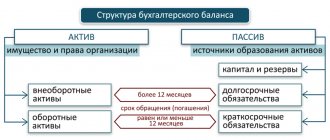

The Tax Code establishes the obligation of business entities to prepare annual and interim financial statements. The purpose of the first document is clear - it contains information about the operations performed at the enterprise during the reporting period. This data is necessary to verify the correctness of the records and the accuracy of the reflection of transactions.

As for the preparation of interim financial statements, not all specialists understand its importance. This document is necessary to ensure compliance with the conditions for the formation (change) of the consolidated group of payers (consolidated group of payers) and compliance with the provisions of Art. 269 NK. Meanwhile, the Code does not contain any special requirements for interim accounting reporting, its form, or the frequency of its preparation. And the current accounting regulations contain contradictory provisions on this matter. Let's look at the current situation in this article.

General requirements

You may be interested: Limit of the Molodezhnaya card from Sberbank: conditions, how to withdraw and top up

Requirements relating to the preparation of financial (accounting) statements, determination of the reporting date and period are enshrined in Articles 13, 15 402-FZ. In accordance with Art. 13 the reporting must contain reliable information on the basis of which users form an idea of the financial condition of the business entity, as a result of its activities, the availability and flow of funds for the period. All this information will subsequently form the basis for management decisions.

Channel PROGRAMMER'S DIARY

The life of a programmer and interesting reviews of everything. Subscribe so you don't miss new videos.

The reporting period (in accordance with Article 15 402-FZ) is the period for which the reporting is generated. Reporting date – the day for which the information is summarized. Simply put, this is the last day of the control period.

The concept of interim reporting

Interim accounting forms are compiled for a period of less than a calendar year; it is necessary to reflect the current activities of the company. The legislation does not define the periods for which indicators are collected in the forms, so the organization independently sets them, this could be:

- Month;

- Quarter;

- Or other periods.

Interim reporting, depending on which user it is provided to and what information he needs, can be compiled in a condensed form or, on the contrary, added with the necessary lines.

Interim reporting is prepared at the request of the company's managers, for example for:

- For owners (founders), the data may be necessary to make the right decisions aimed at stabilizing the company’s activities;

- Banking institutions, if the company took out a loan secured in the form of collateral, to track the required balance on the pledged property;

- Internal divisions of the company, for drawing up plans;

- For other users.

Submit quarterly accounting forms to regulatory authorities, from the first quarter. 2013 is not necessary, since this provision is not in the law.

Interim financial statements: terms and conditions of formation

So, when should you create a document? Let's turn to the legislation. As follows from the provisions of 402-FZ, interim accounting (financial) statements are provided for a period not exceeding one year. At the same time, in paragraph 3 of Art. 13 of this normative act provides cases when an economic entity must draw it up. In particular, interim financial statements are prepared if the corresponding obligation is assigned:

- Federal legislation. For example, such a document is necessary for an LLC if net income is distributed between participants every quarter or every six months (this rule is established in paragraph 1 of Article 28 of the Federal Law “On LLC”), or if it is necessary to determine the real value of the share of a participant leaving composition of the company (clause 1 of article 8 and clause 2 of article 23 of the specified Federal Law).

- In contracts, constituent documentation of the enterprise.

- In decisions of the owner of a business company.

- In the regulations of the Central Bank and the Ministry of Finance.

You may be interested in:Addresses of Avangard Bank in Arkhangelsk

When might a half-year balance be required?

Although the semi-annual balance sheet does not need to be submitted to the tax authorities, taxpayers often generate such a document. There may be many reasons for this, but most of them are related to the use of information from the balance sheet in the company’s activities.

The main reasons for the formation of a balance sheet for six months:

- It is required to provide information on financial activities to the owners of the company.

- It is necessary to make a decision on the payment of dividends based on the results of the past 6 months.

