What is taxpayer status in 2nd personal income tax?

Each legal entity is a tax agent and undertakes the obligation to pay taxes both on its activities and its financial results, and on the wages of all its employees. In fact, every company (including individual entrepreneurs) is an intermediary for paying taxes for its employees.

The key to taxation of income received is the correct determination of the tax rate (percentage of income). It is precisely in order to correctly determine this rate that there is such a thing as taxpayer status.

Each taxpayer may have its own characteristics that affect its status. They may concern parameters such as:

- country of residence/citizenship;

- occupation;

- features of living in Russia, etc.

The company prepares a special certificate for each of its employees (individuals) and submits it to the tax authority after the past calendar year. It is in this certificate that the taxpayer status is stated.

The tax authorities, in turn, check the specified status for each individual and make a decision whether the tax rate was determined correctly.

Main types (1, 2, 3, 4, 5, 6)

Certificate 2-NDFL was previously approved by the Order of the Federal Tax Service on October 30, 2015 and it contained only three statuses.

Today, it contains six meanings for a more precise formulation and decoding of the taxpayer’s status.

The status table for today is as follows:

| Taxpayer status in 2 personal income tax “1” | Resident of the Russian Federation |

| Status "2" | Not a resident of the Russian Federation |

| Status "3" | Highly qualified specialist or skill, but not a resident of the Russian Federation |

| Status "4" | Citizens of the Russian Federation who often travel abroad, but return home, while the tax system does not consider them as residents of the country, applying a different system of tax deductions to them |

| Status "5" | Refugees, not residents of the Russian Federation |

| Status "6" | Applicable to foreign persons who, according to the patent, have permission to work in the country |

The improved status system is very easy to use in the work of the tax service, since it provides a more open decoding and formulation of data and information about a citizen, both domestic and foreign.

Dividends in the certificate in 2021

Code “2” is entered if the Certificate is filled out in relation to an individual who is not a tax resident of the Russian Federation as of December 31 of the reporting year.

If the taxpayer is not a tax resident of Russia, then status codes 2 - 5 are entered in this field. Specifically, in section.

This status is assigned to those who are recognized by Chapter 23 of the Tax Code of the Russian Federation as non-residents, but at the same time are recognized as personal income tax payers if they derive income from Russian sources.

Code “2” is entered if the Certificate is filled out in relation to an individual who is not a tax resident of the Russian Federation as of December 31 of the reporting year.

If in the reporting year the tax agent paid income to a foreign citizen (stateless person) recognized as a refugee or who received temporary asylum in Russia and who is not a tax resident of the Russian Federation, then status “5” must be indicated in 2-NDFL.

Even if the taxpayer status is incorrectly indicated, the funds will be sent to the status of undetermined and will simply hang until the relationship is clarified.

When submitting a certificate, the legal successor of the tax agent indicates OKTMO at the location of the reorganized organization.

When filling out a certificate with attribute “2” or “4”, the section indicates income and deductions only for those periods for which tax was not withheld by the tax agent.

Value in payment

The total values, in accordance with regulatory documentation, are 28. The main ones are:

- 01 - the organization transfers mandatory fees;

- 02 - companies and individual entrepreneurs pay as agents;

- 08 - contributions for injuries;

- 09 — individual entrepreneur performs duties to the supervisory authority;

- 10 - engaged in private practice;

- 11 - lawyers;

- 12 - heads of peasant farms;

- 13 - individual.

Point 14 is currently excluded.

Where can I get the data to accurately fill out the payment order in field 101? All values are indicated in Appendix No. 5 to Order of the Ministry of the Russian Federation dated November 12, 2013 No. 107n. The last changes to it were made on 04/05/2017, some of which came into force on 10/02/2017. This document should be used as a guide when filling out the payment order form. Below are examples of the most common values in practice.

What are the statuses and codes?

Starting from 2021, there are six taxpayer statuses, each of which is assigned a code.

