Explanations to the balance sheet and a note are not the same thing

The explanatory note to the balance sheet 2021, a sample of which can be seen in this article, does not replace the explanation to the balance sheet. By virtue of PBU 4/99 “Accounting statements of an organization”, “Explanations” are a breakdown of the balance sheet items, as well as clarification of individual reporting forms:

- statement of changes in equity;

- cash flow statement;

- other reporting forms and applications as part of the financial statements.

Whereas the note is an arbitrary transcript of the entire financial situation in the organization. It can contain both general information and detailed explanations of the lines of the balance sheet and income statement. According to Article 14 of Federal Law No. 402 dated December 6, 2011 and paragraph 4 of Order No. 66n of the Ministry of Finance of Russia dated July 2, 2010, this document is included in the annual financial statements. In particular, paragraph 28 of PBU 4/99 stipulates that business entities are required to draw up explanations for the balance sheet and Form No. 2 in the form of separate reporting forms and a general explanatory note. Although officials do not put forward any specific requirements for the form and content of this document, all organizations must submit an explanatory note with a balance.

An exception to the general rule are representatives of small businesses, who have the right to prepare and submit accounting reports in a simplified form. They must provide only two mandatory forms: a balance sheet and an income statement. They do not have to decipher the meanings and describe their financial situation. However, if such a desire arises, it is not forbidden to draw up this document.

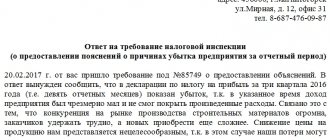

What happens if you don’t respond to the Federal Tax Service’s requirement?

No matter how much the inspectorate threatens punishment, tax officials cannot fine or issue an administrative penalty for the absence of an explanatory letter:

- Article 126 of the Tax Code of the Russian Federation is not a basis for punishment, since the provision of explanations does not apply to the provision of documents (93 of the Tax Code of the Russian Federation);

- Article 129.1 of the Tax Code of the Russian Federation is not applicable, since a request for written explanations is not a “counter check” (93.1 of the Tax Code of the Russian Federation);

- Article 19.4 of the Code of Administrative Offenses is not an argument; punishment is applicable only in case of failure to appear at the territorial inspection.

Similar explanations are given in paragraph 2.3 of the letter of the Federal Tax Service of Russia dated July 17, 2013 No. AS-4-2/12837.

Who needs an explanatory note to the annual report for 2021 and why?

A sample explanatory note to the balance sheet is necessary for all users of financial statements to obtain more complete additional information about the financial and economic activities of a legal entity. Such information, as a rule, cannot be provided in other reporting forms, but it is important and is of interest both to the founders or creditors of the company, and to regulatory authorities. Data in this document can be included based on specific wishes, for example, the board of directors, as well as based on the characteristics of the current economic situation at the enterprise by the end of the year. For example, if the income tax for the reporting period turned out to be significantly lower than the previous one, it makes sense to describe the reasons for this in an explanatory note, since the tax authority, having received such data, will still ask for an explanation. By anticipating this desire, you can avoid not only unnecessary questions from tax authorities and calls to the “carpet” of the inspectorate, but also an on-site inspection, which can be scheduled as part of a desk audit.

How to compose

The general procedure for writing a letter to the tax office for clarification is as follows:

- We compose a response on the organization’s letterhead. If there is no such form, in the header of the document we indicate the full name of the institution, INN, KPP, OGRN and address.

- We indicate the number and date of the requirement for which the explanation is being drawn up. It is permissible to write a response to several tax requests at once.

- If there are errors or inconsistencies in the report, double-check the report to eliminate typos or typos.

- In the descriptive part of the response letter, we reveal in detail and consistently the circumstances of the situation that needs to be explained.

- When answering a request, rely on the facts and document the circumstances. Attach copies of documents to the answer, if any. For example, a copy of the additional agreement to the contract with the condition for increasing prices.

If the inspector requires an explanatory note regarding inconsistencies in the value added tax return, the response will have to be sent electronically. Exceptions to the rules are reserved for organizations that report VAT on paper. If the institution reported electronically, but provided a response to the request on paper, then the tax office will consider such explanations not provided. Such norms are prescribed in the letter of the Federal Tax Service dated January 27, 2017 No. ED-4-15/1443.

ConsultantPlus experts examined whether it is necessary to submit an explanatory note with accounting reports. Use these instructions for free.

to read.

Explanatory note to the financial statements

The sample shows what a document might look like, the more precise name of which is “Explanations for the Balance Sheet.” We took the notional organization LLC “Horns and Hooves,” which has been operating since 2005 and is engaged in the production and sale of dairy products. Its chief accountant compiled this document as follows:

Explanations to the balance sheet of Horns and Hooves LLC for 2019

1. General information

Limited Liability Company (LLC) “Horns and Hooves” was registered by the Federal Tax Service No. 1 for St. Petersburg on March 29, 2005. State registration certificate No. 000000000, INN 1111111111111111, KPP 22222222222, legal address: St. Petersburg, Nevsky Prospekt, 1.

The organization's balance sheet was formed in accordance with the rules and requirements of accounting and reporting in force in the Russian Federation.

- Authorized capital of the organization: 5,000,000 (five million) rubles, fully paid.

- Number of founders: two individuals O.M. Kurochkin and I.I. Ivanov and one legal entity "Moloko" LLC.

- Main activity: milk processing OKVED 15.51.

- The number of employees as of December 31, 2021 was 165 people.

