According to the Tax Code of the Russian Federation, a tax rate of 0% is provided for exported goods, and therefore, when exporting goods from the territory of the Russian Federation, the exporting company does not have to pay VAT. Since the collection of taxes when exporting goods is controlled by the Federal Customs Service of Russia, the company does not calculate VAT at a rate of 0% in column 47 “Calculation of payments” when submitting a customs declaration for exported goods. However, it must confirm its right to apply a zero tax rate. In fact, she needs to report that the goods went through the export procedure and were, in fact, exported from the territory of the Russian Federation.

Where and in what form to submit documents

It is necessary to submit documents to confirm zero VAT to the tax office at the place of registration of the legal entity - this can be done on paper or in the form of electronic registers through the electronic document management (EDF) operator system.

As a rule, a paper package of documents to confirm 0% VAT is used by small companies that have 10–30 deliveries of goods during the year. And large participants in foreign trade activities that move goods in large volumes submit electronic registers to the Federal Tax Service.

What documents need to be submitted

- If you submit documents on paper, you must submit to the tax office (Article 165 of the Tax Code of the Russian Federation):

- Contract for the supply of goods (or a copy thereof). If the contract has already been submitted to the tax authority, then there is no need to send it again. It is enough to send a notification with the details of the previously submitted document and the name of the tax authority to which it was submitted.

- A customs declaration (or a copy thereof) with a mark from the customs authority on the release of goods and a mark on the actual export of goods from the territory of the Russian Federation.

Until 2021, the exporter also had to submit to the Federal Tax Service copies of transport or shipping documents with a mark from the customs authority on the export of goods. Now these documents are submitted only upon request from the tax authorities.

- If you submit documents electronically through the EDI system, then you need to send to the tax office:

- Electronic register of customs declaration.

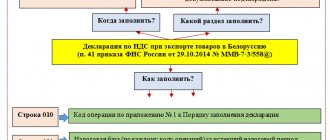

Documents to confirm 0% VAT on export

Export of goods is subject to VAT at a rate of 0%. To use the zero rate, the company must confirm the fact of export.

To confirm the fact of export and reimburse the “export” VAT from the budget, it is necessary to fulfill certain requirements:

- you need to collect documents confirming that the exporter actually exported the goods abroad to Russia. Lists of documents are contained in Art. 165 of the Tax Code of the Russian Federation in relation to the situations given in paragraph 1 of Art. 164 Tax Code of the Russian Federation;

- you need to fill out a VAT return and submit it to the tax office along with documents confirming export.

What documents are needed

To recover VAT, you must submit a package of documents to the tax office. Here is a list of them.

- Foreign economic contract (copy of the contract) with a foreign partner for the supply of goods outside Russia. That is, a document reflecting information about the parties and the subject of the transaction, as well as the conditions for its implementation.

- Customs declaration (CD) or a copy thereof.

The DT must have:

- mark of the customs office that carried out the customs operations;

- mark of the border customs office through which the goods were exported from Russia.

If a company submits a customs declaration in electronic form, then it is sufficient to submit it in the form of information about the release of goods. Such a mark will appear in the document automatically when the customs authority finishes checking the declaration and sends a corresponding message to the customs declaration service.

If the export of goods was carried out through the territories of the member states of the EAEU Customs Union, where customs control has been abolished (Belarus, Armenia, Kyrgyzstan or Kazakhstan), it is sufficient for the DT to indicate the customs office that carried out customs operations with the goods.

O must be obtained in the form of an original stamp only if the exporting company will submit documents confirming zero VAT to the tax office on paper. The stamp is affixed to the customs declaration and transport document by the customs authority at the border crossing point.

Until 2021 (more precisely, until October 1, 2021), the exporter also had to submit to the Federal Tax Service copies of transport or shipping documents with a mark from the customs authority on the export of goods. Now these documents are submitted only upon request from the tax authorities. The Ministry of Finance of Russia reminds us of this in letter dated August 27, 2019 No. 03-07-08/65684.

Registers of documents

If there is a large volume of documents, it is possible to submit registers based on them (Clause 15, Article 165 of the Tax Code of the Russian Federation). This applies to shipping, transport, shipping and other documents, as well as customs declarations. The Federal Tax Service has the right to request for control any of the documents included in such a register.

These registers are presented exclusively in electronic form via telecommunication channels through an electronic document management operator. The forms of these registers and the procedure for filling them out, as well as the formats and procedure for submitting them in electronic form, were approved by order of the Federal Tax Service of Russia dated September 30, 2015 No. ММВ-7-15/427.

Deadline for collecting supporting documents

The period for confirming the legality of using a 0% rate is a single 180 days and does not depend on the specific situation for which such a rate is applied.

The generated set of documents must be submitted to the Federal Tax Service along with the tax return issued for the period in which this set was collected (clause 10 of Article 165 of the Tax Code of the Russian Federation). Documents to confirm zero VAT must be submitted to the tax office at the place of registration of the company. This can be done on paper or in the form of electronic registers.

