What documents are considered cash registers?

Cash transactions are processed using cash documents, among which the following are required for use in 2021:

- cash receipt order (KO-1),

- expense cash order (KO-2),

- cash book (KO-4),

- payroll statement (T-49),

- payroll (T-53).

These documents can be maintained both on paper and on electronic media.

From the list above, only cash receipts and debit orders are directly classified as cash documents (clause 4.1 of Bank of Russia Directive No. 3210-U dated March 11, 2014). Other documents are not cash documents by law, but are still used when processing cash transactions.

The Federal Tax Service spoke about the intricacies of applying 54-FZ

Home • News • The Federal Tax Service spoke about the intricacies of applying 54-FZ

How will Law 54-FZ change in the near future? How to properly issue correction checks? Do I need to use an online cash register if payment comes through Yandex-Money? The head of the Operational Control Department of the Federal Tax Service, Andrey Budarin, answered these and other questions from 1C users.

— Andrey Vladimirovich, let’s remind you who should switch to using online cash registers in 2021, and who has a deferment until 2019.

— Until July 1, 2021, the following are exempt from the mandatory use of cash registers:

- legal entity and individual entrepreneur when performing work, providing services (except for public catering services).

- Individual entrepreneurs without hired employees when selling goods and providing services.

— Continuing the “educational education” — who has the right to tax deductions?

— Individual entrepreneurs on UTII and a patent, who previously did not have the obligation to use CCP, can reduce the amount of tax payable by the amount of expenses associated with the implementation of CCP. The deduction limit is 18,000 rubles per cash register, the number of cash registers is unlimited.

— Amendments to Law 54-FZ are currently being prepared. Please tell us about their essence.

— The bill has already been submitted to the State Duma and is expected to be adopted in the spring session. Among the amendments, for example, is the exemption of vending from receipt printing and the possibility of installing one cash register on several vending machines.

For repeated failure to use an online cash register for an amount exceeding 1 million rubles, an alternative sanction is introduced - a significant fine (now, as is known, only suspension of activities is provided for).

There will be an obligation to use cash register for all types of payments, incl. when money arrives to the current account through a bank operator.

There is direct responsibility for recording fictitious transactions at the cash register. That is, the cash register is increasingly becoming not just a means of recording revenue, but a means of calculating the tax base. And sometimes the only tool for determining it.

The amendments also provide for a change in the essence of the correction check. Now this is a super-simple document (the amount is adjusted plus or minus). The new correction check will be more complex and no less informative than the usual one. He will answer all the questions: what, where, when something went wrong, and how it should be “so.”

Finally, additional liability is introduced for CCP manufacturers for the supply of low-quality products.

— Letter of the Federal Tax Service N ED-4-20/24899 dated December 7, 2017 states that when making calculations without using a cash register (including due to its breakdown), the user must generate a cash correction receipt for each transaction performed. However, the subsequent letter N ED-4-20/25867 dated December 20, 2017 states that in the event of a massive failure, it is allowed to issue one correction check for the entire amount of unaccounted revenue. Does this mean that one check can only be issued in the event of a massive failure?

- In short, yes. The current check formats - 1.0 and 1.05 - do not provide for the detailing of the correction check by product range. Format 1.1. details the nomenclature, but it will only be implemented. It’s better for you if you split the correction checks at least by day - there will be fewer questions on our part. If you make a correction check with one total amount, then there will be no complaints against you, but there may be clarifying questions.

— How to properly report a correction check?

- For now, this is any written request - by Russian Post, by e-mail. For example, on such and such a date a transaction for such and such an amount was not reflected, and here are the details of the correction check for such and such an amount. From the end of February it will be possible to do this through the taxpayer’s personal account. But in the upcoming amendments, everything is simplified: the correction check itself is equated to a proper tax notification.

— The individual entrepreneur’s main activity according to OKVED 88.91 is “Providing day care services for children.” When is an individual entrepreneur required to start using an online cash register, or is he completely exempt from it?