- There are no branches, representative offices or separate divisions.

2. Basic accounting policies

The accounting policy of LLC "Horns and Hooves" was approved by order of director Ivanov I.I. dated December 25, 2013 No. 289. The straight-line depreciation method is used. Valuation of inventories and finished products is carried out at actual cost. The financial result from the sale of products, works, services, goods is determined by shipment.

3. Information about affiliates

Ivanov Ivan Ivanovich is the founder, 50% of the ownership share in the management company, holds the position of general director.

Kurochkin Oleg Mikhailovich - founder, 30% share of ownership in the management company.

LLC "Moloko" - founder, 20% ownership share in the management company, Russian organization (founders V.P. Petrov and Yu.K. Sidorov).

During the reporting period, the following financial transactions were carried out with related parties:

- On March 12, 2021, the general meeting of the founders of Horns and Hooves LLC reviewed and approved the financial statements of the organization for 2021. The meeting decided to pay a profit in the amount of 3,252,000 rubles to the founders based on their share in the authorized capital based on the results of 2019. The payment (including personal income tax withholding for two individuals) was made on 04/01/2020;

- On May 25, 2021, Horns and Hooves LLC entered into a contract with the founder of Milk LLC, Yu.K. Sidorov, an agreement for the purchase of non-residential premises worth 5,102,000 rubles. The cost of the transaction is determined by an independent assessment of the value of the property. Payments under the agreement were made in full on June 6, 2018, and the transfer and acceptance certificate of the real estate was signed.

4. Key performance indicators of the organization for 2021

In the reporting year, the revenue of Horns and Hooves LLC amounted to:

- for the main type of activity “production and sale of dairy products” - 385,420,020 rubles;

- for other types of activities - 650,580 rubles;

- other income: 170,800 rubles (sale of fixed assets).

Costs of production and sales of products:

- acquisition of fixed assets: 1,410,500 rubles;

- depreciation of fixed assets: 45,230 rubles;

- purchase of raw materials: 110,452,880 rubles;

- wage fund: 137,580,040 rubles;

- travel expenses: 238,300 rubles;

- rental of premises: 8,478,190 rubles;

- other expenses: 532,458 rubles.

5. Explanation of balance sheet items as of December 31, 2019 (using the example of accounts payable)

Availability and movement of accounts receivable

Index Period For the beginning of the year Changes over the period At the end of the year Accounted for under contracts Provision for doubtful debts Received Dropped out Remainder In thousands of rubles with decimal places Under contracts (transactions) Fines, penalties, penalties Redeemed Written off in Finnish result Written off to reserve for doubtful debts Current Overdue Total short-term accounts receivable, including: 2019 25 489,3 (200,0) 15 632,7 300,4 (25 023,2) (102,1) (48,9) 15 726,1 522,1 buyers 20 409,0 (200,0) 10 015,5 300,4 (17 315,3) (87,7) (48,9) 12 750,9 522,1 suppliers 5080,3 — 5617,1 — (7707,9) (14,4) — 2975,2 — Total long-term accounts receivable, including: 2019 50 000,0 — — — — — — 50 000,0 — for interest-free loans 40 000,0 — — — — — — 40 000,0 — TOTAL accounts receivable 30 489,3 (200,0) 15 632,7 300,4 (25 023,2) (102,1) (48,9) 65 726,1 522,1 6. Estimated liabilities and provisions

As of December 31, 2021, the organization formed an estimated liability for payment of regular vacations of employees in the amount of 7,458,000 rubles, the number of unpaid vacation days is 67, the due date is 2021.

The reserve for doubtful debts was formed in the amount of RUB 600,000. due to the presence of overdue and unsecured debt of Girya LLC in the amount of 522,000 rubles.

The organization did not create a reserve for reducing the value of inventories in 2021, since inventories do not show signs of depreciation.

7. Salary

Payables for wages as of December 31, 2018 for the organization as a whole amounted to RUB 3,876,400. (payment for December 2021, due date: 01/12/2020). Staff turnover in the reporting period was 14.88%. The number of employees as of December 31, 2019 is 165 people. The average monthly salary is 25,675 rubles.

8. Other information

(In this section you need to describe all extraordinary facts in the business and economic activities of the organization for the reporting period, describe their consequences. You can also describe all other significant facts that affected the balance sheet in general and, in particular, you can list major transactions and counterparties for them for the reporting period, as well as write a forecast or events that have already occurred after the reporting date and are of significant importance.)

Director of LLC "Horns and Hooves" /signature/ Ivanov I.I. 03/19/2020.

When drawing up an explanatory note, special attention must be paid to information about affiliated persons. It is advisable to document this data in a separate section, as required by paragraph 14 of PBU 11/2008. By law, it is necessary to disclose information not only about the founders of the organization itself, but also about persons associated with them, therefore, if the founders (as our example of an explanatory note to the balance sheet shows) includes a legal entity, its participants or shareholders must be indicated. In addition, information on transactions carried out with related parties during the reporting period must be indicated, as well as, regardless of the transactions, on those legal entities and citizens that are recognized as affiliated.

Obviously, competent preparation of an explanatory note to the financial statements can save the manager and accountant from additional communication with regulatory authorities. It is important to remember that the detail of the information in this document depends only on its compiler - on the intention of the organization itself to disclose or not certain indicators for the year. The main and only requirement that the legislator makes for this document is that the information contained in the explanations must be reliable. The person who signed the document is responsible for its correctness.