Registration of a unit

An OP is registered only when financial and economic activities are carried out through it. This is done within one month from the opening of a new separate structure (clause 4 of article 83 of the Tax Code of the Russian Federation). If there is no activity at the time of creation of the OP, there is no need to register the branch. But the moment the parent company begins to conduct operations through the OP, it will have to be registered within the prescribed period.

IMPORTANT!

The fine for failure to inform about the opening of a separate unit is up to 40,000 rubles.

If you don't report the opening

In addition to registration, the parent organization is obliged to notify the territorial tax service office about the opening of a separate division. This must be done in any case, regardless of whether the activity is carried out through the OP or not. Violation of deadlines and failure to comply with the rule on mandatory notification entails penalties.

Here is a table of all possible fines for failure to report discovery. What penalty will be imposed on the parent company depends on the decision of the inspectors of the Federal Tax Service.

| Amount of fine | Norm | Base |

| 10,000.00 rubles | Clause 1 Art. 116 Tax Code of the Russian Federation | Violation of the deadline for filing an application for registration with the Federal Tax Inspectorate |

| 10% of income received during the entire period of activity of the OP, but not less than 40,000.00 rubles | Clause 2 Art. 116 Tax Code of the Russian Federation | Conducting activities by an organization or individual entrepreneur without registration with the Federal Tax Service |

| 5000.00 rubles | Clause 1 Art. 129.1 Tax Code of the Russian Federation | Late reporting of mandatory information to the Federal Tax Service |

| 200 rubles | Clause 1 Art. 126 Tax Code of the Russian Federation | Failure to submit required documents to the Federal Tax Service within the prescribed period |

For failure to provide information about the opening of an OP, a fine is imposed under clause 1 of Art. 126 of the Tax Code of the Russian Federation in the amount of 200 rubles. But there are cases when controllers took a different position and determined the maximum fine in the amount of 10% of revenues lost to the regional budget. The logic is simple: a branch has opened, activities are carried out in a specific region, but taxes do not go to the regional budget, since the OP was not registered with the territorial department of the Federal Tax Inspectorate.

If you do not report the closure of a separate division

The closure of the OP is reported within three days from the moment such a decision is made (clause 3.1, clause 2, article 23 of the Tax Code of the Russian Federation). If this is not done, the parent company will receive a fine for failure to report the closure of a separate division. There is a special form No. S-09-3-2 for notifying the territorial Federal Tax Service. If you do not send a message within three days, the organization will be fined 200 rubles under clause 1 of Art. 126 of the Tax Code of the Russian Federation. The manager will receive a fine of 300 to 500 rubles.

In addition to the S-09-3-2 form, a notification must be submitted in form R 13002. If you do not submit it on time, the fine will be 5,000.00 rubles (clause 1 of Article 129.1 of the Tax Code of the Russian Federation).

Separate divisions in 2020 and 2021

Separate divisions must pay insurance premiums and submit reports to the tax office only if their individual employees received remuneration. Previously, the obligation arose if OPs had their own bank accounts and separate balance sheets. But this is already a thing of the past - now only if there are rewards.

Convenient calculations for employees and automatic reporting in Kontur.Accounting. Try 14 days free!

Parent organizations must inform the tax service at their location that their OPs can pay salaries to employees and benefits to individuals or, conversely, are now deprived of this right. The Federal Tax Service gives the notification a month from the date of changes.

A little information about separate divisions

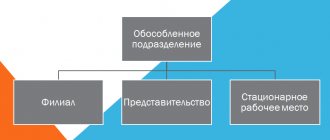

Only organizations have a separate division. This is a room, building or other object that is located at an address different from the organization’s address in the Unified State Register of Legal Entities.

The need to register an EP appears if there is at least one additional workplace that the organization has equipped for an employee. Provided that it is located at a separate address from the parent company and is open for a period of more than 1 month.

A warehouse, an additional office, a meeting room, etc. can become separate. The OP opens separately from the head office and pays taxes at the place of its registration. According to Russian law, any company can open as many separate divisions as it wants.

How to register a separate division

To create a branch or representative office, you will need a decision from the organization’s participants and amendments to the Unified State Register of Legal Entities. Other types of OP can be opened only by order of the head of the organization.

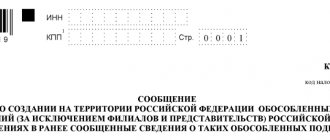

The tax office (at the place of registration of the parent company) must be notified of the opening of an OP a month before the opening by a message in the form C-09-03-1. If the OP will accrue and transfer payments to employees from his bank account, he must additionally submit a separate message to the inspectorate within a month from the date he is vested with such powers in the form of KND 1112536 (Article 23 of the Tax Code of the Russian Federation).

There is no need to register an individual entrepreneur with the Pension Fund of Russia. The Federal Tax Service will transfer all the information to the fund, and it will already register the OPs who pay salaries and have a bank account.

You will have to register the OP with the Social Insurance Fund yourself. This also only applies to OPs with an account that pay employee benefits. This must be done no later than 30 calendar days from the date of creation of the unit. To the FSS office at the location of the OP, submit a registration application, a certificate of opening an account and an order confirming the OP’s right to pay wages independently.

The difference between an OP and a branch or representative office:

A mistake that many people make is to consider branches and representative offices as separate units. This is wrong.

- The presence of an OP must be reflected in the organization’s Charter. A branch or representative office is not necessary.

