Net assets of LLC

Current as of: December 18, 2021

The net assets of a company are those company's own funds that will remain with it after it has paid off all creditors. That is, it is the difference between a company's assets and its liabilities, subject to minor adjustments. Another way to determine the net asset indicator is to take the total indicator of Section III of the balance sheet “Capital and Reserves” and also adjust it by certain amounts. That is, net assets are the capital of the LLC.

Annual reporting: balance sheet liabilities

Let us dwell on the common definition of “liability”, that is, property at the disposal of the owner. There are no particular difficulties in understanding this definition, so let’s immediately consider the principle of filling out lines. Let's start with “Authorized capital” and “Retained earnings (uncovered loss)”. Profit refers to the income of the organization, which can be distributed at the request of the company's participants. Combining the authorized capital and retained earnings in one section of the balance sheet (III. Capital and reserves) sometimes suggests that not only the profit received can be paid to the owner, but also the capital can be divided among the participants, considering it as previously created income. But this is not so: PBU 1/98 “Accounting Policy” establishes the separation of owners and legal entity, and until a decision is made to liquidate the company, the authorized capital remains indivisible. In Russia, the practice of joint stock companies with a large number of shareholders is not very common, or the percentage of their ownership is too small, and they cannot influence decisions on the distribution of income. Therefore, usually dividends are paid to 2-3 participants from profits, but if you still have shareholders, then you can offer them 2 ways: receiving dividends or investing the profits in the further development of the company. Therefore, even if you have only a few shareholders, it is better to discuss these options in advance, since a sudden withdrawal of large amounts can negatively affect the business.

If net assets are less than authorized capital

If your company's net assets have become less than its authorized capital, then you are obliged to reduce the authorized capital to the level of net assets and register such a decrease in the Unified State Register of Legal Entities (clause 4 of article 90 of the Civil Code of the Russian Federation, clause 3 of article 20 of the Law of 02/08/98 N 14 -FZ). That is, at least after drawing up the annual financial statements, you need to compare the authorized capital and net assets.

In addition, the following rule applies. If an LLC decides to pay dividends to participants, but as a result of accrual of dividends, the value of net assets becomes less than required, then dividends cannot be accrued in the planned amount. It is necessary to reduce the profit distributed on dividends to an amount at which the above ratio will be satisfied.

At the same time, no liability has been established for violation of the requirement for the ratio of authorized capital and net assets.

Error in DDS article when submitting annual reports

For example, you received a request to provide explanations regarding discrepancies found in the data of the annual financial statements and 2-NDFL certificates. After a thorough check, it turns out that the disagreement arose due to the fact that one of the details was incorrectly indicated in the cost item, so the amounts were not reflected in the Cash Flow Statement form.

Let's look at this situation.

So, there were discrepancies in 2-personal income tax and annual reporting. What do they have in common? It's all about dividends. But what's wrong with them? They are reflected in the SALT; there is a difference between the balance sheet and the profit and loss account. Then you need to check the “composition” of the DDS article. It turned out that the “Type of movement” attribute was selected incorrectly, and therefore the data on dividends was not reflected in the required column of the report (page 4322). After correcting the error and refilling, everything falls into place.

If you have such discrepancies, first check the subconto. To do this, select the cell with the amount you need and click on the “Decrypt” button. A list of accounts and subaccounts to it will appear, from which this reporting indicator is formed.

Net assets

Net assets are one of the most important indicators that characterize the financial condition of an organization. Not only the assessment of the company’s performance, but sometimes the very existence of the business depends on their amount. Let's look at why net assets are needed and how this indicator is calculated.

What are net assets and how to calculate them

Let's consider this theoretical situation. The owner of the company decided to stop his business. He fired the workers, paid them the settlement, sold the buildings and equipment, sold the remaining raw materials and products (goods), received all accounts receivable, and also fully paid off with suppliers and the budget.

The money that will remain at the disposal of the business owner after all these operations is the net assets (NA) of the company.