— All services to individuals (except for catering) are for 2021. But Article 2 of Law 54-FZ directly names the types of activities exempt from CCP. And child care is listed there.

— If the software installed on a PC does not allow the buyer to send electronic receipts by email, is this critical?

— The question arises about the compliance of the technology used in this case with the law. Based on the current priorities of control work, and unless there is a complaint from the buyer, I cannot say that this is critical today.

— If there was a return from the buyer not on the day of purchase, but the money was issued from the operating cash register, is it necessary to issue a cash receipt order? What if on the day of purchase? For what amount should a cash receipt order be issued in these cases - taking into account the funds returned to the buyer or without taking them into account, based on the Z-report?

— We have been communicating with the Bank of Russia for some time regarding a joint explanatory letter on this topic. It is currently in the approval stage. The Central Bank’s approach is this: you can accept money via cash register and issue it from the cash register as many times as you like during the operating day. And you can issue a refund not on the day of purchase. But when you deposit this money into the organization’s cash desk, then a PKO is issued - and it indicates the balance of transactions made at the cash desk under 54-FZ.

— The organization used cash registers until July 1, 2017, while using UTII and the simplified tax system for excisable goods. Does she now have the right to use cash register only for sales related to the simplified tax system, and to issue a sales receipt for sales related to UTII?

— You may not use the cash register for UTII payments until July 1, 2018. And if there are no employees, then until July 1, 2019.

— What should you do if you incorrectly entered the cash register as cash? In fact, there was a non-cash payment.

— Main scenario: we do the reverse operation. That is, there was a receipt of 100 rubles in cash - we return 100 rubles in cash, and we do a new operation - the receipt of 100 rubles in electronic form.

What if the error was discovered now, but the transaction was performed last quarter? Now the Federal Tax Service has neither the goal nor the ability to completely verify all the data between your accounting records and the data passing through online cash registers. There will always be discrepancies, the question is their amount. If it is above a certain threshold, then we will ask what happened. But in the new 1.1 format this operation will be corrected correctly.

— What information goes to the tax office along with electronic checks? Name of the item sold? Or just amounts?

— All the information is lost, there are about 30 details, including those automatically filled in at the cash register.

— Should organizations now keep a register of cash register registers?

- No, they shouldn't.

— The cash register did not work, but there were sales through acquiring for non-cash payments. The money fell into the current account, but it is not in the OFD, because by the time the cash register was restored, the buyer with the card had already left. What to do?

— It is precisely for such cases that a correction check is needed. If it is not there and the tax authorities notice, it will be considered a violation.

— If an organization has changed its taxation system, does it need to re-register the cash register?

- No. When the cash register was initially registered, all available tax regimes were entered into its settings. If a new mode appears, you also need to load it into the ones available for the cash register. At the checkout, a report is made on changes in registration parameters - there is such a fiscal document. You don’t need to do anything in your personal FTS account.

— Is it necessary to connect an online cash register for an online store if an agreement has been signed with Yandex. Money" and "Robokassa"? Cash is not accepted, payment only through the terminal with bank cards.

— Yes, it is necessary, since the buyer used an electronic means of payment. And from the point of view of the law, what account the operator credited them to before sending them to you is not important.

— Is it necessary to punch a check in ruble equivalent when currency is received into the account?

- Yes, there are no options on this topic.

— The atelier provides repair and sewing services for clothes and shoes, using online cash register technology. The atelier wants to enter into an agreement with a courier service to deliver repaired and manufactured products to customers. It will be the principal, the courier company will be the agent. The courier will accept money from customers and issue a cash receipt from his machine. With such a scheme, how should the principal work with his online cash register?

— The atelier organizes the work correctly: we are not always obliged to use the cash register ourselves, we can entrust this to our agent. If there is a courier, then he has a cash register and should be used, payment is carried out there. But he uses the cash register precisely as an agent. That is, when punching a check, he will not read out this revenue to the agency service, but will assign it directly to the TIN of the principal (in the subject of payment). And put a tag that he is an agent.