- It is necessary to send information about the semi-annual balance sheet to the banking institution that issued a loan to the company or is just negotiating to provide a loan to the legal entity.

- There is a need to assure potential or existing counterparties of the company’s reliability and financial well-being.

- It is required to analyze the company’s economic activity based on the results of past months and predict subsequent financial activity.

- It is necessary to send the document as a response to the request of the tax inspectors in the format of justifications for previously submitted explanations.

- It is necessary to make a decision on bonus payments to company employees based on the results of six-month activities.

Nuances

According to the provisions of paragraph 1 of Art. 30 402-FZ, before state accounting regulatory bodies adopt industry and federal standards, business entities apply the rules for reporting and accounting approved by the Central Bank and authorized federal executive structures. The corresponding rules are today enshrined in PBU 4/99.

Clause 48 of the said PBU establishes that an organization must prepare interim financial statements for a month, a quarter from the beginning of the year on an accrual basis, unless another procedure is provided for by federal legislation. At the same time, in paragraph 52 of the same Regulations there is a clarification that the document we are considering is provided in cases stipulated by law or the constituent documentation of a business entity. And according to paragraph 15 of Art. 21 402-FZ, industry and federal standards cannot contradict the provisions of this law.

Thus, taking into account the content of all the above norms, the payer is not obliged to prepare and provide interim financial statements solely on the grounds provided for by PBU 4/99.

It should also be taken into account that the obligation to send the document to both the Federal Tax Service and the state statistics bodies is not specified in the legislation. Business entities must provide only annual reports (clause 1 of Article 18 402-FZ, Order of Rosstat No. 185 of 08/12/2008, 5 subclause 1 of clause 23 of Article TC).

Interim financial reporting: rules of preparation

Author of the publication

Rybakova Elena Ivanovna

senior specialist of the IFRS department of CJSC "CBA" (at the time of publication)

Although IAS 34 Interim Financial Reporting does not require the presentation of interim financial statements, but only recommends it for companies whose securities are publicly traded, many companies are forced to prepare such reports to meet the needs of interested users of financial information.

According to IAS 34, interim financial statements are a complete package or set of condensed financial statements for a period that is shorter than a full financial year. The company decides whether it will prepare full financial statements or condensed ones. If an entity decides to use condensed financial statements, then such statements must comply with the requirements of IFRS 34. If a decision is made to prepare full financial statements, then in addition to the measurement and additional disclosure requirements of IFRS 34, such statements must comply with all the requirements of IFRS 1 Presentation of Financial Statements. reporting" in the area of disclosures.

As a minimum, condensed interim reporting includes:

– condensed statement of financial position;

– a condensed statement of comprehensive income, which is presented:

• as a single report;

• as two separate statements: the income statement and the statement of comprehensive income;

– abbreviated statement of changes in equity;

– abbreviated cash flow statement.

If, when preparing annual accounts, a company discloses the components of profit and loss in a separate income statement, then when preparing interim accounts, it is necessary to present two separate statements - a profit and loss account and a statement of comprehensive income.

The requirements of IFRS 34 for the presentation of comparative information are given in table. 1.

Table 1

| Report | Current period | Comparative period |

| 1 | 2 | 3 |

| Statement of financial position | End of the current interim period | End of previous financial year |

| Statement of comprehensive income | The current interim period and the period from the beginning of the financial year to the end of the reporting period (see example 1, table 3) | Comparable interim period of the previous financial year |

| Statement of changes in equity | Cumulatively from the beginning of the financial year to the reporting date | Comparable period of the previous financial year |

| Cash flow statement | Cumulatively from the beginning of the financial year to the reporting date | Comparable period of the previous financial year |

Example 1

At the request of creditors in 2009, Space Limited must submit interim reports for the first half of the financial year, which ends on December 31, 2009. According to the requirements of IFRS 34, the comparative period in the interim reports for the first half of 2009 for each type of reporting will be as follows (Table 2).

table 2

| Report | Current period | Comparative period |

| Statement of financial position | June 30, 2009 | December 31, 2008 |

| Statement of comprehensive income | June 30, 2009 | June 30, 2008 |

| Statement of changes in equity | June 30, 2009 | June 30, 2008 |

| Cash flow statement | June 30, 2009 | June 30, 2008 |

If creditors had required the company to prepare quarterly reports, then as of June 30, 2009, the company would have presented information in the same way as in the first case, with the exception of the statement of comprehensive income, which would have looked as follows (Table 3).

