What is salary escrow?

Personnel records, employee reports, automatic calculation of salaries, benefits, travel allowances and deductions in a convenient accounting web service

Get free access for 14 days

The Labor Code requires employees to be paid twice a month. Payment terms are set by the manager and reflected in the company’s internal documents. Before paying wages, the company receives the required amount from the bank and draws up an expense sheet, where the payroll accountant enters data for each employee: name, accrued amount. The salary payment period lasts no more than five days (including the day of receipt of funds from the bank account), and this is the only time when funds in excess of the cash limit can be kept in the company's cash desk.

If one of the employees did not manage to receive their salary within the allotted time, then these funds will have to be deposited - that is, returned to the bank. This is the responsibility of the company, at the request of the Central Bank of the Russian Federation (Instruction dated March 11, 2014 No. 3210-U). To which accounting accounts should funds be deposited when returning to the bank, how to recognize amounts when calculating income tax, is it necessary to charge insurance premiums from them and withhold personal income tax? - read on.

Salary Deposit

Depositing is most often encountered by enterprises that pay cash to employees through the organization's cash desk.

The concept of deposit is funds due for payment that have not been received in person within the regulatory time frame in accordance with the collective contract. The amount is considered subject to deposit only if it is not received through the fault of the employee.

Separately, for each enterprise, the Bank of Russia sets, through bank settlements, a certain limit - a limitation that, when storing monetary assets in the institution’s cash desk, cannot be exceeded.

Amounts for wages received from the bank must be issued within 3 days; in the conditions of the Far North, the period is extended by another 48 hours.

If you have not received payment for hours worked, the accrual should be deposited and deposited in a banking organization.

How to deposit your salary: step-by-step algorithm

When the deadline for paying wages expires, the cashier must check the payroll, recalculate the amounts paid and find out the amount of the balance. In column 23, opposite the names of employees who did not manage to receive the money, the entry “Deposited” is made or the same stamp is affixed. At the end of the statement the amounts are written down. Important: The totals of amounts paid and amounts to be deposited must be equal to the final amount on the statement.

The salary to be deposited must be submitted to the bank the next day after the end of the salary payment period. Record the deposit in the register. There is no unified form for the register of depositors; it can be compiled in free form. The register must contain the following details:

- company name or full name of the individual entrepreneur;

- date of registration of the register;

- period of occurrence of deposited funds;

- payroll number;

- Full name and personnel number (if any) of the employee who did not receive the money;

- amount of unpaid salary;

- total amount for unpaid salary;

- cashier's signature with transcript.

You can also include other details that are important to the company in the register. Transfer the data from the register to the ledger for recording deposited amounts. The book form can also be created independently or taken as a basis for forms for budgetary organizations. Document the accounting of salary deposit operations by posting:

Dt 70 Kt 76-4 - deposited salary not received by employees; Dt 51 Kt 50-1 - deposited salary deposited into the current account.

When an employee who has not received a salary applies for it, the amount will need to be given upon first request, written or oral. There is no deadline for issuing the deposited salary. You need to receive the salary amount from the bank, draw up a cash order in the name of the employee, and reflect the date and number of the order in the book of accounting for deposited amounts.

The issuance of the salary must be recorded in the register of deposited amounts, a note about the amounts received must be placed next to the employee’s name and the date must be indicated. You need to keep salary deposit registers for five years. Record the accounting of the transaction for issuing deposited salary by posting:

Dt 50-1 Kt 51 - money received from the bank to pay the deposited salary; Dt 76-4 Kt 50-1 - the employee was given a deposited salary.

Actions of the accountant (cashier) during deposit

After the time allotted for paying wages has expired, the accountant must carry out sequential actions regulated by the Procedure for Conducting Cash Transactions (clause 18 talks about depositing).

- To confirm the receipt of money by employees, the corresponding columns are provided in the statements: 23 – “Received money” in the payroll and 5 – “Signature on receipt of money” in the settlement and payment slip. If, after the allowed time has elapsed after opening the statement, no employee signatures appear in these columns, the accountant applies a special stamp or writes “Deposited” in them.

- At the bottom of the statements, they are indicated separately and the issued and deposited salaries are calculated; they must coincide with the total, which is what the cashier (accountant) signs on the statement.

- The numbers of deposited salaries are entered into a special register (the form is not approved by law; an enterprise can develop it independently and record it in internal documentation).

