What is considered travel expenses?

Workers often have to travel to other localities for work needs. Such trips (business trips) are provided for by law (Article 166 of the Labor Code of the Russian Federation) and require the completion of specific tasks. The concept of a business trip does not apply to hired workers whose type of activity involves constant work on the road (intercity transport drivers, conductors, etc.).

Art. 167 of the Labor Code of the Russian Federation guarantees the employee reimbursement by the employer for those expenses associated with a business trip.

According to labor legislation (Article 168 of the Labor Code of the Russian Federation), an employee sent on a business trip must pay:

- travel expenses to and from the business trip;

- expenses for renting residential premises, for example, payment for hotel accommodation;

- additional expenses associated with living outside the place of permanent residence (per diem);

- other expenses incurred by the employee with the permission or knowledge of the employer.

Additional expenses include, for example, expenses for food in a cafe, travel on public transport in the locality where the employee was sent, and payment for taxi services. This also includes expenses for communication services. Particular attention should be paid to the agreement between the posted employee and the employer of entertainment expenses.

The law obliges an employee sent on a business trip to be given an advance from the cash register to pay expenses for the trip. It is important that all employee expenses will be paid by the accounting department based on the checks and receipts submitted by him.

Upon returning from a business trip, the employee draws up a report within three working days, according to which the employer will account for the expenses of the business trip employee. If an employee spent personal funds on justified and documented travel expenses, the accounting department will return this money to the person. And if not the entire amount of the travel advance issued from the cash desk is documented, then the employee returns the unspent balance to the cash office or this amount will be deducted from his next salary.

The amount of daily allowance for business trips is set by the employer independently. Obviously, such an amount must be economically justified.

There is no single standard for daily travel expenses that would be mandatory for all organizations in 2021. However, the law establishes the maximum amount of daily allowance, which for an employee will not be subject to personal income tax: for business trips within Russia 700 rubles per day, and for business trips abroad - 2,500 rubles.

Video: Travel expenses

New in calculating travel allowances in 2021

However, there is an opposite point of view, and this is exactly what the Ministry of Labor adheres to. And it is as follows: The Labor Code requires wages to be paid twice a month, and it depends on the amount of time worked or the volume of products produced or work performed. And since this dependence exists, it must be taken into account when calculating wages for the first half of the month. A business trip is also work. In addition, you can rarely refuse a business trip. But while doing their job, employees should not bear their own personal financial losses. Therefore, to ensure that employees do not experience a loss of material resources, the law provides for the payment of travel allowances.

Due to frequent business trips, the accrued amount for the employee’s average earnings is lower than the salary for the days of the business trip.

Does the absence in the LLC charter of an indication of the term of office of the sole executive body (general director) violate the law? In this case, is it sufficient to indicate the term of office in the decision of the general meeting on the election of the general director or in the order on his assumption of office?

In this case, calculate average earnings based on the actual accrued wages for fully worked working days in these months.

Until recently, there was a restriction according to which the amount of the advance could not be lower than the tariff rate for the time worked.

What if we fix the advance amount as a percentage of the employee’s salary? It does not matter how much time he actually worked in the first half of the month. This method exists and has its supporters. Back in 2009, the Ministry of Health and Social Development confirmed the legitimacy of this approach (letter dated February 25, 2009 No. 22-2-709). The advantages include its simplicity, because in this case an accurate calculation of wages, taking into account time worked, additional payments and deductions, will need to be done only once a month. Registration of a business trip begins with an order. In it, indicate the name of your LLC or full name of the individual entrepreneur, full name and position of the employee, place, duration and purpose of the business trip. For convenience, use the standard order form.

Which accounting accounts are used in postings when reflecting travel expenses?

According to the established procedure, before leaving on a business trip, an employee receives at the cash desk the amount to pay for travel expenses according to the expense order form No. KO-2 (). The employer's accountant prepares the document, and the employee signs for the receipt of funds.

The advance payment issued for travel expenses is documented in a cash receipt order

Non-cash payments by organizations with their employees are becoming increasingly widespread. This applies not only to salaries, but also to the transfer of accountable amounts, including travel allowances, to employee salary cards (letter of the Ministry of Finance of the Russian Federation, Treasury of the Russian Federation dated September 10, 2013 No. 02–03–10/37209 No. 42–7.4–05/5.2 –554).

It is wise to open a corporate bank card in the employee’s name, to which an advance can be credited for travel expenses. This is especially convenient for employees who often go on business trips.

Returning from a business trip, an employee draws up and submits an advance report (Form No. AO-1). All expenses of the business traveler should be displayed on the reverse side of it. Daily allowances are reflected on a separate line. Other expenses (payment for a ticket, payment for a hotel room or rented accommodation, etc.) are reflected on the basis of the attached tickets, checks, receipts, properly executed. These documents must comply with the provisions of Art. 252 of the Tax Code of the Russian Federation. Otherwise, it will be impossible for the posted employee to confirm expenses. Although in special cases (for example, when a train ticket is lost), such compensation is made in practice according to a separate algorithm with the drawing up of acts and the attachment of certificates from the transport organization, which are justification for the costs.

When submitted to the accounting department, the advance report is signed by the traveler (accountable person), then the signature of the accountant who checked the report appears on the document. After this, the report is signed by the chief accountant and approved by the director.

If an employee returning from a business trip has not used part of the advance payment, he is obliged to return the remaining amount to the cashier. This amount may be deducted from the employee's next paycheck. If an employee on a business trip did not have enough advance payment for reasonable expenses and he spent his own money, the employer will reimburse him for such expenses.

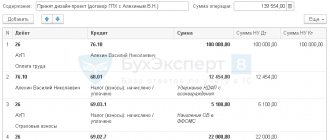

To account for settlements on business trips, account 71 “Settlements with accountable persons” is used, where the debit reflects the amounts of the travel advance issued, and the credit reflects the expenses of the posted employee.

Table: entries for compensation of travel expenses

| Debit | Credit | Accounting transaction |

| 71 | 50 | Issued as a report for a business trip. |

| 71 | 51 | Travel allowances are listed on the salary card. |

| 55 | 51 | Transfer of advance payment to a special corporate card. |

| 71 | 55 | Reflection of the traveler's expenditure from a special card. |

| 50 | 71 | The unspent amounts of the travel advance were returned to the cash desk. |

| 70 | 71 | The unspent balance of the advance payment for the business trip is withheld from the salary. |

| 71 | 50 | The employee was given an amount equal to personal funds reasonably spent on a business trip. |

The employer may not consider certain expenses reflected in the advance report to be justified. These amounts are withheld from the employee's salary, or the employee independently reimburses the amount of unrecognized expenses.

Table: entries for amounts of unreasonable expenses

| 70 | 71 | Expenses not recognized by the employer are withheld from the posted worker’s salary. |

| 50 (51) | 71 | The employee reimbursed unreasonable expenses incurred on a business trip. |

In accounting, checking a traveler’s report begins with confirming the correctness of the daily allowance calculation. The daily amount of subsistence allowance is multiplied by the number of business trip days. These days always include the day of departure and the day of arrival. These dates are verified using the tickets attached to the report.

The time of departure and arrival of transport does not matter.

If the train departed on January 17 at 23:50, then January 17 should be considered the day of departure on a business trip with a daily allowance paid for that day (even if the employee was at work during the day). And also, the day of arrival from a business trip (with payment of daily allowance) will be considered the day on which the business traveler’s train arrived, for example, at 2 am.

The posted worker is paid for all days of travel

Daily allowances must also be paid for weekends and holidays that occur during a business trip, as well as for days en route. The payment of daily allowance is not affected by the inclusion of the cost of food in the ticket price (Letter of the Ministry of Finance dated March 2, 2017 No. 03–03–07/11901).

Expenses are charged to those accounting accounts that reflect the purpose of the employee’s work on a business trip.

If VAT is properly highlighted in the documents attached to the expense report (in invoices, on strict reporting forms), VAT on such documents is charged to account 19 and presented to the budget for deduction.

The cost of a travel document (airplane, bus or train ticket) is reimbursed by the employer. Typically, the choice of transport category is agreed upon by the traveling employee with management, since the cost of the ticket depends on the transport category.

The duration of the business trip is independently agreed upon by the employer and the employee and justified by an order from the manager, and a travel certificate has not been required since 2015 (Government Decree of December 29, 2014).

Table: entries for accounting expenses of a seconded employee

| Debit | Credit | Types of expenses |

| 20 (23, 25, 26, 29) | 71 | The main activity of the company is engaged in production (the balance sheet account depends on the type of activity of the traveler and the assignment for the business trip). |

| 44 | 71 | The main activity of a trading company. |

| 08 | 71 | The purpose of the business trip is the purchase and/or delivery of new fixed assets. |

| 10 | 71 | An employee is sent on a business trip to purchase materials, spare parts, etc. |

| 28 | 71 | Transportation of defective products or warranty repairs. |

| 19 | 71 | Allocation of VAT according to documents attached to the advance report. |

| 68.VAT | 19 | VAT is claimed for deduction. |

If the business traveler’s travel is paid directly by the employer, then the ticket must be received on account 50.3 “Cashier. Monetary documents".

Table: transactions for payment of travel documents

| Debit | Credit | Operation |

| 76 | 51 | Payment for the ticket by the employer. |

| 50.3 | 76 | The ticket has been posted. |

| 71 | 50.3 | The ticket was issued to the traveling employee. |

| 20, 23, 25, 26, 29 (44) | 71 | According to the advance report, the expense for the ticket is written off. |

| 19 | 76 | VAT has been deducted from the ticket price. |

| 68.VAT | 19 | VAT on the ticket price is deductible. |

Calculation of advance payment in 2021 if an employee is on a business trip

The employee requested, referring to Art. 62 of the Labor Code of the Russian Federation, copies of the collective agreement, provisions on remuneration and provisions on bonuses. Is the employer required to provide these documents? The same article establishes the timing of salary payment: no later than 15 calendar days from the end date of the period for which it was accrued.

As we can see, Instruction No. 47 stipulates that if in the months accepted for calculation an employee did not work some days because he was on a business trip, and therefore received payment based on average earnings, then these days and their payment are excluded from the subsequent calculation of average earnings. The employer is obliged to pay wages due to employees within the terms determined by the Labor Code, collective agreement, internal labor regulations, employment contracts (paragraph 7, part 2, article 22 of the Labor Code of the Russian Federation).

Tax accounting of travel expenses

Russian tax legislation does not classify amounts received from the employer for business trip expenses as the income of the posted employee, therefore such amounts are not included in the tax base for personal income tax and insurance premiums (clause 2 of Article 422 of the Tax Code of the Russian Federation and clause 3 of Article 217 Tax Code of the Russian Federation).

These non-taxable amounts include documented travel expenses from the company's location to the point of the business trip and back, as well as all reasonable expenses associated with this travel (boarding passes, airport services, baggage fees).

Non-taxable amounts also include expenses in the locality where the employee was sent. This includes hotel checks and checks for payment for communication services.

Daily allowances are also not taxed, but there is a non-taxable maximum: 700 rubles per day in the Russian Federation and 2,500 rubles for a business trip outside the Russian Federation. This restriction applies to both personal income tax and insurance premiums (clause 2 of article 422 of the Tax Code of the Russian Federation). An exception to this limitation of daily allowances is social insurance contributions “for injuries” - for them the entire amount of daily allowance established in the organization is considered non-taxable (Letter of the Social Insurance Fund of November 17, 2011 No. 14-03-11/08-13985).

Similar to the daily allowance, personal income tax is applied to payments for renting residential premises in the case where documents are not submitted (no more than 700 rubles per day in the Russian Federation and no more than 2,500 rubles abroad). The entire amount is not subject to insurance premiums.

As part of expenses for calculating income tax, actual travel expenses are taken into account in full (clause 12, clause 1, article 264 of the Tax Code of the Russian Federation), including daily allowances. These costs should be classified as general expenses.

The exception is payment for service in a restaurant, additional service in a hotel room, etc. Such expenses are either not recognized by the employer and are paid from the personal funds of the business traveler, or (upon agreement with the employer) are written off as company expenses, but are subject to income tax.

The general basis for accepting VAT for deduction is the presence of an invoice. For travel expenses, you can accept other documents with a designated VAT amount, for example, railway tickets (clause 1 of Article 172 of the Tax Code of the Russian Federation).

Since 01/01/2017, railway services for the transportation of passengers are taxed at a VAT rate of 0% (clause 9.3, clause 1, article 164 of the Tax Code of the Russian Federation), therefore, payment for the use of bedding can be deducted for VAT.

If on the ticket VAT is allocated as one amount for the fee for the use of bedding and for food services, VAT cannot be deducted (Letter of the Ministry of Finance dated October 6, 2016 No. 03–07–11/58108). This amount will be reflected in the company's expenses, not subject to income tax.