Who charges depreciation?

Depreciation on fixed assets belonging to them is charged to non-profit organizations (paragraph 3 of clause 17 of PBU 6/01).

Situation: can a commercial organization charge depreciation on its fixed assets in accounting?

According to the current legislation, as a general rule, commercial organizations in accounting do not charge depreciation on their fixed assets (section III of PBU 6/01). The exceptions are:

- housing facilities used for the organization’s own needs;

- external improvement objects;

- productive livestock and domesticated wild animals;

- specialized shipping facilities;

- forestry or road facilities.

For these objects, charge depreciation if the following conditions are simultaneously met:

- the fixed asset item was accepted for accounting before January 1, 2006;

- for an object, after it was accepted for accounting, depreciation was accrued in accordance with the norms of accounting legislation that were in force on the date of its acceptance for accounting.

It is explained this way. Since 2006, by order of the Ministry of Finance of Russia dated December 12, 2005 No. 147n, the condition on the accrual of depreciation by commercial organizations for a number of objects has been excluded from paragraph 17 of PBU 6/01. However, this order did not provide for the procedure for reflecting the consequences of such changes in accounting policies in accounting and reporting. Therefore, the new approach to charging depreciation instead of depreciation could only be applied to those fixed assets that were accepted for accounting after January 1, 2006. And for previously accounted for fixed assets, the previous procedure for calculating depreciation was retained.

This conclusion is confirmed by letters from the Ministry of Finance of Russia dated July 6, 2006 No. 03-06-01-04/141, dated June 7, 2006 No. 03-06-01-04/129, dated September 20, 2006 No. 03-06 -01-02/41 and the Federal Tax Service of Russia dated November 2, 2006 No. ШТ-6-21/1062. Although they clarify the issue of accounting for housing assets, the conclusions drawn in them can be extended to other fixed assets for which depreciation was accrued before 2006.

The procedure for calculating depreciation in accounting for commercial organizations in this case is similar to the current procedure for calculating depreciation for non-profit organizations.

It should be noted that depreciation accrued in accounting affects the calculation of property tax. When calculating property tax, fixed assets are accounted for at their residual value, which is determined according to accounting rules. If an organization accrues depreciation on the fixed assets it owns, then when calculating the tax base for property tax, such fixed assets must be included at their original cost minus depreciation. To determine the average annual value of property, the amount of depreciation that must be accrued for the year is distributed evenly across the months of the tax period. This procedure is established by paragraph 1 of Article 375 of the Tax Code of the Russian Federation and is explained in the letter of the Ministry of Finance of Russia dated April 18, 2005 No. 03-06-01-04/204. The procedure for calculating depreciation in accounting does not affect the calculation of other taxes.

What is OS wear and tear

Concept and essence

Having studied the role of all elements of the operating system, you can find methods for increasing the effectiveness of their use, which will ensure lower production costs and increase the growth of labor productivity (labor productivity).

Depreciation of an OS is the process of an OS losing its market value. Compensation for OS wear occurs through depreciation. Depreciation refers to the process by which the price of an asset is gradually transferred to the products produced by the enterprise in order to accumulate a certain amount necessary for the further functioning of the asset.

Depreciation of fixed assets is described in the video below:

Kinds

There are 2 types of wear and tear: physical and moral.

- Physical wear and tear is a process in which OSs lose their market value as parts wear out, under the influence of natural factors and the external environment. Physical wear and tear can be either productive or unproductive. With productive wear and tear, value is lost as a result of use. Unproductive wear and tear occurs due to the natural processes of aging. Physical coefficient depreciation is equal to the ratio of the amount of depreciation accrued over the entire service life to the original price of the fixed asset.

- Obsolescence is a process in which the value of an asset decreases as a result of a decrease in the cost of production of a similar product and due to the availability of newer equipment. Moral wear and tear does not depend in any way on physical wear and tear. Equipment physically suitable for work may be so outdated that its operation will be economically unprofitable for the organization. The following types of obsolescence are distinguished: Depreciation of fixed assets due to the production of similar ones, but with less costs and a lower price;

- As a result of scientific and technical progress, the emergence of new, higher quality and more productive equipment. Obsolescence can be equal to the ratio of the difference between the initial and replacement costs of the means of labor to the original cost of these same means.

