Cash discipline implies compliance by the entrepreneur with all the rules for making cash payments established by law. In this article, we will look at how to maintain cash discipline with online cash registers, how to use it to simplify the cash register process, and what liability an entrepreneur faces in case of violations.

Cash discipline is compliance with the rules established by Russian legislation for cash payments, which include all types of income and expense transactions.

Basically, cash discipline at online cash desks affects the following operations:

- payment of wages;

- cash collection;

- return or issuance of borrowed funds;

- receiving or depositing money at the bank;

- settlements with accountable persons, etc.

In 2021, all LLCs and individual entrepreneurs that carry out cash payments are required to use online cash registers. Exceptions are individual entrepreneurs and LLCs on PSN, UTII (clause 2 of Article 346.26 of the Tax Code of the Russian Federation), providing services and vending. They are required to issue a document confirming the receipt of funds.

How to simplify cash management using cash discipline

For some categories of entrepreneurs, the law provides for a simplified procedure for maintaining cash records.

According to the decree of the Central Bank of the Russian Federation, issued in March 2014, businessmen who own enterprises classified as small or micro businesses, as well as individual entrepreneurs, may not set a cash limit.

Individual entrepreneurs, in addition, may not draw up PKO and RKO (receipt and expense cash order), and also have the opportunity to refuse the cash book.

However, these privileges do not replace the obligation to create payroll records when paying wages and benefits to employees.

The category of small businesses includes organizations that fall under the conditions of Law No. 209-FZ (clause 1 of Directive No. 3210-U). They can be briefly summarized as follows:

- The organization is classified as consumer cooperatives or organizations equivalent to commercial ones (except for municipal and federal state unitary enterprises);

- The number of such enterprises should vary from 16 to 100 employees;

- Income for the year should not exceed 400 million rubles.

- If the enterprise employs up to 15 people inclusive, and the revenue for the previous year, according to reporting, did not exceed 60 million rubles, this enterprise will be classified as a micro-business.

Important!

The share of state ownership in such enterprises should not exceed 25%.

Despite the obvious conveniences, a businessman must understand that if the receipt of funds is not confirmed by a cash receipt order, the cash may simply not reach the company’s cash desk, remaining with an unscrupulous employee.

In this connection, we can conclude that simplified management of cash discipline will primarily be convenient for entrepreneurs who do not have hired employees.

Requirements for the premises of cash registers of enterprises

The requirements for cash register premises are complex. They concern all aspects of the room.

Walls and ceilings

The following requirements apply to walls and ceilings:

- Walls and ceilings must be at least 500 mm thick, concrete blocks - at least 200 mm thick, reinforced concrete panels - at least 180 mm thick.

- Partitions should be similar to external walls. They are constructed from 80 mm thick plasterboard panels. A metal grid with a diameter of at least 10 mm is laid between the panels. The cell dimensions are no more than 150 x 150 mm.

- If the walls and ceilings do not meet the listed requirements, their internal surfaces are reinforced with metal gratings. Their diameter is at least 10 mm. If it is not possible to install gratings from the inside, they are installed from the outside. However, this decision must be agreed upon with security units.

- If the cash register premises are located next to other premises (boiler rooms, entrances, etc.), the walls and ceilings on the inside are also strengthened.

Walls and ceilings are the basis for the security of a room.

Doors

The following requirements apply to doors:

- Doors must meet the standards of GOST 6629-88, GOST 24698-81, GOST 24584-81. They must be durable and withstand hacking attempts: both physical (shoulder hits) and those involving the use of tools (crowbar, ax, etc.).

- The requirement for entrance doors is serviceability. Their thickness is at least 40 mm. Doors are equipped with at least two mortise locks. They are mounted at a distance of at least 300 mm.

- Entrance doors are covered with sheet steel. On the inside they are equipped with a metal chain and a peephole.

- The strength of doors can be increased. For this purpose, special linings, corner lock strips, and reliable door hinges are used. You can strengthen the door leaf.

- Shaped grilles can be used to provide increased protection.

- The doorway is framed with a steel profile.

Doors are also the basis of security. It is through them that criminal entry is usually carried out.

Window

Windows must meet these requirements:

- The outer door or wall has a door through which cash transactions are carried out. Its size is no less than 200 x 300 mm. If the window size is larger than the standard size, it is reinforced on the outside with a “rising sun” grille.

- Windows and vents are glazed and equipped with reliable locks. The glass is fastened in the grooves with high quality.

- The openings of the cash register area are equipped with metal bars. They are made from steel rods. Their diameter is at least 16 mm.

- It is possible to use decorative grilles. However, their strength must be sufficient to ensure safety. That is, gratings cannot play only a decorative function.