Table 1. Codes assigned depending on taxpayer status

| Code | Status |

| Code 1 | Placed if the individual is a resident of the country. |

| Code 2 | The individual is not a resident. |

| Code 3 | A highly qualified specialist, he is also not a resident. |

| Code 4 | Participant in the state program for the return of compatriots to their homeland. Non-resident of Russia. |

| Code 5 | Non-resident refugee. |

| Code 6 | A citizen of another country working in the Russian Federation on the basis of a patent. |

On a note! The employee’s status code determines what percentage will be deducted from his income.

To determine which code should be in 2-NDFL and at what rate to calculate taxes, follow this algorithm:

- Check if the foreign employee has a special status.

- Find out whether he is a resident or not.

- Find out exactly what income needs to be paid to the foreigner.

Resident

The vast majority of Russian workers fall into this category. Therefore, in section 2.3 of the 2-NDFL declaration, accountants most often put code No. 1.

Tax resident is an individual who has lived in the state for at least one hundred and eighty-three days during the previous twelve consecutive months. These 183 days also include arrival and departure dates.

Who is a Tax Resident of the Russian Federation? Our article will help you figure this out. In it we will look at what the tax status depends on, documents for confirmation, as well as the regulatory framework for residents and non-residents.

If an individual did not live in Russia, but received treatment or education abroad, the period of his absence will not be counted towards 183 days.

For residents, the income tax rate is 13%

Non-resident

If a foreign employee stays in the country for less than 183 days, he is considered a non-resident. The status of “non-resident of the Russian Federation” has several features:

- A non-resident is required to pay tax and submit a declaration to the fiscal authority only if he received income from a source located on Russian territory.

- A non-resident cannot receive a tax deduction.

- If, as a result of a change in status from non-resident to resident, tax was overpaid, the money can only be returned to the tax office (not through the employer) at the end of the calendar year.

Resident or non-resident status does not depend on citizenship. A resident can be not only a citizen of Russia, but also a citizen of another state or a stateless person. A non-resident can be:

- Russian citizen living abroad;

- a foreigner who arrived less than six months ago.

Refugee

Since October 2014, all income paid to refugees and those who have received temporary housing in the Russian Federation is subject to a reduced income tax rate of 13%.

Code 5 in the “Taxpayer Status” section is entered only if the employee is a non-resident of the country. For non-residents, only income received as a result of work is subject to a thirteen percent tax. All other payments (gifts, financial assistance) are subject to taxation at the same percentage for all non-residents - 30%.

On a note! A refugee cannot count on standard group deductions before he receives Russian tax resident status.

To receive a deduction for children, a refugee must legalize documents (birth or adoption certificate) in the territory of our state. This can be done at the consular offices of the republic that issued the document.

If the country in which the certificate was received is a party to the Hague Convention, it is enough to certify the document with an apostille

Participants in the program for the return of compatriots

Code 4 in the “Taxpayer Status” section is applied if the employee is a participant in the program for the return of compatriots from the CIS countries to their homeland, Russia. Various social benefits are provided for this category of foreigners and their families, including a reduced percentage of income tax.

Rules for calculating personal income tax for immigrants:

- Wages, payments for services, bonuses and other earnings received as a result of work activities are taxed at 13%. The percentage should not be higher, even if the employee is a non-resident of the country. The benefit can be applied only after the foreigner presents a document proving the fact of participation in this state program. When hiring an accountant, you need to keep a copy of the document and regularly check its validity period. The certificate is issued to the migrant for three years.

- The rate applied to other unearned income depends on whether the immigrant becomes a resident. If yes, the percentage is 13%; if not - 30%. The category of unearned earnings includes gifts, financial assistance, and income from rental property.

- Standard group deductions can only be applied if the migrant has already become a resident.

On a note! A program participant has the right to find employment in the Russian Federation without a work permit.

Highly qualified foreign specialists

A highly qualified specialist is a foreigner who has outstanding skills, knowledge, and experience in some field of activity. Such an employee must have signed an employment contract with a company from Russia. Payment for the work of a valuable foreign employee must be at least two million rubles per year. But for teachers and researchers, the minimum wage may be less - from one million rubles.