Also, depreciation can be equal to the ratio of the product of the replacement cost of new equipment and the productivity of obsolete equipment to the productivity of modern equipment/machine. The essence of obsolescence is that tools lose their value before their service life ends.

Please note that any wear and tear implies a loss of value. Therefore, any production association needs to have additional sources of funds in case of need to restore or replace operating systems that are subject to wear and tear.

Due to frequent changes in legislation, information sometimes becomes outdated faster than we can update it on the website. Write your question using the form (below), and our specialists will quickly prepare the best options for solving your problem and call you back on the day you submit your application. It's free!

Types of activities of non-profit organizations

A non-profit organization can have several types of activities:

- statutory (non-profit), for which the organization was created and which is aimed at solving social, cultural and other socially significant problems;

- entrepreneurial (commercial), which is of an auxiliary nature and the results of which (profit) should be aimed at achieving statutory (non-commercial) goals. As part of this activity, a non-profit organization has the right to engage in production, trade, participate in the authorized capital of other organizations, as well as conduct other operations not prohibited by law.

This follows from the provisions of paragraph 2 of Article 2 and paragraph 2 of Article 24 of the Law of January 12, 1996 No. 7-FZ.

A non-profit organization must take into account income and expenses related to business activities separately (clause 3 of Article 24 of the Law of January 12, 1996 No. 7-FZ).

Accounting

Non-profit organizations can conduct accounting in a simplified way. But, if the receipt of funds and property for the previous reporting year exceeds 3,000,000 rubles, accounting should be kept in full.

This procedure is established by paragraph 1 of Article 32 of the Law of January 12, 1996 No. 7-FZ, paragraph 1 of Part 1 of Article 2 and paragraph 2 of Part 4 of Article 6 of the Law of December 6, 2011 No. 402-FZ.

See additional reporting forms for non-profit organizations

Consequently, non-profit organizations must comply with the procedure for accounting for fixed assets established by PBU 6/01.

Unlike depreciation, depreciation of fixed assets is not included in expenses. Depreciation amounts are reflected on the balance sheet in account 010 “Depreciation of fixed assets.” When accruing depreciation, the following is posted monthly:

Debit 010

– depreciation has been accrued on the fixed assets of a non-profit organization.

Such rules are established by paragraph 17 of PBU 6/01.

STRUCTURE OF FIXED ASSETS OF THE ENTERPRISE

An analysis of the structure of the enterprise's fixed assets is presented in table. 2.

| Table 2. Structure of fixed assets of the Mashstroy | ||||

| Fixed assets | Base period | Reporting period | ||

| thousand roubles. | in % of total | thousand roubles. | in % of total | |

| Building | 155 842 | 67,22 % | 150 948 | 62,57 % |

| Facilities | 548 | 0,24 % | 543 | 0,23 % |

| cars and equipment | 72 511 | 31,27 % | 85 412 | 35,40 % |

| Vehicles | 2845 | 1,23 % | 4251 | 1,76 % |

| Industrial and household equipment | 98 | 0,04 % | 99 | 0,04 % |

| Others | 10 | 0,0043% | 10 | 0,0041 % |

| Total | 231 854 | 100 % | 241 263 | 100 % |

Conclusions:

- the main share in the fixed assets of the enterprise is occupied by buildings, machinery and equipment - more than 97% of all fixed assets;

- During the reporting period, the share of machinery and equipment in the fixed assets of the enterprise increased - from 31.27 to 35.4% and the share of buildings decreased - from 67.22 to 62.57%. The share of other fixed assets remained virtually unchanged.

Calculation of depreciation amount

To calculate your monthly depreciation amount, you first need to determine your annual depreciation rate. To do this, use the formula:

| Annual wear rate | = | 1 | : | Useful life of a fixed asset, years | × | 100% |

Then calculate the annual depreciation amount. To do this, use the formula:

| Annual depreciation amount | = | Annual wear rate | × | Initial (replacement) cost of fixed assets |

Every month in accounting you need to reflect accrued depreciation in the amount of 1/12 of the annual amount.