In this situation, the studio itself may not use the online cash register at all. If it also accepts payments itself, then a cash register will be required, but it will not reflect the operations that the agent performed on its own behalf. They are immediately sent to the Federal Tax Service. However, the principal can see in his personal account how much money his agents accept and with what frequency.

— Is it possible to use the same cash register for online sales and sales in the office for cash?

- Can.

— When will taxpayers be required to switch to check format 1.1?

— Formats will change gradually, outdated ones will be phased out. This is more of a market stimulation for convenience, but it should be a natural movement.

— When can you switch from 1.0 to 1.05 without changing the fiscal drive?

— As soon as the order to change the format of fiscal documents is signed. Expected at the end of February. As for the transition from 1.05 to 1.1 without replacing the fiscal drive, this possibility has not yet been confirmed by the drive developers.

— Can an organization, providing additional vocational education services, accept money from individuals on the website? In order not to write out a BSO and, especially, not to connect a cash register, since it works with individuals extremely rarely.

- In this situation, it is better to hire an agent. But the right to use BSO will remain with the organization until July 1, 2019.

— How long should cash receipts be kept?

- There is no need to store them. Unless you don't need them, of course.

— How to process returns of goods from retail customers, through cash register or cash register?

- You can do it both ways.

— Is it necessary to use an online cash register when receiving payments to an organization’s current account from individuals without using acquiring payment systems (for rental services and utility bills in a residential building)?

— If you are sure that electronic means of payment were not used, then there is no need.

— The non-profit organization accepts membership fees and charitable donations from individuals for its activities. Is it necessary to issue cash receipts in this case?

- No no need.

— How detailed should a receipt for the sale of services be? The company provides repair services for household appliances and televisions. In the receipts we indicate: household appliances, power tools, digital equipment. Is this enough or do I need to indicate the name of the repaired product?

— The name on the receipt must correspond to the name in the price list or on the price tag, or on the packaging.

— Is it necessary to use online cash registers if a legal entity issues an invoice to an individual entrepreneur, and he pays it from his current account?

- Of course not.

— The individual entrepreneur has a stationery store on UTII. A commodity accounting program is not used; only the purchase amount is recorded online, and if necessary, a sales receipt is issued manually. Is it possible to trade like this and until when?

— Individual entrepreneurs on UTII (retail and catering with employees) by law must use the cash register from 07/01/2018, and household services and retail/catering without employees - from July 1, 2021. The name and quantity of goods in the receipt may not be indicated until February 1, 2021. But only if there are no excisable goods. If there is at least one, then all names are indicated on the check.

— Registered an online cash register with a 15% simplified tax system. But when the first two checks were punched, it turned out that the simplified tax system was 6% (the company that installed the cash register had set something wrong in the drivers). Then they corrected it. What to do with checks? The amount is correct.

— In this situation, it is better to issue a refund within one tax period, and then a new receipt.

— If the operation of the online cash register of an online store (payment on the website by card) fails, and the checks are not punched, or are punched on a different date (both for receipt and for return), how to make corrections correctly?

— If the check is not cleared (cash register is not applied), make a correction check. If there is an error, then return and subsequent arrival.

— LLC on OSN (wholesale trade). The Ministry of Finance says that when a payment is received from an individual to a bank account, a cash receipt must be issued. But doesn’t this result in doubling of revenue (both to the current account and according to the cash receipt)?

— If an electronic means of payment was used, you need to use cash register. There won't be any confusion, we'll figure it out ourselves.

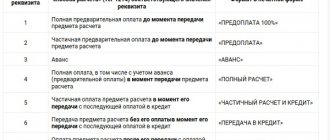

— How to properly issue a check in case of prepayment? An individual, as a rule, makes 40% as an advance payment, the rest of the payment in the amount of 60% after two months.

— First, a check for the 40% advance. Then the payment is 100%, including 40% in advance.

