All entrepreneurs and organizations paying income to individuals are recognized as tax agents. At the end of the calendar year, they must submit a declaration filled out in form 2-NDFL to the tax office. This document must contain information about all individuals who received income in the reporting period, as well as the amount and timing of payments. Column 2.3 “Taxpayer Status” in 2-NDFL raises many questions: how to determine the status of a foreign employee; what tax rate to apply to a particular group of foreigners; what to do if the status has changed during the reporting period, etc. Let's figure it out.

Taxpayer status in 2-NDFL

What are the statuses and codes?

Starting from 2021, there are six taxpayer statuses, each of which is assigned a code.

Table 1. Codes assigned depending on taxpayer status

| Code | Status |

| Code 1 | Placed if the individual is a resident of the country. |

| Code 2 | The individual is not a resident. |

| Code 3 | A highly qualified specialist, he is also not a resident. |

| Code 4 | Participant in the state program for the return of compatriots to their homeland. Non-resident of Russia. |

| Code 5 | Non-resident refugee. |

| Code 6 | A citizen of another country working in the Russian Federation on the basis of a patent. |

On a note! The employee’s status code determines what percentage will be deducted from his income.

To determine which code should be in 2-NDFL and at what rate to calculate taxes, follow this algorithm:

- Check if the foreign employee has a special status.

- Find out whether he is a resident or not.

- Find out exactly what income needs to be paid to the foreigner.

Read more about each tax status below.

About country codes for personal income tax certificates: country code for Russia, Ukraine, Uzbekistan - website about

Sometimes you have to submit documents to the tax office to receive a deduction. Whether the request is approved or not depends on their correct preparation. Therefore, it is important to approach the filling with full responsibility. For example, enter the correct country code. If you are a Russian citizen, for personal income tax certificate 2 it will be 643. This certificate and many other documents indicate the same number.

Help 2 personal income tax

The most popular document for determining the material income and tax accounts of an individual for the required period of time is certificate 2 of personal income tax. Basically, it is filled out in the accounting department by the end of the year, summing up the results, and transferred to the tax office, but it can also be issued at the request of the employee.

Upon request, a certificate is issued in the following cases:

- 2 personal income taxes are required when obtaining auto, mortgage or consumer loans. Sometimes they may be required to take out a large cash loan.

- Issued automatically upon dismissal of an employee. If you haven’t done this, you will have to request a certificate for a new official employment.

- It is transferred to the tax service when a deduction is required. Let's say a deduction is possible for citizens whose children study at a higher educational institution on a paid basis.

- Upon retirement and further calculation of benefits.

- If a person decides to adopt a child.

- In litigation, one way or another, related to labor relations.

- When the issue of alimony obligations is resolved.

In its final form, the document must bear the seal and signature of the head of the enterprise. According to the standard, the certificate is issued within three working days, excluding holidays and weekends.

There is no need to return it to the accounting department. However, it is important to remember that the company has the right to indicate the calculation only for the time during which the employee worked at this particular workplace. This applies to cases where a person has managed to change several jobs over the past year.

Filling rules

Issuing a personal income tax certificate 2 is a common matter, but sometimes it is not at all easy. An inexperienced accountant may have problems.

Feature selection

The first thing a specialist faces is identifying the sign. There are two types of signs:

- Filling out occurs for any employee receiving wage payments from the enterprise and deductions from them. This also includes funds protected from personal income tax withholding. A certificate with this indication must be submitted to the tax office no later than April 1.

- All other situations when it is impossible to deduct taxes from certain material assets. For example, if you need to pay for a gift for a person who is not an employee of the company. Temporary dates: until the first of March. In addition, you must indicate the amount of income that is not subject to taxation and the possible amount of tax.

Usually in the second case you have to make two certificates with different characteristics at once. The first is all income in aggregate, the second is the amounts protected from withholding.

Code of the country

The second task is to indicate a reliable country code. Today there is an OKSM classifier of country codes. It was approved on December 14, 2001 by Gosstandart under number 529-ST.

Information from it can be found for free on many legal Internet resources, but it is important to remember that the database is constantly updated and subject to adjustments.

Therefore, it is necessary to monitor the relevance of the information that comes across on sites and weed out outdated versions. For example:

- Russian citizenship code for personal income tax certificate 2 is 643.

- Belarus - 112.

- Uzbekistan - 860.

- Kazakhstan - 400.

- Armenia - 051.

- Ukraine - 804, etc.

The original classifier is located directly on the official website of Gosstandart. You can also find its changes there, but they are all located separately, which creates a number of inconveniences when searching for the necessary information.

Example document

The standard certificate form has several parts to fill out. The first part includes:

- Full legal name of the organization that was involved in issuing this certificate.

- 1st or 2nd sign indicating the possibility of collecting tax deductions.

- Document data: number, date of completion, what time frame was taken as the basis for the calculation.

- Territorial code of the tax service with which the enterprise is registered.

- The serial number of the adjustments made. If there were none, you must enter the number 0.

- Landline telephone number of the work organization. Required with area code.

- Payment details of the enterprise: taxpayer identification number (TIN), All-Russian Classifier of Municipal Territories (OKTMO) and reason for registration code (KPP). For individual entrepreneurs, it is permissible to put a dash.

- Personal data of the employee for whom the certificate is issued: last name, first name and patronymic, tax identification number, residential address.

- Official taxpayer status. Usually for a Russian resident there is only one.

- State code from classifier 529-ST. This can be either the Russian Federation or any other country from which the employee arrived.

