Home • Blog • Online cash registers and 54-FZ • Correction receipt at the online cash register

A correction receipt at the online cash register is needed when making changes to previously made calculations. Such a document is used to correct errors and violations, and its legality is established by 54 Federal Law of 2003 (clause 4 of Article 4.3).

Online cash register service at a discount

Get a discount on annual technical support for KKT on the “Maxi” and “Standard” tariffs - there is a special offer.

Find out more details

When is a correction check needed?

The correction cash receipt is strictly processed when the cash register shift is open. The procedure can be performed any day before the end of the shift. In the event that an error is noticed on another day, a check is also issued when the shift is open.

What are the errors at the checkout:

- The employee entered the check amount incorrectly.

- The employee completely forgot to fill out the fiscal document on the cash register.

- Instead of an adjustment, a return check was issued.

In case of failure at the checkout:

- The cash register turned off due to a power failure.

- The cash register has broken down or the software has crashed.

Examples of working with a correction check

It is not always possible to immediately understand why an online cash register correction check is needed. Both it and the receipt return check are punched for various reasons. Depending on this, what should be done when an error is detected:

- During the purchase, an incorrect, erroneous cash receipt may be entered. The buyer paid 13 thousand rubles, and the cashier struck 14 thousand. He noticed his mistake immediately, before the customer left. In this case, you should correct the situation in this way: first punch out the “Return of Receipt” check, and after that – a check with the amount that should be. The same steps should be taken if the purchase is returned.

- The fact that an error had occurred became noticeable when the shift was closed. Instead of the required 13,000 rubles, the cashier charged 12,000, although the buyer paid exactly as much as the purchased item cost. The correct decision would be to break the correction check. The “Receipt” attribute must refer to the amount of unaccounted revenue - one thousand rubles.

- A cashier's error led to a shortage. The product cost 13 thousand rubles, the cashier struck 12 thousand, and the buyer paid the same amount. The correction check does not go through, since it is issued only when there is more money in the cash register than there should be.

The instructions in case of such situations say that in the event of a correction check, it is necessary to notify the tax office about this as soon as possible. However, if this was not possible, and the Federal Tax Service issued a fine, it must be remembered that financial punishment in itself does not cancel the adjustment and does not justify its absence.

The best offers in price and quality

The correction check is generated regardless of the circumstances that led to it. The following will need to be specified in the details: in the “Bases” section – the details of the order, the type of manipulation will be defined as “Operation as prescribed”. 1C accounting provides for the reflection of such transactions.

How to properly draw up a correction check

You cannot issue a check for the entire amount of transactions not carried out on the cash register, with the exception of a massive failure in the operation of the cash registers. It is recommended to generate receipts for each transaction separately, which took place without a cash register.

What details should a correction check contain? Order of the Tax Service of 2021 No. ММВ-7-20/ [email protected] establishes the following mandatory details:

Settlement attribute with value 1 (receipt transaction) - issued when a purchase receipt has not been issued.

Payment attribute with value 3 (expense transaction) - issued when you need to withdraw part of the funds from the online cash register.

According to the rules, a corrective fiscal document can contain only one detail; using two at the same time in a check is unacceptable.

Correction type with a value of 0 - indicates the reason, in this case it is data correction at your own request.

Correction type with value 1 - making changes as determined by the Federal Tax Service when a violation is detected.

Correction description details - indicate the reason for the operation and the document (note, act or other document on the basis of which the correction is carried out).

Document date of the basis for the correction.

Foundation document number.

Cashier details - information about the cashier.

The receipt does not need to indicate the product range and price.

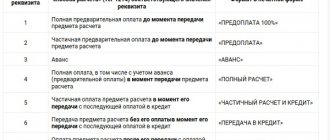

What else needs to be indicated on the check:

|

|

Correction check for different FFDs

Let us remind you that a cash receipt and other fiscal documents are created at the cash desk according to a certain format of fiscal data (for more details, see “Cashier receipt: what details it should contain and in what format they should be indicated”).

To date, three formats have been approved: 1.0, 1.05 and 1.1 (FFD 1.1 is not yet used in practice). Fiscal documents created in different formats differ in the number of details. Thus, a correction check drawn up in format 1.1 will have over 20 details (unlike the current version of the correction check, which has a minimum number of details). All details of the correction check are fixed by order of the Federal Tax Service of Russia dated 03/21/17 No. ММВ-7-20/ [email protected] (as amended by the order dated 04/09/18 No. ММВ-7-20/ [email protected] ).

Depending on which FFD is used at the checkout, the user must decide whether to issue a correction check to correct a particular situation. For clarity, we have shown this in the table.

| Fiscal data format | Why is a correction check created? | |

| 1.0 | Valid until January 1, 2021 (Order of the Federal Tax Service of Russia dated March 21, 2017 No. ММВ-7-20/ [email protected] ) | A correction check is needed in order to process a payment that occurred without using a cash register |

| 1.05 | Valid. Expiration date unknown | |

| 1.1 | Expected to come into effect in 2021 | A correction check is needed in order to process a payment that occurred without using a cash register, as well as in order to correct errors made by the cashier when generating a cash receipt |

Buy a fiscal drive and enter into an agreement with the OFD

You might also be interested in:

Online cash registers Atol Sigma - how to earn more

How to make a return to a buyer at an online checkout: step-by-step instructions

MTS cash desk: review of online cash register models

Scanners for product labeling

Shoe marking for retail 2021

Online cash register for dummies

Results

The purpose of the correction cash receipt is to record changes in calculations made previously. The “Settlement attribute” attribute in the correction check can contain only one of the values: receipt or withdrawal. For the purpose of control by tax authorities, the adjustment must be accompanied by a supporting document.