— The organization entered into an agreement with Russian Post to provide courier services for the delivery of parcels to the population (online commerce). Buyers pay for the parcel upon receipt, and Russian Post then transfers the payment to the organization. Is a cash register needed in this case?

— If Russian Post is an agent of the organization, then no. She has the appropriate technology.

— The company services video surveillance systems for individuals for cash payment. There are 8 foremen in the organization, the nature of the work is traveling. Strict reporting forms are now used. Will every master really have to buy a cash register?

— You need to either organize payment online on the website, or buy each one at the cash register - if all 8 are traveling at the same time.

— What threatens an individual entrepreneur if there are errors in issuing a check?

— 1500-3000 rubles fine for each case. One third of this amount if simplified procedure.

— How much does a license for the right to sell and service cash register machines cost?

— There is no such license in nature.

— If a farmer sells at the market, where you can hardly find an outlet, what should you do with the use of online cash registers in this case?

— You can trade at markets and fairs without a cash register.

CATALOG OF NEW ONLINE CASSES

Did you like the article? Share it on social networks.

Add a comment Cancel reply

How long to store cash documents in 2021

The storage periods for cash documents are specified in the list, approved. Order of the Ministry of Culture of Russia No. 558 dated August 25, 2010, and depend on the type of document. Information on shelf life is presented in the table:

| Document's name | Shelf life | From what date should the deadline be counted? | Base |

| Payroll T-49, payroll T-53, used for calculating and paying salaries, stipends, etc. |

| From January 1 of the year following the year in which the document was generated | clause 412 of the list, approved. Order No. 558 |

| 5 years Note: tax legislation establishes a shorter storage period for primary documents than accounting legislation - 4 years (subclause 8, paragraph 1, article 23 of the Tax Code of the Russian Federation) therefore we take the longest period - 5 years (according to Law dated December 6, 2011 No. 402-FZ) | From January 1 of the year following the reporting year | paragraph 362 of the list, approved. by order of the Ministry of Culture dated August 25, 2010 No. 558, clause 1 of Art. 29 of the Law of December 6, 2011 No. 402-FZ “On Accounting” |

Example

The cash book is stitched, sealed and signed by the manager on December 31, 2021. The shelf life of the book begins on January 1, 2020 and ends on December 31, 2025.

Is it necessary to store Z-reports of an online cash register?

Author of the article Victoria Ananina 6 minutes to read 10,372 views Contents The Z-report (today called the shift closing report) is a daily report on the operation of the cash register, carried out at the end of the cashier’s shift (it is not reset to zero in online cash registers).

The use of online cash registers in work is aimed at reducing paper reporting and exchanging information between the entrepreneur and the Federal Tax Service in electronic format. Today, entrepreneurs, regardless of the applicable tax regime, are required to switch to online cash registers, but conducting cash register transactions directly on site remains the same.

Let's consider the need to generate Z-reports and store them. Federal law on the use of the CCT. The Bank of Russia's instructions on the procedure for conducting cash register transactions. The Ministry of Finance of the Russian Federation rules for the operation of cash registers. Resolution of the State Statistics Committee of the Russian Federation, forms of primary documentation for accounting calculations. Letter of the Ministry of Finance of the Russian Federation dated January 25, 2017 N 03-01-15/3482 is not subject to the mandatory use of primary forms

Storage periods for cash receipts and fiscal storage in 2020

With the introduction of online cash registers, the seller does not need to save paper receipts, however, he is obliged to store the FN (fiscal drive) for 5 years from the moment its use is completed (Clause 2 of Article 5 of the Law of May 22, 2003 No. 54-FZ “On use of cash register equipment...").

Due to the fact that all information about purchases is recorded on the drive, the need to maintain and store the cashier-operator’s book has disappeared.

The situation is completely different when an organization acts not as a seller, but as a buyer - purchasing something for its needs and receiving a payment receipt issued by the supplier’s online cash register. In this case, the buyer keeps the check as the primary document confirming the transaction for 5 years after the end of the reporting year.