Table 3

| Condensed statement of comprehensive income for the period ended June 30, 2009 | ||||

| For the 3 months ended | For the 6 months ended | |||

| June 30, 2009 | June 30, 2008 | June 30, 2009 | June 30, 2008 | |

| Revenue | 115 000 | 100 000 | 250 000 | 210 000 |

| Cost price | (93 000) | (85 000) | (190 000) | (180 000) |

| Gross profit | 22 000 | 15 000 | 60 000 | 30 000 |

The information in the condensed interim financial statements should be presented in the same sections and contain the same subtotals as in the most recent annual financial statements.

Accounting policy

The interim condensed financial statements must contain a statement that the interim financial statements use the same accounting policies and calculations as the most recent annual financial statements. In this case, the company does not need to repeat all accounting policies in the interim reporting.

If these policies and practices have changed, reporting must describe the nature and impact of the change. Any change in accounting policies resulting from the adoption of new or revised standards is accounted for in accordance with the transition provisions required by those standards. In other cases, changes in accounting policies are disclosed in accordance with the general rules for reflecting changes in accounting policies.

Seasonal revenue

Recognition of revenue received by an enterprise seasonally cannot be early or deferred. Such revenue is recognized as incurred.

Example 2

The ICE Cream company produces ice cream. The company's shares are traded on the open market. The company's financial year ends on August 31. In December 2008, the company began preparing financial statements for the first half of the year. The company's management is concerned about the results that will be presented in these reports, since the company receives the main revenue in the third and fourth quarters (in the summer months):

– first quarter – 15% of annual revenue;

– second quarter – 10% of annual revenue;

– third quarter – 30% of annual revenue;

– fourth quarter – 45% of annual revenue.

For the first half of the year, the company's revenue amounted to CU 630,000. The company's management decided that in the semi-annual reporting the revenue would be reflected in the amount of CU 1,260,000, which was calculated in the following way:

CU630,000: 0.25 × 1/2 = CU1,260,000

According to the requirements of IFRS 34, seasonal revenue is recognized when it is actually received, so ICE Cream cannot indicate revenue in the amount of CU 1,260,000 in its interim reporting for the first half of the year: this is contrary to the requirements of the standard. Revenue should be recorded at CU630,000.

Costs incurred unevenly throughout the financial year

The rules regarding the recognition of revenue received by an enterprise seasonally also apply to costs, i.e. those costs that cannot be capitalized at the end of the interim reporting period (such costs do not meet the criteria for recognizing an asset) must be written off as expenses when they are incurred. occurrence.

Example 3

ABC Company is engaged in the production of electronic equipment and prepares financial statements quarterly. In the first quarter of the financial year, the company introduces a new model of electronic equipment to the market, which will be sold throughout the financial year. In connection with the release of the new model, the company is incurring expenses for a promotional campaign that will end in the first quarter. Should the costs incurred for this promotion be spread over the period of revenue associated with the model, or should the costs be charged to the statement of comprehensive income in the first quarter?

The company must write off these expenses in the first quarter. According to paragraph 69 of IFRS 38 “Intangible Assets”, all expenses for advertising and promotion of products must be recognized as expenses in the period in which they arose.

Annual bonuses paid to employees

There are various types of bonuses. There are bonuses that are paid for length of service. Some are paid based on operating results for the quarter or year.

