Peculiarities

Companies, in accordance with the Civil Code of the Russian Federation, can be created to conduct business activities in general or perform certain tasks. In this they are no different from other entities engaged in economic activities.

A legal entity has the opportunity to open its own separate divisions (hereinafter also referred to as OP). This right is enshrined in Art. 55 of the Civil Code. Let us clarify that merchants are formally deprived of this opportunity.

Opening an OP does not entail the creation of a separate legal entity. It is part of an already registered organization, which means it does not have the same scope of legal rights and obligations.

The Tax Code contains clear features that must necessarily be inherent in “separateness”:

- availability of stationary workplaces;

- different addresses for the head office and the OP.

The absence of at least one of these signs means that there are insufficient grounds for opening a new structure in the OP status. The creation of a “separateness” in this case will contradict Article 11 of the Tax Code. This means that there will not be a separate checkpoint of a separate unit .

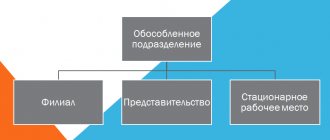

The Civil Code mentions only two forms of OP:

- branch;

- representation.

At the same time, Art. 55 of the Tax Code of the Russian Federation provides another type of separate unit - equipped working positions.

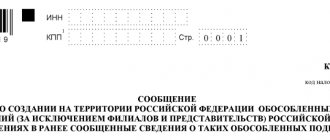

The opening of branches and representative offices implies the appearance of data about them in the Unified State Register of Legal Entities (in the case of equipped workplaces with the status of EP, this does not happen). To do this, you must first fill out an application (there are approved forms) and send it to the tax authorities.

For more information about this, see “How to open a separate division of an LLC: instructions.”

The separate division has not yet received a checkpoint how to trade

Should we pay property tax on fixed assets used by the OP, and if so, where should it be paid? You can read about the possibility of paying personal income tax for employees of several divisions located in the same region with one payment slip: 2011, No. 6, p. . 64

- The Civil Code (Article 55) characterizes a separate division only in the form of a representative office and a branch. That is, from these provisions it is also unclear what other separate divisions, besides a representative office and a branch, can be.

- The Labor Code (Article 40) indicates that “...a collective agreement can be concluded in the organization as a whole, in its branches, representative offices and other separate structural units.”

Update: September 21, 2021

Each domestic legal entity has the right and opportunity to open one or more separate divisions. These can be branches and representative offices, as well as other units, for example, stationary workplaces. The procedure for opening them and the requirements for them are described in some detail in the current legal acts. The opening of representative offices is of a notification nature. Based on the results of such notification, the tax authority may assign a checkpoint for a separate division.

Basic codes

When the registration of an OP has occurred, it may be assigned special codes. But the parent organization and all its divisions will still have the same TIN. This is due to the fact that the OP is not a legal entity.

Thus, find out the checkpoint of a separate division using the TIN of the main enterprise by applying for an extract from the Unified State Register of Legal Entities.

The judgment that there is no need to obtain a separate TIN is based on an analysis of the regulatory document regulating the procedure for obtaining, using and changing the TIN (approved by order of the Ministry of Taxes of Russia dated 03.03.2004 No. BG-3-09/178). And it is valid only when registering or deregistering legal entities and individuals.

A TIN can only be assigned to the organization itself. None of its divisions, including separate ones, have the right to receive their own TIN. Only upon initial registration with the Federal Tax Service does the organization receive its TIN at the place of registration.

General provisions on separate divisions

The Civil Code of the Russian Federation allows for the creation and existence of legal entities that, along with other business entities, take part in business activities or are created to achieve specific goals (Article 48 of the Civil Code of the Russian Federation).

Each legal entity has the right and can create separate divisions (Article 55 of the Civil Code of the Russian Federation). It is important to remember that separate divisions are not legal entities, and therefore lack the legal capacity inherent in legal entities.

By virtue of Art. 11 of the Tax Code of the Russian Federation, a separate division must be located at an address different from the address of the main organization, and have stationary jobs, i.e. jobs created for a period of more than one month. A separate division is not only a branch or representative office, but also a separate stationary workplace (Article 55 of the Civil Code of the Russian Federation and Article 11 of the Tax Code of the Russian Federation).

Information about each separate division (with the exception of stationary workplaces) is indicated in the unified state register of legal entities, for which the organization creating them must submit completed applications to the tax office on approved forms No. P13001, No. P13002 or No. P14001.

After state registration, each branch and representative office may be assigned different codes. However, a separate TIN is not assigned to a separate division, because a separate division is not a legal entity and, as a result, is not a taxpayer (clause 7 of article 84 of the Tax Code of the Russian Federation).

This conclusion follows from the analysis of the “Procedure and conditions for assigning, applying, as well as changing the taxpayer identification number when registering, deregistering legal entities and individuals” (hereinafter referred to as the Procedure), approved by Order of the Ministry of Taxes and Duties of Russia dated 03.03.2004 No. BG-3-09/178.

For example, from the analysis of clause 2.1.2 of the Procedure it follows that a taxpayer identification number is assigned only to an organization and only at the place of its tax registration.

Right to a reason code

Absolutely any business entity receives certain codes, as stated in the law. They are needed for the following purposes:

- identification in classification systems according to various criteria (territory, industry, etc.);

- maintaining records of subjects (for the purposes of taxes and insurance premiums, statistics, etc.).