Paper checks fade quickly, so to fulfill the duty of storing them you can:

- ask the seller to send the check electronically (for this you need to provide an email address, phone number, read the QR code);

- Immediately make a copy of the check and file it with the original.

The data specified in the receipt or BSO must be readable for at least 6 months after the business transaction (Clause 8, Article 4.7 of Law No. 54-FZ).

Shelf life of control tape

“Raschet”, 2006, N 12 LIFE LIFE OF “CONTROLS”: DAYS OR YEARS The question of the shelf life of cash register tapes and Z-reports is unlikely to arise for a company where only a few checks are punched per day. But if the turnover is rather large and the entire roll of cash register tape is used per shift, then the picture turns out to be completely different. All this “waste paper” must be stored, and not for a day or two. How much? Let's try to figure it out. Five years... Cash register tapes must be stored for at least five years. This period is established in clause 11 of the Regulations on the use of cash registers when making cash payments to the population (approved by Government Resolution No. 745 of July 30, 1993). One of the retail companies tried to clarify with specialists from the Ministry of Finance: is it possible to shorten the five-year period and destroy the used control tape of cash registers earlier? The fact is that the company includes fifty stores. The amount of waste tape is huge. Storing it for five years is simply unrealistic. Warehouses will be required no less than for storing goods. And from a fire point of view, it is dangerous to store so much “waste paper”. Paper is a highly flammable material. It turns out that the company will have to not only allocate space for storing waste paper tape, but also think through fire safety issues. However, officials from the Ministry of Finance were adamant. They made an unambiguous conclusion: the shelf life is at least five years (Letter dated December 27, 2004 N 03-01-10/6-219). 15 days... However, the ministry’s specialists forgot about the Standard Rules for the Operation of Cash Registers, which they themselves approved. So, in these Rules it is written in black and white that “used control tapes are stored in packaged or sealed form in the accounting department of the enterprise for 15 days after the results of the last inventory have been carried out and signed” (clause 6.4 of the Model Rules, approved by the Letter of the Ministry of Finance dated August 30 1993 N 104). Officials of the Ministry of Finance expressed a similar opinion in 2001 (Letter of the Ministry of Finance dated April 3, 2001 N 16-00-14/155). As you know, a company must conduct an inventory of property regularly. There are cases when it is necessary to take an inventory. All of them are listed in Art. 12 of the Law of November 21, 1996 N 129-FZ “On Accounting”. For example, before preparing annual financial statements. This means that if, for example, the control tape ended in December, and the inventory takes place at the end of the year, then the tape only needs to be stored until mid-January of the next year. The January “control” will have to be left in the accounting department for about one year. Of course, this is a long period of time, but still not five years. In addition, it can be shortened. The fact is that trade organizations, as a rule, traditionally carry out scheduled inventories at least once a month (on the first day). At the very least, once a quarter. And since the results of the inventory are approved by the head of the organization within a month after it is carried out, then, consequently, the lifespan of the used control tape is a maximum of two months. It turns out that the company must independently decide: to protect the used cash register tape for five years or to limit its storage period to the nearest inventory - annual, quarterly, monthly. But the opinion of the company may not coincide with the opinion of the inspectors. Will they be able to “punish” the company in this case? There are no legal grounds Officials from the State Interdepartmental Expert Commission on Cash Register (GMEC) tried to legitimize a fine of thirty-five thousand rubles for “improper storage of information about cash transactions in the fiscal memory of a cash register and on control tapes.” However, their proposal did not go through. In the Law on Cash Register No. 54-FZ of May 22, 2003, there is no article on liability for unsaved “control”. Let's figure out what tax authorities can refer to if they want to fine a company for the lack of a cash register tape or Z-reports. For example, would this be a tax offense? No, it will not. And that's why. Let's take Art. 120 Tax Code. It states that “a gross violation of the rules for accounting for income, expenses and taxable items is the lack of primary accounting documents.” If the lack of primary registration does not lead to an underestimation of the tax base, then the company may be fined 5,000 rubles. (Clause 1 of Article 120 of the Tax Code). But, according to the judges, neither the cash register tape nor the Z-report can be classified as primary accounting documents (Resolution of the Federal Antimonopoly Service of the Ural District dated January 3, 2002 N F09-3224/01-AK). The fact is that a document will be primary if it is drawn up in a form from an album of unified forms or contains mandatory details (Clause 2, Article 9 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting”). The list of unified forms was approved by State Statistics Committee Resolutions No. 132 of December 25, 1998 and No. 88 of August 18, 1998. There is no trace of a cash register tape or Z-report there. Only the cashier-operator's journal has been approved as a form of primary documentation for cash transactions. There is also art. 126 of the Tax Code. According to it, a company can be held liable for “failure to submit to the tax authorities documents and (or) other information provided for by the Code and other acts of legislation on taxes and fees.” The fine is fifty rubles for each document. But the legislation on taxes and fees does not establish the taxpayer’s obligation to submit cash register tapes and Z-reports. And the Regulations on the use of cash registers have nothing to do with the legislation on taxes and fees. Consequently, tax authorities have no reason to fine the company under Art. 126 of the Tax Code. Judges adhere to a similar position (Resolution of the Federal Antimonopoly Service of the Ural District dated January 3, 2002 N F09-3224/01-AK). Price of the issue But it will probably be possible to bring the director of the company to administrative responsibility. After all, it is he who is responsible for storing accounting documents (clause 11 of the Regulations on the use of cash registers when making cash payments to the population (approved by Government Resolution No. 745 of July 30, 1993)). And the legislation provides for administrative liability for officials for violating the terms and procedures for storage (Article 15.11 of the Code of Administrative Offenses of December 30, 2001 N 195-FZ). Fine - from 2000 to 3000 rubles. So the company must decide how significant this amount is for it. Let's believe in progress As you know, modern cash registers are equipped with EKLZ - an electronic control secure tape. It registers and stores information about each check issued on the cash register. Moreover, the storage is “non-volatile and long-term” (clause 1.1 of Appendix No. 4 “Guidelines for the use of EKLZ”, approved by the GMEC on June 25, 2002 No. 4/69-2002). Using queries from EKLZ, its data can be obtained by document number, control tapes by shift number, and generalized reports by a given period. Information from the EKLZ can be printed on a cash register or saved electronically on another medium. Storing such an “electronic tape”, unlike its paper counterpart, is safe and easy. If officials believed in progress and decided to abandon the storage of “waste paper,” then the question of shelf life would become unimportant. A small electronic device can be protected for a year, five years, or more. A. Ignatov Signed for publication on November 25, 2006