- Code of the employee’s personal identification document, as well as its number and series. Russian passport code is 21.

The second part is further divided into three more sections. Here they describe monthly material income, tax and other deductions, the amount of actual tax and that already paid.

The third part displays income in coded form. For example, salary code is 2000, vacation payments are 2012, other one-time amounts are 2720. All this is subject to personal income tax.

The fourth is coded deductions. For example, code 126 is a deduction for a minor child.

The fifth part is the total amount of personal income tax. To calculate, you need to add up the income for the entire previous year and subtract deductions. From the amount received, calculate 13 percent (if the rate is for the first taxpayer status).

Document for a foreigner

If a citizen of another country works for an organization and requires a 2nd personal income tax certificate, the procedure remains the same. However there is a slight difference :

- The amount of the tax rate directly depends on the length of residence and work in the Russian Federation. For 183 days or more of continuous stay, the rate will be the usual - 13 percent. In addition, in the certificate the taxpayer status will be standard - 1. If the stay is shorter than the established framework, then the rate increases to 30, and the status - 2. There may be other statuses. For example, visitors from the Eurasian Economic Community countries. Their rate is 13% anyway.

- It is necessary to indicate permanent citizenship according to OKSM, regardless of Russian temporary documents.

- It is not necessary to fill out the column with a Russian or foreign TIN.

- You can indicate your place of residence both in Russia and in your home country, but always with a code.

- The identity document of a foreign citizen is entered under code 10.

- In the fifth section, a column with fixed income is added. This is if the employee works on the basis of a patent. In addition, it is permissible to apply to the NFS to reduce personal income tax by an amount equal to fixed payments. After receiving official permission, indicate its number and date of receipt.

If you take into account all the above factors, then registering 2nd personal income tax should not cause much difficulty . The main thing is to correctly understand country codes and other encodings. These can be found in government legal documents.

Source:

Citizenship and country code for reference 2 Personal income tax: formation features

The main document regulating the filling out of form 2 of personal income tax is the order of the Federal Tax Service dated October 30, 2015 with all changes registered as of the date of compilation of the indicators.

In addition to the Internal Revenue Service, for which information on income is generated at the end of the reporting year, a certificate may be needed from a physical person. face in many situations. Some fields are difficult to fill out, for example, which region code to indicate in the second part. If there are no questions for a resident of the Russian Federation, what about non-residents?

In the review, we will consider all the nuances of the formation of this graph according to the OKSM classifier of countries of the world.

Resident

The vast majority of Russian workers fall into this category. Therefore, in section 2.3 of the 2-NDFL declaration, accountants most often put code No. 1.

Tax resident is an individual who has lived in the state for at least one hundred and eighty-three days during the previous twelve consecutive months. These 183 days also include arrival and departure dates.

Who is a Tax Resident of the Russian Federation? Our article will help you figure this out. In it we will look at what the tax status depends on, documents for confirmation, as well as the regulatory framework for residents and non-residents.

If an individual did not live in Russia, but received treatment or education abroad, the period of his absence will not be counted towards 183 days.

For residents, the income tax rate is 13%

Video - Confirmation of Russian tax resident status

Filling out personal income tax certificate form 2

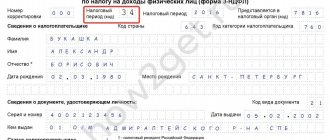

In paragraph 2.3 “Taxpayer status” the taxpayer status code is indicated. If the taxpayer is a tax resident of the Russian Federation, the number 1 is indicated, if the taxpayer is not a tax resident of the Russian Federation, the number 2 is indicated, if the taxpayer is not a tax resident of the Russian Federation, but is recognized as a highly qualified specialist in accordance with Federal Law dated July 25, 2002 N 115- Federal Law “On the Legal Status of Foreign Citizens in the Russian Federation”, then the number 3 is indicated. In paragraph 2.4 “Date of Birth”, the date of birth (day, month, year) is indicated by sequentially recording data in Arabic numerals, for example: 05/01/1945, where 01 is date, 05 - month, 1945 - year of birth. In paragraph 2.5 “Citizenship” the numeric code of the country of which the taxpayer is a citizen is indicated. The country code is indicated according to the All-Russian Classifier of Countries of the World (OKSM). For example, code 643 is the code of Russia, code 804 is the code of Ukraine. If the taxpayer does not have citizenship, the code of the country that issued the document proving his identity is indicated in the “Country Code” field. Clause 2.6 “Identity document code” indicates the code that is selected from the “Document Codes” Directory. In paragraph 2.7 “Series and number of the document” the details of the taxpayer’s identity document are indicated; accordingly, the series and number of the document; the “N” sign is not affixed. Clause 2.8 “Residence address in the Russian Federation” indicates the full address of the taxpayer’s permanent place of residence on the basis of an identification document or other document confirming the address of residence.

Address elements are: “Postal code”, “Region code”, “District”, “City”, “Settlement”, “Street”, “House”, “Building”, “Apartment”. If you have any questions, you can consult for free via chat with a lawyer at the bottom of the screen or call by phone (consultation is free), we work around the clock.