And if for the main organization codes are an integral attribute, then separate divisions may have their own or coincide with the codes of the main organization.

Any organization must register with the tax service before starting its activities. This is enshrined in paragraph 1 of Article 83 of the Tax Code of the Russian Federation. But not everyone understands which inspectorate they need to contact in order to register. Belonging to the Federal Tax Service can be determined:

- the address of the organization itself (for an individual entrepreneur - the address of his permanent registration);

- the location of its real estate;

- OP's address.

The organization is required to register with the tax office at the address not only of the head office, but also of all separate divisions.

The company must inform the tax authorities about the opening of a separate division. After this, it is registered.

Despite the fact that the parent organization and all its separate divisions have one TIN, KPP is assigned to each of them. This will happen even if the organization does not submit an application to the checkpoint of a separate unit .

Then information about the checkpoint of a separate division is sent from the local tax office to the one where the parent company is registered.

According to the rules on TIN (approved by order of the Federal Tax Service dated June 29, 2012 No. ММВ-7-6/435), when creating any form of a separate unit, it must be assigned a checkpoint.

CPR in legislation

According to Article 83 of the Tax Code, separate divisions (hereinafter referred to as OP) are subject to tax control at the location of each of them. In this case, the registration is carried out by the department itself on the basis of a message from the enterprise about the opening of an OP. Article 23 of the Tax Code of the Russian Federation, in addition to the obligation to register, sets an enterprise a period of one month for registering an OP.

Read more: Deputy Director for Sports and Mass Work

According to Article 55 of the Civil Code, the OP is not a legal entity. This means that it acts on behalf of the head of the enterprise by proxy, is endowed with the company’s property and is not assigned a TIN. But he is assigned a checkpoint. This is done on the basis of Order of the Federal Tax Service of Russia dated June 29, 2012 N ММВ-7-6/ [email protected] .

How to find out

Before you understand the decoding of the assigned checkpoints in order to obtain information about the EP, you need to understand how you can find out including by TIN

Information about such structural divisions as branches and representative offices is displayed in the Unified State Register of Legal Entities (other types of EP do not appear in it). Tax officers transmit all checkpoint numbers of existing separate divisions to the inspectorate at the head office address.

Many people believe that to obtain information about the checkpoint of a separate unit, it is enough to go to the official website of the Federal Tax Service of Russia and request an extract from the Unified State Register of Legal Entities. The exact link is www.egrul.nalog.ru.

However, this won't help. The fact is that by order of the Ministry of Finance dated December 5, 2013 No. 115n, the exact composition of the information in the extract from the Unified State Register of Legal Entities was approved. And the checkpoint of the separate unit is not mentioned in it. Therefore, such an extract will not help to recognize the checkpoint of a separate unit by TIN .

Also see “Electronic services for accountants on the Federal Tax Service website: use wisely.”

Therefore, there are two options left:

- send a request to the tax office (or to the counterparty you are interested in);

- use various databases (but no one is responsible for their reliability).

Can different organizations have the same checkpoint?

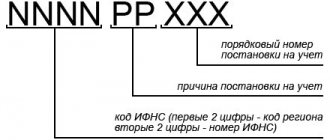

KPP is the reason code for registration.

It can be obtained as a supplement to the TIN when registering a taxpayer. This code shows which tax authority the enterprise or any of its structural divisions belongs to, and on what basis each of them is registered. One enterprise may have several checkpoints. A code of this type is included in a special certificate or notice that is issued by the tax authority to an enterprise or its separate division upon registration.

Where does it appear?

The checkpoint must be indicated as part of the details of the legal entity in all official papers and forms of the organization. It must be reflected in the texts of contracts, various letters and powers of attorney.

There are a number of forms in which checkpoints are a mandatory element. For example, checkpoint in the invoice of a separate division . It is indicated when the OP sells something through himself.

EXAMPLE The sale of goods produced by the parent organization is carried out by its separate division. Then the checkpoint is written on the invoice not of the main office, but of the OP that makes the transaction. The same rule applies if goods are purchased by a separate division.

But the TIN is indicated to the parent organization, since the OP does not have its own.

Read also

28.11.2016

Same checkpoints for different organizations

The TIN is assigned to any person upon registration; this number is unique and does not change under any circumstances. In contrast, the checkpoint depends on the region and tax authority to which the enterprise is attached, so all organizations belonging to the same tax authority can have the same checkpoint. Provided that the reason for registering with these organizations also coincides.

That is, the same number can be assigned to many organizations when they are registered with the same tax office.

What is an organization's checkpoint

KPP is a set of numbers that complements the TIN. It determines on what basis the legal entity is registered. Includes 9 characters. The checkpoint is deciphered in the organization details as follows:

- the first two digits are the code of the region or region of the Russian Federation where the company is registered;

- the second pair of digits is the number of the Federal Tax Service, which registered the company or separate division at the place of its registration, location of real estate or transport. This may also be the number of the inspection that performed other registration actions;

- the fifth and sixth digits are the direct reason for accounting. For Russian organizations, values from 01 to 50 are available, for foreign companies - from 51 to 99. Unlike all other characters, there can also be Latin letters;

- the last digits in the organization’s checkpoint are the serial number.

From the decoding you can understand how the checkpoint is assigned to an organization. Important points are the place of registration and the reason.