What budget classification codes (BCC) for UTII are defined for 2018? Have the BCCs for UTII changed? Have new codes been approved for the single imputed tax? This article presents an up-to-date table with a breakdown of the BCC for UTII for 2021, and also provides a sample payment order for the transfer of a single tax. The table may be useful for legal entities and individual entrepreneurs. If you indicate an incorrect BCC on your payment slip, you will need to clarify the payment. Also see “Changes to UTII in 2021“.

When to pay UTII in 2021

Transfer the calculated amount of UTII to the budget in 2021 no later than the 25th day of the first month following the expired tax period (quarter). This is provided for in paragraph 1 of Article 346.32 of the Tax Code of the Russian Federation. Therefore, the deadlines for paying UTII in 2021 are as follows:

| Deadlines for paying UTII in 2021 | |

| For the fourth quarter of 2021 | No later than 01/25/2018 |

| For the first quarter of 2021 | No later than 04/25/2018 |

| For the second quarter of 2021 | No later than July 25, 2018 |

| For the third quarter of 2021 | No later than October 25, 2018 |

Also see “Terms for payment of UTII in 2021”.

Calendar of reporting and payment of tax on UTII

The UTII declaration is submitted within the deadlines specified in Article 346.32 of the Tax Code of the Russian Federation - no later than the 20th day of the first month following the reporting quarter.

The rule applies: if the deadline for submitting a declaration falls on a weekend or holiday, it is postponed to the next business day. However, in 2021, all these days will be working days, so there will be no postponement of the deadline. Deadlines for submitting UTII declarations in 2021 for individual entrepreneurs and organizations

| Reporting period | Deadline for submitting the declaration |

| 4th quarter 2021 | 20.01.2020 |

| 1st quarter 2021 | 20.04.2020 |

| 2nd quarter 2021 | 20.07.2020 |

| 3rd quarter 2021 | 20.10.2020 |

| 4th quarter 2021 | 20.01.2021 |

We recommend using our online service to prepare your UTII declaration. Spend just a few minutes and you will receive a print-ready and correctly completed report.

Create a UTII declaration

The UTII declaration contains information about the amount of tax to be transferred to the budget, so the Federal Tax Service will immediately be able to control their timely and full payment.

Only 5 days are allotted for this, i.e. The deadline for transfer is no later than the 25th day of the first month following the reporting quarter. Deadlines for paying UTII in 2021 (taking into account the postponement of weekends)

| Reporting period | Tax payment deadline |

| 4th quarter 2021 | 27.01.2020 |

| 1st quarter 2021 | 27.04.2020 |

| 2nd quarter 2021 | 27.07.2020 |

| 3rd quarter 2021 | 26.10.2020 |

| 4th quarter 2021 | 25.01.2021 |

Not sure if you calculated the tax on imputed income correctly? Check the amount on our UTII calculator. And if necessary, you can contact 1C:BO specialists for a free consultation.

Free accounting services from 1C

Where to pay

In 2021, pay UTII according to the details of the Federal Tax Service, which has jurisdiction over the territory where the “imputed” activity is carried out. In this case, the organization must be registered by the Federal Tax Service as a payer of UTII (clause 2 of Article 346.28, clause 3 of Article 346.32 of the Tax Code of the Russian Federation). However, if there are certain types of business that these rules do not apply to, namely:

- delivery and distribution trade;

- advertising on vehicles;

- provision of services for the transportation of passengers and cargo.

For these types of businesses, organizations do not register as UTII payers at the place where they conduct their activities. Therefore, they pay UTII at the location of the head office.

Deadline for payment of UTII in 2021

According to Article 346.32 of the Tax Code of the Russian Federation, taxes are transferred to the budget for individual entrepreneurs and organizations using UTII until the 25th day of the month following the tax period (quarter). The last time you need to pay UTII is for the 4th quarter of 2020 - before January 25, 2021.

Payment of tax to the budget is possible earlier than the specified deadlines, and the listed dates are the deadlines for making payments. As for fines and penalties, they should be listed as they are recognized. If the tax office requires payment of fines and penalties, be guided by the date indicated in the requirement.

Budget classification code for 2018

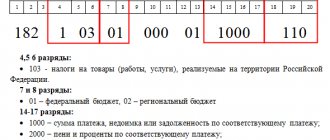

The budget classification code for paying UTII in 2021 is 182 1 0500 110. In payment orders you must put this 20-digit BCC for paying UTII for the 1st quarter of 2021 and subsequent reporting periods.

If, in addition to tax, it is necessary to pay a penalty or a fine, the BCC will be distinguished by four characters from 14 to 17. The meanings of these codes are as follows:

- for imputed tax – 1000;

- penalties – 2100;

- fine – 3000.