“

Region code ” is the code of the region in which the individual has his place of residence. The region code is selected from the Region Codes Directory. “ Postal code ” is the index of a communications company located at the taxpayer’s place of residence. When reflecting the "house" address element, both numeric and alphabetic values can be used, as well as a "/" sign to indicate a corner house. For example: 4A or 4/2. Modifications of the “structure” type are filled in the “body” field. Let us give the following examples of filling out the elements of the address of residence. Example 1 . The address, Moscow, Leninsky Prospekt, building 4a, building 1, apartment 10, is reflected as follows. The “Postal Code” field indicates 110515; in the “Region code” field 77 is indicated; in the “Street” field, Leninsky Prospekt is indicated; in the “House” field 4A is indicated; in the “Body” field, 1 is indicated; in the “Apartment” field 10 is indicated Example 2 . Address Moscow region, Naro-Fominsk district, Aprelevka, microdistrict. Augustinsky, house 14, building 1, apartment 50 is reflected as follows. The “Postal Code” field indicates 143360; in the “Region code” field 50 is indicated; in the “District” field the Naro-Fominsk district is indicated; in the “City” field Aprelevka city is indicated; in the “Street” field the microdistrict is indicated. Augustinian; in the “Home” field 14 is indicated; in the “Case” field, page 1 is indicated; in the “Apartment” field - 50. Example 3 . Address Voronezh, Borovoe village, st. Gagarina, house 1 is reflected as follows. The “Postal Code” field indicates 394050; in the “Region Code” field 36 is indicated; in the “City” field indicate Voronezh; in the “Settlement” field, Borovoe village is indicated; in the “Street” field, Gagarina Street is indicated; in the “House” field, 1 is indicated. Example 4 . The address Ivanovo region, Ivanovo district, Andreevo village, 12 is reflected as follows. The “Postal Code” field indicates 155110; in the “Region code” field 37 is indicated; in the “District” field the Ivanovo district is indicated; in the field “Settlement” Andreevo d is indicated; in the “Home” field, 12 is indicated. If one of the address elements is missing, the field allocated for this element is not filled in and may not appear in the Help. In clause 2.9 “Address in the country of residence” for individuals who are not tax residents of the Russian Federation, as well as foreign citizens, the address of residence in the country of permanent residence is indicated. In this case, the code of this country is indicated in the “Country Code” field, then the address is written in any form (letters of the Latin alphabet are allowed). For individuals who are not tax residents of the Russian Federation and foreign citizens, the absence of the indicator “Residence address in the Russian Federation” is allowed, provided that clause 2.9 of the Certificate is completed.

Non-resident

If a foreign employee stays in the country for less than 183 days, he is considered a non-resident. The status of “non-resident of the Russian Federation” has several features:

- A non-resident is required to pay tax and submit a declaration to the fiscal authority only if he received income from a source located on Russian territory.

- A non-resident cannot receive a tax deduction.

- If, as a result of a change in status from non-resident to resident, tax was overpaid, the money can only be returned to the tax office (not through the employer) at the end of the calendar year.

Resident or non-resident status does not depend on citizenship. A resident can be not only a citizen of Russia, but also a citizen of another state or a stateless person. A non-resident can be:

- Russian citizen living abroad;

- a foreigner who arrived less than six months ago.

Filling out a certificate by Russians

Regardless of whether your place of permanent registration is Russia, Ukraine, Belarus or another country, when filling out tax forms and other documents related to work and income, you must know all the necessary codes, OKIN, citizenship, etc. Until they are entered in the appropriate boxes, the document will be considered invalid, since it will not provide complete and comprehensive information about you. Russian citizens will need to indicate the code combination of numbers assigned by the Russian Federation in the 2-NDFL certificate. It is written in paragraph 2.5 of the second block of the document called “Data on a civilian.” The OKSM of the Russian Federation is assigned the number 643. It must be entered in the above column. The status of a stateless person does not relieve you of the obligation to enter the data recorded in the classifiers into the certificate. In the document, such a person needs to enter information about the country that issued him the identity paper. The 2-NDFL certificate form and a sample form can be downloaded here.

Sample of filling out the 2-NDFL certificate Next, continuing to work with the certificate, you should repeat the number from paragraph 2.5, but in line 2.9. Next, indicate the detailed address where the person for whom the document is being filled out lives. If we are talking about a foreign citizen, it is not the Russian temporary registration where the registration was carried out that is entered, but information about the foreigner’s place of residence in his homeland, the code of which he indicates, taking it from the all-Russian classifier. For convenience, the line can be filled in with both Cyrillic characters and Latin characters.

Documents confirming residence

According to the law, the tax agent himself keeps records of data about his employees and independently determines his status. And based on this, the tax amount is calculated. An employee's residence can be confirmed by the following documents:

- a passport containing information about the date of crossing the Russian border;

- a visa containing the appropriate notes;

- air tickets, railway tickets;

- papers on registration of foreigners temporarily living in the Russian Federation;

- contract with the employer, civil contract;

- a time sheet in which labor time was recorded.

Air ticket can confirm your residence

Personal income tax for citizens with a residence permit in 2021

2. Foreigners operating on the basis of a patent In the case of a patent, personal income tax from foreigners in 2021 is paid at a rate of 13%. When determining the amount of tax deductions, the employing company's accountant must deduct from the employee's fiscal obligations the amount of the advance payment transferred when purchasing the permit.

We recommend reading: Lawsuit against Non-Payers of Membership Fees SNT

And finally, if highly qualified specialists with the status of permanently or temporarily residing in the Russian Federation are involved in work, then pension and social contributions for them are paid at regular rates, and the employer does not make deductions for healthcare.

Highly qualified foreign specialists

A highly qualified specialist is a foreigner who has outstanding skills, knowledge, and experience in some field of activity. Such an employee must have signed an employment contract with a company from Russia. Payment for the work of a valuable foreign employee must be at least two million rubles per year. But for teachers and researchers, the minimum wage may be less - from one million rubles.