The procedure for calculating net assets was approved by order of the Ministry of Finance of the Russian Federation dated August 28, 2014 No. 84n.

NA = (A – DZU) – (O – DBP)

A – company assets (line 1600 of the balance sheet)

DZU – receivables of the founders for contributions to the authorized capital;

О – company liabilities (sum of lines 1400 and 1500 of the balance sheet);

DBP – separate income of future periods.

In practice, situations when it is necessary to use the corrective indicators DZU and DBP are rare. Therefore, in most cases the formula looks like

HA = A - O = page 1600 – page 1400 – page 1500 = page 1300

Those. In general, the company’s net assets are the result of Section III of the balance sheet, “Capital and Reserves.” It consists of:

- Authorized capital (AC).

- Retained earnings (RE).

- Reserve and other similar funds (RF).

- Additional capital

- Amounts of revaluation of non-current assets.

- The value of shares in the management company owned by the company itself.

Most small LLCs usually only use the first three positions, because... They rarely use other types of sources of funds.

CHA = UK + NP + RF = line 1310 + line 1370 + line 1360

What do net assets show?

As can be seen from the previous section, the main factor that affects the value of net assets is retained earnings. After all, changes to the management company rarely occur, and reserve funds are also mainly formed from profits and, moreover, not by all LLCs.

Therefore, an increase in net assets in most cases indicates that the company is operating consistently at a profit. This is a positive factor in assessing a business both for its owners and for external users - counterparties, banks, potential investors.

Each LLC is obliged to calculate its net assets at least once a year and include this information in its financial statements (Clause 3, Article 30 of Law No. 14-FZ dated 02/08/1998).

The law also provides for other situations when it is necessary to take into account the size of net assets. We will talk about this in more detail in the following sections.

Net assets in unprofitable activities

If the company is operating at a loss, then the balance sheet line 1370 may become negative. Therefore, the formula for calculating net assets will take the form

NA = UK + RF – NU (uncovered loss)

If the reserve fund is less than the accumulated loss (or is absent altogether), then the net assets will become less than the authorized capital.

In this case, the management company will no longer be able to perform one of its main functions - to guarantee the company’s counterparties the fulfillment of their obligations to them. After all, after all the calculations, the business owners will actually have at their disposal an amount less than the amount of the authorized capital indicated in the balance sheet.

If the amount of the company’s net assets remains below the authorized capital for two years in a row, then the organization must reduce the authorized capital to the amount of net assets within 6 months. The first year of work “does not count.” Thus, the law gives a new business the opportunity to develop without imposing requirements at the initial stage of activity.

But the Criminal Code can only be reduced to a certain limit. In general, its minimum amount for an LLC is 10 thousand rubles. If net assets fall below this amount, then the owners must decide to liquidate the organization. For this purpose, 6 months are also allotted after the end of the two-year period of reduction in the value of net assets (clause 4 of Article 30 of Law No. 14-FZ).

Net assets in settlements with founders

There are two main situations when an operating LLC makes payments to its members:

- Dividend payment.

- Payment of the actual value of the share when a participant leaves the company.

In both of these cases, the size of net assets must be taken into account.

When the founders intend to use the profit received or part of it to pay dividends, it is necessary, in particular, to comply with the following rules (Article 29 of Law No. 14-FZ):

- The size of net assets should not be less than the sum of the authorized capital and reserve funds at the time of the decision or actual payment.

- The amount of net assets should not fall below this amount after payment of dividends.

A participant who leaves the company must receive a portion of the net assets corresponding to his share. The net asset value is determined based on the financial statements for the previous year.

The rule here is similar to the situation with the payment of dividends. Payment of the actual value of the share should not result in the company's net assets being less than its authorized capital. Otherwise, the organization must first reduce the capital, and only then make settlements with the exiting participant.

Since the law has established restrictions for reducing the authorized capital, the maximum amount that a participant can receive upon leaving the LLC is also limited. It is equal to the difference between the current size of net assets and the minimum size of the capital company (Clause 8, Article 23 of Law No. 14-FZ).

