What kind of trade is delivery?

In the Tax Code of the Russian Federation (part two) dated 05.08.2000 No. 117-FZ (as amended on 28.12.2016) Ch. 26.5. Art. 346.43. A fairly clear definition is given:

11) distribution trade - retail trade carried out outside a stationary retail network using specialized or specially equipped vehicles for trade, as well as mobile equipment used only with the vehicle. This type of trade includes trade using a car, a car shop, a car shop, a toner, a trailer, a mobile vending machine;

Thus, it becomes clear to us that delivery trade is mobile trade, not tied to a specific location. In other words, if you want, you can make a decision at any time and change your location, but at the same time you have the right to trade from a vehicle for a long time, remaining in the same place. But, suppose you are the owner of a mobile shop, devoid of signs of mobility (no wheels, towbar, etc.) - it rather resembles a kiosk, then trade from such a counter cannot be considered delivery trade.

In general, the Tax Code quite clearly defines the types of vehicles:

- automobile,

- auto shop,

- auto shop,

- tonar,

- caravan,

- mobile vending machine.

The legislator has a number of requirements for vehicles planned to be used for distribution trade:

- Your vehicle must meet the requirements of environmental class no lower than 4 (Euro 4);

- the vehicle must undergo technical inspection;

- the vehicle must be kept in proper sanitary and technical condition;

- according to modern requirements, you will have to equip the vehicle with a mobile geolocation system with the ability to track the vehicle via the Internet;

- the vehicle must be specially equipped for trading. What does this mean? Perhaps we are talking about a vehicle that was originally created for distribution trade, and, perhaps, converted for these purposes through a major overhaul. But in any case, the signs of trade should be obvious. You need to take care of the presence of a display case or counter, refrigeration, cash register and other technological equipment provided for by the requirements of regulations for the sale of products. Do not forget about the equipment of the seller’s workplace - it is necessary to install an umbrella or canopy, a chair, a table to be able to work with the client.

During operation, connection to utility networks may be required. You have the absolute opportunity to connect to energy and water supply networks on a temporary basis - this does not deprive your activity of the status of distribution trade.

After equipping the vehicle, it is very important to decide on the range of products sold. Here the All-Russian Product Classifier comes to our aid, according to which, and in accordance with the specialization of the vehicle, you can determine the list of goods:

| No. | Specialization |

| 1 | Fast food |

| 2 | Milk products |

| 3 | Meat products |

| 4 | Vegetables fruits |

| 5 | Fish, seafood |

| 6 | Bread, bakery products, confectionery |

| 7 | Products |

| 8 | Non-food products |

| 9 | Printed products |

| 10 | Flowers |

It is necessary to pay attention to the fact that you can work with the “Products” and “Non-Food Products” specializations only in cities with a population of less than 300 thousand people and in rural areas.

Characteristics of trading operations

In peddling trade, the seller is in direct contact with the buyer. This type of trade includes trade from hands, trays, baskets and hand carts. This is stated in paragraph 18 of Article 346.27 of the Tax Code of the Russian Federation.

In distribution trade, goods are sold through specialized vehicles, as well as mobile equipment used only with transport. This type of trade includes trade using a car, a car shop, a car shop, a toner, a trailer, a mobile vending machine. This follows from paragraph 17 of Article 346.27 of the Tax Code of the Russian Federation.

Situation: are there any restrictions on the types of goods sold during delivery (distribution) trade for the purpose of applying UTII?

Yes, they do exist.

Despite the fact that Chapter 26.3 of the Tax Code of the Russian Federation does not establish such restrictions, when conducting retail trade outside of stationary retail facilities, the sale of:

- food products (except for ice cream, soft drinks, confectionery and bakery products in manufacturer's packaging);

- medicines;

- products made of precious metals and precious stones;

- weapons and ammunition for them;

- copies of audiovisual works and phonograms;

- programs for electronic computers and databases.

These restrictions are established by paragraph 4 of the Rules, approved by Decree of the Government of the Russian Federation of January 19, 1998 No. 55.

Thus, peddling and delivery trade in these goods is prohibited and, therefore, as an independent type of activity cannot be transferred to UTII. This special regime can only be applied if such goods are sold through a stationary retail chain.

What kind of trade cannot be considered delivery trade?

Now let’s look at the mistakes that will help you avoid problems with the law when determining the type of trade as delivery:

- trade cannot be considered delivery if you deliver the goods in accordance with a previously completed application or purchase and sale agreement;

- if your vehicle is not properly equipped, then trade from this vehicle also cannot be considered a delivery trade;

- if you trade from a tray, table, box, drawer, etc., i.e. Your trade equipment does not have the characteristics of a vehicle, then such trade cannot be considered delivery trade either.

Is it possible to apply UTII for distribution trade?