On a note! The income of a highly qualified foreign specialist is taxed at 13%, even if he is a non-resident of the Russian Federation.

The employer must assess the level of competence and qualifications. Evidence of a high level of knowledge and experience can include:

- diploma;

- education certificates;

- comments from previous employers about the employee;

- awards;

- information from specialized organizations.

The status of a highly qualified specialist is awarded to a foreign employee from the moment a work permit is issued. The document must contain a corresponding note.

The thirteen percent rate for this category of workers can be used even if the employment contract is concluded for a short period. If the contract is drawn up for a period of less than 1 year, the amount of remuneration for the period of work must be at least two million rubles.

The reduced rate applies only to those incomes of a valuable specialist that relate to labor payments. For example, salary, production bonuses, payment for services.

All income that goes beyond the scope of the employment relationship is taxed at 30%, even if the money is transferred by the same employer

On a note! If a specialist has left the country and payments must be made outside the Russian Federation, then a 13% rate is still applied to the income. For the last payments after the dismissal of a foreign employee, the tax amount also remains unchanged.

Personal income tax for foreign citizens in 2021

Step 4. 10 working days after submitting the documents, officials will issue a work permit or notice of refusal. When obtaining a patent, a foreigner must provide a receipt that confirms the payment of the advance payment for personal income tax. It may happen that a foreigner does not make payments for the months for which his permit is extended. Then it ceases to be valid from the day following the end of the period for which the advance payment was paid (paragraph 3. 4 clause 5 art. 13.3 of Law No. 115-F)

First of all, the cost consists of personal income tax (NDFL), in 2021 it is the same for everyone and amounts to 1,307 rubles. This figure is multiplied by a coefficient that is established annually by government agencies in different regions. Thus, in Moscow the cost of a patent is 4,000 rubles, in St. Petersburg – 3,000 rubles, and in the regions even less. The document is issued for a period of one to three months, after which it must be renewed every month.

Participants in the program for the return of compatriots

Code 4 in the “Taxpayer Status” section is applied if the employee is a participant in the program for the return of compatriots from the CIS countries to their homeland, Russia. Various social benefits are provided for this category of foreigners and their families, including a reduced percentage of income tax.

Rules for calculating personal income tax for immigrants:

- Wages, payments for services, bonuses and other earnings received as a result of work activities are taxed at 13%. The percentage should not be higher, even if the employee is a non-resident of the country. The benefit can be applied only after the foreigner presents a document proving the fact of participation in this state program. When hiring an accountant, you need to keep a copy of the document and regularly check its validity period. The certificate is issued to the migrant for three years.

- The rate applied to other unearned income depends on whether the immigrant becomes a resident. If yes, the percentage is 13%; if not - 30%. The category of unearned earnings includes gifts, financial assistance, and income from rental property.

- Standard group deductions can only be applied if the migrant has already become a resident.

On a note! A program participant has the right to find employment in the Russian Federation without a work permit.

Classification of population information

Upon hiring, all new employees receive personal cards for all new employees. They also contain the following information:

- Family status.

- Presence or absence of education.

- Knowledge of languages of other countries.

- Citizenship, etc.

To fill them out, you will need OKIN - another classifier used in Russia to systematize information about the population.

Whether you are a stateless person or have been adopted in one of the countries of the world, this document must be created for you.

The current OKIN was approved in 2015.

Having entered into force, it abolished its previously valid counterpart. The classifier used for T-2 cards is a set of digital blocks that can be used in various documents. If you have any questions, you can consult for free via chat with a lawyer at the bottom of the screen or call by phone (consultation is free), we work around the clock.

Information collected for population accounting is systematized and studied using OKIN. The advantage of the classifier is that it consists of facets that can be applied independently of each other. We invite you to watch the video, which describes in detail how to correctly fill out the 2-NDFL certificate.

The population registration system continues to be improved and brought in accordance with international standards. Taxpayers must be aware of all changes that occur. Filling out a 2-NDFL certificate in relation to a foreign worker is practically no different from filling out a certificate in relation to a Russian employee, but has some features.

Refugee

Since October 2014, all income paid to refugees and those who have received temporary housing in the Russian Federation is subject to a reduced income tax rate of 13%.

Code 5 in the “Taxpayer Status” section is entered only if the employee is a non-resident of the country. For non-residents, only income received as a result of work is subject to a thirteen percent tax. All other payments (gifts, financial assistance) are subject to taxation at the same percentage for all non-residents - 30%.

On a note! A refugee cannot count on standard group deductions before he receives Russian tax resident status.

To receive a deduction for children, a refugee must legalize documents (birth or adoption certificate) in the territory of our state. This can be done at the consular offices of the republic that issued the document.

If the country in which the certificate was received is a party to the Hague Convention, it is enough to certify the document with an apostille

Filling out a certificate by Russians

Regardless of whether your place of permanent registration is Russia, Ukraine, Belarus or another country, when filling out tax forms and other documents related to work and income, you must know all the necessary codes, OKIN, citizenship, etc. Until they are entered in the appropriate boxes, the document will be considered invalid, since it will not provide complete and comprehensive information about you.

If you have any questions, you can consult for free via chat with a lawyer at the bottom of the screen or call by phone (consultation is free), we work around the clock.