As a result, the table with BCC for UTII for 2021 looks like this:

KBK table from 2021 for LLC and individual entrepreneur

| Payment type | KBK details |

| Imputed tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

Payment period

The payment terms are established in Art. 346.32 Tax Code of the Russian Federation. The deadline for payment is the 25th day of the month following the reporting quarter. In 2021 the deadlines are:

- for the fourth quarter of 2021 - until January 27 (01/25 - Saturday);

- for the first quarter - until April 27 (04/25 - Saturday), but due to the pandemic it was postponed to 10/26/2020;

- for the second quarter - until July 27 (07/25 - Saturday), but due to the pandemic it was postponed to 11/25/2020;

- for the third quarter - until October 26 (10/25 - Sunday);

- for the fourth quarter - until January 25, 2021.

Penalties will be charged for late payment. The current BCC for penalties for UTII for individual entrepreneurs and LLCs is 182 1 0500 110. Penalties are transferred based on requirements from the Federal Tax Service.

Legal documents

- Art. 346.26 Tax Code of the Russian Federation

- by order of the Ministry of Finance No. 207n dated November 29, 2019

- Art. 346.32 Tax Code of the Russian Federation

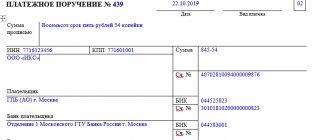

Sample payment order for payment of UTII in 2021

The BCC for payment of UTII in the payment order must be indicated in field 104.

As for the other fields of the payment order for the payment of current UTII payments in 2021, pay attention to the following:

- in field 105 “OKTMO” - OKTMO of the municipality in which the company or entrepreneur is registered as a payer of “imputed” tax;

- in field 106 “Basis of payment” - for current “imputed” payments - “TP”;

- in field 107 “Tax period indicator” - the number of the quarter for which UTII is transferred. Let’s say “KV.01.2018”;

- in field 108 “Document number” – for current payments “0”;

- in field 109 “Date of payment basis document” - for current payments - the date of signing the UTII declaration;

- Field 22 “UIN” – is filled in if the company (IP) pays imputed tax at the request of the Federal Tax Service. Then this detail will be required by the tax authorities. Otherwise, field 22 is “0”.

- field 110 “Payment type” is not filled in.

Example:

Stella LLC pays UTII for the 1st quarter of 2021. The deadline for paying UTII for the 1st quarter is no later than April 25, 2021. In field 104 of the payment, the company will indicate KBK - 182 1 05 02010 02 1000 110. In field 101, Stella LLC will write 01, in field 105 there will be OKTMO, in field 106 - TP, in field 107 - KV.01.2018. The accountant will put 0 in field 108, and in field 109 the date of signing the UTII declaration for the 1st quarter of 2018. In field 21 –5, in field 22 – 0.

Read also

16.11.2017

KBK for payment of penalties on UTII for individual entrepreneurs and legal entities

| PENALIES, INTEREST, FINES | KBK | |

| Penalties, interest, fines on the single tax on imputed income for individual entrepreneurs and legal entities | penalties | 182 1 05 02010 02 2100 110 |

| interest | 182 1 05 02010 02 2200 110 | |

| fines | 182 1 05 02010 02 3000 110 | |

FILES

Budget classification codes for individual entrepreneurs working on UTII

All individual entrepreneurs make two types of budget payments: tax and social. BCCs applied when paying taxes, penalties and fines depend on the taxation system. The code for paying UTII will be the same both when working independently and when you have hired employees. Only in the latter case do entrepreneurs also pay personal income tax for employees (KBK - 182 1 01 02010 01 1000 110). Codes for transferring insurance premiums are common to all individual entrepreneurs.

Table: KBK for payment of insurance premiums

| No. in order | Type of insurance premiums | Used KBK | |

| In 2021 – 2021 | Until 01/01/2017 | ||

| 1 | Compulsory pension insurance (OPI) | 182 1 0210 160 | 182 1 0200 160 |

| 2 | Compulsory health insurance (CHI) | 182 1 0213 160 | 182 1 0211 160 |

| 3 | Compulsory social insurance in case of temporary disability and in connection with maternity (VNIM) | 182 1 0210 160 | 182 1 0200 160 |

| 4 | Compulsory social insurance against industrial accidents and occupational diseases (“injuries”) | 393 1 0200 160 | |

| 5 | OPS for work with hazardous working conditions (additional tariff does not depend on the results of the special assessment) | 182 1 0210 160 | |

| 6 | OPS for work with hazardous working conditions (additional tariff depends on the results of the special assessment) | 182 1 0220 160 | |

| 7 | OPS for work with difficult working conditions (the additional tariff does not depend on the results of the special assessment) | 182 1 0210 160 | |

| 8 | OPS for work with difficult working conditions (special tariff depends on the results of the special assessment) | 182 1 0220 160 | |

| 9 | OPS on yourself | 182 1 0210 160 | 182 1 0200 160 |

| 10 | OPS for yourself (1%, if the amount of annual income exceeds 300 thousand rubles) | 182 1 0210 160 | 182 1 0200 160 |

| 11 | Compulsory medical insurance for yourself | 182 1 0213 160 | 182 1 0211 160 |

Table: BCC for tax payments on UTII

| No. in order | Payment type | KBK |

| 1 | UTII, including debts and additional payments | 182 1 0500 110 |

| 2 | Penalties from UTII | 182 1 0500 110 |

| 3 | Interest on UTII | 182 1 0500 110 |

| 4 | Fines with UTII | 182 1 0500 110 |

What is the BCC for UTII in 2021?