On a note! The income of a highly qualified foreign specialist is taxed at 13%, even if he is a non-resident of the Russian Federation.

The employer must assess the level of competence and qualifications. Evidence of a high level of knowledge and experience can include:

- diploma;

- education certificates;

- comments from previous employers about the employee;

- awards;

- information from specialized organizations.

The status of a highly qualified specialist is awarded to a foreign employee from the moment a work permit is issued. The document must contain a corresponding note.

The thirteen percent rate for this category of workers can be used even if the employment contract is concluded for a short period. If the contract is drawn up for a period of less than 1 year, the amount of remuneration for the period of work must be at least two million rubles.

The reduced rate applies only to those incomes of a valuable specialist that relate to labor payments. For example, salary, production bonuses, payment for services. All income that goes beyond the scope of the employment relationship is taxed at 30%, even if the money is transferred by the same employer

On a note! If a specialist has left the country and payments must be made outside the Russian Federation, then a 13% rate is still applied to the income. For the last payments after the dismissal of a foreign employee, the tax amount also remains unchanged.

Foreigners working under a patent

If a foreign employee is a citizen of a visa-free country, he must apply for a patent. This document gives the right to work on the territory of the Russian Federation. A labor patent is necessary both for hired work and for individual entrepreneurial activity or opening a company.

Citizens of Kazakhstan, Kyrgyzstan, Armenia and Belarus do not need to obtain a patent. These countries are not only visa-free, but also part of a single customs union with Russia. According to international agreement, patents and work permits are not required for natives of these four states.

Citizens of other visa-free countries - Uzbekistan, Ukraine, Abkhazia, Azerbaijan - need to obtain a patent.

The patent indicates the territory in which the foreigner has the right to work. So, if the document was issued in the Moscow region, a foreigner cannot work in Moscow. And, conversely, a patent issued in Moscow does not give the right to work outside its borders.

On a note! The employer must prevent double taxation, since there is a possibility of calculating personal income tax twice - when the employer accrues income and when paying advance payments for the patent. The employer is obliged to help the foreign employee reduce tax. To do this, it is enough to reflect this information in the 2-NDFL certificate.

It is also possible to receive a refund of overpaid income tax by a foreigner. The employer can also help the employee with this. The amount that is planned to be returned should not exceed the amount of the advance payment for the month. Also, the amount to be refunded depends on the employee’s income.

On a note! Since the sizes of monthly advance payments are different in all regions, the amounts to be returned will also be different.

What category do foreign citizens fall into?

For foreign citizens, the rules for determining status are equivalent to the general ones. In other words, depending on who exactly a foreigner is recognized as for work and the procedure for paying taxes.

You can also define a status for it from one to six. Most often, foreigners working in the Russian Federation receive a pass for a patent.

As a rule, they have no visas. A work patent is needed to work in the country for employment, for entrepreneurship, to open your own business, etc.

Highly qualified foreign specialists

A highly qualified specialist is a foreigner who has outstanding skills, knowledge, and experience in some field of activity.

Such an employee must have signed an employment contract with a company from Russia. Payment for the work of a valuable foreign employee must be at least two million rubles per year. But for teachers and researchers, the minimum wage may be less - from one million rubles. On a note! The income of a highly qualified foreign specialist is taxed at 13%, even if he is a non-resident of the Russian Federation.

The employer must assess the level of competence and qualifications. Evidence of a high level of knowledge and experience can include:

- diploma;

- education certificates;

- comments from previous employers about the employee;

- awards;

- information from specialized organizations.

The status of a highly qualified specialist is awarded to a foreign employee from the moment a work permit is issued. The document must contain a corresponding note.

The thirteen percent rate for this category of workers can be used even if the employment contract is concluded for a short period. If the contract is drawn up for a period of less than 1 year, the amount of remuneration for the period of work must be at least two million rubles.

The reduced rate applies only to those incomes of a valuable specialist that relate to labor payments. For example, salary, production bonuses, payment for services.