According to the Tax Code of the Russian Federation, entrepreneurs engaged in delivery trade have the right to apply a single tax on imputed income (UTII). To do this, you must submit an application to the tax office at the location of the organization or at the place of residence of the individual entrepreneur within five days from the date of commencement of business. Within five days from the date of receipt of the application, the tax office issues a notice of registration as a single tax payer on imputed income.

Types of activities for individual entrepreneurs subject to imputed tax in 2021

As for the OKVED and OKP codes, in the field of consumer services, the types of activities of UTII for individual entrepreneurs in 2021 constitute a huge block with more than 600 items. The full list is given in Order No. 2496-r dated November 24, 2016.

Definition of special mode

When receiving individual entrepreneur status, the applicant correlates his type of business transactions with information from the classifier. If these numbers are in the permit list of local legislation, and all other necessary conditions are met, then the payer has the right to UTII.

We recommend reading: What documents are needed to get a free train ticket to St. Petersburg

If the tax payment deadline falls on a holiday or weekend, it is postponed to the next business day. For example, for the fourth quarter of 2021, taxes can be paid until January 27, 2021, because January 25 is a Saturday.

The tax office reviews the application within five days and issues a notification of registration under UTII. If a business operates in several regions, you need to register in each of them. You can switch to UTII at any time, even in the middle of the year. But there is an exception for individual entrepreneurs and simplified companies: they can switch to UTII only from the beginning of the year.

Tax accounting and reporting on UTII

Each region can enter its own requirements for UTII. We go down to the section “Features of regional legislation” and find Yaroslavl. Requirements for UTII may vary not only for individual regions, but even for municipal districts. In the decision of the municipality of Yaroslavl, the service is included in the list, which means that a car wash in Yaroslavl can switch to UTII

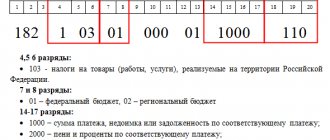

- First of all, please note that the application for UTII indicates only two digits of the code, while OKVED codes when registering a business by type of activity have four or more digits.

- Secondly, the classifier of types of economic activity has a complex branched structure of hundreds of different codes having from two to six characters. And there are only 22 activity codes that are indicated in the UTII application.

- Thirdly, the codes are approved by various legal acts:

- by order of the Federal Tax Service of Russia dated December 11, 2021 No. ММВ-7-6/ [email protected] for an application for the transition to imputation;

- by order of Rosstandart dated January 31, 2021 N 14-st for the OKVED classifier.

Calculation of UTII for distribution trade

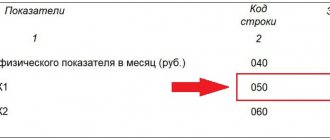

When calculating UTII, a physical indicator is used - the number of employees, including the entrepreneur, which is 4,500 rubles for each employee. In addition to the physical indicator, the following coefficients are used:

- K1 – deflator coefficient

- K2 – correction factor

K1 for the next calendar year is established by the Ministry of Economic Development of the Russian Federation.

K2 is determined by municipalities for an indefinite period.

If local authorities do not apply a reduced tax rate, then the amount of UTII must be calculated at a rate of 15% .

So, to calculate UTII, first of all, we determine the tax base for the reporting quarter:

| Tax base for UTII for the quarter | = | Basic profitability per month (4500.00) | * | (Average number of employees for 1 month of the quarter | + | Average number of employees for the 2nd month of the quarter | + | Average number of employees for the 3rd month of the quarter) | * | K1 | * | K2 |

Having determined the tax base for UTII for the quarter, you can calculate the amount of UTII using the formula:

UTII = Tax base for UTII for the quarter * 15%

Example:

IP Ivanov I.I. trades seedlings from its own vehicle in Yekaterinburg. In the region, the UTII rate is 15%.

Let's determine the tax base for the quarter:

4500 rub/person*(1+1+1)*1.798*0.64 = 15534.72

Let's calculate the amount of UTII:

15534,72 * 15% = 2330,21

UTII for the 1st quarter is equal to 2330.21 rubles.

If during the specified period there were payments of hospital benefits and insurance premiums, then the amount of UTII can be reduced.

Retail trade on UTII in 2021: rules

UTII taxpayers are not VAT payers, except for operations involving the import of goods into the customs territory of the Russian Federation and operations regulated by Art. 161 and 174.1 of the Tax Code of the Russian Federation. Also, UTII taxpayers are exempt from a number of basic taxes

by type of activity:

Formula for calculating UTII

- —

- If you have questions about the implementation of labeling, get advice from PORT managers.

- We will carry out free diagnostics of equipment and programs to ensure compliance with the requirements of the new system, provide an algorithm of actions, and help with the selection and configuration of equipment.

- Come to our offices in Krasnoyarsk or call us on the same phone number.