How to quickly increase your net worth

The “normal” way to increase net worth is to make a profit. All retained earnings fall into section III of the balance sheet and “automatically” increase net assets. But what to do if there is no profit, or its amount is not enough?

Then the founders will have to resort to other ways to increase net assets:

- Increase the authorized capital.

- Pay off debt on deposits in the management company.

- Make contributions to the company's property without increasing the authorized capital.

- Conduct a revaluation of assets.

- Write off accounts payable.

The best of the options listed is a contribution to property. It is available to every organization, does not require complex registration and, in most cases, does not entail tax consequences.

An increase in the charter capital requires amendments to the Charter and state registration. Repayment of debt on contributions to the authorized capital is possible only if such debts exist, i.e. This option is not suitable for every company.

The last two methods are also not available to everyone. After all, not every organization has overdue accounts payable or assets for revaluation in sufficient quantities. In addition, when writing off a “creditor”, you will have to pay income tax, and an increase in the value of fixed assets can lead to an increase in the taxable base for property tax.

Conclusion

Net assets are the most important financial indicator, the growth of which indicates the efficient operation of the business. Net assets are generally formed from the authorized capital, reserve funds and retained earnings.

The law does not allow the reduction of net assets to an amount not exceeding the amount of the authorized capital. This rule must be followed both within the framework of current activities and in settlements with the founders.

If the accumulated profit is not enough, then the company owners can invest additional funds in the authorized capital or property of the LLC. Also, the growth of net assets can be achieved through accounting operations: writing off accounts payable and revaluing assets.

The simplest and most profitable way for founders to support a company in order to increase its net assets is to contribute to the company’s property without changing the authorized capital.

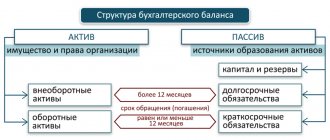

Section 3 refers to the liability side of the balance sheet and contains digital indicators characterizing the capital and reserves of the organization, namely:

· Authorized capital.

· Own shares purchased from shareholders.

· Revaluation of non-current assets.

· Extra capital.

· Reserve capital.

· Retained earnings (uncovered loss).

Authorized capital (share capital, authorized capital, contributions of partners) (line 1310) - indicates the amount of the authorized capital of the organization at the end of the reporting period, fixed in the constituent documents.

The balance sheet indicators on line 1310 do not contain information about changes in capital.

The explanation for line 1310 “Authorized capital (share capital, authorized capital, contributions of partners)” of the balance sheet is the Statement of Changes in Capital.

Please note: The indicator in line 1310 of the balance sheet must correspond to the indicator in the “Authorized Capital” column of the line “Capital Amount as of December 31, 2013.” (line 3300) Statement of changes in capital.

Own shares purchased from shareholders (line 1320) - indicates the amount of the debit balance in account 81 “Own shares (shares)” at the end of the reporting period.

Own shares/shares purchased from shareholders/participants are reflected in the financial statements in the amount of actual costs for their redemption, regardless of the nominal value.

Please note: The indicator in line 1320 of the balance sheet must correspond to the indicator in the column “Own shares purchased from shareholders” of the line “Capital value as of December 31, 2013.” (line 3300) Statement of changes in capital.

This indicator is reflected in parentheses.

Revaluation of non-current assets (line 1340) – the credit balance is indicated in account 83 “Additional capital”, in terms of revaluation of non-current assets, at the end of the reporting period, taking into account the revaluation carried out as of December 31, 2013.

Please note: Revaluation of fixed assets is carried out by recalculating their residual or current (replacement) value (if this object was revalued previously), and the amount of depreciation accrued for the entire period of use of the object (clause 15 of PBU 6/01).

Revaluation of intangible assets is carried out by recalculating their residual value (clause 19 of PBU 14/2007).