In 2021, the BCC for UTII did not change compared to 2021. As before, the BCC depends on the type of payment (tax, penalty or fine):

| Type of payment for UTII | KBK |

| Tax | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

Differences in the KBK by type of payment (tax, penalty, fine) are only in 14-17 categories (1000, 2100, 3000, respectively).

According to the BCC table, taxes, penalties and fines are listed by both organizations and individual entrepreneurs using UTII.

It is worth noting that KBK-UTII (2019) for legal entities are the same as KBK-UTII (2019) for individual entrepreneurs.

Where to pay UTII

Payment of taxes to the budget according to imputation, as well as payment of fines, interest and penalties, should be made according to the details of the tax office where the entrepreneur or organization is listed as a UTII payer. However, this condition does not apply to certain types of activities:

- transportation of passengers or cargo;

- placement of advertising materials on transport;

- trade that is carried out through delivery or distribution.

Individual entrepreneurs or organizations engaged in the listed types of activities can pay UTII at their place of residence or the address of the organization’s main office. Also, according to paragraph 3 of Art. 346.28 of the Tax Code of the Russian Federation, the Federal Tax Service to which the tax must be paid will be indicated in the notification immediately after registration as a UTII payer.

KBK for tax calculations of individual entrepreneurs on UTII

The table shows the BCC for 2020-2021, which may be needed by an individual entrepreneur working on imputation.

IMPORTANT! In 2021, the list of BCCs is regulated by Order of the Ministry of Finance dated 06/08/2020 No. 99n. In 2021, the list of KBK codes is determined by a new order of the Ministry of Finance dated November 29, 2019 No. 207n, but it has not changed the KBK for UTII. Find out which BCCs have changed here.

| Payment | What is paid | KBK 2020-2021 |

| UTII | The tax itself, including debts and additional calculations | 182 1 0500 110 |

| Penalty | 182 1 0500 110 | |

| Fines | 182 1 0500 110 | |

| Contributions to OPS | Contributions for employees for periods starting from 2021 | 182 1 0210 160 |

| Individual entrepreneur contributions for themselves (in 2019-2021, a single BCC is used for the fixed part and for 1% of the amount of annual income over 300,000 rubles) | 182 1 0210 160 | |

| Contributions to compulsory medical insurance | Contributions for employees for periods starting from 2021 | 182 1 0213 160 |

| Insurance premiums of individual entrepreneurs for themselves for periods starting from 2021 | 182 1 0213 160 | |

| Social Insurance Contributions | Contributions for temporary disability and in connection with maternity for employees for periods starting from 2021 | 182 1 0210 160 |

| Contributions for accidents and injuries for employees | 393 1 0200 160 | |

We pay UTII without penalties

To avoid the obligation to pay penalties, UTII must be paid within the time limits established by Art. 346.32 Tax Code of the Russian Federation. This must be done quarterly. For the past quarter - no later than the 25th day of the first month of the next quarter (clause 1 of Article 346.32 of the Tax Code of the Russian Federation). When the deadline for paying UTII falls on a weekend or non-working holiday, it will be possible to pay the tax on the first working day following such a day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). This will not be considered late, and therefore no penalties will be charged. To avoid penalties, UTII for tax periods 2021 must be paid within the following deadlines:

| Tax periods 2021 | Deadline for payment of UTII |

| 1st quarter | 25.04.2019 |

| 2nd quarter | 25.07.2019 |

| 3rd quarter | 25.10.2019 |

| 4th quarter | 25.01.2020 |

Reporting (UTII) for individual entrepreneurs in 2019

| Period | Deadline for submitting UTII |

| 4th quarter 2021 | January 21, 2021 |

| 1st quarter 2021 | April 22, 2021 |

| 2nd quarter 2021 | July 22, 2021 |

| 3rd quarter 2021 | October 21, 2021 |

For failure to submit a tax return for UTII in 2019 within the established deadlines, a fine is charged in the amount of 5% of the amount of tax payable, but not more than 30% of this tax amount and not less than 1,000 rubles (clause 1 of Article 119 of the Tax Code of the Russian Federation ).

KBK for UTII when paying penalties and fines for individual entrepreneurs

As a general rule, for the payment of a penalty or fine, generally the same BCC is used as for the tax, but the fourteenth from the beginning (or the seventh, if counted from the end of the code) digit from one is replaced by a two when a penalty is paid, and a three in the case of repayment fine

Thus, the BCC for UTII looks like this:

- 182 1 0500 110 - for the tax itself;

- 182 1 0500 110 - for penalties;

- 182 1 0500 110 - for a fine.

A similar procedure applies to personal income tax paid by individual entrepreneurs on UTII from the income of its employees:

- 182 1 0100 110 - tax;

- 182 1 0100 110 - penalty;

- 182 1 0100 110 - fine.

The same rule applies to insurance premiums, but there are exceptions for which it does not work.