UTII includes the types of activities included in OKUN. In addition, they must be named in the local list of household services, that is, UTII can be applied to these types of activities in a particular municipality.

Therefore, if you trade these goods in 2021, you will not be able to apply UTII. And even if you haven’t traded anything from this list, but start doing so in the middle of the year, as soon as you make the first sale, you will automatically lose the right to use UTII and a patent.

Common mistakes in maintaining UTII

Let's look at the most common mistakes in maintaining UTII.

| Common mistakes | Explanation |

| The start date of business activity is incorrectly determined | An application to the tax office must be submitted within 5 days from the date of commencement of activities falling under UTII. There is no need to submit an application in advance - you will be forced to pay tax for the period in which there was actually no activity. The date of commencement of business can be considered the date of the first economic fact. |

| The individual entrepreneur does not count himself as an employee | When calculating the tax base for UTII, the physical indicator is the number of employees. But often, when making calculations, an individual entrepreneur does not take himself into account as an employee, because in fact, he is not an employee, which is a mistake. The consequence of this error is an incorrect calculation of the tax base, and, consequently, the tax will be underestimated, which will certainly lead to the accrual of fines and penalties. |

| Incorrect calculation to reduce the amount of UTII | Individual entrepreneurs working independently have the right to reduce UTII by fixed contributions paid for themselves. But if an individual entrepreneur hires workers, then this right is lost, but the tax amount can be reduced due to insurance payments for employees. Please note that the tax amount cannot be reduced by more than half. |

| Lack of activity when applying UTII | UTII is a tax that does not depend on the income received, so even if there is no actual activity of the company or entrepreneur, the tax will still have to be paid. This explains the lack of point in switching to UTII in advance. If an activity falling under UTII is suspended for any reason, it is better to deregister with the tax office. In this case, the tax will be charged on the number of days of the quarter when the activity was carried out. |

UTII: types of activities 2021

Provision of services for the transfer for temporary possession and (or) use of land plots with an area exceeding 10 square meters. m, for the placement of stationary and non-stationary retail chain facilities, as well as catering organizations

Basic UTII yield 2021 by type of activity: full table

Provision of services for the transfer for temporary possession and (or) use of retail spaces located in facilities of a stationary retail chain that do not have trading floors, facilities of a non-stationary retail chain, as well as catering facilities that do not have customer service halls, if the area of each of them exceeds 5 sq. m

If an entrepreneur has chosen one or more types of activities for his business, he needs to check whether he can count on UTII. For this purpose, the presence of this area in the relevant list of Tax Codes is not enough. It is necessary that it correspond to certain physical parameters of the business, which are taken into account in the same document:

FOR EXAMPLE! If an individual entrepreneur decides to open a cafe, then the tax he must pay will depend on the area of the hall where visitors are served, and the imputed income will be calculated from the amount of 1000 rubles. per month. The UTII code for this type of activity is 11. If a service hall is not planned, as, for example, in cheburechnayas, then UTII will depend on the number of hired personnel, and the income rate will increase to 4,500 rubles. per month. The code for such activities is already different - 12, although both of them are related to the organization of public catering.

We recommend reading: Disabled group 3, what are the dsgkfns in 2021 in Moscow

Physical parameters of a business according to UTII

- application in specific areas of business provided for by the Tax Code of the Russian Federation;

- the number of hired employees, including the entrepreneur himself - the owner of the business;

- restrictions on the area of territory or premises;

- the number of units involved (vehicles, etc.).

If any changes are made to the existing scheme of tents and stalls, for example, in a particular market, then these changes cannot affect those tents, vans and stalls that are already operating. That is, if, according to the new scheme, there should not be a tent in some place, but before the changes this tent stood there and worked, then you can move it or remove it after the lease expires.

Using online cash registers

Online cash registers will soon occupy a significant place in the trade sector. The new cash register equipment will differ in that it will send online tax information about completed sales in real time. The online cash register does not require ECLZ or fiscal memory, but a fiscal storage device is required. A fiscal drive is a removable unit used to store, protect and transmit information to the Federal Tax Service. As the drive fills up, it must be replaced, as well as the online cash register. Each copy is registered electronically with the tax authority.

When will the special regime be cancelled?

From July 1, 2021, all entrepreneurs engaged in delivery trade and falling under UTII will be required to start using online cash registers.

| Term | Explanation |

| Until July 01, 2021 | Voluntary use of the online cash register |

| From July 01, 2021 | Mandatory use of online cash register |

In order to start using the online cash register you need to:

- purchase cash register equipment;

- connect the cash register to the Internet;

- select a fiscal data operator and conclude an agreement (indicate the operator’s IP at the checkout);

- register an online cash register with the tax office and receive an online registration card;

- start using it!

For non-compliance with the law and the lack of an online cash register, significant fines are provided (for legal entities at least 30,000 rubles, for individuals at least 10,000 rubles).