Additional capital (without revaluation) (line 1350) – indicates the amount of the credit balance in account 83 “Additional capital” at the end of the reporting period, minus the amount of the credit balance formed in connection with the revaluation of assets.

Amounts of additional capital include, for example, the excess of the selling price of shares/shares over their nominal value.

Reserve capital (line 1360) – indicates the amount of the organization’s reserve capital at the end of the reporting period.

This line reflects the amounts of reserve (and other) funds formed in accordance with the constituent documents and provisions of the current legislation.

In accordance with clause 1 of Article 30 of Law No. 14-FZ “On Limited Liability Companies”, the Company may create a reserve fund and other funds in the manner and in the amounts established by the company’s charter.

In accordance with clause 1 of Article 35 No. 208-FZ “On Joint-Stock Companies,” a reserve fund is created in the company in the amount provided for by the company’s charter, but not less than 5 percent of its authorized capital.

The reserve fund of the company is formed through mandatory annual contributions until it reaches the size established by the charter of the company.

The amount of annual contributions is provided for by the company's charter, but cannot be less than 5 percent of net profit until the amount established by the company's charter is reached.

The company's reserve fund is intended to cover its losses, as well as to repay the company's bonds and repurchase the company's shares in the absence of other funds.

The reserve fund cannot be used for other purposes.

We recommend that the procedure for creating reserve (and other) funds, as well as the procedure for contributions to these funds, be fixed in the accounting policy for accounting purposes and reflected in the explanatory note to the statements.

Please note: The indicator in line 1360 of the balance sheet must correspond to the indicator in the “Reserve capital” column of the line “Capital value as of December 31, 2013.” (line 3300) Statement of changes in capital.

Retained earnings (uncovered loss) (line 1370) – indicates the amount of retained earnings (uncovered losses) reflected at the end of the year in account 84 “Retained earnings (uncovered loss)”.

Please note: The indicator in line 1370 of the balance sheet must correspond to the indicator in the column “Retained earnings (uncovered loss)” of the line “Capital value as of December 31, 2013.” (line 3300) Statement of changes in capital.

The indicator on line 1370 is indicated without brackets if the balance is positive (when reflecting retained earnings) and in parentheses if the result is negative (when reflecting uncovered losses).

Total for section III (line 1300) – indicates the total amount of the organization’s equity capital at the end of the reporting period.

Line 1300 = line 1310 + line 1320 + line 1340 + line 1350 + line 1360 + line 1370.

Please note: The indicator in line 1300 of the balance sheet must correspond to the indicator in the “TOTAL” column of the line “Capital value as of December 31, 2013.” (line 3300) Statement of changes in capital.

In the article we will determine which property, material and monetary values of an economic entity can be classified as net assets. We will provide a calculation formula and tell you how to analyze and improve the indicators.

Formation of the organization's reserve capital

Reserve capital is a form of insurance that increases the guarantee of liability to third parties. The source of formation of reserve capital is the retained earnings of the enterprise. Less often, the source of creation of the Republic of Kazakhstan is the property of the founders. Contributions from founders in the form of property are not taxed, while the monetary form of replenishment of net assets is recognized as income. Reserve capital in an LLC may not be formed. There is no obligation to create an RK in the LLC Law. Contributions to the fund are made voluntarily, the amount is fixed in the Charter.

Unlike LLCs, joint stock companies are required to contribute to the fund an amount of at least 5% of net profit. The fund's funds accumulate over several periods. Organizations forced to use funds to cover losses or repurchase their own shares must cover the amount spent in the next period.

Net assets of the enterprise on the balance sheet

The cost of NA is calculated based on the results of the reporting period - a year or intermediate periods - a quarter, half a year, 9 months. The determination of net assets on the balance sheet is made by subtracting the debts of the liability section from the asset, applying adjustments to off-balance sheet accounts, debts of the founders/shareholders and income for future periods.