- The tax office must be notified about the creation of an OP, but not about the creation of branches and representative offices.

- Information about branches and representative offices is indicated in the Unified State Register of Legal Entities, but for other OPs it is not indicated.

- Enterprises with an EP can apply the simplification, but those with a branch and representative office cannot.

Differences in taxes and reporting between the parent company and the OP

There are differences. Separate divisions do not pay all taxes and do not submit all reports that must be submitted to the parent company.

- On the income of the employees of the OP, it is necessary to pay personal income tax and submit 6-NDFL and 2-NDFL to the inspectorate at the place of registration of the OP, but only if the OP itself accrues and pays them remuneration.

- Insurance premiums are paid and reported only at the place of registration of the OP, which itself accrues and pays money to employees from its current account.

- Transport tax at the place of registration of the OP is paid for cars registered at the OP.

- Land and property taxes are paid at the location of the land or real estate. You need to pay tax and report at the location of the OP only if it coincides with the location of the real estate. If the OP has his own current account, then his payment of tax will not be a violation.

- The regional part of the income tax of the OP is transferred to the place of its registration. If the OP is in the same region, you can pay tax at the place of registration of the parent organization.

- VAT is calculated for the entire organization without breakdown by OP. There is also no need to submit declarations separately.

Separate divisions that conduct cash transactions have their own cash books. All these books are transferred to the parent organization. In the cash book of the parent organization, information on cash transactions of the OP is not reflected, unless the OP does not hand over cash to the organization's cash desk under PKO.

From January 2021, a new version of clause 2 of Art. came into force. 230 Tax Code of the Russian Federation. This paragraph established that if an organization and its separate divisions or only divisions are located in the same municipality, the calculation of 6-NDFL and 2-NDFL certificates for them can be submitted to the tax office at the place of registration of one of the OPs or at the location of the organization. To exercise this right, separate divisions must notify all tax authorities where they are currently registered of their choice no later than the 1st day of the tax period.

As for insurance premiums, the legal entity-insurer will need to report the granting of the authority to calculate and pay wages or the deprivation of such authority only if a branch or other separate division has a bank account. Without an account, the department will not be able to interact with the Social Insurance Fund, for example, receive reimbursement for sick leave. Giving departments such powers is a right, not an obligation.

In addition, legislators clarified that it is necessary to report and transfer contributions precisely to the location of such an authorized unit. Previously, if a unit did not have a current account, contributions were paid at the location of the head office.

The fine for unregistered OPs will increase in 2021

For late submission of a notice on the creation of an OP, a fine of 200 rubles is provided for the organization and 300-500 rubles for the director. Violation of the deadline for registering an OP with the Social Insurance Fund will result in a fine of 5,000 rubles if the delay is up to 90 days and 10,000 rubles if the delay is more than 90 days.

Also, for failure to submit reports for an unregistered division, tax authorities have the right to fine the organization. The fine will be 5% of the amount payable on the declaration for each month of delay, but not more than 30% and not less than 1,000 rubles.

Do you need to keep convenient records for an enterprise with separate divisions? Try the online accounting service Kontur.Accounting. It is convenient to calculate salaries, send reports, prepare and pay taxes. The first 14 days of using the service are free for all new users!

Try for free

Arbitrage practice

Parent organizations go to court regarding the amount of the fine and the amount of punishment. There are several solutions regarding penalties for failure to report the opening of a separate structure:

- In accordance with Articles 23, 83 and 84 of the Tax Code of the Russian Federation, organizations are required to notify the Federal Tax Service only about the creation of a separate division, but not about the actions of the enterprise to register an enterprise. The violator is fined under Art. 126 of the Tax Code of the Russian Federation (Resolution of the AS UO No. F09-7309/15 dated October 19, 2015 in case No. A76-2261/2015, Resolution of the AS UO No. F09-10484/15 dated December 28, 2015 in case No. A60-4800/2015).

- Some judges impose penalties for late informing the tax authorities about the opening or closing of separate departments under paragraph 1 of Art. 129.1 of the Tax Code of the Russian Federation (Resolution of the AS MO No. F05-11191/14 dated October 30, 2014 in case No. A40-130227/2013).

- In some cases, tax authorities and arbitration judges determine capital punishment under paragraph 1 of Art. 116 of the Tax Code of the Russian Federation. The basis is the conduct of activities without registration with the Federal Tax Service at the location of a separate structure (Resolution of the AS ZSO No. F04-5897/2016 dated January 27, 2017 in case No. A70-2645/2016).

The Supreme Court of the Russian Federation has a clear position on this issue. The Tax Code of the Russian Federation has established an obligation for taxpayers to report to the Federal Tax Service the existence of special structures within a specified period. A violation is the failure to provide documents to the territorial tax authority, which means that violators should be fined under clause 1 of Art. 126 of the Tax Code of the Russian Federation (Determination of the Supreme Court of the Russian Federation No. 303-KG17-2377 dated June 26, 2017 in case No. A04-12175/2015). This decision is the basis for similar cases and resulting verdicts.

A separate division in the Tax Code of the Russian Federation

In accordance with paragraph 2 of Article 11 of the Tax Code of the Russian Federation, a separate division of an organization is recognized

Based on the definition given in the Tax Code of the Russian Federation, taking into account the requirements of paragraph 4 of Article 83 of the Code, the essential features of a separate division can be identified:

As a matter of priority, when deciding on the creation of a separate division, it is necessary to establish the true meaning of isolation and its essential features. |