In interim reporting, employee bonuses may be recognized early if and only if:

– at the reporting date, the company has a legal obligation to pay bonuses or an imputed obligation based on past practice, and the company has no realistic alternative to avoid fulfilling this obligation;

– the amount of payment at the date of preparation of interim reports can be reliably estimated.

Intangible assets (IMA)

To prepare interim reporting, a company must apply the same criteria for recognizing intangible assets as for annual reporting. Costs that arose before the criteria for recognizing intangible assets began to be met must be recognized as expenses. An entity may not recognize a cost as an asset in its interim reporting if the asset recognition criteria are not met, even if it is expected that the criteria will be met in the future.

Example 4

The IT International company develops software products for stock exchanges. The company's financial year ends on December 31. The company prepares reports quarterly. In January 2008, she began research into the development of a new software product that included solving complex problems that IT International could not previously implement in its software products. Expenses for research and development of new software products during 2008 were incurred in the following periods:

– first quarter – CU 200 thousand;

– second quarter – CU 200 thousand;

- third quarter:

• July 1 – August 31 – CU 100 thousand;

• September 1 – September 30 – 80 thousand;

– fourth quarter – CU 350 thousand.

The company publishes semi-annual reports on August 25 and recognizes research costs in the amount of CU400 thousand incurred in the first and second quarters of 2008 in profit and loss. On September 1, 2008, it became known that the criteria for capitalization of expenses as part of an asset, established by IAS 38, had been met.

IAS 38 requires that asset recognition (i.e. capitalization of expenses) commences from the time it is known that all recognition criteria for the asset have been met, rather than from the beginning of the period during which this became known. The company's reporting for the third quarter and for the entire financial year will look as follows (Table 4).

Table 4

| September 30th | 31th of December | |||

| Asset recognized in the statement of financial position | 80 | 430 | ||

| 3 months ended 30 September | 9 months ended 30 September | 12 months ended 31 December | ||

| Research expenses recognized in profit or loss | 100 | 500 | 500 | |

Expenses that the company incurs irregularly

A company's budget may include certain expenses that the company incurs irregularly during the financial year, such as charitable contributions, staff training costs. These expenses are discretionary, even if the company plans to incur such expenses from year to year. Recognition of a liability for expenses of this type that have not actually been incurred at the end of the interim period is not permitted, since these expenses do not meet the definition of a liability.

Reserves

Impairment losses on inventories arising during the interim period are recognized using the same procedures as those used in preparing the annual accounts. An entity cannot defer recognition of such losses on the basis that they are expected to recover by the end of the year.

If a company has contracts that provide for discounts for volumes of purchased goods, and the company’s management assesses that the likelihood of receiving such a discount is high, then when preparing interim reporting, the company must adjust the cost of such goods taking into account the discount.

Non-guaranteed discounts are not recognized early.

Assets measured at fair value

The carrying amount of assets measured at fair value should be determined as at the interim reporting date. When determining fair value for interim reporting purposes, an entity may use estimates that are less accurate than when preparing annual financial statements. For example, when preparing interim reports, a company may not use appraisers to determine the fair value of investment property, but rather extrapolate the data provided by appraisers to prepare the previous annual reports. But in the event of significant changes in the economic situation in the country compared to the previous reporting period, extrapolation will be unacceptable.

Changes expected in the future

In August 2009, the IASB published amendments to IAS 34 for public comment, proposing:

– for financial instruments measured at fair value, establish the same disclosures that are required for annual financial statements in accordance with IFRS 7 “Financial Instruments – Disclosures”;

– for financial instruments measured other than at fair value, establish the same disclosures required for annual reporting under IFRS 7 Financial Instruments – Disclosures, including fair value disclosures for such instruments;

– for non-financial assets and liabilities, do not establish additional disclosure requirements beyond those already required by IFRS 34.

If these amendments are adopted, this will complicate the preparation of reporting and lead to an increase in the time frame for its preparation.