The calculation formula was approved by the Ministry of Finance of the Russian Federation in order No. 84n dated August 28, 2014 and is described in detail in a separate article. To calculate the size of an organization's net assets according to financial statements, the following mathematical algorithm is used:

NA = (line 1600 – Debts of the founders as part of receivables) – (line 1400 + line 1500 – Income of future reporting periods).

The net asset indicator is entered into the form for calculating the value of the net assets developed by the enterprise. It is allowed to use the form approved by the Ministry of Finance and the Federal Securities Commission in order No. 10n dated January 29, 2003. The result obtained may be positive or not. Negative net assets indicate unprofitable operations and possible insolvency of the company in the near future; they show the complete dependence of the business on external investments and loans. The exception is newly opened companies that have not yet received income.

Important! Repeated reductions in the level of asset capital below the limit value (size of authorized capital) may become a prerequisite for the forced liquidation of the enterprise in accordance with the requirements of Law No. 208-FZ of December 26, 1995 (Article 35, paragraph 11).

Income statement

The financial performance statement is intended to reflect information about the income and expenses of the organization. It is compiled based on the results of the reporting period and for the same period of the previous year.

| Indicator name | Line code | What is reflected | Reflection order |

| Revenue | 2110 | Revenue from the sale of products, goods, works and services | Credit turnover on account 90 (subaccount 90-1 “Revenue”) - Debit turnover on account 90 (subaccounts: 90-3 “VAT”, 90-4 “Excise taxes”) |

| Expenses for ordinary activities | 2120 | Expenses associated with the production and sale of products, goods, works and services | Debit turnover on account 90 (sub-account 90-2 “Cost of sales”) |

| Percentage to be paid | 2330 | Expenses in the form of accrued interest payable | Debit turnover on account 91 (subaccount 91-2 “Other expenses” in terms of interest paid) |

| Other income | 2340 | Income from participation in other organizations, interest receivable and other income | Credit turnover on account 91 (subaccount 91-1 “Other income”) - Debit turnover on account 91 (subaccount 91-2 “Other expenses” in terms of VAT, excise taxes and other similar payments) |

| other expenses | 2350 | Other expenses not reflected in other lines of this form | Debit turnover on account 91 (subaccount 91-1 “Other income”) - Debit turnover on account 91 (subaccount 91-2 “Other expenses” in terms of VAT, excise taxes and other similar payments) |

| Profit taxes (income) | 2410 | The amount of income tax accrued for payment to the budget or a single tax paid under the simplified tax system | (Credit turnover – Debit turnover) on account 68 (sub-account “Calculations for current income tax” or “Calculations for single tax”) |

| Net income (loss) | 2400 | Profit (loss) remaining at the disposal of the organization | Turnover on account 99 in correspondence with account 84 line 2400 = line 2110 – line 2120 – line. 2330 + page 2340 – page 2350 – page 2410 (calculated automatically) |

Net assets of a joint stock company

Net assets in the balance sheet of the joint-stock company, line 3600 section. 3 statements of changes in capital are calculated according to the formula used by LLCs and enterprises of other forms of ownership. Joint-stock companies calculate the NAV before paying dividends to shareholders, when a shareholder leaves the business, to determine the ratio between the authorized capital and the amount of net assets, in the case of purchasing placed shares or when repurchasing shares owned by the company.

What is a comparative analytical balance sheet of net assets?

A similar analysis is carried out to study the dynamics of changes in the financial condition of the enterprise. At the same time, absolute and specific ratios are calculated at the beginning/end of the reporting period for individual indicators and the overall picture of the state of affairs in the organization is determined. The calculations use various indicators, formulas and coefficients. For example, the method for determining the value of own working capital (SOC):

SOS = Own sources (section 4 of the balance sheet) – Non-current assets (section 1 of the balance sheet).

Conclusion - to find out where the net assets are on the balance sheet, it is necessary to calculate the amount of the company's own funds, not encumbered with liabilities. The cost is determined in monetary terms as of the latest reporting date based on accounting data.