This procedure is provided for in paragraph 19 of PBU 6/01.

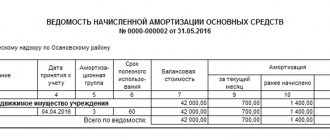

An example of reflecting depreciation on a fixed asset of a non-profit organization in accounting

The non-profit organization "Alpha" purchased a car for use in its statutory (non-commercial) activities. Its initial cost, formed in accounting, is 200,000 rubles. When commissioned, the vehicle had a useful life of 4 years.

The annual depreciation rate for a car is: (1: 4 years) × 100% = 25%.

The annual depreciation amount is: RUB 200,000. × 25% = 50,000 rub.

The monthly depreciation amount is: RUB 50,000. : 12 months = 4167 rub.

Starting from the month following the commissioning of the vehicle, the Alpha accountant reflects the accrual of depreciation on a monthly basis by posting:

Debit 010 – 4167 rub. – depreciation has been accrued for the vehicle for the current month.

BASIC

In tax accounting, non-profit organizations must reflect only those income and expenses that are associated with their entrepreneurial (commercial) activities. Targeted revenues and expenses associated with non-commercial (statutory) activities are not taken into account when calculating income tax. This follows from the provisions of subparagraph 14 of paragraph 1, paragraph 2 of Article 251 and paragraph 1 of Article 252 of the Tax Code of the Russian Federation.

Fixed assets used in commercial (entrepreneurial) activities and acquired from income from this activity can be depreciated in tax accounting (subclause 2, clause 2, article 256 of the Tax Code of the Russian Federation). Depreciation accrued on these fixed assets is included in expenses and reduces the tax base for income tax (clause 1 of Article 252 of the Tax Code of the Russian Federation). Since depreciation is accrued in accounting for these fixed assets, a constant difference will appear, with which organizations applying PBU 18/02 must calculate a permanent tax asset (clauses 4, 7 PBU 18/02). Reflect its appearance with wiring:

Debit 68 subaccount “Calculations for income tax” Credit 99

– a permanent tax asset is reflected from the difference between the amounts of depreciation and amortization reflected in accounting and tax accounting.

However, non-profit organizations have the right not to use PBU 18/02, which must be enshrined in the accounting policy for accounting purposes (clause 2 of PBU 18/02). Therefore, if an organization does not apply PBU 18/02, there is no need to reflect permanent and temporary differences in accounting.

An example of reflection in accounting and taxation of depreciation and amortization for fixed assets of a non-profit organization. According to the accounting policy for accounting purposes, the organization applies PBU 18/02

Using income from business activities, the non-profit organization "Alpha" purchased sewing equipment, which is used exclusively in business activities. The initial cost of equipment in accounting and tax accounting is 175,000 rubles. The useful life established according to the Classification approved by Decree of the Government of the Russian Federation dated January 1, 2002 No. 1 is 4 years (48 months). According to the accounting policy, for tax purposes, depreciation on fixed assets used in business activities is calculated using the straight-line method.

The monthly amount of depreciation of sewing equipment in tax accounting is equal to the monthly amount of depreciation in accounting and amounts to: 175,000 rubles. : 48 months = 3646 rub./month.

Starting from the month following the commissioning of the sewing equipment, the accountant monthly includes the amount of accrued depreciation in expenses when calculating income tax. At the same time, he makes the following entries in accounting:

Debit 010 – 3646 rub. – depreciation has been accrued for sewing equipment for the current month;

Debit 68 subaccount “Calculations for income tax” Credit 99 – 729 rub. (RUB 3,646 × 20%) – a permanent tax asset is reflected from the difference between the amounts of depreciation and depreciation for sewing equipment.

Fixed assets that are purchased using targeted proceeds (targeted financing funds) are not depreciated. It does not matter whether they are used in statutory (non-commercial) activities or not. Depreciation accrued for these objects in accounting does not affect the calculation of income tax. This procedure follows from subparagraphs 2 and 7 of paragraph 2 of Article 256 of the Tax Code of the Russian Federation. It is confirmed by the Federal Tax Service of Russia in a letter dated December 8, 2009 No. 3-2-13/236.

