The general ledger in accounting performs the function of a single consolidated register. It contains summary information for all accounting accounts that are provided for in the company’s working chart of accounts. Data is reflected by month and for the full reporting year. The basis for filling out the book are order journals (account registers), which reflect the initial balances as of January 1, credit and debit turnover for the period with the resulting final balance.

When maintaining the general ledger, it is necessary to compare the total amounts of debit and credit entries (turnovers and balances are compared separately). If the entries in the document are made correctly, the book totals for debit and credit will be identical; if discrepancies are identified, it is necessary to check the correct posting in the general ledger and the correct compilation of the original accounting registers.

General ledger in accounting: sample filling

The form of the general ledger is approved by business entities in their accounting policies. In accordance with Art. of the Law on Accounting dated December 6, 2011 No. 402-FZ, each enterprise independently develops templates for accounting register forms (with the exception of public sector organizations). The structure of the document must contain the following data:

- name of the accounting register;

- name of the company on behalf of which the register is compiled;

- dates of opening and closing of the register, designation of the period for which the results are summed up;

- grouping of accounting objects with reference to the chronology of events;

- units of measurement and size of cost parameters;

- an indication of the positions of the persons responsible for maintaining the general ledger, a place to decipher the names of these employees.

The document can be issued on paper or electronically. When maintaining records using accounting programs, the general ledger is generated automatically. The accuracy of the information entered must be confirmed with the handwritten signatures of responsible specialists. Corrections in the paper register are permitted, but provided that the date of the amendments is indicated and the person who made the adjustment is identified.

The general ledger in accounting, filling it out, is necessary to systematize the entire complex of business transactions carried out by the enterprise during the reporting year. This document allows you to obtain summarized information about the results of activities, which is important when preparing reports. From the general ledger, the accountant can transfer data on the opening and closing balances for any of the accounting accounts to the balance sheet. An additional function of the register is to independently verify the correctness of accounting.

How to create a General Ledger in 1C 8.3

Open the General Ledger (Reports - General Ledger).

Please indicate:

- Period— period of report generation;

- Organization— the organization for which the report is being compiled.

The report will be generated based on accounting data by clicking the Generate .

Click the Show settings to configure the desired report format for yourself. Let's take a closer look at how to do this.

Setting up data grouping

On the Grouping you can set:

- output of data on subaccounts and subaccounts of corresponding accounts;

- frequency of report generation.

If the By subaccounts and By subaccounts of correspondent accounts , the information in the report will be displayed in the following form:

If the frequency is set, for example, “By months” , the data in the report will be generated broken down by the selected period:

Setting up an expanded balance

You can display the expanded balance in the report:

- by account;

- by subaccounts;

- according to subconto.

To do this, on the Expanded balance , select the appropriate checkboxes.

The report for the selected account displayed detailed information on the debit and credit balances:

Setting up report design

To ensure that the report meets the legal requirements for the design of accounting registers, go to Show settings and on the Design , select the following checkboxes:

- Heading,

- Signatures;

- Unit.

To print data for each account (subaccount) on a separate sheet, check the Split into sheets .

Saving report settings

The report settings can be saved.

Click the Show settings to open the report settings. Save settings button Saving report settings form , specify a name for the new setting and click the Save .

Period field when saving the settings , then the next time you select the General Ledger , it will be generated for the same “old” period.

To avoid errors, we recommend saving the report settings without the Period .

You can open saved settings by clicking the Select settings from the report settings form.

General ledger structure

Each account has a separate page in the general ledger. The debit turnover on the account is indicated broken down by corresponding accounts, and the credit turnover is transferred without breakdown - the total amount for the month (these data are reflected in detail in the order journal of the corresponding account).

When filling out the general ledger, information is reflected only for synthetic accounts without breakdown into subaccounts. Analytics is recorded in other order journals, the task of the general ledger is to summarize the data.

For example, in the reporting month there is data on accrued and paid taxes:

- from the income of individuals (account 68/NDFL);

- for added value (invoice 68/VAT);

- income tax (account 68/NNP).