Line 1300 balance

Indicator analysis

NA must be calculated to record the current financial condition of the enterprise. By studying their value, the owners draw conclusions about the efficiency and productivity of the business and make decisions on further investment or withdrawal of their funds. Net assets in the balance sheet, line 3600, demonstrate to the owners how profitable their cash investments and the institution's equity capital are.

NA is extremely necessary for analyzing financial and economic activities. They are also taken into account when paying dividends. NA must be positive, and their indicator must exceed the size of the authorized capital. When their value grows, management can conclude that the organization’s profits are growing.

Negative net assets can be observed in the first year of the enterprise’s operation - the most difficult period for operation, when the NAV can decrease and be significantly lower than the invested capital. In the case when an enterprise has been operating for a long period of time, and the NAV is negative, this indicates that the organization is operating ineffectively and investments are not profitable.

An increase in net assets is associated either with a change in their value (for example, revaluation of fixed assets) or with a change in the value of liabilities. Also, the increase in the NAV is made due to additional investments of the founders when additional capital is used.

What accounting data is used. when filling out line 1300 “Capital and reserves”

commercial organizations - small businesses are not entitled to use simplified methods of accounting if they are microfinance organizations or their financial statements are subject to mandatory audit (clause 1, 4, part 5, article 6 of Law No. 402-FZ).

The procedure for filling out this line by small businesses does not differ from the generally established procedure for filling out line 1410 “Borrowed funds” section. IV Balance Sheet, the form of which is given in Appendix No. 1 to Order of the Ministry of Finance of Russia No. 66n.

For information about what obligations of the organization are taken into account as part of borrowed funds, how their value is determined and what accounting data is used when filling out line 1410 “Borrowed funds”, see section. 3.1.4.1 “Line 1410 “Borrowed funds”.

For an example of filling out line 1410 “Borrowed funds”, see section. 3.1.4.1.4.

3.6.1.9. Line “Other long-term liabilities”

On this line, small business organizations reflect all long-term liabilities existing as of the reporting date (with the exception of those reflected on line 1410 of long-term borrowed liabilities). Long-term obligations are understood as obligations whose maturity exceeds 12 months after the reporting date (clause 19 of PBU 4/99).

Attention!

Small business organizations (with the exception of issuers of publicly offered securities) have the right not to apply the Accounting Regulations “Estimated Liabilities, Contingent Liabilities and Contingent Assets” (PBU 8/2010) and the Accounting Regulations “Accounting for Income Tax Calculations of Organizations” » PBU 18/02. If an organization uses this right, then estimated liabilities and deferred tax liabilities are not recognized in its accounting.

From November 16, 2014, commercial organizations - small businesses are not entitled to use simplified methods of accounting if they are microfinance organizations or their financial statements are subject to mandatory audit (clause 1, 4, part 5, article 6 of Law No. 402 -FZ).

Date added: 2016-03-15; ;

Accounting statements of small businesses 2021: sample

Let’s fill out the reporting of a small enterprise, LLC Giatsint, which uses the simplified tax system “Income” using the example:

The company's balance sheet for the year:

| Balance at the beginning of the period | Closing balance | |||||

Let’s assume that the interest paid for the loan amounted to 5,000 thousand rubles, the company had no other expenses, and the calculated tax according to the simplified tax system amounted to 69,000 thousand rubles.

Let's look at filling out simplified financial statements for 2017. Observing the principle of equivalence of both parts, we enter the values in the lines:

| Account balance | |

| D/t (01 + 08) – K/t 02 | 400000 + 157000 – 240000 = 317000 |

| D/t (10 + 41 +44) | 18000 + 61000 + 5100 = 84100 |

| D/t (50 + 51 + 52) | 42200+ 292600 + 50000 = 384800 |

| D/t (62 + 71 + 76) | 111900 + 67000 = 178900 |

| Asset Line Sum | 317000 + 85000 + 84100 + 384800 + 178900 = 1049800 |

| K/t (80 + 82 + 83 + 84) | 500000 + 23000 + 32000 + 202600 = 757600 |

| K/t (60 + 68 + 69+ 70) | 9500 + 30000 + 30000 + 57700 = 127200 |

| Sum of liability lines | 757600 + 165000 + 127200 = 1049800 |

The second form of simplified accounting financial statements, a sample of which is presented, is the OFR. The algorithm for filling it in the table:

| What is it made up of? |

- Purpose of the article: displaying the state of the authorized capital (share capital, authorized capital) of a legal entity at the end of the reporting period.