If a fixed asset was acquired at the expense of targeted proceeds (targeted financing funds), but is intended for use in business activities, its cost must be included in non-operating income subject to income tax (subclause 14, clause 1, clause 2, article 251 , paragraph 14 of Article 250 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated December 8, 2009 No. 3-2-13/236).

Such property is recognized as received free of charge, therefore the amount of income must be determined as the market value of the object, taking into account the restrictions provided for in paragraph 8 of Article 250 of the Tax Code of the Russian Federation. The amount of recognized income cannot be lower than the residual value of the fixed asset. But since depreciation was not accrued for such an object, non-operating income must include:

- the initial cost of the fixed asset (if it is higher than the market value);

- market value of the fixed asset (if it is higher than the original).

Downtime of technological installations during repairs ranges from 10 to 15% of calendar time, which significantly reduces their production capacity.

The inevitable physical wear and tear of fixed assets can be slowed down and their performance maintained through organized repairs. [p.111] One of the forms of simple reproduction of fixed assets is major repairs, with the help of which the physical wear and tear of fixed assets is partially compensated. Financing of capital repairs is carried out on the basis of a capital repair plan with costs allocated to the cost of production. However, the choice of the method of attributing costs to the cost of production is within the full competence of the organization (enterprise) and is fixed in its accounting policy. [p.298] A high degree of depreciation of fixed assets may be caused by the impossibility of their timely renewal due to a lack of financial resources. A high degree of wear and tear does not always reflect the real physical wear and tear of fixed assets, but is a warning about the possible occurrence of difficulties with insufficient attention to investment policy. In some cases, a high depreciation rate of fixed assets may be a consequence of high depreciation rates used by the organization. [p.98]

Depreciation for accounting purposes is defined as a decrease in the useful value of fixed assets as a result of physical wear and tear. Fixed assets may also decline in useful value through obsolescence as new inventions and more advanced equipment become available that render existing equipment obsolete. Costs incurred in connection with the acquisition of property, plant and equipment should be allocated over the entire expected use of the equipment, taking into account the above factors. [p.233]

Physical wear and tear of fixed assets (funds) occurs from their use in the production process (from friction, pressure, etc.), as a result of which fixed assets lose not only their own, but also their consumer value, and from their non-use, as a result of which they lose their consumer value cost due to the influence of natural forces. [p.88]

Physical depreciation of fixed assets due to their occurrence can be divided into two groups: a) depreciation of fixed assets due to their use b) depreciation of fixed assets due to their non-use. [p.30]

In addition to physical wear and tear, fixed assets and, first of all, production equipment wear out morally, that is, they become obsolete before their complete physical wear and tear occurs. The enterprise must constantly take care of the timely replacement or modernization of equipment and the introduction of new technical means. [p.39]

PHYSICAL WEAR OF FIXED ASSETS - material wear and tear of fixed assets. As a result of wear, the productivity and reliability of machines and their performance decrease. [p.362]

The amount of physical depreciation of fixed assets depends primarily on the duration and intensity of their use. To measure the degree of physical deterioration of fixed assets, an expert assessment of technical [p.283]

PHYSICAL WEAR OF FIXED ASSETS - see PHYSICAL WEAR OF FIXED ASSETS [p.250]

PHYSICAL WEAR OF FIXED ASSETS - material [p.795]

PHYSICAL WEAR OF FIXED ASSETS - material wear and tear of fixed assets, loss of their physical properties, qualities, sizes, performance. [p.419]

But the decline in production potential is caused not only by the physical wear and tear of fixed assets. Another significant factor is obsolescence, caused by technological progress and changes in the need for asset services. Taking into account a significant number of factors reducing the production potential of an asset, it seems very difficult to determine the magnitude of this decrease for the reporting period and give it an accounting estimate. Some believe that the services of an asset should be valued based on its cost, others - at current prices. Some argue that depreciation should be measured at the cost of replacing the services received from the asset, while others present the cost of maintaining the asset in its original operating condition as the best estimate of depreciation. There is an opinion that the most acceptable method of calculating depreciation is the interest method. But none of these solutions to depreciation problems are perfect. Therefore, for financial reporting purposes, the simplest approach, the straight-line depreciation method, is most preferable. [p.348]