- Grilles can be mounted both from the inside and between the frames. In the latter case, the window opens outward.

- If bars are placed on windows, one of them should be sliding. A padlock is installed on this grille.

- If the room belongs to group A, protective shields must be used in addition to the grilles.

Windows can be internal or external. The first ones are used to issue funds.

Ventilation shafts and chimneys

You can also enter the room through the ventilation shaft. Therefore, it is also equipped with structures for protection:

- Shafts and chimneys with access to other rooms and to the roof are equipped with metal gratings.

- For protection, you can use false grilles, which are made of metal tubes with a diameter of at least 6 mm.

The gratings must be durable. They provide a barrier to penetration.

Locking devices

Locking devices are locks. If they are equipped in rooms of group “A”, the devices must be highly reliable. Let's consider the requirements for locking devices:

- Mortise locks without an automatic latching function, padlocks and padlocks, bolts and latches are used as locking devices.

- High security locks of the “Abloy” type are installed.

- The degree of protection is considered high if there are five locking pins on the locking cylinder.

- Padlocks are usually a tool for added security.

- Door hooks are made of metal rods with a diameter of at least 12 mm.

The security qualities are influenced by the method of fastening the safety linings and other parts. Fastening in locks is carried out using screws.

Door hinges

Door hinges are made of steel. The latter provides the necessary strength. Fastening is done using screws. If the doors open outward, end hooks are installed.

What you should not spend cash on

Quite often, store owners or accountants have a question about what expense items can be spent on cash proceeds from the cash register.

First, let's look at what an entrepreneur has the right to spend cash proceeds on:

- Payment of wages to employees;

- Expenses for scholarships;

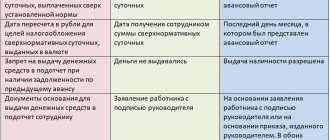

- Issuance of travel expenses to accountable persons;

- Any other payments to persons who are accountable;

- Expenses on goods or services (except for payment for securities);

- Insurance payments;

- Payment for returned goods;

- Issuance of funds for services/work not provided;

- Issuance of funds for the consumer needs of the owner of the organization, if these needs are classified as personal;

- Payments to the paying agent when carrying out banking transactions.

The list of expense items on which an entrepreneur cannot spend cash from the enterprise’s cash desk includes much fewer items, but their compliance is strictly mandatory:

- Rent;

- Interest on loans, as well as the issuance or repayment of the loans themselves;

- Any manipulation with securities;

- Costs of organizing games from the gambling category.

If an entrepreneur needs to make one of the above payments, the funds will need to be withdrawn from the organization’s current account.

What does a check look like?

An electronic check has the same legal force as a printed one on paper. This means that the receipt is proof of purchase and can be used in court in disputed cases. Checks contain the same information about the transaction:

- seller tax regime;

- check and shift number;

- information about the cashier - name and position;

- date, time and place of purchase;

- name and TIN of the store;

- names of purchased products, as well as cost, VAT and total quantity;

- payment method - cash or card;

- registration numbers of the cash register and fiscal drive;

- QR code.

Previously, the receipt did not contain many items, for example, a QR code.

The procedure for maintaining cash discipline

As for measures aimed at maintaining cash discipline at online cash registers, the company develops them independently.

Cash limit at the cash desk

The organization determines it for itself independently. When calculating, the company’s field of activity, the approximate amount of daily revenue, etc. are taken into account. All cash in excess of the established limit must be collected into the bank.

Cash payment limit

The maximum permissible limit for cash payments between organizations or individual entrepreneurs cannot exceed 100,000 rubles within the framework of one agreement. Moreover, this limit will remain in effect even after the expiration of the contract.

For example, a lease agreement was concluded between IP Volga and IP Berkut. After the expiration of the contract, IP "Berkut" still had a debt to IP "Volga" in the amount of 300 thousand rubles. Of the total debt of IP Berkut, only 100 thousand rubles. will be able to pay in cash.

Cash acceptance

If the organization does not belong to the category of small or micro business, cash is received through a cash receipt order (PKO). The employee accepting the document must check whether it contains:

- signatures of an accountant or manager;

- indicating the amount in accordance with the amount of cash actually transferred;

- availability of supporting documents, if such are indicated in the PQS.

Cash is counted piece by piece in the presence of the person transferring it. If the amount declared in the PKO coincides with the actual amount of cash, the cashier stamps and signs the receipt for the cash receipt order, and then hands it over to the person from whom the funds were received.

Cash withdrawal

When dispensing cash from the cash register, the cashier must check the cash receipt order (RKO) for the presence of:

- signatures of an accountant or manager;

- correspondence of the amount indicated in words with the amount indicated in the document in numbers.