- Line in the balance sheet: 1310.

- Account numbers included in the line: account credit balance. .

The authorized capital of a legal entity is the initial provision of the organization’s activities by contributing funds (property, securities) by owners or shareholders.

Note from the author!

The size of the authorized capital undergoes the procedure of official state registration and is displayed in the constituent documentation of the company; the data in the financial statements and documents must be identical.

Depending on the organizational and legal form of legal entities, a certain procedure for the formation of the initial property of the organization is established:

- JSC: authorized capital - the nominal value of shares purchased by shareholders.

The minimum amount for a public joint stock company is 100 thousand rubles, a non-public company is 10 thousand rubles. - LLC: authorized capital - the initial amount of funds contributed by the founders.

Minimum amount: 10 thousand rubles, funds must be deposited within 4 months from the date of state registration of the company.Note from the author!

The initial deposit can be formed not only in cash, but also in tangible assets (fixed assets, goods, etc.), securities. When making a contribution with property, its value must be assessed by an independent appraiser.

- State and municipal unitary enterprises: the formed fund is the minimum amount of initial property that ensures the interests of potential creditors of the organization.

The minimum amount of the fund for a government institution: not less than 5,000 minimum wages established by the government on the date of registration.The minimum amount of the fund for municipal enterprises: not less than 1000 minimum wages established by the government on the date of registration.

Note from the author!

From January 1, 2021, the Federal Law established the minimum wage at 9,489 rubles. Regions have the right to apply federal laws to determine the minimum wage for employees. From May 1, 2021, the minimum wage will be 11,163 rubles.

Line 1310 of the balance sheet of the financial statements belongs to the Capital and liability reserves section of the balance sheet: information on the state of the authorized capital of the organization as of December 31 of the current year, the previous year and the previous one is displayed here. The data must completely match the registered constituent documentation.

Note!

In the financial statements, the amount of the authorized capital is reflected in full, regardless of whether it has been paid at the moment.

What accounting data is used. when filling out line 1300 “Capital and reserves”

when filling out line 1300 “Capital and reserves”

When filling out the line “Capital and reserves”, data on credit balances on accounts 80, 82, 83, debit balance on account 81, balance on account 84 as of the reporting date can be used.

┌───────────────────────┐ ┌─────────────────┐ ┌─────────┐ ┌─────────┐

│Line 1300 “Capital and │ │Credit balances│ │Debit│ │Balance by│

│reserves" of Accounting│ = │accounts 80, 82,│ - │balance on│ + │account 84 │

│balance │ │83 │ │account 81 │ — │ │

└───────────────────────┘ └─────────────────┘ └─────────┘ └─────────┘

The comparative indicators of the line “Capital and reserves” (indicators as of December 31 of the previous year and as of December 31 of the year preceding the previous one) are transferred from the Balance Sheet for the previous year.

For reference: Small businesses may not perform a retrospective recalculation of comparative indicators of financial statements...

Small businesses (except for issuers of publicly offered securities) may not perform a retrospective recalculation of comparative financial statements. These organizations have the right to reflect the consequences of changes in accounting policies prospectively, except in cases where a different procedure is established by the legislation of the Russian Federation and (or) the regulatory legal act on accounting (clause 15.1 of PBU 1/2008).

Retrospective recalculation of comparative indicators of financial statements is not carried out by such organizations even in the case of correction of errors of previous years identified after the approval of the financial statements for the reporting year in which the errors were made (clauses 9, 14 of PBU 22/2010).