Russian citizens will need to indicate the code combination of numbers assigned by the Russian Federation in the 2-NDFL certificate. It is written in paragraph 2.5 of the second block of the document called “Data on a civilian.” The OKSM of the Russian Federation is assigned the number 643. It must be entered in the above column. The status of a stateless person does not relieve you of the obligation to enter the data recorded in the classifiers into the certificate. In the document, such a person needs to enter information about the country that issued him the identity paper. The 2-NDFL certificate form and a sample form can be downloaded here. Sample of filling out the 2-NDFL certificate Next, continuing to work with the certificate, you should repeat the number from paragraph 2.5, but in line 2.9. Next, indicate the detailed address where the person for whom the document is being filled out lives. If we are talking about a foreign citizen, it is not the Russian temporary registration where the registration was carried out that is entered, but information about the foreigner’s place of residence in his homeland, the code of which he indicates, taking it from the all-Russian classifier. For convenience, the line can be filled in with both Cyrillic characters and Latin characters.

Foreigners working under a patent

If a foreign employee is a citizen of a visa-free country, he must apply for a patent. This document gives the right to work on the territory of the Russian Federation. A labor patent is necessary both for hired work and for individual entrepreneurial activity or opening a company.

Citizens of Kazakhstan, Kyrgyzstan, Armenia and Belarus do not need to obtain a patent. These countries are not only visa-free, but also part of a single customs union with Russia. According to international agreement, patents and work permits are not required for natives of these four states.

Citizens of other visa-free countries - Uzbekistan, Ukraine, Abkhazia, Azerbaijan - need to obtain a patent.

The patent indicates the territory in which the foreigner has the right to work. So, if the document was issued in the Moscow region, a foreigner cannot work in Moscow. And, conversely, a patent issued in Moscow does not give the right to work outside its borders.

On a note! The employer must prevent double taxation, since there is a possibility of calculating personal income tax twice - when the employer accrues income and when paying advance payments for the patent. The employer is obliged to help the foreign employee reduce tax. To do this, it is enough to reflect this information in the 2-NDFL certificate.

It is also possible to receive a refund of overpaid income tax by a foreigner. The employer can also help the employee with this. The amount that is planned to be returned should not exceed the amount of the advance payment for the month. Also, the amount to be refunded depends on the employee’s income.

On a note! Since the sizes of monthly advance payments are different in all regions, the amounts to be returned will also be different.

How to make a tax refund

The return of tax to a foreign employee begins with the employer sending an application to the Federal Tax Service. Also, a certificate filled out in form 3-NDFL must be provided to the tax office. You need to have copies of receipts for advance payments with you. The documents must be sent to the department in which the employer is registered.

The response from the Federal Tax Service will come no later than 10 days after submitting the documents

The employee first worked on the basis of a permit, and then quit and was hired again the same year, but on the basis of a patent

In this case, the employer is obliged to recalculate the tax. This must be reflected in the 2-NDFL declaration as follows:

- You only need to submit one 2-NDFL certificate.

- In the line “Taxpayer Status” you need to enter code No. 6, as for an employee who works under a patent.

- The tax rate should be 13%.

When working on the basis of a permit, a 30% tax is deducted from the employee. When switching to a patent, the rate changes to 13%. Personal income tax must be recalculated for the entire current year, and the overpaid tax must be returned to the foreigner.

It does not matter in what month the notification from the fiscal authority arrived. The employer can reduce the tax for the entire year in which the permit was received. So, if the notification from the tax office arrived in April, and the validity of the patent begins in February, personal income tax can be recalculated for the entire time period from February to April.

What should I do if my tax refund was not made last year?

A situation often arises when, in the past year, a refund of overpaid personal income tax was not issued for an employee registered under a patent. In this case, it will no longer be possible to return the tax. The legislation does not provide for the possibility of a foreigner returning personal income tax in the past year.

The validity period of a patent covers two periods (years)

Many people who fill out the declaration do not know how to return the money if the patent expires over two periods. A tax refund is possible only after receiving a “permit” notification from the fiscal inspectorate. Returns can only be made in the year in which this notification was received. For example, a patent affects both 2021 and 2021. If the notification was received in 2018, then only the tax that was overpaid in 2021 can be refunded.

Example. A foreign employee with a patent was hired by a Russian company. The document is valid from November 1, 2017 to March 1, 2018. The new employee provided checks for payment of monthly advances in the amount of 20,000 rubles.

In 2021, the employer received a notification from the Federal Tax Service about the need to take into account advance payments when calculating personal income tax. Since permission from the fiscal authority was received in 2021, only that part of the payments that are included in this time period needs to be taken into account. This means that from the total amount paid for advance payments, you need to subtract what is due in 2017.

The period we are considering has 120 calendar days.

20,000 / 120 = 166.7 rubles

In 2021, the patent was valid for 61 days, so 166.7 * 61 = 10,168.7 rubles

In 2021, 20,000 – 10,168.7 = 9,831.3 rubles were paid

Thus, the employer can reduce the income tax of a foreign employee by 9,831.3 rubles.

Personal income tax of Ukrainian citizens with RVP 2021

Hiring citizens of Tajikistan in 2021. Having determined the status, residence and type of income paid, we look at what personal income tax rate should be applied. The tax status of the taxpayer is resident or non-resident.

Foreign citizens can work in Russia under a patent, temporarily. When payments in favor of foreigners are not subject to contributions in 2021.

However, for certain foreign borrowers, special rules remain relevant, which apply to the return of personal income tax to foreigners working under patents in 2021 and double taxation of personal income tax.

For foreign citizens who during the calendar year changed their status from non-resident to resident status of the Russian Federation, a system for recalculating personal income tax is provided. Insurance premiums for foreigners on patent in 2020.

Rules for the employment of foreign citizens with a temporary residence permit in 2021. At the moment, loans to foreign citizens with a temporary residence permit are not provided by this organization, just like credit cards.