All income that goes beyond the scope of the employment relationship is taxed at 30%, even if the money is transferred by the same employer

On a note! If a specialist has left the country and payments must be made outside the Russian Federation, then a 13% rate is still applied to the income. For the last payments after the dismissal of a foreign employee, the tax amount also remains unchanged.

Is the fact of the employee's residence at the end of the year important for the tax rate?

Agree, this is a strange question, because having just analyzed the norms of the Tax Code of the Russian Federation and the Treaty, we came to the conclusion that for the purpose of calculating personal income tax, the status of a tax resident of the Russian Federation does not matter for such employees. It was not there, the Ministry of Finance of Russia in May 2021 issued a Letter in which it explains that based on the results of the tax period, the company’s accountant must determine the final tax status of an individual depending on the time of his stay in the Russian Federation in a given tax period.

An employee from an EAEU country: is it necessary to track his tax status?

In 2021, citizens of Kyrgyzstan worked in the organization. Personal income tax was withheld from their salaries at a rate of 13% from the first day of work. What status should be indicated in the 2-NDFL certificates regarding the income of such persons?

Before moving on to the nuances of filling out form 2-NDFL, let us recall that Article 73 of the Treaty on the Eurasian Economic Union of May 29, 2014 allows employers to withhold personal income tax in the amount of 13% from the first day of work for citizens of Kyrgyzstan (letter of the Federal Tax Service of Russia dated August 27, 2015 No. ZN -4-11/15078). Exactly the same taxation regime applies to income from employment received by citizens of other EAEU member countries: Belarus, Kazakhstan and Armenia.

But at the same time, these citizens are not automatically recognized as tax residents of the Russian Federation. Their tax status is determined in accordance with the general procedure provided for in paragraph 2 of Article 207 of the Tax Code of the Russian Federation. That is, it depends on the number of calendar days spent on the territory of the Russian Federation over the previous 12 months (letters of the Ministry of Finance of Russia dated January 22, 2019 No. 03-04-06/3032 and dated May 23, 2018 No. 03-04-05/34859; see “Rate Personal income tax for citizens from the EAEU depends on their tax status at the end of the year." Therefore, if during the period from January 1 to December 31, 2021, a citizen of Kyrgyzstan spent less than 183 calendar days in the Russian Federation (excluding short-term, that is, lasting no more than 6 months, trips for treatment or training), then he is not a tax resident of the Russian Federation.

In accordance with clause 3.5 of the Procedure for filling out the new form 2-NDFL, the taxpayer status code is indicated in the “Taxpayer Status” field in Section 1 of the certificate. In this case, a tax resident of the Russian Federation (except for persons working on the basis of a patent) corresponds to code 1, and a tax non-resident of the Russian Federation - code 2.

Thus, despite the fact that personal income tax on the wages of foreigners from EAEU countries is withheld at a rate of 13% from the first day of work, it is still necessary to monitor their tax status taking into account the time they spent in the Russian Federation and correctly reflect this status in 2-NDFL certificates.

Keep personal income tax records in the web service, generate and submit 6‑personal income tax and 2‑personal income tax via the Internet

What to indicate the payer status in a payment order in 2021

The payer status is entered in field 101 of the payment slip, indicating the payer and the type of payment. This column can be filled with a numeric code or left empty. The last option is typical for transferring funds in favor of ordinary counterparties. Indication of status is required only when making payments to the budget. This allows the treasury to send and post payments quickly and correctly.

The main document regulating the procedure for filling out payment slips is the Order of the Ministry of Finance dated November 12, 2013, No. 107n. Options for current digital designations indicated in field 101 are specified in Appendix No. 5 of Order No. 107n:

- Code 01 – payer status in the payment order in 2021, designating the taxpayer (including the payer of insurance premiums) – a legal entity.

- The numerical combination 02 means that the money is transferred to the budget by a tax agent.

- Code 03 is used by postal organizations at the federal level for transfers on behalf of individuals (with the exception of customs duties paid).

- Tax authorities are designated by code 04.