From November 16, 2014, simplified methods of accounting, including simplified financial statements, are not entitled to be used by commercial organizations - small businesses if they are microfinance organizations or their accounting statements are subject to mandatory audit (clause 1, 4, part 5 Article 6 of Law No. 402-FZ).

Filling example

lines 1300 “Capital and reserves”

EXAMPLE 27

Indicators for accounts 80, 82, 83 and 84 in the accounting of an organization - a small business entity (indicator for account 81 is missing):

rub.

| Index | As of the reporting date (December 31, 2014) |

| 1 | 2 |

| 1. On account credit 80 | 10 000 |

| 2. On the credit of account 82 | 2000 |

| 3. On the credit of account 83 | 450 000 |

| 4. On the credit of account 84 | 27 218 157 |

Fragment of the Balance Sheet for 2013

| Indicator name | Code | As of December 31, 2013 | As of December 31, 2012 | As of December 31, 2011 |

| 1 | 2 | 3 | 4 | 5 |

| Capital and reserves | 1300 | 27 190 | 22 471 | 15 640 |

Solution

The indicator for line 1300 “Capital and reserves” is equal to:

as of December 31, 2014 - RUB 27,680 thousand. (RUB 10,000 + RUB 2,000 + RUB 450,000 + RUB 27,218,157);

as of December 31, 2013 - RUB 27,190 thousand;

as of December 31, 2012 - RUB 22,471 thousand.

A fragment of the Balance Sheet in Example 27 will look like this.

| Indicator name | Code | As of December 31, 2014 | As of December 31, 2013 | As of December 31, 2012 |

| Capital and reserves | 27 680 | 27 190 | 22 471 |

3.6.1.8. Line 1410 “Long-term borrowed funds”

For this line, small business organizations reflect information on long-term loans and borrowings attracted by the organization (the repayment period of which as of the reporting date exceeds 12 months) (paragraph 2, paragraph 17 of PBU 15/2008, paragraphs 19, 20 of PBU 4 /99).

Attention!

If the repayment period of borrowed funds previously presented in the Balance Sheet as long-term liabilities is less than 12 months at the reporting date, these liabilities are presented as short-term (Letter of the Ministry of Finance of Russia dated January 28, 2010 N 07-02-18/01).

Attention!

Small businesses, with the exception of issuers of publicly placed securities, have the right to recognize all borrowing costs as other expenses (clause 7 of PBU 15/2008). However, this rule does not affect the procedure for determining interest debt reflected in the Balance Sheet as part of the indicator in line 1410 “Long-term borrowed funds” or line 1510 “Short-term borrowed funds.”

Since November 16, 2014

Requirements for filling out a simplified balance sheet

The annual balance sheet must contain data on the assets and liabilities that the organization has at the end of the reporting year, that is, as of December 31. Additionally, information on previous years is entered into the balance sheet, that is, as of December 31 of last year and as of December 31 of the year before. For example, the balance sheet prepared by an enterprise for 2021 must contain data as of December 31, 2017, December 31, 2021 and December 31, 2015.

All last year's information is taken from last year's reports. And for indicators for the current year, information is taken from sources such as:

- The balance sheet for the organization as a whole for the reporting year;

- Indicators of accrued interest on credits (loans) for the reporting year.

If there is no data to fill out any balance line, it is not filled in and a dash is placed.

Simplified balance sheet

At the same time, small businesses can choose the form for preparing financial statements independently. They can provide reporting using both general and simplified forms. The composition of the reporting will depend on this. Thus, for small enterprises, special forms of simplified financial statements have been approved, given in Appendix 5 of Order No. 66n of the Ministry of Finance of Russia dated July 2, 2010. The composition of simplified financial statements is as follows:

- Balance sheet;

- Income statement.

If an enterprise needs to provide any additional information, and the simplified reporting forms do not contain the required columns, then general reporting forms can be used.

Thus, small businesses decide on their own which forms to submit financial statements. The main thing is that the decision made is reflected in the accounting policy.