In accounting, they are reflected in account 68, but separately from each other in different subaccounts. In the general ledger, turnover for all specified taxes will take place in one line of account 68. Detailing by dates of accrual and payment, by type of tax obligations is reflected not in the general ledger, but in the corresponding register.

The opening balances reflected in the book at the beginning of the year must coincide with the turnover indicators at the end of the previous year. The balance at the end of the period indicated in the general ledger must be identical to the data in the balance sheet for the reporting period in question. In the general ledger, it is recommended to indicate the number of accounting registers (order journals) from which account data was transferred.

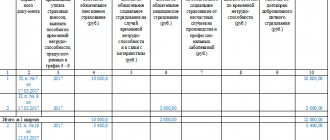

Sample of filling out a sheet of the general ledger for account 50:

Management and assignment

The general ledger is a summary document (a kind of journal) that is filled out within one calendar year. Maintaining a document for a longer period of time, for example, for several years, is not allowed.

All records are kept in strict chronological order, starting in January and ending in December of the reporting year. The general ledger must contain all the information on all synthetic accounts available at the enterprise (and of any form of ownership). That is, the general ledger is a reflection of all economic activities of the organization.

Why do you need a general ledger for an accountant?

First of all, for an accounting employee, this document is necessary to double-check his own work, since when entering information, all already processed operations are reviewed again.

That is, all current operations within one calendar year are carefully studied, information on them is posted in various audit journals (the initial stage of verification), and then all the same information is entered into this document (the final stage of verification).

For accounting, the importance of this kind of journal is difficult to overestimate - after all, its maintenance is the result and assessment of the professional activities of employees of the financial department.

Why is this document needed for the enterprise?

Its main purpose is to obtain information for drawing up a balance sheet. It includes information on opening and closing balances, as well as current turnover for each individual synthetic account. Naturally, the balance sheet of an enterprise is the most important indicator of its production and financial activities, and the fact that it goes through several stages of verification is an invaluable aid in analyzing annual work.

Procedure for filling out the General Ledger

This book contains reporting documents, their names, numbers of all accounts, including the cash register. Then fill in the amounts for the calculations carried out by the company for the period of the financial statements. The next part of the work is calculating the total amount of debit and credit, the data is entered into the necessary columns of the ledger, their correctness is checked by numbers, including checking the filling out forms.

All these instructions must be approved by management, who need to know how to properly maintain documents.

The general ledger must be prepared according to the instructions.

Simplified taxation system

The book of accounting for income and expenses under the simplified tax system consists of a title page and four sections. The following table shows the features of filling out the Book depending on the taxable object chosen by the individual entrepreneur.

Table 1. Sections of KUDiR for the simplified tax system and their completion when choosing different objects of taxation

| Chapter | Who fills it in and what does it reflect? | |

| Object " Revenue " | Object " Income - Expenses " | |

| Title page | Basic information about the entrepreneur: full name, address, contact details, TIN, object of taxation, bank details | |

| Section I | Income and expenses for the first quarter, half year, 9 months and year on a cumulative basis | |

| Fill in columns 1-4 | Fill in columns 1-5 | |

| Section II | — | Calculation of expenses for the acquisition of fixed assets and intangible assets, which are taken into account in the tax base |

| Section III | — | Calculation of the amount of loss that reduces the tax base |

| Section IV | The amount of insurance premiums paid by the entrepreneur and some other expenses specified in paragraph 3.1 of Article 346.21 of the Tax Code of the Russian Federation, reducing the amount of tax | — |

An example of filling out Section I is in the following image.

This is how to fill out Section 1 KUDiR IP on the simplified tax system with the object Income-Expenses

book - assistant accountant for reporting

book – a register that combines accounting information of the entire organization. This document contains accounts for one year. During such a period, a huge amount of information appears that cannot be calculated manually. It is recommended to use specialized software.

Of course, the general ledger can be maintained in Excel, but this is also inconvenient. Thanks to the program, you can make all calculations in one click. Any change is immediately reflected in the results. It is noteworthy that the program is capable of creating both a standard general ledger and free reports.