Physical wear and tear of fixed assets is the loss of consumer value of fixed assets due to their intensive use, as well as inaction and the impact of natural forces on them, due to which fixed assets are destroyed and become unsuitable for further use. [p.241]

And - nominal investments (capital investments) in non-current assets (in this case, investments can be negative if, for example, in some period there was a massive sale of non-current assets); the term nominal means the fact that part of these investments is eaten up by the physical wear and tear of fixed assets, ( in the case of taking into account only net real investments directed to non-current assets, the depreciation component A should be removed from the above formula [p.73]

Physical wear and tear of fixed assets is the gradual loss of their original use value as they participate in the production process, as a result of which they become unusable and require replacement with new means of labor. [p.158]

When establishing the service life, it is necessary to take into account not only physical, but also obsolescence of fixed assets. [p.100]

In addition to physical depreciation of fixed assets, there is obsolescence. There are two types of it. The first of them assumes that due to an increase in labor productivity, the cost of produced means of labor decreases over time. As a result, existing equipment loses value as similar machines begin to be reproduced more cheaply. Loss of the value of fixed assets as a result of obsolescence of the first kind is calculated as the difference between the original and replacement cost of fixed assets in rubles, and the degree of obsolescence of the first kind is determined by the ratio of this difference to the original cost. [p.34]

For a long time, when solving important national economic problems - the formation of new industries, the development of the outlying regions of the country, the creation of large territorial production complexes - the main share of capital investments was occupied by the construction of new and expansion of existing enterprises. This met the objectives of the corresponding stages of economic development, but gradually began to lead to the allocation of insufficient funds to existing enterprises, which predetermined the moral and physical wear and tear of their means of labor, production technologies and non- [p.20]

Fixed assets wear out over time during the production process and lose their original performance qualities. The economic essence of the phenomenon of wear and tear of fixed production assets lies in the fact that during the production process they gradually transfer their value to the newly created product. A distinction is made between physical and obsolete depreciation of fixed assets. Physical wear and tear occurs both during their operation and under the influence of natural and climatic conditions. The degree of physical wear and tear of fixed assets depends on the design and material from which they are made, the intensity of use, the quality of service and maintenance. After a certain time, fixed assets wear out so much that they become unusable. The essence of obsolescence is that the means of labor lose their value due to cheaper machines and equipment of the same design or the emergence of new, more advanced and productive machines and equipment. Obsolescence means that existing fixed production assets become economically ineffective. The active part of fixed production assets is more susceptible to obsolescence. [p.276]

These indicators are measured as a percentage or as a fraction of a unit and can be calculated both at the beginning and at the end of the reporting period. Obviously, an increase in the depreciation rate means a deterioration in the condition of the organization's fixed assets. However, the depreciation coefficient does not reflect the actual depreciation of fixed assets, and the serviceability coefficient does not provide an accurate assessment of their current value, for example, when mothballing equipment, since physically in this case the fixed assets do not wear out, but the total amount of their depreciation increases. As for the current valuation of fixed assets, it depends on a number of factors, in particular, on the state of the market and demand, and therefore may differ from the assessment obtained using the suitability coefficient. The amount of depreciation of fixed assets is greatly influenced by the depreciation system adopted in the organization. With the current accounting and reporting system, depreciation and serviceability coefficients provide only a conditional assessment of the condition of fixed assets in their total mass, which significantly limits the possibility of their use for analysis. In order to expand the available reporting capabilities, depreciation should be highlighted in separate lines for the active and passive parts of fixed assets, and even better, by classification groups. [p.260]

There are physical and moral wear and tear of fixed assets, complete and partial. [p.341]

Calculate the coefficients characterizing the physical condition of the enterprise's fixed assets; serviceability coefficient; wear and tear coefficient; renewal coefficient; retirement coefficient. [p.157]