Share a link to the article on social networks:

Internal documents of the organization

If an enterprise, in the absence of an obligation to prepare and submit interim financial statements on the above grounds, nevertheless recognizes its preparation for management or taxation purposes as necessary, then the decision on the frequency, timing, volume, forms, and procedure for calculating individual indicators should be fixed by local acts.

One of such documents is the accounting policy. The standards state that it is approved by the head of the company. Changes to accounting policies can also be accepted. They are approved by a separate order of the head.

Another local act is the standard of an economic entity - “Regulations on accounting and reporting at an enterprise.” It can be developed separately and approved as a separate document or made an annex to the accounting policies.

Booking deadlines annual and interim reporting

The deadlines for a company to submit annual forms are specified in the Tax Code of the Russian Federation - this is no later than 3 months after the end of the reporting year. The reporting year is equal to a calendar year if the company operated fully from January 1 to December 31. If the last day for submitting forms falls on a non-working day (weekend) or holiday, the deadline is extended to the first working day after this day.

Regarding the submission of forms according to the intermediate account. reporting, then the deadline for submission, according to current legislation, is not provided. If it needs to be compiled and provided to internal and external users, then the deadline is set by the head of the company.

Features of the internal standard

If we consider this document from the point of view of the provisions of paragraphs 1, 11, 12 21 of Article 402-FZ, then it will be considered an act regulating the company’s accounting. In other words, an internal standard will have the force of a normative act in the field of accounting if its content does not contradict industry and federal standards.

You will be interested in: PBU, expenses: types, classification, decoding, name, symbol and rules for filling out financial documents

Taking this into account, the enterprise can establish the procedure necessary for an economic entity to streamline the processes of organizing and maintaining accounting.

Preparation of reports for compliance with the conditions of education (changes) of the group of groups

In accordance with sub. 3 p. 3 art. 252 of the Tax Code, an enterprise party to an agreement on the formation of a consolidated group of payers must meet a number of requirements.

Thus, the amount of net assets calculated in accordance with the financial statements as of the reporting date preceding the day of submission of documents to the Federal Tax Service for registration of the agreement must be greater than the size of the share (authorized) capital.

If the enterprise, in accordance with paragraph 2 of Art. 23 of the Federal Law “On LLC”, must pay the participant the real value of his share in the capital and the company’s accounting policy, then the need to generate quarterly reports is established; the calculation basis is based on information from reporting documents drawn up at a later date preceding the day the participant submitted the relevant requirements.

The legitimacy of this approach is confirmed by the Ministry of Finance. In letter No. 03-03-10/51217, the department explains the following. An enterprise party to an agreement on the formation of a consolidated group of payers may be required to prepare interim financial statements for different periods (on different dates). This depends on the specific act providing for such a requirement. For example, a decision by the owner of a business entity may establish the obligation to generate and submit reports on a monthly basis.

Taking into account the provisions of 402-FZ and sub. 3 p. 3 art. 252 of the Tax Code, the Ministry of Finance came to the conclusion that the amount of net assets should be determined in accordance with accounting documents, the preparation and provision of which is fixed by one of the conditions established by 402-FZ, at a later date. This procedure was included in the letter of the Federal Tax Service dated January 19, 2013 and was sent for familiarization and application in the activities of lower tax services.

The letter of the Ministry of Finance No. 03-03-06/1/47681 dated November 8, 2013 also states that the amount of the organization’s net assets should be calculated based on information from the latest reports generated before the day of submission of documents for registration of the agreement on the creation of the consolidated group of groups.

Where and when are financial statements submitted?

During the period when the balance sheet is submitted, it is necessary to clarify whether the address of the tax authority to which the company belongs has changed. You can provide documents:

- To the inspection in person or through a representative by proxy;

- By mail with a mandatory list of attachments, which is subsequently stored along with the report;

- Through the Internet.

Having submitted the documents to the tax authority, it is necessary to send the report to the state statistics body.

