When to check

An order is usually drawn up by order of the manager in a planned or unscheduled manner. The person responsible for this is the chief accountant or another accounting employee, and if he is ill or absent, a person authorized to maintain accounting records.

Inventory is required in several cases (clause 27 of Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n):

- before preparing annual reports (you will need to inventory all assets and liabilities);

- when changing financially responsible persons, including those associated with the transfer of property to third parties;

- after emergency situations - fires, floods, other disasters;

- upon detection of theft or damage to property.

Inventory schedule - sample

The legislation gives the management of the enterprise the right to independently determine the frequency of inventory checks. Their frequency reflects the inventory schedule and a separate item in the accounting policy. The exception is cases of mandatory unscheduled recalculation of values:

- during reorganization activities;

- when the liquidation of the organization has begun;

- when assessing the consequences of emergency situations;

- conducting an inventory is necessary to confirm the fact of theft or damage to property;

- preparation of annual reports;

- the inventory procedure must also be observed in the event of changes in the composition of financially responsible persons;

- inspection of property on the eve of their transfer to third parties for a fee or free of charge.

If there is a large volume of inventory items, it is advisable to draw up an inventory plan, a sample of which will help optimize the work of the members of the inventory commission. The inventory schedule includes mandatory information about:

- The list of objects subject to verification and recalculation,

- The composition of the inventory commission by name.

- Timing of audit actions indicating their frequency.

There is no sample inventory schedule approved by law. Its form is developed by the chief accountant. The document must contain the signature of the head of the institution approving the audit plan.

Inventory when preparing annual reports

The procedure, timing and list of objects are established in the accounting policy. On its basis, a sample inventory order is prepared annually before the annual report. List in it the composition of the commission, the name of the assets and liabilities being inventoried, the start and end dates, and state the reason:

the need to prepare annual financial statements.

How to draw up an inventory report?

Before the inspection, you need to select the form of the act and establish the exact composition of the commission. Next comes only calculations and comparisons.

Form

The act is drawn up strictly in writing. Usually they use a ready-made electronic form in *xlm format. All you need to do is enter the required values into Excel and it will produce a sample for printing. It is also possible to fill out the A4 sheet by hand.

The form of the act on the results of the inventory depends on the type of valuables. There is no universal and unified template for all assets and liabilities of the company - by virtue of clause 1.2 of Resolution of the State Statistics Committee No. 88 of August 18, 1998.

For example, if you need to calculate fixed assets, the INV-1 act form is used. For intangible assets (trademark, licenses), form INV-1a should be prepared. Goods are entered into the INV-3 form, and precious metals into the INV-8 form. Even for debts and obligations of the company, a separate form is provided - IVN-17.

If the situation requires it, responsible persons can make new items or changes to the unified form. In this case, it is prohibited to delete document details (but you can add new lines in the form).

Content

The selected form must be filled out:

- “Document header” – name of the organization, OKUD and OKPO codes, start and end dates of the inventory process, as well as details of the basis document (order, resolution or regulation), details of the order on its appointment and the period of the inventory;

- The main part is to note the type of assets (inventory, cash, precious metals, accounts receivable), their location (office, warehouse, workshop), quantity or cost;

- Full name of financially responsible persons, for example, chief accountant, warehouse manager, etc.

- Inventory results;

- Full names and positions of commission members + signatures with their transcripts;

- Date and year of the event.

The report on the results of the inspection is drawn up in 2 copies - both are certified by an expert commission. One will go to the accounting records, and the second will remain with the financially responsible person. Subsequently, it will be possible to raise the verification data at any time.

How to draw up an order for inspection using form No. INV-22

Resolution of the State Statistics Committee of Russia dated August 18, 1998 No. 88 approved form No. INV-22 - on its basis, a sample order for conducting an inventory 2021 was prepared. Form INV-22 must be used regardless of what the proceedings are related to, whether it is full or partial, whether it was planned in advance or carried out unexpectedly.

The order contains:

- the specific purpose of the conduct is an inventory of goods, fixed assets, assets, receivables, and all property;

- listing the divisions of the organization where the inspection will be carried out, for example, only in a warehouse or in another department, throughout the company;

- period and duration of the event - from what date to what date, when to provide the results of verification actions;

- composition of the commission, including full name its chairman - it is allowed to include not only company employees capable of assessing the state of property and liabilities, but also third-party auditors;

- information about the order: its date, number, information about the manager who signed the order.