Simplified export confirmation procedure

According to the current rules, you can claim VAT deduction on goods, works and services purchased for export operations in the generally established manner before you have collected a package of documents confirming the zero VAT rate. That is, at the moment of acceptance of these goods for accounting and receipt of invoices from suppliers.

An exception to this rule is the export of primary goods, which include: mineral products, chemical products and other related industries, wood and wood products, charcoal, pearls, precious and semi-precious stones, precious metals, base metals and products of them.

When are customs stamps needed?

An important condition for confirming zero VAT is the presence of stamps from the customs authority on the customs declaration. Tax legislation provides for two types of marks:

- “Release permitted” - about the placement of goods under the customs export procedure;

- “Goods exported” - about the export of goods from the territory of the Russian Federation.

The original marks are affixed in the form of a rectangular stamp with lilac-pink-blue mastic (the shade depends on the degree of wear of the stamp pad). In addition, the mark can be indicated in the form of information and be an analogue of the original stamp for electronic customs declaration.

Let's figure out in what cases the tax office needs one or another mark and in what form.

"Release permitted"

In a letter dated July 31, 2018 No. SD-4-3/ [email protected], the Federal Tax Service explained: if a company submits a customs declaration in electronic form - and there can be no other option, since 100% of customs declarations in the Russian Federation are submitted in electronic form - then It is enough to present it in the form of information about the release of goods. Such a mark will appear in the document automatically when the customs authority finishes checking the declaration and sends a corresponding message to the customs declaration service.

The Federal Tax Service also clarifies that in the future it is not necessary to affix the original “Release Permitted” stamp to printed copies of customs declarations.

It happens that the accounting department of an exporting company asks for a “Release Permitted” stamp to maintain internal records. Then the stamp can be obtained at the customs post where the goods declaration was submitted. In the case of remote declaration of goods, the stamp can be placed at the customs post indicated in column 30 of the customs declaration “Location of goods”.

The customs mark in the form of information about the release of goods in a copy of the electronic customs declaration looks like this:

How long does it take to confirm the zero VAT rate and reflect the data in the declaration?

In paragraph 9 of Art. 165 of the Tax Code of the Russian Federation defines the deadlines for submitting documents to confirm the zero VAT rate.

However, the 180-day period is determined differently depending on the country of export.

If exports are made to third countries, then the period is calculated from the date the goods are placed under the customs export procedure (clause 9 of Article 165 of the Tax Code of the Russian Federation).

If export is carried out to the territory of the EAEU, then the period is calculated from the date of shipment of goods. The date of shipment of the goods will be the date of drawing up the primary document issued to the buyer of the goods or to the first carrier (clause 5 of the Protocol on the collection of indirect taxes within the EAEU).

Documents (or registers) are transferred to the fiscal authorities when submitting the VAT return for the quarter.

The report contains special sections 4–6 for export transactions. These sections are filled out only if they contain the relevant information:

- If a set of documents is collected before the expiration of 180 calendar days:

- the goods were shipped and the documents were collected in one tax period - section 4 of the declaration is completed for the quarter in which the shipment occurred;

- the goods were shipped in one quarter, and the documents were collected in another quarter - section 4 of the declaration is filled out for the reporting period in which the documents were collected.

- If there are no documents after 180 calendar days from the date of shipment, Section 6 of the updated declaration for the tax period in which the goods were shipped is completed, with VAT charged at a rate of 20% (10%).

- If a complete package of supporting documents is nevertheless collected, then the data is entered into section 4 of the declaration for the period in which the documents are ready. And the tax amounts paid are subject to deduction in accordance with Art. 171 and 172 of the Tax Code of the Russian Federation.

Foreign currency proceeds from export sales received from a foreign counterparty are recalculated into rubles at the Bank of Russia exchange rate on the date of shipment (clause 3 of Article 153 of the Tax Code of the Russian Federation).

The nuances of filling out a VAT return for export in each of the above cases were described in detail by ConsultantPlus experts. To study the material, sign up for free temporary demo access to the K+ legal reference system.

The procedure for applying deductions when exporting depends on what goods are exported - raw materials or non-raw materials. This issue is described in detail in the section “Filling out a VAT return when exporting” in the article “VAT when exporting goods in 2021”.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

"The goods have been exported"

As for o, it must be obtained in the form of an original stamp only if the exporting company will submit documents confirming zero VAT to the tax office on paper.

The stamp is affixed to the customs declaration and transport document by the customs authority at the border crossing point. At the same time, the inspector enters information about the export of goods into the database of the Federal Customs Service of Russia and then this information is transferred to the Federal Tax Service for control (clause 17 of Article 165 of the Tax Code of the Russian Federation).

If the stamp was not affixed at the checkpoint, then confirmation of the fact of export can be obtained from the customs office where the goods were declared. To do this, you must submit an application to the customs post, which is drawn up in any form, and the following must be indicated:

- registration number of the goods declaration, which requires confirmation of the fact of export;

- serial number and description of the product;

- code of the customs authority of the place of departure.

The application can be submitted either in paper or electronic form. Within 10 days, the customs authority will send the declarant information about the actual export of goods in the same way - in writing or electronically.