Firstly, the depreciation coefficient, strictly speaking, does not reflect the actual depreciation of fixed assets, just as the serviceability coefficient does not give the exact current value of their assessment. This happens for a number of reasons. In particular, depreciation is charged on mothballed equipment and vehicles for full restoration, i.e., these assets do not physically wear out, but the overall assessment of the depreciation of fixed assets changes. [p.288]

The economic depreciation of fixed assets, calculated according to depreciation standards, does not correspond to their physical and moral wear and tear. Therefore, the given wear percentages only relatively characterize the degree of wear. [p.305]

Such an element of the compensation fund as depreciation charges also deserves special attention. Depreciation is calculated according to the physical and moral wear and tear of fixed assets. Worn-out fixed assets require either replacement or partial restoration through repair, reconstruction or modernization. Depreciation serves the purpose of accumulating the financial resources necessary for this. [p.46]

Physical wear and tear of fixed assets is the loss of their original consumer value, as a result of which they gradually become unusable and require replacement with new means of labor of the same kind. Thus, buildings and structures are subject to gradual aging, machinery and equipment are subject to material wear and tear as a result of working on them, metal corrosion, etc. [p.12]

Physical wear and tear of fixed capital means that the means of Labor lose their usefulness, as a result of which they become materially unsuitable for further use. This wear occurs in two cases: a) in the process of productive use (breakdown of machines, destruction of a factory building from vibrations, etc.) and [p.238]

WEAR OF FIXED ASSETS - a decrease in the value of fixed assets according to established standards during their operation. Norms I.o.s. are established by law. The residual value of fixed assets is determined as the difference between their original cost and the amount of accrued depreciation. There are two types of depreciation of fixed assets: moral and physical. [p.86]

WEAR, aging, wear and tear of things, objects, loss of the original qualities and properties that they possessed. Due to wear and tear, means of production lose their efficiency, value, and usefulness; funds have to be spent on their restoration and repair. Depreciation of fixed assets is the aging and wear and tear of buildings and equipment during their production use. A distinction is made between physical wear and tear, characterized by a gradual loss of original qualities, destruction of structures, and obsolescence, associated with the consistent lag of previously created fixed assets of production from the modern technical level (obsolescence). See also Depreciation. [p.90]

The turnover of fixed capital includes three main phases: depreciation, depreciation, and compensation in kind. Physical depreciation of fixed capital consists of wear and tear of the means of labor. Obsolescence is associated with the reduction in cost of means of labor over time or with the creation of new, more productive machines. [p.118]

On the one hand, the amount of depreciation deductions is the monetary expression of the loss of objects (fixed production assets) of their physical technical and economic qualities and reflects the value of their wear and tear. The accrued amount of depreciation of fixed assets, accumulating, is the source necessary for the restoration of completely worn-out objects. [p.363]

PHYSICAL WEAR OF FIXED ASSETS - operational or natural wear and tear of fixed assets. Operational wear and tear is the result of industrial consumption during the operation of fixed assets. Natural [p.503]

Participating in the production process for a long time, fixed assets physically wear out, i.e., they lose their original qualities, which is called physical wear. The intensity of wear depends on operating conditions (temperature, pressure, reaction speed, etc.), the design of equipment, equipment and machines, the materials from which they are made, corrosion protection products, etc. Complete physical wear and tear of fixed assets means the need to replace them , partial - carrying out repairs, during which the original properties of fixed assets are partially or completely restored. [p.175]