- For sums of money issued as wages, it is required to draw up an expense cash order (form No. KO-2, approved by Decree of the State Statistics Committee of Russia dated August 18, 1998 No. 88), its details are also noted on the statement and entered into the cash book.

- All records previously certified by the signature of the accountant (cashier) must be transferred for control to the chief accountant or management.

- The cashier is obliged to hand over money not given to employees to the bank, since it is prohibited to keep amounts in the cash register that exceed the permitted limits, even if they are intended for future expenses.

IMPORTANT! If the funds were issued not by the cashier, but by another person on his behalf, then at the bottom of the document an additional mark is required about who issued the money according to this statement.

How to arrange the release of deposited wages from the cash desk by proxy ?

What to do with unclaimed wages?

The employee has three years to receive his deposited salary. The countdown begins from the next day after the date on which the company should have issued the salary. If the employee or his representative has not applied for a deposited salary within three years, the following actions must be taken.

In accounting, write off the amount as other income. To calculate the tax, include it in non-operating income. Prepare an inventory report, an accounting certificate and an order from the head of the organization to write off accounts payable.

Never miss a thing in payroll

“Accounting is a convenient program. Thanks to the developers. I have been working with Kontur for a long time. And it’s convenient to manage personnel; you’ll never miss anything in payroll. All reports reach the recipient on time. Everything is updated with the times. I really like it, everything is convenient. And when something is unclear, you can call - and they will always come to your aid. Thanks again to the developers."

Natalia Abbasova, accountant, senior Veshenskaya, Rostov region.

Shelf life

There is a certain time established by the director of the company or the entrepreneur, during which it is necessary to pay all employees of the enterprise.

If the PO is not received on time, it will be considered deposited, and the recipient will be considered a depositor.

The maximum period for storing wages in the cash register of an enterprise is 5 working days, this period also includes the day when employees receive cash.

There is no deadline for receiving the deposited salary; if for some reason the employee has not received the salary, after the period of storage of the salary in the cash register expires, he contacts the accounting department of the enterprise and receives the already deposited salary at any working time.

It is important to know that the statute of limitations for depositing a salary is not established by the legislation of the Russian Federation; however, there is a general statute of limitations, which is three years. During this time, in court, the plaintiff can request payment through the court, if the situation so requires.

How to generate income tax?

The procedure for writing off amounts of deposited salary in tax accounting depends on the method by which the company calculates income tax.

- With the accrual method, the deposited salary is included in expenses in the same month when it was accrued.

- With the cash method, the amount of the deposited salary is included in expenses only at the time of its payment. Then, in the month the salary is accrued, a deductible temporary difference arises and a deferred tax asset is created, which will be written off after the salary is issued.

Today, most companies have salary project agreements with banks with the transfer of money to employee cards, and salary deposit transactions rarely occur.

Kontur.Accounting is a web service in which you can easily conduct accounting, calculate salaries (and arrange salary deposits), and submit reports. Get to know the service's capabilities for free for 14 days!

Try for free

How can an employee receive deposited wages?

All relations with the employee are recorded in the employment contract; most of these agreements contain the procedure for the employee’s actions when paying amounts not received on time. If the employment contract does not provide for a deposit clause, then the employer must record the information in any other internal document of the organization.

An employee can withdraw earned money in three ways:

- together with advance payments;

- with remuneration for the next working month;

- after a written request to the accounting department.

An expense cash order is filled out for the employee, which indicates his personal data and the purpose of the payment. A new statement is printed. The signature is placed on the statement and in the RKO. If there are several recipients, then the statement and RKO are created for each individually.

Where should unpaid wages be kept: in a bank or at a company?

If the cash register limit is exceeded, the amount of unpaid wages will need to be handed over to the bank, in accordance with clause 2 of the Directive of the Bank of the Russian Federation of 2014 No. 3210-U. But if the cash limit is not exceeded, then the deposited salary can be kept in cash at the organization’s cash desk.

The cash balance limit is set by the bank that services the organization. For violation of cash discipline, the employer may be held administratively liable. The fine for managers is 4-5 thousand rubles, for organizations - 40-50 thousand rubles. according to Art. 15.1 Code of Administrative Offences.