But how many times a year do they hand over their balance sheets? Fortunately, this question can now be answered - only once, and not every quarter as before. The Tax Code requires reporting to be submitted no later than three months after the end of the year.

You should pay attention to the deadlines for submitting balance sheets for newly created organizations. They depend on the date of registration

If an enterprise is registered after September 30, then it submits its first report only at the end of the next year.

When answering the question of when organizations hand over their balance sheets, it is necessary to note cases of reorganization or liquidation. Then the inspection must be provided with a separation or liquidation balance sheet, respectively, in which the end date of the reporting period will be the day of making an entry about changes in the Unified State Register of Legal Entities.

You should also remember how many times a year the balance sheet must be submitted to the owners of the organization for approval. The problem is that the deadline for submitting reports to the tax office occurs earlier than the last date established for holding annual meetings of participants or shareholders (or the Board of Directors). Because of this, corrections to reports based on the results of the annual meeting are possible, because When new facts of activity are discovered, the impact of business transactions on the balance sheet is inevitable. And clause 8 of PBU 22/2010 states whether it is possible to submit an updated balance sheet. It is possible only if a significant error found before the date of approval of the report is corrected in the manner prescribed by law.

For some types of activities, provision is made for the submission of interim quarterly reports to the authorities that control such activities. However, there is no need to provide such reports to the tax office. We are talking about the following companies:

- Insurance companies;

- Professional participants in the securities market.

Late submission of the balance sheet entails a fine of 200 rubles for each form, this is stated in Article 126 of the Tax Code of the Russian Federation, and officials can be brought to administrative liability with a fine of 300 to 500 rubles.

When preparing a balance sheet, you must remember accuracy, care, and accuracy, and then the document will become not only an unnecessary report, but a tool for competent management of the enterprise.

Capitalization rate

It is calculated on the last day of the corresponding period. To determine it, first, the outstanding controlled debt is divided by the amount of equity capital corresponding to the share of indirect or direct participation of a foreign enterprise in the share capital (fund) of a domestic company, and then the resulting indicator is divided by 3 (for banking organizations and entities engaged in leasing activities - by 12.5).

How to create a balance sheet for six months?

The semi-annual balance sheet is an optional report, so its form may differ from the standard one submitted to the Tax Service.

Filling out a balance sheet is mainly necessary to reflect specific performance indicators.

Detailing certain data that is not stated in a standard form will help the taxpayer in making management decisions that are primarily important for the company itself, and not for regulatory authorities. However, accountants quite often prepare a six-month balance sheet in the usual form, since this allows them to compare information with the previous annual balance sheet and subsequently simplify the work at the end of the year when the next annual report needs to be generated. A balance sheet in a standard form is of interest primarily to tax authorities, banking institutions and counterparties. For local use within the company itself, you can use a free form of a semi-annual balance sheet.

Determining the amount of equity capital

In pursuance of the requirements of paragraph 2 of Art. 269 of the Tax Code are not taken into account when calculating the amount of debt on fees and taxes. We are talking about current arrears, amounts of deferrals and installments, as well as an investment tax credit.

In paragraph 2 of Art. 269 of the Tax Code there is no indication of specific data sources by which an economic entity must determine the amount of equity capital. It follows from this that the enterprise is not obliged to calculate it solely on the basis of information from the financial statements. This means that when calculating the capitalization ratio, the amount of capital can be determined based on accounting data available in any sources.

Why is interim reporting needed?

A calendar year is a very long period. During such a time, very serious changes can occur in the company. Naturally, owners want to receive information about their business more often.

In addition to owners, other users may be interested in receiving interim reporting:

Banks. When applying for a loan, the company usually provides its statements for analysis. Further, in the process of debt servicing, banks also regularly request the borrower’s accounting reports, including interim reporting.

Counterparties. When working on large and long-term contracts, the company’s partners usually also want to regularly receive information about the status of their counterparty.