separate division

According to Article 83(1) of the Tax Code of the Russian Federation, organizations must register for tax purposes at the location of each of their separate divisions. An additional requirement to report to the tax inspectorate about all separate divisions (within a month) and changes in information about them (within three days) is established by Article 23(3) of the Tax Code of the Russian Federation.

Thus, when creating a separate division (that is not a branch or representative office), the LLC must:

- report this to your tax office using form No. S-09-3-1, approved by order of the Federal Tax Service of Russia dated 06/09/2011 No. ММВ-7-6/ [email protected] ;

- register with the tax authorities at the location of this unit, if it was created in a territory under the jurisdiction of a tax office other than the one in which the head office is registered.

The tax inspectorate at the place of registration of the head office, to which message No. S-09-3-1 was submitted, itself reports this fact to the Federal Tax Service at the location of the created separate division (Article 83(4) of the Tax Code of the Russian Federation), that is, from the LLC you do not need to register yourself.

If several separate divisions are located in the same municipality, but in territories under the jurisdiction of different tax inspectorates, registration can be carried out at the location of one of the separate divisions, at the choice of the organization. For example, if in one city an LLC has several stores open in the territories of different Federal Tax Service, you do not need to register with each of them, you can select one inspection, indicating this choice in the message.

If the address of a separate division changes, it does not need to be closed and re-opened (such an obligation existed until September 2010), but only to submit a message in form No. S-09-3-1 to the tax office at the place of registration of the division indicating the new address.

Economic activities of a separate division

Information about branches and representative offices is in the extract from the Unified State Register of Legal Entities and in the charter, but divisions that are neither one nor the other may not be there. In this case, an outsider can only find out information about the existence of divisions in an unofficial way - for example, by asking management.

TIN is not assigned to any type of unit, but KPP and OKTMO are assigned to all, regardless of the availability of an application for assignment of a number. OKTMO is the territorial code of the municipality where the unit operates, and KPP is the code for the reason for registration. Also, a branch or representative office may have separate details of a current account registered in the name of the main company.

A separate division pays taxes for its activities independently and at its location, but on behalf of a legal entity (Article 19 of the Tax Code of the Russian Federation). So it fulfills the duties of a legal entity to pay taxes in the area where it operates. Divisions do not pay income taxes, since the amounts are formed based on the results of reporting periods for the company as a whole. Reporting 2-NDFL and 6-NDFL can be submitted to the tax office where the branch is registered, or to the same inspectorate as the reporting of the main company.

Responsibility for non-payment of taxes by a division lies with a legal entity, unless deliberate concealment of income by the head of the division is proven.

Video: accounting of departments in the 1C program

Registration with funds

Previously, registration with the Pension Fund when opening a separate division was carried out on the basis of an application from the LLC; now this data is automatically transmitted by the tax office. However, the obligation to independently register with the Social Insurance Fund remains.

To register with the FSS, notarized copies are submitted:

- tax registration certificates;

- certificate of state registration of a legal entity or Unified State Register of Legal Entities;

- notice of registration as an insurer of the parent organization, issued by the regional branch of the Social Insurance Fund;

- information letter from the State Statistics Service (Rosstat);

- notifications about tax registration of a separate division;

- opening order, Regulations on a separate division, documents confirming that the separate division has a separate balance sheet and current account;

- original registration application.

A single simplified tax and insurance premiums for employees employed in a separate division must be paid at the place of registration of the parent organization, and personal income tax from these employees must be withheld at the location of the separate division.

Responsibility for violation of the procedure for registering a separate subdivision

Violation of the deadlines for submitting messages and applications for registration of a separate division entails the following fines:

- violation of the deadline for filing an application for registration - 10 thousand rubles (Article 116 of the Tax Code of the Russian Federation);

- Conducting activities as a separate division without registration - a fine of 10 percent of the income received as a result of such activities, but not less than 40 thousand rubles (Article 116 of the Tax Code of the Russian Federation);

- violation of the deadline for registration with the Social Insurance Fund - 5 thousand rubles or 10 thousand rubles if the violation lasts more than 90 calendar days (Article 19 No. 125-FZ of July 24, 1998).

Registration

Individual entrepreneurs have the right to create jobs in any region of Russia. But certain tax regimes require additional registration with the local tax office. If an entrepreneur hires employees for a new branch, and this is inevitable, he will have to pay contributions from their salaries. That is, you also need to register with the Social Insurance Fund and Pension Fund.

PSN

If an entrepreneur works under a “simplified” system, in another city he can conduct activities under a patent (if this type of activity is included in the list of those to which the PSN applies). Two applications must be submitted to the tax office. The first is about registration. The second is about obtaining a patent.

The declaration is submitted at the place of residence. The entrepreneur pays for the patent in the region where the additional office is opened. An entrepreneur maintains two UDR books: USN and PSN. The latter reflects only income.

simplified tax system

With “simplified” taxes are paid at the place of registration. It does not matter in which cities the commercial activities are carried out. Tax base is the totality of income received over a certain period, regardless of geography. There should be one UDR book.

UTII

Where should an entrepreneur who plans to open a business in another city that requires payment of UTII submit reports? In the city in which this type of business activity is carried out, within five days from the opening of the branch.

An entrepreneur submits a declaration under the simplified tax system at his place of residence. According to “imputation” - in the tax authority where he is registered as a UTII payer. If other types of activities, except those under UTII, are not conducted, you need to submit a zero declaration under the simplified tax system to the tax office at your place of residence.

Action plan for creating a separate unit

- Determine that the organization is creating a separate division that is not a branch or representative office (since they have a different registration procedure).

- Make sure that the created workplace is stationary, that is, created for a period of more than a month, the employee is present at it constantly, and this is related to the performance of his official duties. If the employee is remote, there is no need to create a separate unit.

- Within a month after creating a permanent workplace, inform the tax office where the LLC is registered about the creation of a separate division using form No. S-09-3-1.

- Register with the social insurance fund within 30 days.

- If necessary, report a change in the address or name of a separate division to the Federal Tax Service at the place of registration of the division within three days using Form No. S-09-3-1.

Can an individual entrepreneur have a separate division?

An individual entrepreneur is a citizen who has registered with the tax authority for the purpose of carrying out commercial activities and receiving regular income, without creating a legal entity.

The concept of “separate division” is reflected in paragraph. 17, 19 paragraph 2 art. 11 of the Tax Code of the Russian Federation, as well as in Art. 55 of the Civil Code of the Russian Federation and contains a number of distinctive features, namely:

- is a division of the organization;

- is located on a territory separate from the legal entity;

- has permanently equipped workplaces created for a period of more than 1 month.

Based on the above provisions, it is incorrect to classify the commercial activities of a citizen, carried out by him in various places, as a separate division of an individual entrepreneur.

An individual has the right to register as an individual entrepreneur (Part 1 of Article 83 of the Tax Code of the Russian Federation):

- at your residence address (registration);

- finding real estate or transport belonging to him;

- another location, which may include the place of actual activity of the entrepreneur.

In addition to registering as an individual entrepreneur with the Federal Tax Service, a person is required to register with the Pension Fund and the Social Insurance Fund. In this regard, reporting and transfer of taxes and mandatory contributions will be carried out according to the details of these authorities.

Don't know your rights? Subscribe to the People's Adviser newsletter. Free, minute to read, once a week.