How to create a tax accounting register

To use tax accounting registers, you will have to spend time developing their form, and then consolidate them in the annex to the accounting policy by issuing the appropriate order (paragraph 7 of article 314 of the Tax Code of the Russian Federation).

Read about the nuances of developing a tax accounting policy in the article “How to draw up an organization’s tax policy?” .

The legislator does not limit taxpayers in choosing the type and form of these documents, so tax accounting registers may look different. The volume of information contained in them should give an idea of the basis on which documents and how the tax base is formed. The placement of data in the register can be any (in tabular or text form) - these features are provided for when developing tax accounting register forms.

The only thing you cannot be proactive about when preparing tax registers is the required details. Their composition must comply with the Tax Code of the Russian Federation. For example, when calculating income tax, tax accounting registers containing the following information are used (paragraph 10, article 313 of the Tax Code of the Russian Federation):

- register name;

- date of compilation;

- natural (if possible) and monetary measures of the operation;

- name of accounting objects or business transactions;

- signature of the person responsible for compiling the register and its decoding.

Such registers can be maintained in any way convenient for the taxpayer: on paper or electronically.

What tax registers exist for VAT? See the answer to this question in the Ready-made solution from ConsultantPlus. If you don't have access to the system, get a free trial online.

What are accounting registers and why are they needed?

The activities of enterprises, especially large ones, directly depend on competent control of financial flows, as well as on monitoring the final balance of the enterprise. This is exactly what accounting does: without its work, it would be extremely difficult for enterprises of all sizes to develop.

In addition, even if the head of an enterprise would like to do without such financial self-control, according to Federal Law No. 402 of December 6, 2011, legal entities are required to send data on balance sheets, debts, etc. to the Federal Tax Service. Taken together, this means that it is simply impossible to circumvent the accounting requirement, but this is also not unnecessary bureaucratization, because self-control contributes to the growth of the enterprise.

The answer to the main question - what are accounting registers in simple words - sounds like this: it is a means of systematizing accounting data . They look like counting tables, constructed in such a way that the existing balance sheet and sources of assets and liabilities are clear.

With the help of registers, the alienation of rights to any property in the company, the movement of financial resources and other processes are taken into account. Next, all these papers are sent to the Federal Tax Service (FTS). So all data about the company, its balance sheet, open deposits and loans is registered with government agencies.

Note: accounting registers are protected by trade secrets. This is easy to understand if you consider that the accounting registers used during registration are the code for the entire official income of the enterprise, its debts, recipients of deductions, employee salaries, etc. Anyone who had acquired such data before the amendment to Russian legislation could have used it as a means to undermine competitive businesses.

Accounting registers reflect all expenses and income of the enterprise, but this can be done in different ways depending on the convenience and goals pursued by the accountant. Therefore, there is a classification of registers that allows every entrepreneur to adapt to the current business situation.

Requirements for tax registers

From Art. 314 of the Tax Code of the Russian Federation it follows that tax accounting registers (TA) are filled out on the basis of primary accounting documents continuously in chronological order. This means that random or unfounded entry of data into the register, as well as omissions or any deletions are not allowed.

IMPORTANT! There is no decoding of the phrase “primary accounting document” in the Tax Code of the Russian Federation, therefore the primary accounting document can serve as confirmation of the entries in the NU (letter of the Ministry of Finance of Russia dated January 17, 2014 No. 03-03-06/1/1156).

We should not forget that the generated tax registers must be protected from unauthorized correction. Any errors in tax accounting registers are corrected only with appropriate justification, and the responsible executor certifies all adjustments made with his signature and indicates the date.

IMPORTANT! Information reflected in tax registers is a tax secret. For its disclosure (including by tax authorities), administrative and criminal liability is provided (letter of the Ministry of Finance of Russia dated April 12, 2011 No. 03-02-08/41).

Read more about the requirements for tax accounting and tax registers here.