And it turns out that a foreign citizen pays personal income tax twice.

Personal income tax of a citizen of Ukraine with a temporary residence permit

Good afternoon A Ukrainian citizen wants to work in our company; she is registered in Volgograd at her place of stay and has a TRP (temporary residence permit), but has no citizenship. How much personal income tax should be withheld from her salary and will she be entitled to a deduction for 1 child under 18 years of age? (I have a son - 14 years old). Lives in Volgograd since July 2014. Is he a resident?

Julia, hello. A resident of the Russian Federation is any individual, regardless of whether he is a citizen of Russia or another country, who stays on the territory of the Russian Federation for more than 183 days during one calendar year. The presence or absence of a temporary residence permit does not affect the tax in any way - the length of actual stay in the Russian Federation is important.

More than 184 days - 13%, less - 30%. A resident is entitled to benefits, a non-resident is not.

Filling out a 2-NDFL certificate for a foreigner

- official salary;

- additional income - from authorship, innovation, publications;

- any activities subject to payment;

- financial deposits indicating the currency equivalent;

- stock earnings;

- insurance charges;

- buyouts;

- rental income;

- profit from the sale of goods or products;

- maternity, pension, vacation and sick leave accruals.

The document reflects information about both the employee and the employer. As part of regulations and legislation, all migrants working in enterprises in the country must have a special permitting patent.

How to hire a citizen of Ukraine with a temporary residence permit in 2021

If a person lived in eastern Ukraine at the time of the outbreak of the military conflict, he can receive refugee status in Russia.

For such citizens, the procedure for getting a job has been simplified; the state has made this process as simple as possible.

For refugees and their families, according to the new law in force since 2020, the admission process is carried out in the same way as for people with Russian citizenship, but the identification document will be an asylum certificate

- Monitor the registration of a Ukrainian citizen for migration registration with the Federal Migration Service. The law allows citizens of Ukraine to register later than others - they are given 90 days to do this. But, it is better to carry out this procedure earlier in order to quickly resolve the issue with the work. To obtain a registration order, the employer must contact the Federal Migration Service at the place of the migrant’s actual stay. The authorities must provide the employee’s internal passport, a stamped migration card, and a power of attorney to perform actions for the employing company. If the employee will live in a room or apartment allocated by the company, you must also bring documents proving the legal entity’s ownership of the premises provided.

- The second stage is obtaining a work permit for the migrant. This can be done some time later, after the migrant is registered. You again need to contact the territorial bodies of the Federal Migration Service at the place of residence of the citizen of Ukraine. The following documents will be required: a Ukrainian passport, a migration card with a registration mark, an application for obtaining a permit and a receipt for payment of the state fee. The issuance of residence and work permits in Russia is paid, therefore, you will have to pay a fee of 1,600 rubles. In the case where the documents are submitted by the employer, the period for preparing a residence permit is significantly reduced. The whole process will take about ten days. If the documents are submitted by a foreign citizen himself, you will have to wait several months.

- After issuing a temporary residence permit, a foreigner can be officially employed. But, before this, he must undergo a full medical examination to make sure that the person’s health allows him to work, and also that he does not pose a danger to other people. The employer independently sends the employee for examination; this must be done immediately after the permit is issued. Within a month after registration of the temporary residence permit, a health certificate must be submitted to the migration service, otherwise their decision will be cancelled.

- The final stage is the conclusion of an employment contract. This procedure is standard; not only migrants, but also residents of Russia undergo it when applying for a job. It is no different from the procedure for employing a Russian in a company. If a Ukrainian gets a job in Russia for the first time, his company must transfer information about the person to the Pension Fund and arrange insurance for him, if this is provided for by the company’s policy.

Personal income tax for foreigners with temporary residence permit in 2020

Sample of filling out an application for a temporary residence permit 2021 in Moscow At what rate should personal income tax be withheld from the income of a citizen of Ukraine with a temporary residence permit? len-a (question author) 0 points January 9, 2021 at 4:32 pm 11/19. Let's consider how to calculate the tax on income of foreigners on a patent in complex cases.

Personal income tax from Ukrainians in 2021 with a residence permit. If the period of residence in the Russian Federation has already been 3 years, you will need a document that can confirm the availability of housing.

Every year he himself goes to the Federal Migration Service and submits data on employment and 2-personal income tax.

In cases where the validity period of the patent refers to different calendar years, for example, the document is valid from June 2021 to May 2020, personal income tax is reduced in accordance with the amount of contributions made for a particular year.

Land tax, like property tax, is regional, that is, its rates are set by local governments (but within approved limits). Land tax (LT) is calculated using the following formula: The Federal Tax Service is responsible for calculating land and property taxes, after which the owner receives a notification about the need to pay the tax indicating its amount.

- 1000 rubles, if the tax has been paid;

- 5% of the tax amount for each overdue month if payment has not been made.

It is convenient to fill out the declaration through your personal account on the Federal Tax Service website - lk2.service.nalog.ru/lk/

- Group (land, air, water transport);

- Period of use;

- Tax base, which depends on engine power, capacity;

- Type of transport (car, truck, motorcycle, etc.).

What taxes are imposed on a temporary residence permit in Russia for citizens of Ukraine in 2020

Source: https://pravitzakon.ru/migratsiya/ndfl-grazhdan-ukrainy-s-rvp-2019

Taxpayer status has changed: what to do?

An employee's status may change during the year. Therefore, the final status is assigned based on the results of the reporting year. If the status has changed, the rate also changes. Therefore, the amount of income in this case must be recalculated.