Key Features

- It is possible to view an example of filling out forms;

- Work is underway with monthly accounts;

- Work is carried out with subaccounts;

- It is possible to upload to Excel;

- Breaking down the results into debit and credit;

- Calculation and display of balances;

- It is possible to edit already entered data;

- Document printing is possible.

Advantages

The accountant's book program has several advantages over its competitors and reporting in Excel spreadsheets. As everyone knows, the most difficult and time-consuming process is filling out a chart of accounts. To make things easier for the accountant, the developer has added a sample form. Of course, this is not a complete report, but it can be used to create a proper general ledger.

For convenience, the program divides the journal into debit and credit. This will make it easier for an accountant to keep records. It is also possible to view totals and balances.

Filling out the general ledger can be done on separate accounts. To do this, just select the account you are interested in in the navigation panel, and then enter the correct data. It is important to note that accounts can be added and edited. This is very convenient because adjustments can be made to accounts.

An indisputable advantage is that the program can be downloaded for free. It is worth noting that the application interface is Russian, which means that even a novice accountant can handle the program.

Sometimes there are cases when the accounting form has already been filled out, but new information appears. Don’t be upset, because the “book” program allows you to edit documents. In this case, all adjustments are immediately reflected in the results.

Flaws

Unfortunately, like any book program, it has several disadvantages. To fill out the journal, you must have accountant skills. It will be difficult for the average user to understand the correctness of filling out accounts, credits and debits.

Although all calculations are carried out automatically, the form will have to be filled out manually. Since you have to enter a huge amount of data, difficulties may arise. Of course, you can use samples, but they are incomplete.

How the program works

Anyone can download and install the application. When the program is launched, you will see a form divided into several zones:

- Navigation bar;

- Block with months;

- The main block of accounting (debit and credit);

- The column on the right displays the total and balance.

After creating the report, first fill in the year and select the month. You also need to select a subaccount to enter information. Now you need to fill out the invoice. For a debit, indicate the month, amount and from which credit account the debit will be made. To save the recording, you must click the “Record” button.

Don't forget about the balance at the beginning of the year. First you need to click on the appropriate button, and then specify:

If necessary, check the boxes next to debit and credit. When all fields are filled in, you need to click on the “Save” button. Please note that this procedure is done only once at the beginning of each year.

In addition to maintaining accounting records, it is possible to customize the program. You can change:

- Title color;

- Specify the main color;

- Change font.

If desired, you can change the settings of Excel tables. After making changes, all that remains is to click “OK”. It should be noted that on the navigation bar there is a button to export to excel, as well as send to print.

General Ledger Sample

Contents The general ledger is one of the main annual synthetic accounting documents for all accounts used by the enterprise.

It is the most general form of operational economic activity.

The book provides an opportunity to obtain a complete understanding of production and financial processes, and also identifies possible violations that may arise as a result of the company's economic activities. All financial statements for the year are also completed based on the data entered in the general ledger.

Officially, this document appeared in 1960 and since then has been used in almost all areas of business. There are some organizations that do not use a general ledger.

They make do with order journals, summarized in a checkerboard sheet, the data from which is then transferred to the balance sheet report. But this is a more labor-intensive and not very convenient procedure.

Features of the structure and filling of the general ledger The structure of the ledger is made up of separate accounts, which display the final monthly, quarterly and annual data on them. Each sheet of the book is formed for one specific account. On the sheet you need to consider:

- account turnover from credit to debit;

- overall loan results;

- debit and credit balance.

- general flow rate results;

The general ledger displays credit turnover by transferring the amount for each month.

Corresponding accounts are not subject to breakdown, since all data on them is already available in the order.

Document storage

The general principles for storing documents are reflected in Art. 29 of the Accounting Law. An economic entity must ensure safe storage conditions for accounting documents and their protection from changes for a period established in accordance with the rules for organizing state archival affairs, but not less than five years after the reporting year.