- Code 05 is intended for payments from the FSSP - Bailiff Service.

- If a legal entity acts as a participant in foreign economic transactions, code 06 is used.

- Code 07 has been introduced for customs authorities.

- To designate payers who transfer funds to the budget, but the purpose of their payment is not related to the payment of taxes, insurance premiums or fees administered by the Federal Tax Service, code 08 is used. This payer status in a payment order in 2021 can be used by both legal entities and individual entrepreneurs, and by persons engaged in private practice when paying contributions for “injuries” to the Social Insurance Fund.

- When paying off obligations for taxes, insurance premiums and fees, which are under the jurisdiction of the tax authorities, the taxpayer status is indicated in the payment slip: 09, if we are talking about individual entrepreneurs;

- 10, if the payer is a notary;

- 11, when money is transferred on behalf of the lawyer who opened the law office;

- 12 – code designates the payer-head of the peasant farm;

- 13, if the payment is made by an individual.

- Code 15 was introduced to designate credit institutions and postal institutions. The code is used in cases where a payment order for a transfer from individuals is issued in one amount with the attached register.

- For individuals participating in foreign economic transactions, combination 16 is provided, and if the person has the status of an individual entrepreneur, then code 17 is used.

- When paying customs duties and there is no obligation to declare valuables, code 18 is entered.

- If organizations and their branches send money to the budget to repay an individual’s debt on the basis of a writ of execution, code 19 is applied. This combination can be used provided that the transferred money was withheld from the debtor’s salary.

- Code 20 denotes a credit structure that transfers funds for a separate payment received from an individual.

- Code 21 was introduced for responsible participants of consolidated groups of tax payers, and code 22 denotes ordinary participants of such groups.

- The FSS transfers funds by identifying the payer’s status in the payment order in 2021 with code 23.

- If the payment is made on behalf of an individual in favor of the Social Insurance Fund, code 24 is entered.

- Code 25 is used by guarantor banks when returning VAT and paying excise taxes.

- Code 26 denotes the founders of the debtor company who make payments to cover creditor obligations according to the register of claims in bankruptcy.

- For payments that, as a result of non-crediting to the recipient, are subject to return to the budget, banking organizations assign status 27.

- The latest version of the code combination is 28. It is intended to identify recipients of international mail.

Definition of status "24"

The taxpayer status number is useful when paying taxes and fees to the budgetary funds of the Russian Federation. The code itself is necessary to determine the payer in the Federal Tax Service system. A special code is indicated in field No. 101 of the payment slip.

Status “24” is a definition of an exclusively natural person, that is, a person who does not carry out legal activities. In the payment order, code “24” is entered when paying money to the country’s budget:

- Tax contributions.

- Insurance premiums “for yourself”.

- Contributions under the heading “injury”.

- Other contributions monitored by tax authorities.

The payer code is indicated not only in payments, but also in collection orders and payment orders.

Participants in the program for the return of compatriots

Code 4 in the “Taxpayer Status” section is applied if the employee is a participant in the program for the return of compatriots from the CIS countries to their homeland, Russia. Various social benefits are provided for this category of foreigners and their families, including a reduced percentage of income tax.

Rules for calculating personal income tax for immigrants:

- Wages, payments for services, bonuses and other earnings received as a result of work activities are taxed at 13%. The percentage should not be higher, even if the employee is a non-resident of the country. The benefit can be applied only after the foreigner presents a document proving the fact of participation in this state program. When hiring an accountant, you need to keep a copy of the document and regularly check its validity period. The certificate is issued to the migrant for three years.

- The rate applied to other unearned income depends on whether the immigrant becomes a resident. If yes, the percentage is 13%; if not - 30%. The category of unearned earnings includes gifts, financial assistance, and income from rental property.

- Standard group deductions can only be applied if the migrant has already become a resident.

On a note! A program participant has the right to find employment in the Russian Federation without a work permit.

How to download a certificate in a taxpayer’s personal account?

To download the 2-NDFL certificate, you need to go to the “My Taxes” tab and select “Income Information”.