What are the consequences of violating the storage period for cash documents?

If you get rid of a cash document confirming a business transaction ahead of schedule, tax authorities may deduct the corresponding expenses during audits. The result is additional taxes, penalties and fines.

In addition, for the absence of primary documents, inspectors can fine the taxpayer 10,000 rubles. (for primary violation) or 30,000 rubles. (if repeated) - in accordance with Art. 120 Tax Code of the Russian Federation.

There is also an administrative penalty for officials for violating the terms of storage of documents:

- fine under art. 15.11 Code of Administrative Offenses in the amount of 5,000-10,000 rubles. (for a primary offense), 10,000-20,000 rubles. or disqualification for a period of one to two years (for repeated violation);

- fine under art. 13.20 Code of Administrative Offenses in the amount of 300-500 rubles.

Should I save receipts for closing an online cash register shift?

News Tools Forum Barometer.

Login Register. Login for registered:. Forgot your password? Login via:. Previously, you entered through. WATCH THE VIDEO ON THE TOPIC: Online cash register Atol 91F Shift closure report The reform of the gradual transfer of business to online cash registers was not initially accepted by all entrepreneurs; many saw this as unjustified costs for their activities.

Time has convinced us of the usefulness of the innovation.

One of the positive aspects is the elimination of some reports on online cash registers. In this article we will look at what reports are generated by the online cash register, the features of each type and the procedure for storing cash documentation. I accept the terms of information transfer.