The example shows that fixed assets continue to be used after they have been fully depreciated. Consequently, while continuing to accrue depreciation, the chief accountant, crediting the Depreciation of fixed assets account, in our example by 2000 rubles, reduced the Fixed Assets account by the same amount, turning it into a passive one. However, according to tradition, it is impossible to place the Fixed Assets account in the liability side, so its contractual account Depreciation of Fixed Assets is placed in the liability side. But since the depreciation turned out to be greater than the cost of fixed assets, the amount of funds invested by the owner should automatically be reduced, i.e. Authorized (or Additional) fund. So, on the one hand, the Fixed Assets account belongs to the group of material accounts (1.1.1.1.1), and on the other hand, if the nominal regulatory contract is removed from accounting (group - 1.2.2.2.1), the Fixed Assets account becomes resultant (group - 1.2.1.2.1). Further, from a traditional point of view, the account Depreciation of fixed assets, being a counter-contractual account, should regulate the initial valuation of fixed assets. However, this is not entirely true, because the account does not show the amount of physical and moral wear and tear, but the amount of accrued depreciation, and, therefore, it does not act as a contractual to the Fixed Assets account, but as an additional to the Authorized Fund account, being the carrier of an independent depreciation fund. In addition, the example shows the absurdity of the statements that the residual value can be defined as the difference between the balance of the Fixed Assets and Depreciation of Fixed Assets accounts, because depreciation is, of course, a financial and not a material process. It is almost impossible to accurately calculate the acceptable service life of an object, since it is impossible to foresee in advance the expected service life, operating conditions and, most importantly, the circumstances associated with scientific and technological progress, which determines the obsolescence of fixed assets. [p.311]

In the process of operation, fixed capital is subject to physical and moral wear and tear. Physical wear and tear is the process as a result of which elements of fixed capital become physically unsuitable for further use in production. The physical wear and tear of fixed capital is determined by many factors. First of all, this is the duration and intensity of use of machinery and equipment, the features of production technologies where fixed capital is used, the impact of atmospheric conditions, internal processes occurring in the material from which the means of labor are made. There is a directly proportional relationship between the degree of physical wear and the duration of use of fixed capital; the longer the operating time of machinery and equipment, the greater the degree of physical wear. [p.152]

Property tax

Non-profit organizations that apply the general tax system are recognized as payers of property tax (Clause 1, Article 373 of the Tax Code of the Russian Federation). When calculating property taxes, consider:

- objects of movable property registered before January 1, 2013 and reflected in the balance sheet in accounts 01 “Fixed Assets” and 03 “Profitable Investments in Material Assets”;

- real estate objects reflected in the balance sheet in accounts 01 “Fixed Assets” and 03 “Profitable Investments in Material Assets”.

When calculating this tax, fixed assets are taken into account at their residual value, determined according to accounting rules. Since fixed assets of non-profit organizations are not depreciated in accounting, they must be included in the calculation of the tax base at their original cost minus depreciation. To determine the average annual value of property, the amount of depreciation that must be accrued for the year is distributed evenly over the months of the tax period. This procedure is established by paragraph 1 of Article 375 of the Tax Code of the Russian Federation and is explained in the letter of the Ministry of Finance of Russia dated April 18, 2005 No. 03-06-01-04/204.

Some non-profit organizations are eligible for property tax relief. The list of benefits and conditions for their application are given in the table.

Calculation of physical depreciation of fixed assets

This type of wear and tear manifests itself as a result of changes in various properties of fixed assets, which appear due to their use in the labor process, as well as the impact of natural and other factors on them. In an economic sense, physical wear and tear is a decrease in the original consumer value of fixed assets. It becomes the result of wear and tear, dilapidation and obsolescence. This type of wear can be determined in two ways:

1. Based on the volume of work: a comparison of the actual volume of work performed with the standard is used. This calculation method can only be used in cases where the fixed asset has a certain productivity . In other words, it can be applied to objects such as machines and machine tools. In this case, wear is calculated using the formula:

And = (Tfact x Pfact) / (Tnorm x Pnorm), where

- Tfact – time actually worked by the equipment (measured in years);

- Pfact – the average volume of products produced annually (in physical terms);

- Tnorm – standard service life of a fixed asset (in years);

- Pnorm – production capacity or productivity according to standards (in natural units).

2. According to service life. Determined by comparing the actual and standard operating time. This method is applicable to any fixed asset.

simplified tax system

Subject to the restrictions established by Article 346.12 of the Tax Code of the Russian Federation, non-profit organizations have the right to apply a simplified tax regime. Unlike other organizations, non-profit organizations can apply a simplified tax system even if the share of participation of other organizations in it exceeds 25 percent (subclause 14, clause 3, article 346.12 of the Tax Code of the Russian Federation).

If a non-profit organization conducts business activities, then it is obliged to keep separate records of income and expenses for statutory and business activities (clause 1 of article 346.15, clause 2 of article 251 of the Tax Code of the Russian Federation).