If an exporting company submits electronic registers to the tax office, then it is not required on customs documents - neither in the form of information, nor in the form of an original stamp (Clause 15 of Article 165 of the Tax Code of the Russian Federation). However, to prepare the register, information on the date of actual export of goods will be required. They can be obtained through your personal account on the FCS portal using the information service “Information about the export of goods.”

How export operations are reflected in accounting, including in 1C 8.3

In accounting, export transactions are recorded as follows:

VAT

If an advance payment is received for an export transaction (clauses 1, 3 of Article 154 of the Tax Code of the Russian Federation):

- no advance invoice is issued for the buyer;

- the amount of the advance received is not reflected in the VAT return.

Next, after the goods have been shipped for export:

- ruble foreign exchange earnings are determined at the Bank of Russia exchange rate on the date of shipment of the goods, even if a 100 percent advance was previously received;

- the foreign counterparty is issued a shipping invoice, and if he does not need the document, then an invoice is drawn up for himself in one copy.

The shipping invoice is recorded in the invoice journal. It must be reflected in the sales book on the last day of the quarter in which documents confirming the right to a zero rate are collected. The amounts of export proceeds, converted into rubles at the exchange rate on the date of shipment, are indicated in section 4 of the VAT declaration.

Income tax

Recalculation of proceeds from the sale of goods for foreign currency for profit tax purposes looks like this:

- 100% prepayment has been received - we recalculate at the Bank of Russia exchange rate on the date of receipt of money.

- In case of partial payment:

- for goods paid in advance, payment is made at the exchange rate on the date of receipt of the advance;

- for goods paid for after shipment, we calculate at the exchange rate on the date of shipment.

- The amount of unpaid goods after shipment is subject to revaluation. Exchange differences are calculated at the end of each month (if the receivables of the foreign counterparty are retained) and at the date of debt closure.

In the absence of documents to confirm the application of the 0% VAT rate, the calculated VAT is included in other expenses associated with production and sales, on the basis of subclause. 1 clause 1 art. 264 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of Russia dated October 20, 2015 No. 03-03-06/1/60045, resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated April 9, 2013 No. 15047/12). The position on this issue was previously ambiguous.

Statistics

The statistical form for the movement of goods when exported to the EAEU countries must be submitted to the customs authority no later than the 8th working day of the month following the month of delivery (Law “On Amendments to Articles 12 and 104 of the Federal Law “On Customs Regulation in the Russian Federation” and the Code of the Russian Federation on administrative offenses" dated December 28, 2016 No. 510-FZ). Fines for violating reporting deadlines range from 10 to 50 thousand rubles. (Article 19.7.13 Code of Administrative Offenses of the Russian Federation).

How to respond to a tax demand after submitting documents

The tax inspectorate may request documents in the following cases (clause 1.2 of Article 165 of the Tax Code of the Russian Federation):

- if the information provided by the taxpayer does not correspond to what the tax authority has;

- if the Federal Tax Service does not have information that the Federal Customs Service transmits as part of departmental exchange.

If, based on the results of the reconciliation, the tax office has requested a transport document, the exporter must submit a paper invoice with the original “Goods Exported” stamp.

If the tax office has requested a declaration from an exporter who used an electronic register to confirm zero VAT, then it is enough for him to submit a copy of the electronic customs declaration, printed from his software, with customs information about the release of goods (in the future, put the “Release permitted” stamp on this copy of the EDT no need). At the same time, the “Goods exported” stamp on a paper copy is not required (clause 15 of Article 165 of the Tax Code of the Russian Federation) - this has been permitted since October 2021 by amendments to Federal Law dated August 3, 2018 No. 302-FZ in the provisions of Art. 165 Tax Code of the Russian Federation.

Is it possible to refuse the zero VAT rate and when must it be applied?

Until January 1, 2021, the procedure for confirming the zero rate described in Art.

165 of the Tax Code of the Russian Federation was mandatory. But thanks to the changes made to paragraph 7 of Art. 164 of the Tax Code of the Russian Federation by federal law dated November 27, 2017 No. 350-FZ, the right has appeared to refuse to apply and confirm the 0% VAT rate for exports if certain conditions are met. If the exporting organization considers it inappropriate to apply a zero VAT rate, then a refusal is possible for a period of at least 12 months, and for all export transactions (which is not always beneficial). The application of a zero rate selectively, in relation to individual companies, is unacceptable.

To refuse the 0% rate, you must submit an application to the Federal Tax Service at the place of registration in any form (there is no approved form). The deadline for submitting such an application is no later than the 1st day of the quarter from which the company will apply a VAT rate of 20% or 10%. If there is no such statement, the organization must apply a zero VAT rate within the time limits established by law.

The right to refuse to apply the zero rate arises when exporting goods to third countries that are not members of the Customs Union. As for exports from the Russian Federation to the countries of the EAEU (Belarus, Kazakhstan, Kyrgyzstan and Armenia), the application and confirmation of the zero VAT rate is the responsibility of the organization.