In order to issue the cashier, the cashier must identify the recipient using an identification document (passport). The recipient, in turn, must sign the cash register, thereby confirming the receipt of funds.

Discipline required for a cash authority

Cash discipline includes a set of measures aimed at ensuring compliance with legislation and local documentation governing all cash transactions of the company.

This discipline includes:

- Timely and correct use of revenue accounting documentation

- Compliance with the norms of local acts regulating the operation of the cash register

Compliance with established settlement and residual limits- Implementation of legal norms when accounting for cash receipts

- Use of CCP only in good condition

- Ensuring the identity of indicators (one direction) in different reporting documentation

- Compliance with legal regulations when issuing cash register receipts or alternative documentation

Violations of the cash discipline established at the enterprise are grounds for bringing the guilty person to justice.

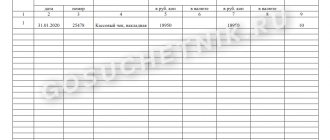

Procedure for preparing cash documents

The main documents that are involved in the process of maintaining cash discipline at an online checkout are PKO and RKO.

Receipt cash order

Records the fact of receipt of cash at the cash desk. The document contains the following information:

- household operation;

- receipt amount;

- tax on the amount deposited;

- documents attached to the PQS;

- code of the department in which the funds will be capitalized.

Account cash warrant

This document, according to its name, records the expenditure of cash. Mandatory information in this case is:

- expenditure;

- amount of expense;

- recipient;

- documents attached to the RKO. All specified documents are also registered in the PKO/RKO journal.

Abolished cash documentation

Today, all legal entities are switching to the use of online cash registers, which allow you to instantly transfer information about issued documents to the tax service, registers, etc. Before the introduction of the presented innovation, financial transactions of enterprises were accompanied by the creation of the following documents:

- Log of calls to equipment maintenance specialists

- Journal used by the cashier to conduct financial transactions

- Acts on changing the readings of cash register meters when it is put in for repairs and an act on the translation of such readings

- A journal for registering cash registers that are not related to the operator’s work in conducting cash transactions

- Help report

- Verification report on the amount of cash in the cash register

- Information about the proceeds, as well as about cash register counters

- The act of recording the transfer (return) of funds to the client

The use of an online cash register allows you to avoid paper duplication of the submitted list of documentation due to the automatic transfer of the specified information to the Federal Tax Service.

How is cash discipline checked?

Cash discipline is checked as part of on-site activities of the tax service.

The main aspects that the Federal Tax Service pays attention to:

- Algorithm for posting revenue, availability of uncapitalized funds;

- Compliance with the cash limit;

- Condition, serviceability and availability in the state. online cash register register;

- Compliance of cash documents with actual amounts;

- The fact of issuance/non-issuance of cash receipts to customers;

- The presence of large amounts issued on account for unreasonably long periods, etc.

Simplified procedure

Starting from June 1, 2014, individual entrepreneurs and small enterprises (number of employees no more than 100 people and revenue no more than 800 million rubles per year) are no longer required to set a cash balance limit at the cash desk.

In order to cancel the cash limit, it is necessary to issue a special order. It must be based on the Directive of the Bank of Russia dated March 11, 2014 No. 3210-U and must contain the wording: “Keep cash in the cash register without setting a limit on the cash balance” (sample order).

Limitation of cash payments

Another important rule of cash discipline is compliance with the limitation of cash payments between business entities (individual entrepreneurs and organizations) within the framework of one agreement in an amount of no more than 100 thousand rubles.

For settlements with individuals, this restriction does not apply. There is also no need to comply with this limit when issuing salaries, social benefits and accountable amounts to employees from the cash register (except for cases where the accountable person makes a transaction on behalf of the organization on the basis of a power of attorney).

Please note : cash proceeds cannot be used to repay loans, pay dividends or pay for real estate rent.

Money from the cash register for personal needs

Everything that an organization earns is its property. Therefore, even if there is only one founder in an LLC, he still does not have the right to dispose of the organization’s money at his own discretion. Accordingly, the founders cannot take cash from the cash register for their personal needs.

Individual entrepreneurs, unlike LLCs, have the right to take cash from the cash register or withdraw from a current account at any time. The amounts that an individual entrepreneur can spend on his personal needs are not limited (the most important thing is to avoid arrears in paying taxes and insurance premiums).

Note: if the individual entrepreneur has not issued an order canceling the maintenance of cash documents, then when receiving cash from the cash register, he needs to draw up a cash settlement with the wording: “Issue of funds to the entrepreneur for his own needs” or “Transfer to the entrepreneur of income from current activities.”