Once the establishing document has been prepared, it must be recorded in a journal to record control over the implementation of such decisions. Take the corresponding register form from Goskomstat Resolution No. 88 - form No. INV-23. This is not necessary; companies are allowed to develop their own version of the magazine, but for convenience, use the template proposed by officials.

It is important that all employees listed in it are familiar with the order. They place their signatures directly on the sheet containing data on the upcoming inspection, or on a separate sheet for familiarization with the document, which is filed with the order.

The intention to compare goods, inventories, and valuables on paper and in reality must be notified and signed by the financially responsible persons of the department where the reconciliation is being carried out.

General rules for conducting inventory

Clause 2 of the Methodological Instructions of Order No. 49 of the Ministry of Finance reveals the rules for conducting inventory. They apply to:

- the responsibility of enterprise management to determine the frequency of inspections;

- aspects of the formation of the commission;

- inventory regulations;

- documentation of the audit results.

The procedure for conducting an inventory involves issuing an order to form a commission. It should include representatives of:

- administrative department;

- accounting employees;

- employees attracted from other departments.

Inventory rules prohibit inspections in the absence of even one of the commission members. It is also mandatory that all involved persons familiarize themselves with the data from reports on the movement of material assets and monetary resources, as well as receipt and expenditure documentation.

How to conduct an inventory - with or without the participation of financially responsible persons? The presence of this category of employees is mandatory. Before the start of audit activities, they give a receipt for the completion of operations to document the movement of property. The procedure for carrying out an inventory at an enterprise involves a piecewise count of all valuables; if necessary, they must be weighed and measured.

If the audit extends over several days, the premises with the assets being inspected are sealed. The inventory schedule, a sample of which you will find below, should allow sufficient time for summing up the results of the inspection and documenting them. The results of the audit are entered into the inventory manually or using office equipment. The document form is signed by all participants in the verification process - members of the commission and financially responsible persons.

Example: how to draw up an order for an inventory of material assets (2021 sample)

Step 1. In the appropriate fields, enter the name of the organization (IP), indicate OKPO, specify the order number and the date of its preparation.

Step 2. manta, specifying what event is being held and which of the employees is participating in it: the order for inventory contains the full name. employees, but when listing it is allowed to abbreviate their names and patronymics.

Step 3. We indicate what needs to be checked and in which department, we explain the reasons why it is necessary to compare real stocks, valuables, goods and those indicated in the documents. In our case, an example of the reason for inventory in the order contains the wording:

Detection of the theft of valuables from a warehouse by a security guard.

At the same time, we enter the start and end dates of the property condition analysis procedure.

Step 4. The last thing is to determine the last date for submitting the report based on the results of the reconciliation, and sign it with the manager who appointed the inspection.

This is what a completed order looks like.

Drawing up an order in any form

The order can also be drawn up in any form. But there is a list of information and details that must be indicated in an official document:

- company name;

- date of preparation and document number;

- objects and purpose of the inspection;

- list of departments involved;

- period;

- deadlines for providing results;

- composition of the commission indicating the last names, first names, patronymics and positions of each of its members;

- last name, first name, patronymic and signature of the manager.

Inventory and registration of its results

The verification consists of comparing and contrasting the actual volumes of values with those recorded in the primary documents. Therefore, first, the commission members get acquainted with the inventories of existing valuables, goods, and supplies. They then compare the property on hand to what is on paper.

At the end of the counting and comparison procedure, the commission members draw up documents containing the results of the inspection. Most often this is not one document, but several. Thus, the identified discrepancies are recorded in the results sheet. As a template for such a document, use form No. INV-26 from Goskomstat Resolution No. 26 dated March 27, 2000.

Documents for recording the results of the inventory are drawn up after it is completed. For example, if your organization carried out an inventory before drawing up annual reports in December 2019, then you are allowed to draw up documents based on its results as early as January 2021. If a discrepancy is identified between the actual data and accounting data, then they must be recorded in the reconciliation statement. A separate comparison sheet is drawn up for objects in custody or leased objects.

The accountant draws up a matching statement in two copies. One of them will remain in the accounting department, the second will be transferred to the financially responsible person.