The latest generation cash registers create fiscal documents and remotely send them to the Tax and Duty Inspectorate.

The memory of the fiscal drive stores reports on the online cash register, which reflects:. Printing out cash register reports and storing them on physical media are a thing of the past; nowadays everything is stored in an electronic version; let’s look at them in more detail. Subscribe to our channel in Yandex Zen - Online Cashier!

Be the first to receive the hottest news and life hacks!

After registration with the Federal Tax Service, a registration report is displayed once

How to destroy expired documents

If cash documents have expired, they must be destroyed. It is necessary not only to get rid of documents, but also to arrange it correctly. For this purpose, an act “On the allocation for destruction of documents that are not subject to storage” is drawn up. It is signed by an expert commission, the composition of which must be approved by the head of the organization.

Form for document destruction act

If there are a lot of documents to be destroyed, you do not need to indicate a complete list, but only their type. For example: advance reports for ____ year.

There are two ways to get rid of documents:

- on your own (if the volume of papers is small);

- with the help of a hired organization.

If you destroy papers yourself, you can use a shredder - it's quick and convenient.

Ways to restore faded ink

When a receipt is urgently needed for reporting, but it turns out to be pale and illegible, you can try to restore it.

- In order for the text printed on the paper to appear, you need to hold it a little over the flame of a candle or lighter. Do this carefully so that the document does not catch fire. This method of restoring checks may well work. But it’s better to practice on unnecessary receipts first.

- You can also use a solution of soda and salt , into which the check requiring restoration is dipped. This will help return the inscriptions to readability, but the paper will need to be dried.

- Heat treatment with an iron is another option for returning a lost image. As it turned out, under the influence of high temperature, letters can not only disappear, but also appear.

The methods for restoring faded checks that were described above are not a guarantee of success. They are all quite risky. Any mistake can lead to the complete destruction of the receipt.

Let's sum it up

- The shelf life of most cash primary documents is 5 years, counted from January 1 of the year following the reporting year. Salary statements are stored for 5 years (if there are personal accounts), 75 (50) years (if there are no personal accounts).

- Owners of online cash registers are required to store not the punched checks themselves, but a fiscal drive in which all information about sales is recorded.

- Tax and administrative liability is provided for violation of the terms of storage of documents.

If you find an error, please select a piece of text and press Ctrl+Enter.

How to store checks with cancellation online at cash desks

The Z-report today, called the shift closing report, is a daily report on the operation of the cash register, carried out at the end of the cashier’s shift in online cash registers and is not reset to zero. The use of online cash registers in work is aimed at reducing paper reporting and exchanging information between the entrepreneur and the Federal Tax Service in electronic format.

Today, entrepreneurs, regardless of the applicable tax regime, are required to switch to online cash registers, but conducting cash register transactions directly on site remains the same.

Let's consider the need to generate Z-reports and store them. The Z-report implied closing and resetting the cash register once a day, and the proceeds were handed over to the administrator and senior cashier for further collection. WATCH THE VIDEO ON THE TOPIC: Paycheck: How will the transition to online cash registers hit small businesses?

Features of generating a report on the closure of a shift at an online cash register The reform of the gradual transfer of business to online cash registers was not initially accepted by all entrepreneurs; many saw this as unjustified costs for their activities.

Time has convinced us of the usefulness of the innovation.

One of the positive aspects is the elimination of some reports on online cash registers.

In this article we will look at what reports are generated by the online cash register, the features of each type and the procedure for storing cash documentation.

I accept the terms of information transfer.

What are checks needed for?

It’s time to ask the question: why keep a pile of unnecessary papers at all? In fact, often the receipt turns out to be needed precisely after it has already been thrown away.