Targeted revenues and expenses paid from these revenues do not affect the calculation of the single tax during simplification. When calculating the single tax, take into account only those incomes and expenses that are associated with business activities. This follows from the provisions of paragraph 1.1 of Article 346.15, paragraph 2 of Article 251, paragraph 2 of Article 346.16, paragraph 1 of Article 252 of the Tax Code of the Russian Federation. Moreover, if an organization pays a single tax on income, then when calculating the tax base it does not have the right to take into account any expenses (clause 1 of Article 346.18 of the Tax Code of the Russian Federation).

If an organization pays a single tax on the difference between income and expenses, then the cost of acquired (created) fixed assets reduces the tax base in the manner prescribed by paragraph 3 of Article 346.16 of the Tax Code of the Russian Federation. For more information about this, see How to take into account the receipt of fixed assets and intangible assets during simplification. This procedure can only be applied to paid (partially paid) fixed assets, which are recognized as depreciable property for calculating income tax (clause 4 of Article 346.16 of the Tax Code of the Russian Federation). This means that the organization does not have the right to write off as expenses fixed assets acquired from targeted revenues (targeted financing funds). It does not matter whether they are used in statutory (non-commercial) activities or not. This procedure follows from subparagraphs 2, 7 of paragraph 2 of Article 256 and subparagraph 4 of paragraph 2 of Article 346.17 of the Tax Code of the Russian Federation. It is confirmed by the Federal Tax Service of Russia in a letter dated December 8, 2009 No. 3-2-13/236. Despite the fact that the letter concerns organizations using the general tax system, the conclusions drawn in it can also be extended to organizations using the simplified tax system (clause 4 of Article 346.16 of the Tax Code of the Russian Federation).

Thus, expenses for the acquisition of fixed assets will reduce the tax base while simultaneously meeting two conditions:

- fixed assets have been paid (in whole or in part);

- fixed assets were acquired from income from business activities and are used exclusively in this activity.

If the costs of purchasing depreciable property are partially paid, they can be taken into account in reducing the tax base in the payment amount. There is no need to wait for the full repayment of the cost of fixed assets (subclause 4, clause 2, article 346.17 of the Tax Code of the Russian Federation).

If a fixed asset was acquired using income from business activities, but is used in statutory (non-commercial) activities, its cost is not taken into account when calculating the single tax. This follows from the provisions of subparagraph 4 of paragraph 2 of Article 346.17 of the Tax Code of the Russian Federation.

If the organization uses a fixed asset acquired at the expense of targeted revenues in business activities, then in fact there is an inappropriate use of the received property (clause 1 of article 346.15, subclause 14 of clause 1, clause 2 of article 251, clause 14 of art. 250 Tax Code of the Russian Federation). This is confirmed by the letter of the Federal Tax Service of Russia dated December 8, 2009 No. 3-2-13/236. Although it concerns organizations on the general taxation system, the conclusions drawn in it can be extended to organizations on the simplified tax system.

In this case, the organization must recognize non-operating income in the amount of the market value of this fixed asset (clause 1 of Article 346.15, clause 8 of Article 250 of the Tax Code of the Russian Federation). Despite the fact that such property is depreciable (clause 1 of Article 256 of the Tax Code of the Russian Federation), its value cannot be written off as expenses. The object is considered to have been received free of charge, therefore, the organization did not have expenses for its creation or acquisition, which could be taken into account when calculating the single tax (clause 3 of Article 346.16 of the Tax Code of the Russian Federation).

Organizations using the simplified system are required to keep accounting records in full, including fixed assets (Part 1, Article 2 of Law No. 402-FZ of December 6, 2011). However, depreciation accrued on fixed assets of non-profit organizations in accounting is not taken into account when calculating the single tax.

Accrued depreciation does not affect the calculation of property taxes. Non-profit organizations using the simplified tax regime do not pay this tax either on fixed assets used in statutory activities, or on fixed assets used in business activities (clause 2 of Article 346.11 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated March 30, 2007 No. 03 -05-06-04/18).