Later, the results are discussed at a special meeting of the permanent inventory commission, which is the basis for drawing up a protocol. There is no approved form for the protocol, so the main requirements are to correctly indicate the data from the order on the initiation of control measures, about the members of the commission, and the discrepancies identified. If there are no discrepancies, this must be documented. At the same time, the commission puts forward proposals to capitalize, write off the identified surpluses (deficiencies), and reflect them on the balance sheet. In addition, it is permissible to record other initiatives in the protocol, for example, to strengthen security in order to avoid theft in the future. So, the list of final documents contains the following documents:

- a statement of records of the results identified by the inventory;

- comparison sheet of inventory results;

- a comparative statement of the results of the inventory of valuables owned by the organization;

- a comparative statement of the results of the inventory of rented objects;

- inventory list;

- explanatory letter.

Inventory commission

2.1. The organization has a permanent inventory commission throughout the year. During the period of planned inventories, working inventory commissions are created. The personnel of all inventory commissions is approved by order of the head.

2.2. The permanent inventory commission summarizes the work of the working inventory commissions and provides management with the results of the inventories (about misgrading, about stocks that have partially lost their original quality, about unused material assets, etc.).

The permanent inventory commission includes: the chairman of the commission - the executive director, members of the commission - an internal auditor, an accountant of the material group, the head of the technical department, and a personnel manager.

2.3. The permanent inventory commission performs the following functions:

- organizing inventories by working inventory commissions;

- instructing members of working inventory commissions;

- carrying out control checks of the correctness of inventories by working inventory commissions;

- checking the validity of the conclusions based on the results of inventories of working inventory commissions, including in relation to the proposed offsets for misgrading;

- Carrying out, in necessary cases (if serious violations of the rules for conducting inventories, etc.) are established, repeated complete inventories;

- consideration of explanations from officials who committed shortages or damage to material assets, as well as other violations, and provision of proposals on the procedure for regulating identified shortages, losses from damage and other deviations;

- carrying out preventive work to ensure the safety of property;

- carrying out an inventory of the organization’s assets and liabilities, including conducting selective inventories of material assets in places of their storage (processing);

- summarizing and submitting inventory results for approval to the manager;

- making proposals and additions to these Regulations.

2.4. The working inventory commission provides a natural count (actual availability) of property (liabilities), checks their condition and draws up inventory lists for each type of inventory property (liabilities). Working inventory commissions are created for the period of planned inventories.

The operating procedure of working inventory commissions (including objects and types of inventory, the number of commissions, the number of members, personnel, appointment of the chairman of the commission) is determined by the head of the organization in agreement with the chairman of the permanent inventory commission.

2.5. The competence of working inventory commissions includes:

- conducting an inventory of assets and liabilities in all divisions of the organization;

- analysis of inventory results and development of proposals, including the offset of shortages and surpluses by re-grading, write-off of shortages within the limits of natural loss (together with accounting);

- preparation of proposals to improve the procedure for acceptance, storage and release of material assets, accounting and control of their safety.

2.6. All inventory commissions are responsible for compliance with the timing and procedure for conducting an inventory, the timeliness and correctness of execution of inventory documents (including for the completeness and accuracy of indications in the inventory list (act) of the distinctive features and actual balances of the material assets being inspected).

2.7. Financially responsible persons are not members of the inventory commission on their site and are present when checking the actual presence of property on it (clause 2.8 of the Inventory Guidelines).

2.8. By order of the head of the organization, representatives of an independent audit organization may be present during the inventory (clause 2.3 of the Inventory Guidelines).

2.9. Before the start of the inventory, the chairman of each inventory commission:

- provides the commission and financially responsible persons with forms of inventory records (acts) prepared for inventory objects, financially responsible persons and storage locations;

- seals property storage areas that have separate entrances and exits;

- checks the serviceability of weighing instruments used for the work of the commission during the inventory process, and compliance with the established deadlines for their verification;

- receives the latest incoming and outgoing documents at the time of inventory on the movement of property subject to inventory, and endorses them (paragraph 1, 2, clause 2.4 of the Methodological Instructions for Inventory);

- receives a receipt from financially responsible persons in the relevant inventory records (acts) (paragraph 3, clause 2.4 of the Methodological Instructions for Inventory).

Summarizing

After the commission has completed the inventory, a meeting is held. During it, the main results and identified discrepancies are determined. At the same time, the cause of the discrepancies and ways to correct the situation are determined. Based on the results, minutes of the meeting are drawn up. Typically this document has the following structure:

- name of the company indicating the organizational and legal form;

- the name of the unit where the inventory was carried out;

- name of the document - protocol of the inventory commission;

- list of commission members indicating surnames, initials and positions;

- description of the test results;

- list of speakers at the meeting;

- decision;

- conclusion of the commission;

- identified violations (if any);

- those responsible for the violation, indicating their surnames, initials and positions;

- information about measures to eliminate violations;

- signatures of the chairman and all members of the commission;

- applications.