When changing the head of an economic entity, the transfer of accounting documents must be ensured in accordance with the procedure established by the institution itself.

When organizing the storage of documents on the activities of an institution, it is also necessary to be guided by the provisions of the Tax Code of the Russian Federation and Order of the Ministry of Culture of Russia dated August 25, 2010 No. 558 “On approval of the List of standard management archival documents generated in the course of the activities of state bodies, local governments and organizations, indicating storage periods” , where their shelf life is indicated.

For example, according to the above document, the charters and regulations of the organization (standard and individual) must be kept:

- a) at the place of development and (or) approval - constantly;

- b) in other organizations - three years (after replacement with new ones).

To documents of permanent storage (until liquidation

organizations) include: consolidated annual reporting, analytical documents thereto; transfer, separation, liquidation balance sheets; consolidated annual reports on the implementation of budget estimates; reports on the transfer of funds to state extra-budgetary funds; documents on the revaluation of fixed assets and assessment of the value of property; annual tax returns.

Personal payroll accounts of employees and documents confirming the use of benefits must be stored for 75 years.

How often should the General Ledger (form 0504072) be printed in a federal budgetary institution (the institution does not provide for storage of accounting registers in the form of electronic documents containing an electronic signature)?

July 26, 2017

Having considered the issue, we came to the following conclusion: If the institution does not have the ability to store accounting registers in the form of electronic documents containing an electronic signature, the General Ledger (form 0504072) must be generated and printed monthly.

Rationale for the conclusion: The general ledger (form 0504072) is one of the accounting registers, the form and guidelines for the formation of which in accordance with the requirements of Part 5 of Art. 10 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting” (hereinafter referred to as Law N 402-FZ) was approved by Order of the Ministry of Finance of Russia dated March 30, 2015 N 52n (hereinafter referred to as Order N 52n). According to the provisions of the Methodological Instructions, the General Ledger (form 0504072) is maintained by institutions on a monthly basis. In the General Ledger (form 0504072), the total turnover for the period from the beginning of the year is calculated. Accordingly, when forming the General Ledger (form 0504072) by the institution, in columns 7 “Turnover for the period on debit” and 8 “Turnover for the period on credit”, the turnover on the corresponding accounting accounts for the month must be reflected. According to the provisions of paragraphs. 11, 19 of the Instructions, approved by order of the Ministry of Finance of Russia dated December 1, 2010 N 157n, the formation of accounting registers on paper, in the absence of the possibility of storing them in the form of electronic documents signed with an electronic signature, and (or) the need to ensure their storage on paper, can be carried out at intervals established within the framework of the formation of accounting policies by the accounting entity. We believe that within the framework of the accounting policy, the frequency of formation of accounting registers can be established, the frequency of formation of which is not regulated by the provisions of Order No. 52n. The establishment by an institution of the frequency of formation of the General Ledger (form 0504072), different from that established by Order No. 52n, will not ensure compliance with the requirements of the Methodological Instructions regarding the formation of indicators in columns 7 “Turnover for the period on debit” and 8 “Turnover for the period on credit”.

We also recommend that you familiarize yourself with the following materials: — Encyclopedia of solutions. Systematization of accounting data. Transaction logs. General ledger (for the public sector). — Encyclopedia of solutions. Accounting registers used by government agencies.

Answer prepared by: Expert of the Legal Consulting Service GARANT Olga Emelyanova

Response quality control: Reviewer of the Legal Consulting Service GARANT, Advisor to the State Civil Service of the Russian Federation, 2nd class Anna Shershneva

Results

An extract from the cash book may be requested by the bank (to check the expenditure of withdrawn cash) or the Federal Tax Service. There is no specially designed register. The taxpayer has the right to develop a document in free form. We have provided a sample extract from the cash book in this material.

You may need information on how to design and complete your own tax and accounting ledgers. Read more about this in the articles:

- “How to independently develop tax registers for income tax?”

- “Tax accounting registers for VAT: we fix them in accounting policies”

- “How is the personal income tax register maintained?”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.