Storage periods for tax registers

The tax authorities’ request for the submission of documents often contains a list of NU registers according to the number of completed declaration lines. The fine for each document not submitted is 200 rubles (Article 126 of the Tax Code of the Russian Federation). They also have the right to apply Art. 120 of the Tax Code of the Russian Federation for a gross violation of the rules of the NU.

Expenses can be applied to reduce income only if they are justified and primary documents are available for confirmation (clause 1 of Article 252 of the Tax Code of the Russian Federation).

Accordingly, for 4 years (3 years of a possible on-site inspection + current year), it is necessary to ensure the safety of documents showing the receipt of income, expenses and payment of taxes (subclause 6, clause 1, article 23 of the Tax Code of the Russian Federation).

Not long ago, the Ministry of Finance reminded that this period begins at the end of the period in which this document was last used when preparing tax reporting (letter dated July 19, 2017 No. 03-07-11/45829).

Thus, documents confirming the amount of loss, in the event of its transfer in order to reduce the tax base over several subsequent years (clause 4 of Article 283 of the Tax Code of the Russian Federation), are stored after completion of the transfer of this loss for 4 years (letter of the Ministry of Finance of the Russian Federation dated May 25 .2012 No. 03-03-06/1/278).

Documents confirming the formation of the initial cost of a depreciable asset begin to count their 4-year shelf life only after depreciation is completed (letter of the Ministry of Finance dated February 12, 2016 No. 03-03-06/1/7604).

It is clear that the corresponding NU registers are stored according to the same rules.

Every taxpayer must have tax registers for NP, since the Federal Tax Service has the right to request them during its regular audits of reporting.

It is important to understand what NU registers are and how to fill them out correctly so as not to expose your company to unwanted fines for unsubmitted documents or flagrant violation of NU rules.

The article shows samples of tax registers for income tax that will help fulfill the requirements of tax authorities for their registration.

Tax accounting registers for income tax

To fill out a “profitable” declaration, you will need at least 2 NU registers: one for accounting for income, the other for expenses. Information about income received and expenses incurred, generated according to NU norms, will make it possible to determine profit - an object of taxation, without which the calculation of the income tax itself is impossible.

Read about what the tax base for different types of taxes may be in the article “Basic elements of taxation and their characteristics .

Additional registers will have to be drawn up in the case where the taxpayer has many types of activities, and also, in addition to standard business transactions, operations are carried out with special conditions for the transfer of ownership or for which a special procedure for forming the tax base is provided.

IMPORTANT! If the taxpayer cannot or does not want to develop tax accounting registers, but does not want to be punished under Art. 120 of the Tax Code of the Russian Federation for their absence, he has the right to use ready-made ones. Their forms can be found in the recommendations of the Ministry of Taxes of Russia “Tax accounting system recommended by the Ministry of Taxes of Russia for calculating profits in accordance with the norms of Chapter 25 of the Tax Code of the Russian Federation” dated December 19, 2001.

Example

Specialists of Ritm LLC reflect the information necessary for calculating income tax for the year in the following tax accounting registers (RNU):

- RNU "Income from sales" LLC "Rhythm";

- RNU "Expenses that reduce sales income" LLC "Rhythm";

- RNU "Non-operating income" LLC "Rhythm";

- RNU "Non-operating expenses" LLC "Rhythm".

Taking into account that during the specified period, Ritm LLC had no non-operating income and expenses, let us dwell in more detail on the preparation of tax registers for income received and expenses incurred for core activities.

ConsultantPlus experts spoke about the nuances of organizing tax accounting for income tax. Get trial access to the K+ system and move on to the Ready-made solution for free.

“Profitable” register of NU

Continuation of the example

The income of Ritm LLC in the reporting period consisted of the following components:

- revenue from sales of self-made products (RUB 50,367,000);

- revenue from sales of purchased products (RUB 30,590,000)

- proceeds from the sale of other property (RUB 300,000);

IMPORTANT! It is necessary to take into account in the “income” part the entire amount of products sold during the reporting period, with the exception of the income listed in Art. 251 Tax Code of the Russian Federation.