The rules on the need to deposit wages not received on time apply to representatives of small businesses, as well as individual entrepreneurs. But according to the rules that are prescribed in the Directives of the Bank of the Russian Federation of 2014 No. 3210-U0, they have the right not to comply with cash limits. Thus, they can avoid depositing the salary with the bank and keep it in the till until the employee is paid.

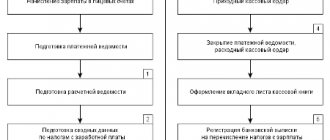

Documenting

The procedure for depositing funds differs from simply storing cash. According to Bank of Russia Directives No. 3210-U dated 2014, this procedure consists of the following stages:

- Accountant doing about in payroll.

- The cashier determines the amount of paid and deferred wages . He indicates it in the final line of the statement.

- He then reconciles the amounts of wages issued and deposited and reconciles them with those indicated in the statement.

- The signed statement is handed over to the manager.

Payment of wages in cash from the organization's cash desk is processed through payroll or payroll. If the salary was not received within the established time frame, then opposite the name of such an employee in the statement you need to write an o (in the place where the employee must sign).

The amount of the deposited salary should also be displayed in a special register of depositors, which is compiled in free form. It contains an indication of the employee and the amount of wages owed to him.

What accounting entries appear in accounting when calculating compensation?

Record the accrual and payment in account 73 “Settlements with personnel for other operations.” Maintain analytical records for each employee. Compensation for late payment of wages and accrued insurance premiums from it is recognized in accounting as another expense and is charged to account 91.

Compensation for late payment of wages: postings

| Operation | Debit | Credit |

| Compensation accrued for delay in salary transfer | 91 | 73 |

| Insurance premiums accrued | 91 | 69 |

| Compensation payment for delayed salary paid to employee | 73 | 50, 51 |

| Insurance premiums listed | 69 | 51 |

It is risky to recognize compensation for late payment of wages as tax expenses (Letter of the Ministry of Finance dated October 31, 2011 No. 03-03-06/2/164).

How is the amount calculated?

In case of untimely payment of wages or other amounts established by the remuneration system, the employer is obliged to pay compensation to the employee in accordance with Article 236 of the Labor Code of the Russian Federation. The employer is obliged to pay compensation regardless of whether it is his fault for the delay or not.

Before generating entries for compensation for delayed payment of wages, it must be calculated.

The Labor Code establishes only the required minimum compensation payment. The organization has the right to establish a higher size by approving it in a local regulatory act:

- collective agreement;

- regulations on wages;

- order, disposition, other LNA.

Compensation for delayed payment of wages is calculated for each calendar day of delay, starting from the day following the established day of payment of wages and up to and including the date of repayment of the debt. The minimum amount of compensation is calculated based on 1/150 of the key rate of the Central Bank of the Russian Federation:

At CLUB.TK LLC, wages are paid no later than the 15th of the next month. For May, manager Ivanov I.I. the salary in the amount of 10,000 rubles was transferred on June 19. The transfer delay was 4 calendar days. The key rate of the Central Bank for the settlement period is 5.5%. The amount of compensation paid to the employee will be:

Employee compensation calculator for late wages

Fill in the amount of debt, the established and actual date of payment of wages. The calculator will calculate the amount of compensation:

The procedure for receiving and features of payment of DPZ

The employer is obliged to pay unpaid wages upon request of the employee. He can apply orally or in writing. When applying in writing, you must write a statement addressed to management.

If limits allow, the deposited amount can be stored in the cash register at the enterprise. If the limits are exceeded, these funds are sent back to the banking organization.

According to the regulations, the cash register limit is the maximum permitted amount of money that can be left in the cash register at the end of working hours.

The manager sets the cash limit independently, taking into account the instructions of the Central Bank of the Russian Federation.

If the money is in the cash register, then it can be returned to the employee without any problems upon first request. If the limits are exceeded, the employee can receive his salary along with the next planned payments. But if he insists on immediate return, then the organization sends a request to the bank to transfer the required amount of money.

Next, after the money is received, the cashier issues a settlement settlement in the name of the employee to pay the unpaid salary. The accountant must maintain a book of deposits, which should reflect the numbering of orders and dates. The consumables must be signed by the manager and the chief accountant and left to be stored at the enterprise.

The employer is obliged to issue the DPZ in full. If some amount is withheld, the employee can go to the labor inspectorate. This process is regulated by the Labor Code. After 3 months of overdue wages, the court will accept the claim.