If you trade or plan to do so via the Internet, read the article “Do you need an online cash register for an online store?”

See also: “How to cancel a check at an online cash register?”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to correct an error on a check

Let's assume that the buyer paid cash for the purchase, and the cashier punched the receipt, as if paying with a plastic card. In this case, it is necessary to punch out a new document, but not a correction check. The online cash register has already transmitted information about the completed transaction to the tax authorities, and the data has been recorded on the fiscal drive. Therefore, the cashier needs to cancel the operation with a new check; it will essentially be returnable. It is necessary to indicate the calculation attribute “receipt return”. This fiscal document must contain the same data as the primary one, including the incorrect form of “electronic” payment, as well as its fiscal attribute. This allows you to undo an invalid operation. After which the cashier will be able to issue a new correct check with the “receipt” calculation sign. In this case, the buyer must receive both documents: return and corrected. However, there is no need to ask for an old, erroneous check back.

In an interview with the General Ledger, a Federal Tax Service specialist explained that the correction check can only contain calculation signs of “receipt” and “expense”. The signs “return of receipt” and “return of expense” can only be indicated on receipts for the return of goods. By the way, if the cashier made a mistake in the cost of the goods and sold the buyer an item more expensive than it costs, for example, 300 rubles instead of 200, he must issue a fiscal document for return with the “return of receipt” sign, and then re-sell the goods at the correct price. This is what you should do if an inaccuracy is discovered immediately. If excess money in the cash register and an incorrect amount in the check are discovered at the end of the shift, then he will have to draw up a corrective document with the sign “receipt”, and also write an explanatory note regarding the excess in the cash register.

However, any kind of correction may be required not only on the day of purchase, but also several days later. After all, a mistake may be discovered later if the buyer brings an incorrect document. By opening a new shift for, an online cash register user can enter a correction or refund check for any date (for example, if a shift was opened on August 20, but the error needs to be corrected on March 3). In this case, the date does not play a role and you need to issue a refund of the receipt through a correction check in the same way. When online CCT is used, this makes it possible to correct any inaccuracy or oversight.

Differences between a correction check and a refund check

If an error was discovered by the buyer, there is no need to generate an expense correction check and use a return document. They differ in content.

A correction check differs from a “receipt return” in the following ways:

- sign “Return”;

- generated when an error is detected in the presence of the buyer;

- each item being returned is indicated;

- along with this document there must also be a memo and an invoice in two copies: one for the retail outlet, and the second for the buyer.

The receipt correction check has the following design features:

- sign “Correction”;

- breaks through if there is a shortage or extra money in the cash register;

- the Cheka does not have a list of goods and their prices;

- together with it, an act and an explanatory note must be drawn up: the originals remain at the enterprise, and copies are sent to the Federal Tax Service.

An example of a correction receipt at an online cash register can be seen above. Example “Return of receipt”:

How to issue a correction check: step-by-step instructions

If a shortage or excess of funds is detected in the cash register, the seller must first draw up an act or explanatory note with a comprehensive description of the problem. Then the same document is drawn up for the correction check itself. The details of this paper will be indicated on the receipt.

After this, the seller begins to actually generate the correction check. The release procedure is described in detail above. Then all that remains is to transfer information about the correction to the local tax office - and the correction procedure can be considered completed. The Federal Tax Service will promptly make a decision and, most likely, release the enterprise from administrative liability.

Using a correction check: legislative framework

Federal Law No. 54 of May 22, 2003 states: entrepreneurs and organizations that violated the law in the field of using cash register equipment are required to issue a correction check. The law covers any cases of violations: working without a cash register at all, incorrectly punched check, etc.

Article 14.5 of the Code of Administrative Offenses adds: a person who has reported to the tax authority that he has discovered violations in his work can avoid administrative liability for these violations. The fine will be canceled if the following conditions are met:

- A legal entity must independently discover its violation and report it to the tax office, which, in turn, should not know about this violation until the very moment the application is received. That is, if the tax office discovers errors before the entrepreneur himself, it will not be possible to avoid a fine.

- The legal entity must independently correct its violations by running a correction check. Accordingly, without such a check it will also be impossible to avoid punishment.

- The legal entity must submit detailed, comprehensive explanations about the fact of the offense to the tax office. This is necessary so that tax authorities can reliably establish the circumstances and causes of the violation.

If the entrepreneur fulfills each of these points, administrative responsibility will be removed from him.

note

Fines for violations of cash register equipment are quite impressive:

- for individual entrepreneurs – from 10 thousand rubles;

- for legal entities – from 30 thousand rubles.

The statute of limitations for such cases is a full year. That is, during the year, the tax inspectorate can come to the enterprise, check it for errors in receipts and fine it if they are found.