Cases in which a check may be needed:

1. Return of goods under warranty. When purchasing expensive equipment or furniture, the buyer is given a guarantee that is valid for several years. It often turns out that an item has become damaged and needs to be returned or exchanged, and the receipt, after being stored for a long time, has already lost not only its presentable appearance, but also its information. In this case, it will be very unpleasant for the buyer, since nothing can be done with the broken product in the absence of evidence of its purchase. 2. Receiving a discount in the store. Some stores have bonuses that you can get when you accumulate purchase receipts. For example, the buyer presents checks for a certain amount, and the seller gives him a discount card. 3. Housekeeping. Many families accumulate monthly receipts and at the end count the amount spent on certain products. These calculations are a necessary part of the family economy, because without this it is impossible to calculate future prospects. 4. Proof of payment for services. When paying for training or housing and communal services, any problems may arise that can only be resolved by submitting a receipt for the actual payment. As a rule, these amounts are quite large, so it would be sad to lose money due to bad check paper and ink.

How to work with different models of online cash registers when closing a shift

A cash register closure report can be generated in different ways at new online cash registers. In most cases, the cashier needs to perform a number of operations provided by the equipment program, that is, in a certain sequence, press buttons on the machine or touch screen, selecting the necessary items in the menu.

Get acquainted with the algorithm for generating a report receipt at the Atol cash register in the video:

On Mercury equipment, the procedure for closing a shift is much simpler and more logical, as can be seen from the video instructions:

Is it necessary to store Z-reports of an online cash register?

The Z-report (today called the shift closing report) is a daily report on the operation of the cash register, carried out at the end of the cashier’s shift (it is not reset to zero in online cash registers). The use of online cash registers in work is aimed at reducing paper reporting and exchanging information between the entrepreneur and the Federal Tax Service in electronic format.

Today, entrepreneurs, regardless of the applicable tax regime, are required to switch to online cash registers, but conducting cash register transactions directly on site remains the same.

Let's consider the need to generate Z-reports and store them. The use of cash register systems implies the cash flow of an organization or individual entrepreneur.

The Z-report implied closing and resetting the cash register once a day, and the proceeds were handed over to the administrator (senior cashier) for further collection. Based on the Z-report, the cashier generated: a cashier’s certificate-report and a cashier-operator’s journal.

These documents reflected the movement of money through the cash register for the shift and were transferred to the accounting department. The document was displayed once a day (at the end of each shift), that is, it is necessary to prepare a report for each shift. Generating a Z-report seems to be a simple operation depending on the specific cash register. However, there were the following restrictions:

- on weekends there was no need to reset the cash register

- on weekdays, in the absence of cash transactions, the Z-report was taken with zero indicators, and cashier reports were also compiled on its basis.

Z-reports that should have been kept

Features of generating a report on the closure of a shift in the online cash register

» Amendments to Law 84-FZ affected not only the scope of use of cash register equipment, the generation and transmission of checks, but also basic reports.

The Z-reports familiar to cashiers are a thing of the past, but they have been replaced by shift closure reports. The main difference between the new fiscal document is the need to send it automatically to the Federal Tax Service. But there are a number of other features of its formation and storage.

After losing force on July 1, 2021, which is reflected in the regulations governing the use of CTT using paper control tapes, the question logically arose about the forms of primary documents.

IN . It is explained that Resolution of the State Statistics Committee No. 132 dated December 25, 1998, which reflects the provisions on the forms of primary documents, as well as Federal Law-402 “On Accounting”, which has been regulating since January 2013 the form of primary accounting documentation used for the formation of unified journals and albums , are no longer valid and are not binding. It turns out that with the transition to online versions of cash registers, organizations and entrepreneurs do not have to generate the usual Z-report, information from which was previously entered without fail into the Cashier’s Certificate Report (f.

No. KM-6), as well as in (f. No. KM-4).

How then can entrepreneurs record data at the end of a working day or shift?

Clause 4 of Article 4.1 of Federal Law No. 84 brings clarity, where the list and requirements for the formation are prescribed.

When using an online cash register, closing is carried out with the appropriate report, the mandatory details of which are reflected in Chapter II of Appendix 2 of FSN Order No. ММВ-7-20/229 dated March 21, 2017.