As an illustration, we will give a variant of the protocol.

To easily draw up such a document, prepare the minutes of the meeting attached to the article.

The following documents are attached as appendices to the minutes of the meeting:

- acts and inventories of the inventory carried out according to INV forms for each materially responsible employee, facility, warehouse or division;

- list of products unsuitable for further use;

- a list of missing or excess products with an indication of price;

- explanatory notes from financially responsible employees or other officials.

We would like to add that at the meeting the commission must make the following proposals:

- on the timing and methods of eliminating shortages, on conducting internal investigations (if a shortage is detected);

- on the continued use of outdated and unsuitable products for subsequent use;

- other proposals regarding work with inventory items.

If no violations were found during the inspection, then there is no need to draw up an inventory protocol.

Based on such a protocol, the manager issues an order based on the results of the inventory.

Control activities

3.1. Control checks are carried out upon completion of the inventory, but always before the opening of the premises in which the inventory was carried out.

Control checks are carried out by a permanent inventory commission in the presence of members of working inventory commissions and financially responsible persons (clause 2.15 of the Inventory Guidelines).

Objects and types of inventory during control checks are established by the head of the organization based on proposals from the chairman of the permanent inventory commission.

3.2. Unscheduled (sudden) sample inventories are carried out throughout the year in relation to valuables in the cash register and inventories in places of their storage.

Unscheduled sample inventories are carried out by a permanent inventory commission on the orders of the head of the organization (clause 2.16 of the Inventory Guidelines).

The following frequency of unscheduled sample inventories is established:

| Inventory object | Periodicity |

| Inventories | One to three times a year |

| Cash desk (cash, strict reporting document forms) | Two to four times a year |

The timing of unscheduled selective inventories, the types of inventoried inventories, and valuables stored in the cash register are approved by the head of the organization at the proposal of the chairman of the permanent inventory commission.

Order based on inventory results

This document necessarily reflects the “reaction” of management to the proposals of the commission members and specific instructions on what needs to be done: conduct an additional inspection, punish the perpetrators, introduce additional security measures. The manager sometimes reserves control over the execution of orders. Let's take a closer look at the structure of the order. It, like a similar administrative document, is drawn up according to certain rules. Its structure must contain the following points:

- name of the organization and its legal form;

- details (it is convenient to use a letterhead);

- date and order number;

- preamble, which lists all the documents regulating the inventory (inventory acts, matching and accounting statements, audit protocol);

- order part.

The last part of the order reflects the following points:

- the results of the inspection are subject to approval;

- it is necessary to indicate the requirement to resolve discrepancies identified during the inventory and recorded in the relevant documents;

- an employee is appointed, usually from the accounting department, who is responsible for fulfilling the requirements of this order related to the elimination of discrepancies previously identified during the audit;

- an employee is appointed responsible for monitoring the implementation of the orders recorded in the provisions of the order on summing up the results.

After the order is signed by the first person of the company, the form is handed over to the responsible employee who is authorized to familiarize the designated employees with the provisions of the order against signature.

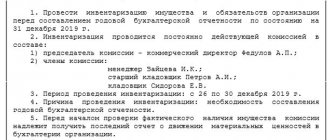

Sample order for inventory

ORDER

On conducting an inventory and analysis of the state of the educational fund of MBOU Secondary School No. 32

In order to monitor compliance with accounting, ensure storage conditions for the library fund of MBOU Secondary School No. 32, as well as on the basis of the Protocol of instructions following the meeting of heads of educational institutions of the city of Krka dated October 13, 2018, I ORDER: 1. Conduct an inventory and analysis of the state of the library fund of MBOU Secondary school No. 32 from October 19, 2021 to October 26, 2021. 2. To carry out the inventory, create a commission consisting of: Chairman - Mikhailova M.M., Deputy Director for Water Resources Management Members of the commission: Borisova B.B. Head of the library, Petrova P.P. chief accountant, Ivanova I.I. leading accountant. 3. The Inventory Commission shall conduct a complete inventory of the institution’s library collection. 4. The commission shall draw up an act based on the results of the inventory and provide a report on the results of the inspection by October 30, 2018. 5. I reserve control over the execution of the order.

Director Vasilyeva V.V.