About what income is reflected in Art. 251 of the Tax Code of the Russian Federation, read the material “Art. 251 of the Tax Code of the Russian Federation: questions and answers" .

IMPORTANT! When drawing up the RNU “Income from sales”, one should not forget that revenue in the register and tax return must be indicated without taking into account VAT and excise taxes (clause 1 of Article 248 of the Tax Code of the Russian Federation).

Information for filling out the “income” RNU is taken from accounting data (according to accounts 90 “Sales” and 91 “Other income and expenses”).

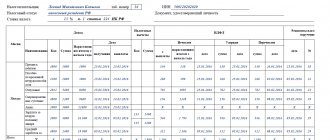

On our website you can download completed tax accounting registers, a sample of which relating to income is drawn up according to the data in the example discussed.

Recommendations of the Ministry of Taxation on NU registers

The NU system proposed in this document distinguishes 5 groups of registers:

- Intermediate calculations.

- Accounting for the condition of an accounting unit.

- Accounting for business transactions.

- Generating reporting data.

- Accounting for targeted funds of non-profit organizations.

You can use the proposed forms of registers, you can develop your own, but the calculation of the tax base for a certain tax/reporting period should reveal the process of forming the final amounts:

- income from sales for this period of time;

- expenses related to these incomes;

- non-operating income;

- non-operating expenses;

- profits from sales and non-sales operations.

In order to create NU registers, you can use data from accounting registers: account turnover, cards, account analyses, etc. This is permitted by the Tax Code of the Russian Federation if tax and accounting are the same, i.e. there are no standardized or non-accounted expenses. They can be maintained in regular Excel tables.

We suggest looking at the difference between accounting and tax registers using examples.

How to fill out the “expenditure” tax register

Taxpayers may experience certain difficulties filling out expense registers. This is due to the fact that the recognition of expenses in tax accounting does not always coincide with the reflection of similar expenses in accounting. So it is not always possible to use accounting registers without making additional adjustments to them.

For example, certain types of expenses are reflected in full in the accounting system, but are normalized in the accounting system (advertising, representative expenses, etc.). And tax legislation generally prohibits recognizing some types of expenses as expenses that form the taxable base for income tax.

Read about the nuances of recognizing other expenses associated with production and sales here.

Continuation of the example

A specialist from Ritm LLC formed a RNU “Expenses that reduce sales revenue”, which reflected the following types of expenses: costs for basic raw materials and supplies, wages along with accrued insurance premiums, depreciation of property of Ritm LLC, expenses for heat, water, electricity, etc.

The accountant took the information to fill out the register from accounting data (for accounts 20, 26, 44, 91, etc.). During the reporting period, the company did not incur expenses, the recognition of which in the financial accounting does not coincide with the accounting rules, so there was no need to adjust the accounting data.

You can also download a sample of a completed tax accounting register “Expenses that reduce sales revenue” on our website.

IMPORTANT! If tax expenses exceed tax revenues and there is no taxable base for profit in any of the periods (tax or reporting), a declaration must still be submitted to the tax authorities (clause 1 of Article 289 of the Tax Code of the Russian Federation).

Results

Tax accounting registers are developed by the taxpayer himself, and their form is approved as an annex to the tax accounting policy. They can be compiled electronically or on paper - it doesn't matter. The main thing is that they contain the mandatory details established by the Tax Code of the Russian Federation. There is a basic requirement for information reflected in registers: all entries must be justified and reliable, and from the contents of the register it must be clear how the tax base is formed.

If tax accounting registers are not maintained by the taxpayer, penalties may be imposed by tax authorities under Art. 120 Tax Code of the Russian Federation.

Tax registers, samples of which you can download on our website, allow you to group available information about the company’s income and expenses and correctly calculate income tax.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.