For example, an employee has been working in a Russian company as a non-resident since January, and in May he became a resident. Until May, 30% was deducted from his income, and after six months of stay in the country, the rate changed to 13%. Personal income tax from January to May must be recalculated. And what was paid in excess must be returned to the foreign employee.

To do this, a foreigner needs to fill out the 3-NDFL form and, together with papers confirming his new status, go to the fiscal inspectorate.

On a note! It is the accountant's responsibility to check the taxpayer's status each time money is paid. This is especially important if the foreign employee receives money regularly.

Hiring Ukrainian citizens in 2021: step-by-step instructions

- identity card (passport) / refugee card;

- residence permit / temporary residence permit / migration card;

- VHI policy (contract);

- patent (for a temporarily staying Ukrainian);

- SNILS (if a Ukrainian gets a job in Russia for the first time, register him for pension yourself);

- work book (if a Ukrainian is getting a job in Russia for the first time, issue a work book for him yourself);

- educational documents (if necessary);

- certificate of no criminal record (if necessary).

The validity period of patents varies: not less than a month, but not more than a year. If the patent is expired, the Ukrainian cannot work until his documents are renewed. Therefore, it is very important to supervise your employee in this matter and carefully ensure that the person does not go to work with an expired patent. You don't want to fall under administrative liability, do you?

Recommended reading: 340 349 Articles

Personal income tax for foreigners from the countries of the Commonwealth of Independent States (CIS)

For citizens of some neighboring countries, there are special tax conditions that also apply to personal income tax.

Personal income tax for Ukrainians who receive payments in Russia

Russia and Ukraine signed an Agreement on the Prevention of Double Taxation. According to this document, a Ukrainian working in Russia pays income tax in the Russian Federation. But, if he worked in the Russian Federation for less than 183 days, then the tax will have to be paid in Ukraine.

A Ukrainian employee must provide a document confirming the fact of permanent residence in this country. The document must be issued by the fiscal service of Ukraine. This can be either confirmation that the employee is a Ukrainian resident, or documents on income and payment of taxes to the Ukrainian budget.

Confirmation must be provided:

- employer;

- the fiscal department in which the employing company is registered.

Income tax for citizens of Belarus

If a contract is signed between a Russian company and a native of Belarus requiring the employee to reside on Russian territory for more than 183 days, the income tax rate is 13%. This rule applies from the first day the employee begins his work duties.

But, if the employment agreement was terminated in less than 183 days, the tax amount is subject to recalculation upward - 30%. The employer in this situation is not obliged to calculate the missing tax from the income of his former employee. This responsibility rests with the Belarusian employee himself.

Income tax for citizens of the Republic of Kazakhstan

The Russian and Kazakh sides signed a convention eliminating double taxation.

The convention provides for several situations when an individual is obliged to pay tax only in the Republic of Kazakhstan:

- Remuneration for labor is not paid by an institution located on the territory of the Russian Federation.

- The employer is a non-resident of Russia.

- The recipient of the income lives in the Russian Federation for less than 183 days.

Thus, if a Kazakh citizen works and lives in Russia for less than 183 days a year or the payment is issued by a tax non-resident of Russia, he is obliged to pay taxes in Kazakhstan. But for this, the employee must provide documents confirming that he is a tax resident of the Republic of Kazakhstan.

On a note! The tax rate on the income of Kazakhstanis, including non-residents, is 13%.

Income tax rate for citizens of Armenia

It does not matter whether a citizen of Armenia is a resident or non-resident of the Russian Federation. If he is a resident of Armenia, his income received in the Russian Federation will be taxed at a rate of 13%.

Income tax rate for citizens of Kyrgyzstan

In 2015, Kyrgyzstan joined the Eurasian Economic Union. As a result, Kyrgyz people can work in Russia without having a patent.

The period of stay of an employee from Kyrgyzstan on the territory of the Russian Federation is equal to the duration of the employment contract concluded with the Russian employer. If the contract is terminated, the foreigner must leave the country within 90 days. But you can conclude a new agreement without leaving the Russian Federation. The next contract must be signed within 15 days.

On a note! Citizens of Kyrgyzstan may not confirm in the Russian Federation educational documents that were issued by authorized Kyrgyz authorities.

For citizens of Kyrgyzstan, the general taxation procedure applies. The income tax rate for Kyrgyz who work in the Russian Federation is 13%.

Taxation of foreigners with temporary residence permit 2021

Otherwise, both when hiring foreigners with temporary residence permits and temporary residence permits, and with reporting on them, taxation, and insurance contributions, persons with temporary residence permits and permanent residence permits do not differ from citizens of the Russian Federation. clause 8 art.

13 FZ-115 obliges the employer or customer of work (services), who attracts and uses a FOREIGN CITIZEN to carry out labor activities, to notify the FMS within 3 days about the conclusion and termination of a TD, which contradicts the above

They acquire a special document - a patent, which represents payment of income tax in advance. This gives them the right to get hired by individuals and companies in a certain region of Russia. In the case of a patent, personal income tax from foreigners in 2021 is paid at a rate of 13%.

How to confirm a temporary residence permit in the Russian Federation

If a migrant is required to confirm his permit annually, then he will have to think about renewing it after three years. However, Russian legislation does not provide for such a procedure. When the temporary residence permit expires, the foreigner can apply for a residence permit. It is important to do this within the last two months, while the temporary residence permit in the country is still valid.