The window that appears will display the history of 2-NDFL certificates. You need to select a year and a tax agent.

A zip archive containing files in XML, p7s and PDF formats is downloaded.

The electronic signature in the 2-NDFL certificate in PDF format is built directly into the document, and for the certificate in XML format it is a separate file in p7s format.

The downloaded certificate in PDF format can be attached to the 3-NDFL declaration. However, please note that if you also send a declaration through your personal account, you will not be able to attach a zip archive, a certificate in XML or p7s form. In this case - only in PDF format. However, as practice shows, an attached PDF with Federal Tax Service marks is sufficient.

If you need a certificate to apply for a loan or mortgage, then you usually need 2-NDFL for the last six months (or for the time actually worked, but not less than three months). But in LKN you can download a certificate for at least the previous year.

For example, you are applying for a mortgage in August 2021. The bank asks to provide a 2-NDFL certificate for the last six months. This certificate will not be in the LKN, since it will appear there no earlier than June 2020. This means that in this case you need to contact your employer, who can generate a certificate not only for the full calendar year, but also for the months actually worked, even if the year is not over yet.

Moreover, although the validity period of the 2-NDFL certificate is not established, since this is a report on income already actually received for the past period, most banks limit its validity to 30 days. And the downloaded certificates from the LKN indicate the date when 2-NDFL was submitted to the inspectorate by the tax agent. That is, in most cases, a 2-NDFL certificate downloaded from LKN is not suitable for banks.

Current rules for filling out a certificate

Certificate 2-NDFL is filled out section by section and item by item in the established order. The help contains up to 5 sections, each of which has filling lines.

Let's consider the filling rules in order:

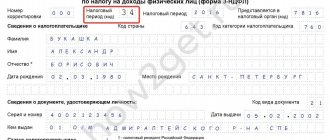

| Chapter | Line | Designation |

| 1 | — | Displays data regarding the tax agent himself, including information about his employer, TIN, checkpoint, etc. |

| 2 | 2.3 | Contains taxpayer status |

| 2 | 2.4 | The taxpayer's date of birth is displayed (in Arabic numerals) |

| 2 | 2.5 | Citizenship according to OKSM. For the Russian Federation this value is “643”. If your country is not on the list, then the country that issued the registration document is entered |

| 2 | 2.6 | A special code is noted that displays the type of registration document |

| 2 | 2.7 | Series and number of the registration document (for example, civil passport of the Russian Federation) |

| 2 | 2.8 | Address of residence or registration of the taxpayer, with accurate display of data (zip code, city, street, etc.) |

| 3 | — | Contains information according to the taxpayer’s income level. Information is displayed monthly. It is also necessary to indicate the presence of deductions from these incomes, displayed by code |

| 4 | — | The type of deduction is determined by category, which are property, standard, social, investment |

| 5 | — | Contains general values depending on the level of income of a citizen, his tax base, withholding taxes |

The finished document must be signed by a responsible person or authorized person on behalf of the employer, followed by an initial and signature.

Deadlines for submitting a certificate

It is necessary to submit reports on 2-NDFL certificates indicating the new status codes in order to avoid claims from regulatory tax authorities. If for some reason the organization did not withhold income tax by the end of the year, it is necessary to notify the tax authorities about this before March 1 of the following year in order to avoid penalties.

If an employee was dismissed for any reason during the year, then the certificate must indicate the code of his status at the time of dismissal. If a foreign citizen was employed, but by the end of the year he acquired resident status, then the certificate for him must indicate the number 1 in the status column. This rule does not apply to those who originally came from abroad and work under a patent. The status “6” remains for them.

The updated classification has simplified the determination of the status of specialists coming to work in Russia on patents, as well as on invitations from large companies. However, when filling out documentation, difficulties periodically arise that require detailed explanations.

Read also

11.01.2018

Documents confirming residence

According to the law, the tax agent himself keeps records of data about his employees and independently determines his status. And based on this, the tax amount is calculated. An employee's residence can be confirmed by the following documents: