Accounting for settlements with suppliers when purchasing OS

Postings reflecting the acquisition of a fixed asset allow, along with the reflection of debt to organizations, to ensure the correct formation of the initial cost of the fixed asset. For accounting purposes, all costs related to fixed assets are reflected by entries in the debit of account 08 in correspondence with the corresponding accounts. Particular attention should be paid to the procedure for reflecting VAT in accounting:

- if the fixed asset is planned to be used in activities, the results of which are subject to VAT, then it is subject to reimbursement from the budget;

- otherwise, the VAT amounts issued by the supplier should be included in the cost of the fixed asset.

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| Postings on receipt of fixed assets for production purposes involved in activities subject to VAT | ||||

| 08.4 | 60 | The cost of the OS object is taken into account. debt to the supplier is reflected | price without VAT | |

| 19.1 | 60 | VAT charged by the supplier is taken into account | VAT | |

| Postings for the receipt of a fixed asset that is NOT involved in activities subject to VAT | ||||

| 08.4 | 60 | The cost of the OS object is taken into account. debt to the supplier is reflected | Value with VAT | |

| Suppliers' invoices for received operating systems have been paid | ||||

| 60 | 50-1 | In cash from the company's cash desk | ||

| 60 | 51 | By cashless transfer from the company's account | ||

| 60 | 55 | By bank transfer from special accounts of the enterprise | ||

| 60 | 71 | Through an accountable person | ||

Account 07 Equipment for installation

Account 07 “Equipment for installation” is intended to summarize information on the availability and movement of technological, energy and production equipment (including equipment for workshops, pilot plants and laboratories) that require installation and are intended for installation in facilities under construction (reconstruction). This account is used by property developers.

Equipment that requires installation also includes equipment that is put into operation only after its parts have been assembled and attached to the foundation or supports, to the floor, interfloor ceilings and other load-bearing structures of buildings and structures, as well as sets of spare parts for such equipment. This equipment includes control and measuring equipment or other devices intended for installation as part of the installed equipment.

Account 07 “Equipment for installation” does not take into account equipment that does not require installation: vehicles, free-standing machines, construction mechanisms, agricultural machines, production tools, measuring and other instruments, production equipment, etc.

Costs for the purchase of equipment that does not require installation are reflected directly in account 08 “Investments in non-current assets” as they are received at the warehouse or other storage location.

Equipment for installation is accepted for accounting as a debit to account 07 “Equipment for installation” at the actual cost of acquisition, which consists of the cost at acquisition prices and expenses for the acquisition and delivery of these assets to the organization’s warehouses.

The purchase of equipment for a fee from other organizations and persons is reflected in the debit of account 07 “Equipment for installation” in correspondence with account 60 “Settlements with suppliers and contractors” or others.

Acceptance for accounting of equipment contributed by the founders on account of their contributions to the authorized (share) capital of the organization is reflected in the debit of account 07 “Equipment for installation” and the credit of account 75 “Settlements with founders”.

The receipt of equipment for installation can be reflected using account 15 “Procurement and acquisition of material assets” or without using it in a manner similar to the procedure for accounting for relevant operations with materials.

The cost of equipment handed over for installation is written off from account 07 “Equipment for installation” to the debit of account 08 “Investments in non-current assets”. At the same time, the contractor accepts equipment delivered to the construction site that requires installation for off-balance sheet accounting under account 005 “Equipment accepted for installation.” The contractor removes the cost of this equipment or its parts handed over for installation from off-balance sheet accounting in account 005 “Equipment accepted for installation.” The cost of equipment transferred to a contractor, the installation and installation of which at a permanent place of operation has not actually begun, is not deregistered from the developer’s register.

When selling, writing off, transferring free of charge or other equipment for installation, its cost is written off to the debit of account 91 “Other income and expenses.”

Analytical accounting for account 07 “Equipment for installation” is carried out by equipment storage locations and individual items (types, brands, etc.).

Reflection of additional costs to bring the OS to a usable state

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| The cost of services for fixed assets involved in activities subject to VAT is reflected. | ||||

| 08.4 | 60 | The cost of services for the asset and the debt to the company that provided the services are taken into account | ||

| 19.1 | 60 | VAT charged by the supplier is taken into account | ||

| Cost of services for a fixed asset NOT involved in activities subject to VAT | ||||

| 08.4 | 60 | The cost of services for the asset and the debt to the company that provided the services are reflected | ||

| Invoices for services rendered have been paid | ||||

| 60 | 50-1 | In cash from the company's cash desk | ||

| 60 | 51 | By cashless transfer from the company's account | ||

| 60 | 55 | By bank transfer from special accounts of the enterprise | ||

| 60 | 71 | Through an accountable person | ||

New type of admission

A new type of Fixed Assets operation has appeared in the document Receipt (deed, invoice). Quick access to this type of receipt document is provided from the fixed assets and intangible assets section using the hyperlink Receipt of fixed assets.

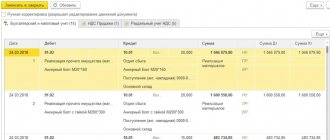

The type of transaction Fixed assets is intended to simultaneously reflect the receipt and acceptance for accounting of fixed assets that do not require installation and additional costs (for example, computers, office equipment, office furniture, etc.). In the header of the document, along with other details, you must indicate the Method of reflecting depreciation expenses, the Asset Accounting Group, the Location of the Asset and the MOL (materially responsible person). In the tabular part you need to indicate the name of the purchased object, its cost, VAT rate and service life in months (Fig. 2).

Rice. 2. Receipt with the type “Fixed assets”

In the receipt document with the Fixed Assets view, it is now possible to quickly enter new objects - to do this, just enter the name of this fixed asset in the appropriate field and select the Create command (the “+” button in the context menu). In this case, the Fixed Assets directory does not open, but the required details are automatically filled in:

- OS accounting group - the value specified in the header is substituted;

- Depreciation group - determined when recording a document in accordance with the specified service life.

If necessary, the user can open the Fixed Assets directory at any time to enter additional information about a specific object. Postings after posting the document:

Debit 08.04.2 Credit 60.01 and Debit 01.01 Credit 08.04.2 – for the cost of acquired fixed assets; Debit 19.01 Credit 60.01 – for the amount of VAT presented by the seller.

For the purposes of tax accounting for income tax, the corresponding amounts are also recorded in the resources Amount NU Dt and Amount NU Kt for accounts with a tax accounting attribute (TA).

If the cost of fixed assets does not exceed 100 thousand rubles, then for the purposes of tax accounting for income tax, the program includes the specified cost in expenses by entries in special resources of the accounting register:

Amount NU Dt 26 (44, 20) and Amount NU Kt 01.01 - for the amount of expenses for acquired fixed assets.

The procedure for reflecting expenses is determined in accordance with the attribute Method of reflecting depreciation expenses.

If the organization applies the provisions of PBU 18/02 (approved by order of the Ministry of Finance of Russia dated November 19, 2002 No. 114n), then permanent differences between the accounting and tax accounting data on the cost of fixed assets, simultaneously included in expenses, are reflected.

In addition to movements in accounting and tax accounting, the document creates entries in periodic information registers that reflect information about the operating system.

Using a receipt document with the type Fixed Assets has limitations:

- the document is not intended to subsequently reflect additional expenses for the acquisition of fixed assets;

- by default, for accounting purposes, the straight-line depreciation method is established;

- bonus depreciation cannot be applied.

If the user is not satisfied with these restrictions, then he can apply the previous scenario for working with fixed assets, using the documents: Receipt (invoice), type of operation Equipment; Receipt of additional. expenses; Acceptance of fixed assets for accounting.

Reflection of interest on credits (loans) used for the purchase of fixed assets

When creating entries to reflect interest accrued on loans and credits used to purchase fixed assets, special attention should be paid to the difference in requirements for accounting for these transactions in accounting and tax accounting: Accounting

— the amounts of interest accrued before the facility was put into operation increase the cost of the non-current asset (entry Dt 08 - Kt66, 67).

Interest accrued after commissioning is included in other expenses of the organization (entry Dt 91 - Kt 66.67). Tax accounting

- for tax accounting purposes, the amount of accrued interest is included in the expenses of the reporting period, within the limits established by Article 269 of the Tax Code of the Russian Federation.

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| Postings reflecting the accrual of interest on loans and borrowings before the facility is put into operation | ||||

| 08.4 | 66 | The cost of interest on short-term loans is taken into account | ||

| 08.4 | 67 | The cost of interest on long-term loans is taken into account | ||

| Interest on loans and borrowings (used for the purchase of fixed assets) accrued after the object is put into operation | ||||

| 91.2 | 66 | The cost of interest on short-term loans is taken into account | ||

| 91.2 | 67 | The cost of interest on long-term loans is taken into account | ||

How to reflect the acquisition of a building in transactions

The purchase of a building by a non-profit organization can be carried out if it is intended for use in work, as well as in the expansion of the enterprise, in particular the implementation of business activities, and also if the conditions of subparagraphs “b” and “c” of PBU 6/01 are met.

The transactions made when purchasing a building are as follows:

| Debit | Credit | Operation name | A document base |

| 08.04 | 60.01 | Arrival of OS | Clauses of PBU 6/01 |

| 60.01 | Payment for the building | Clauses of PBU 6/01 | |

| 01.01 | 08.04 | OS commissioning | Clauses of PBU 6/01 |

Postings reflecting exchange rate and amount differences for fixed assets

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| Postings reflecting exchange rate differences for fixed assets | ||||

| 91.2 | 60 | Negative exchange rate differences reflected | ||

| 60 | 91.1 | Positive exchange rate differences reflected | ||

| Postings reflecting the amount differences for fixed assets | ||||

| 91.2 | 60 | Negative amount differences for fixed assets are reflected after the object was accepted for accounting | ||

| 60 | 91.2 | Positive amount differences for fixed assets are reflected after the object was accepted for accounting | ||

Categories of articles on fixed assets

- Liquidation of fixed assets: postings, complete wear and tear

- Postings for the sale of fixed assets

- Revaluation of fixed assets in accounting

- Postings for repair and modernization of the OS

- Accounting entries for fixed assets in budgetary organizations

- Equipment in accounting - postings with examples

- Accounting entries for revaluation of fixed assets

- Accounting entries for the acquisition of fixed assets

- Accounting entries for the transfer of fixed assets

- Accounting entries for write-off transactions of fixed assets

- Accounting entries for depreciation of fixed assets

- Accounting entries upon receipt of fixed assets

- Renting and leasing of fixed assets in accounting

Video tutorial on accounting for fixed assets in accounting: