Table of KBK used by taxpayers of the simplified tax system in 2020

The simplified tax system with the object “income minus expenses” and the minimum tax should be calculated and paid according to the following BCC:

- 18210501021011000110 - tax;

- 18210501021012100110 - penalties;

- 18210501021012200110 - interest;

- 18210501021013000110 - fines.

The simplified tax system with the object “income” should be accrued and paid according to the following BCC:

- 18210501011011000110 - tax;

- 18210501011012100110 - penalties;

- 18210501011012200110 - interest;

- 18210501011013000110 - fines.

The sample payment system for the simplified tax system “income minus expenses” 2021 contains details that are applicable both for paying tax in connection with the simplified tax system and for paying the minimum tax calculated at a rate of 1% of annual income. The only difference will be in the purpose of payment.

When paying tax in connection with the simplified tax system, in the purpose of payment we write: “Tax in connection with the application of the simplified tax system for the 1st quarter of 2021.”

When paying the minimum payment, the following text is appropriate in the purpose of payment: “Minimum tax for 2021.”

The minimum tax is calculated at the end of the year; at the end of the quarter, advance payments are made according to the simplified tax system.

Payment period

— for the 1st quarter — until April 25

- for half a year - until July 25

- 9 months - until October 25.

But organizations pay tax for the year no later than March 31 of the following year, entrepreneurs - no later than April 30. If the day falls on a weekend, the deadline is moved to the next working day.

Elba will calculate the tax on the simplified tax system “Income” and “Income minus expenses”. Get 30 free days when you sign up and try it yourself. If you are using the simplified tax system “Income” and all payments are sent to your current account, use our free service.

Sample payment order for payment of the minimum tax in 2020 for individual entrepreneurs

Since the minimum tax is paid only at the end of the year, field 107 should always contain the value KV.04.2019; For advance payments, use the value of the quarter for which the payment is made.

The sample payment system for the simplified tax system “income” 2021 contains the same values of fields from 104 to 110 for both organizations and individual entrepreneurs.

To what budget is the simplified taxation system paid and when do you need to give the payment to the bank?

Simplified taxation is a special tax regime (Article 18 of the Tax Code of the Russian Federation).

Taxes paid under special regimes are a type of federal taxes (clause 7 of Article 12 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of the Russian Federation dated April 20, 2006 No. 03-02-07/2-30). However, the answer to the question “To which budget is the simplified tax system paid?” not so obvious. The fact is that the Tax Code of the Russian Federation does not connect the type of tax with the type of budget to which it goes. In accordance with paragraph 2 of Art. 56 of the Budget Code of the Russian Federation, the simplified tax in full (including its minimum part) is subject to credit to the regional budget.

Current simplified tax payments are made quarterly in advance until the 25th day of the month following the reporting quarter. To determine the final annual amount, you need to perform the following actions according to the deadlines indicated below:

Tax payment is carried out by submitting a receipt to the bank (this is only possible for individual entrepreneurs) or a payment slip according to the simplified tax system - in 2020 you need to pay for 2021. The moment of payment (clause 3 of Article 45 of the Tax Code of the Russian Federation) is considered the moment of submission of the payment to the bank, provided that the required amount of funds is available in the payer’s account. The last days for the formation and transfer of payment slips to the bank will be March 31 (for legal entities) and April 30 (for individual entrepreneurs) 2021.

General procedure for processing tax payment orders

Order of the Ministry of Finance of the Russian Federation dated November 12, 2013 No. 107n determines the mandatory details for paying taxes and insurance premiums:

- 101 - status of the payer who issued the payment document;

- 104 - twenty-digit budget classification code, where the first three digits correspond to the tax administrator number;

- 105 - OKATO;

- 106 - basis of payment, consists of two letters (TP, ZD, AR);

- 107 - frequency of tax payment - month, quarter, half year, year;

- 108 — document date, filled in depending on the indicator of field 106;

- 109 - document number, if the debt is repaid on demand;

- 110 - payment type, currently not filled in.

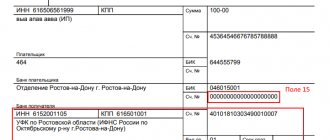

Details for paying the simplified tax system “Income” in 2021

| Payment details | Code (decoding) | Note | |

| Field no. | Name | ||

| 101 | Payer status | 01 – legal entity 09 – IP | They are indicated only when transferring funds to the budget (in our case, tax under the simplified tax system). |

| 18 | Type of operation | 01 | The payment order is assigned code 01. |

| 21 | Payment order | 5 | Self-payment of taxes has the fifth priority. |

| 22 | Code | 0 | The transfer of current taxes is encrypted with code 0. If a request is made by the Federal Tax Service, then the request code (UIN) is indicated. |

| 24 | Purpose of payment | Advance tax payment/Tax transferred in connection with the application of the simplified taxation system (income), for _____ 2021/for 2021 | |

| 104 | KBK | 182 1 0500 110 | |

| 105 | OKTMO | OKTMO code at the location of the individual entrepreneur or enterprise. It must match the OKTMO code specified in the declaration under the simplified tax system. You can determine it by calling the supervising Federal Tax Service Inspectorate or by checking ]]>on the Federal Tax Service website]]>. | |

| 106 | Basis of payment | TP TR ZD | TP – current payment TR - at the request of the inspection ZD – transfer of debt |

| 107 | Taxable period | KV.01.2018 (quarterly) GD.00.2018 (for 2021) | KV – the second two digits indicate the number of the quarter for which the payment is made; GD – the second digit is set to 00 |

| 108 | Document Number | 0, or the Federal Tax Service requirement number | 0 - upon voluntary payment of tax/advance payment; No. of the Federal Tax Service's requirement - when paying on its basis. |

| 109 | Document date | 0, or the date of signing the declaration, or the date of the request of the Federal Tax Service | When paying advances - 0, tax for the year - the date of signing the declaration, if the payment is required by the Federal Tax Service - its date. |

Calculation of the advance payment of the simplified tax system for the 1st quarter of 2017

Data for calculating the advance payment must be taken from KUDiR.

First of all, we will determine the amount by which the advance payment of the simplified tax system can be reduced in the 1st quarter of 2021. This amount, in accordance with clause 3.1 of Article 346.21 of the Tax Code of the Russian Federation, is calculated from the following payments made in the 1st quarter of 2021:

- insurance premiums paid for employees (including persons working under civil contracts);

- temporary disability benefits paid at the expense of the employing organization for the first three days of illness;

- insurance premiums for individual entrepreneurs for themselves.

The next step: determining the maximum amount by which the advance payment of the simplified tax system can be reduced for the 1st quarter. Let us turn to clause 1 of article 346.20, clause 3.1 of article 346.21 of the Tax Code of the Russian Federation and use the formula:

Maximum amount = (All income received in 1st quarter X 6%) / 2

Example:

The individual entrepreneur received an income of 400,000 rubles in the 1st quarter of 2021.

(400,000×6%) / 2 = 12,000 rubles.

This is the maximum amount by which an individual entrepreneur can reduce the advance payment of the simplified tax system.

Now we will directly calculate the advance payment payable for the 1st quarter of 2021, according to paragraphs 3, 3.1, 5 of Art. 346.21 Tax Code of the Russian Federation:

Advance payment = Income X tax rate (maximum 6%) - maximum reduction amount.

Example:

The amount of income received in the 1st quarter of 2021 amounted to 400,000 rubles.

Contributions in the amount of 15,000 rubles were paid, sick leave benefits were paid at the expense of the employer in the amount of 8,000 rubles.

If we add up all the costs of reducing the advance payment of the simplified tax system, we will get 23,000 rubles. This amount exceeds the maximum reduction amount, so we reduce the advance payment only by the maximum amount calculated above. We cannot reduce the advance payment by an amount greater than this.

Therefore, the advance payment of the simplified tax system for the 1st quarter will be:

400,000×6% - 12,000 = 12,000 rubles.

Payment order for payment of the simplified tax system for the 1st quarter of 2021

The last stage is filling out a payment order for the advance payment for the 1st quarter of 2021.

The payment order is drawn up based on the Rules approved by Order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n, and the Regulations of Russia dated June 19, 2012 No. 383-P.

Recipient

The recipient of the advance payment of the simplified tax system for the 1st quarter of 2021 is the territorial department of the treasury of the specific Federal Tax Service Inspectorate, at the location of which the organization is registered, according to the Unified State Register of Legal Entities. If the organization has separate divisions, the single tax and advance payments are transferred, in accordance with clause 6 of Article 346.21 of the Tax Code of the Russian Federation, according to the details of the inspectorate in which the head office is registered.

Requisites

For individual entrepreneurs, when transferring an advance payment to the simplified tax system, the details of the Federal Tax Service Inspectorate at his place of residence are indicated as the recipient in the payment order.

KBK

BCC for advance payment of the simplified tax system for the 1st quarter of 2021: 18210501011011000110

Field 101

Organizations in the payment order indicate 01 in field 101, individual entrepreneurs indicate 09.

Using the button below you can download samples of filling out payment orders for payment of an advance payment of the simplified tax system for the 1st quarter of 2021 for individual entrepreneurs and LLCs:

USN payment (6 percent) 2021

The main part of the payment order contains the payer's details (name, INN, KPP, current account number), the payer's bank details (name, location of the bank, BIC, correspondent account number), the recipient's bank details, the recipient's name, the recipient's account number.

Filling out some payment order details often causes difficulties. Let's look at some of them:

- “Taxpayer status”, field number 101. If the taxpayer is an organization, then it is necessary to put “01”, if the taxpayer is an entrepreneur, then “09”.

- “KBK”, field number 104. The codes will be different depending on which tax object is applied. So, for the payment of tax and advances under the simplified tax system with the object of taxation, “income” KBK will be as follows: 182 1 0500 110.

- “OKTMO code”, field number 105. In this field you must indicate the code of the municipality where the recipient is located (can be found on ]]>the tax office website]]>). The code consists of 8 characters (digits).

- “Basis of payment”, field number 106. If you are paying tax for the current year, then you must indicate “TP”. If this payment is the repayment of debt without a tax requirement, then you must indicate “ZD”. If you are repaying a debt at the request of the tax authorities, you must indicate “TR”. Other values are also provided, for example, “Repayment of debt under an inspection report” - “AP”, etc.

- “Tax period”, field number 107. Here you need to indicate the period for which you pay the tax - for the advance payment the quarter is indicated (QW.02.2018), for the tax - the year (GD.00.2018).

- “Document number”, field number 108. This field must be filled in if you are repaying the debt at the request of the tax authorities - this field indicates the request number. Otherwise, you must enter “0”.

- “Document date”, field number 109. If you pay tax for the current year, and in field 106 you have “TP”, then in this field you must enter the date when the declaration was signed. If you have entered “TR” in field 106 (that is, you are repaying the debt at the request of the inspectorate), then you must enter the date of the request. If you pay tax before filing a return or in other cases, you can enter “0” in this field.

- “Payment type”, field number 110 – no information is indicated.

Many payers have difficulty with the “Purpose of payment” field. This field provides additional information that will help identify the tax payment. How to indicate the purpose of payment simplified tax system 6 percent 2021? When paying the simplified tax system for 2021, the following information should be indicated in the “Purpose of payment” field: “Tax (or “advance tax payment”) paid in connection with the application of the simplified taxation system (USN, income), for 2018.”

We provide a sample of the simplified tax system “income” 2021 for individual entrepreneurs below. It must be remembered that fields 106-109 should not be left empty (unfilled). If for some reason you cannot indicate values in them, you must enter “0”.

Payment of the simplified tax system “6 percent” 2021 (sample):

Payment order under the simplified tax system with the object of taxation “income-expenses” in 2021: sample

For those taxpayers who have chosen the object of taxation “income minus expenses” under the simplified tax system, the obligation to pay the minimum tax is provided (clause 6 of Article 346.18 of the Tax Code of the Russian Federation).

The taxpayer pays the minimum tax if, at the end of the tax period, the amount of tax calculated in the general manner under the simplified tax system is less than the minimum tax.

Let us remind you that the minimum tax is the same for the entire territory of Russia and is 1% of income for the tax period.

In 2021, in the payment order on the simplified tax system “income-expenses” when paying the minimum tax, pay attention to the change in the details when specifying the BCC. We have filled out a sample payment slip with the new KBK and provided it below.

sample payment order under the simplified tax system with the object of taxation “income - expenses”

sample payment order under the simplified tax system with the object of taxation “income - expenses” for payment of the minimum tax