To confirm income, you can submit one of several documents, depending on whether the foreigner works for someone or has his own enterprise. For example, after finding a job in a Russian company, a migrant can ask for a corresponding certificate at the place of work. It is drawn up on the organization’s letterhead, always indicating the amount of wages paid.

Hiring a foreigner with temporary residence permit in 2021

An employer can issue SNILS for an employee when he is employed for the first time. If a new employee does not have a Russian (or Soviet) standard labor record, then one is created in the personnel department of the organization. The employer also has the right to enter into agreements with a specific medical organization to provide paid services to foreign workers.

In fact, the main documents when employing a foreigner with a temporary residence permit are the temporary residence permit itself, a policy and a personal passport. The rest are presented at the request of the employer and within the framework of Art. 65 Labor Code of the Russian Federation. There is no need to present military registration documents.

Permit for temporary residence, issued in the form of a mark in the identity document of a foreign citizen or stateless person, or in the form of a document of the established form issued in the Russian Federation to a stateless person who does not have an identification document with a mark of residence in the territory Russian Federation for at least 183 days (document validity period is 3 years) Employment contract or certificate of employment or other document confirming the location of a person in the territory of the Russian Federation for more than 183 days (if there is no passport and visa regime between the states).

If the Russian Federation has an incorporation agreement with the state on the avoidance of double taxation and the client wishes to apply this Agreement, an additional document must be submitted confirming that the client has a permanent location in the state with which the Russian Federation has a valid Agreement.

Taxes of foreigners in the Russian Federation: on income and property - payment procedure, rules, rates

According to tax legislation, foreigners, like Russians, are required to pay tax on any income received in the Russian Federation, including from the sale of real estate, land plots, and vehicles.

Civil affiliation does not matter when selling a house or apartment; tax residency is important here, since personal income tax rates are associated with this: for residents - 13%, for non-residents - 30% of the amount for which the property was sold .

To sell real estate at lower costs, you need to become a resident of the Russian Federation, that is, live in the country legally for more than 183 days without interruptions.

After the sale of real estate or a car, the former owner is obliged to submit a declaration to the Federal Tax Service in form 3-NDFL and pay tax. This must be done before April 30 of the year following the tax period. For late submission of the declaration, penalties are imposed in the amount of:

How is personal income tax collected from foreigners in 2021?

However, it is worth considering that certain categories of migrant workers are not considered residents, but pay taxes under special conditions. This:

- highly qualified specialists;

- citizens of other countries working under a patent;

- individuals from the EAEU countries - Belarus, Armenia, Kazakhstan;

- refugees.

In accordance with the Tax Code of the Russian Federation, tax residents include people who have been on its territory for more than 183 days over the past 12 months. If a foreigner has received this status, then taxes are withheld from him in the same amounts as from Russian citizens. Thus, personal income tax from a temporarily residing foreigner in 2021 is withheld in the same way as from a non-resident.

Notification for a foreigner with a temporary residence permit sample

What documents will be needed to confirm a temporary residence permit in 2021 What is the notification procedure? As practice shows, most citizens do not fully understand migration terminology.

To avoid inaccuracies, let’s dot all the i’s.

Russian legislation provides for two procedures regarding temporary residence: obtaining it; annual notification of stay within Russia.

Who should be notified when hiring a foreigner with a temporary residence permit? When accepting a citizen with a temporary residence permit, do you need to notify the FMS about the admission, and do you need to notify the tax and pension fund? About hiring a foreigner with a temporary residence permit, you must notify the territorial body of the Main Directorate for Migration Issues of the Ministry of Internal Affairs of Russia, in whose territory the foreigner works.

A foreigner with a temporary residence permit, resident or non-resident

The main issues relate to different rates for residents and non-residents. Let us remind you that residents are citizens who have been in Russia for at least 183 calendar days over the past 12 months. Moreover, this period does not have to be in the same calendar year.

We correct mistakes of lawyers, accountants, auditors, tax inspectors, employees of the Ministry of Internal Affairs, judges and other law enforcement officers before they happen, and even after... The non-profit partnership “Republican Legal Society” has been operating since 2002. Our work is aimed at developing effective legislative regulation in Russia, increasing professionalism and competitiveness

How to hire a foreigner with a temporary residence permit

Contributions for health insurance Insurance premiums for compulsory health insurance are allocated to payments to foreigners (except for highly qualified specialists) who have the status of permanent or temporary residents in Russia. Do not charge compulsory health insurance contributions for payments to foreigners who have the status of temporarily staying in Russia. This procedure follows from the provisions of paragraph 15 of part 1 of article 9 of the Law of July 24, 2009 No. 212-FZ.

In turn, an employer hiring a temporarily resident foreigner does not need to obtain permission to hire foreign labor. At the same time, the migration service must be notified about the employment of temporarily residing foreigners. This follows from paragraph 8 of Article 13 of the Law of July 25, 2002 No. 115-FZ*.

Source: https://zakonandporyadok.ru/bankrotstvo/nalogooblozhenie-inostrantsev-s-rvp-2019

Temporary residence permit for citizens of Ukraine in 2021 personal income tax

Registration of foreign citizens with a temporary residence permit can be carried out in a legal entity, and not in a residential premises. In this case, employment must be accompanied by migration registration and registration with the enterprise. To do this, you need to fill out an application for registration as a citizen of Ukraine and prepare the following documents:

- preparation and reception of documents;

- determination of the status of a citizen of Ukraine in Russia;

- employment of an employee;

- determination of the mode of stay;

- registration;

- notification of the Main Directorate of Migration Affairs about the conclusion of an employment contract.