If he does not do this, the buyer will lose the right to deduct VAT.

An invoice is a document that serves as the basis for accepting the VAT amount for deduction. According to paragraph 3 of Article 169 of the Tax Code of the Russian Federation, an invoice is issued:

- taxpayers for transactions carried out in relation to the object of taxation (Article 146 of the Tax Code of the Russian Federation);

- persons exempt from VAT under Articles 145 and 145.1 of the Tax Code of the Russian Federation (clause 5 of Article 168 of the Tax Code of the Russian Federation);

- tax agents for purchases on the territory of Russia from foreign suppliers (subclauses 1 and 2 of Article 161 of the Tax Code of the Russian Federation) or when using state property (clause 3 of Article 161 of the Tax Code of the Russian Federation);

- VAT payers on received advances and when changing the price or volume of shipments already made (clause 3 of Article 168 of the Tax Code of the Russian Federation);

- non-payers of VAT when selling on their own behalf or when re-issuing invoices (subclauses 1 and 3.1 of Article 169 of the Tax Code of the Russian Federation).

The established forms of the invoice form and the procedure for filling it out are contained in Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 (hereinafter referred to as the Rules).

The information required to fill out an invoice consists of a certain set of indicators (subclauses 5, 5.1, 5.2 of Article 169 of the Tax Code of the Russian Federation):

- details (number and date);

- information about the seller and buyer;

- the currency in which the numerical data of the document is reflected;

- unambiguous name of the object of sale;

- the total sale price without taxes and with taxes, the amount of taxes, the VAT rate, if there is a tax;

- signatures of persons entrusted with this right.

Significant errors in the invoice

An invoice in which (clause 2 of Article 169 of the Tax Code of the Russian Federation) is completely unsuitable for deduction:

- there is no information about individuals or this information is fundamentally incorrect;

- it is impossible to unambiguously determine the object of sale;

- the sales price, rate and amount of tax are missing or given with errors (see, for example, the letter of the Ministry of Finance of Russia dated April 19, 2017);

- the currency is missing or incorrectly indicated (see letter of the Ministry of Finance of Russia dated March 11, 2012 No. 03-07-08/68).

These defects prevent a reliable determination of the basic data included in the invoice. Therefore, tax deduction based on documents with such errors is impossible.

This means that if in the invoice the cost of the purchased goods and, accordingly, the amount of VAT are indicated incorrectly (including with arithmetic and technical errors) or their indicators are missing, then a deduction on such an invoice is not provided.

note

Some courts (see Resolution of the Federal Antimonopoly Service No. F03-2116/2014 of June 10, 2014 in case No. A51-17093/2013) believe that the signing of invoices by unidentified persons is an independent basis for refusing to accept VAT tax deductions. However, there are also opposing court decisions in which the arbitrators recognized the signing of invoices by an unidentified and unauthorized person as an insignificant circumstance (see Resolution of the AS SKO dated June 11, 2015 No. F08-3452/2015 in case No. A32-26952/2012).

Errors in invoices that prevent deductions: 10 dangerous details

The S/F must be signed by the head of the form, as well as by the accountant or other persons. Based on an order or power of attorney, you can authorize an employee to sign an invoice. In the case where the S/F was issued by the entrepreneur, he either signs the papers himself or transfers these powers by proxy.

We recommend reading: Okey Service Unit

Error 1: missing TIN or filling it out incorrectly

The name of goods, services or work is written by the supplier in column 1 of the S/F. If inspectors fail to identify the goods, an error in this detail will be dangerous. In confirmation of this there is a letter from the Ministry of Finance of Russia dated 08.14.15 No. 03-03-06/1/47252.

Tax authorities pay attention to the absence of this detail in the advance invoice if VAT is claimed for deduction on such an invoice. In this case, even during a desk audit, but before the tax authority makes a decision, the taxpayer has the right to enter information about the details of the payment order by hand. Since such information is not related to changes in the cost, volume and other indicators of the business transaction performed.

Minor errors in the invoice

Some errors in the invoice are not grounds for denial of the VAT deduction highlighted in this document. These are errors that do not prevent inspectors from identifying during a tax audit (Clause 2 of Article 169 of the Tax Code of the Russian Federation):

- seller, buyer of goods (works, services), property rights;

- name of goods (works, services), property rights;

- their cost;

- tax rate;

- the amount of VAT charged to the buyer.

Such “non-critical” defects include, in particular, the date the invoice was issued by the seller, as well as obvious typos in information about the supplier and buyer, the absence of a number, the inclusion of additional details in the invoice, etc.

Thus, with regard to such details as the address, officials are not very strict. It can be written in the invoice with abbreviations (partly in capital letters and partly in small letters), since such address abbreviations are not prohibited in the Unified State Register of Legal Entities (see letter of the Ministry of Finance of Russia dated October 11, 2017 No. 03-07-09/66329).

If the address of the seller and buyer from the register does not indicate a country, the seller can independently add the words “Russian Federation”, “Russia” or “RF” to the address.

Also, if the words “district”, “street”, “house” are not written in the address, or the words “city” and “street” are written in abbreviated form, this will not be considered an error due to which the tax office will refuse to deduct VAT. The deduction of VAT is also not prohibited when replacing the word “premises” with the word “office”.

As for such details as checkpoint, it, unlike the TIN, which is indicated here, is not among the mandatory invoice details listed in paragraph 5 of Article 169 of the Tax Code of the Russian Federation.

That is, these are defects that will not lead to denial of deduction.

Invoices: we make corrections

Re-invoicing In practice, sellers do not always correct a “defective” invoice in accordance with the Rules for maintaining received and issued invoices. Often they simply issue a new invoice with the same details or a new number and date. Financiers have repeatedly spoken out against re-issuing invoices as a way to eliminate errors in this document 19 . Some arbitration courts support this point of view of officials 20 . According to the judges, there are no grounds for deducting VAT due to the fact that there is a discrepancy with the procedure for making corrections to primary accounting documents. The judges also pointed out that the rules of law governing the procedure for making changes to invoices do not provide for the possibility of re-issuing them with new ones 21 . But in the overwhelming majority, arbitration courts rule in favor of companies, noting that neither the Tax Code nor the Rules prohibit making corrections to a “defective” invoice, including by replacing it with a document drawn up in the prescribed manner 22 . At the same time, the absence of a date for making corrections in the newly submitted invoices does not entail a violation of the requirements of paragraphs 5, 6 of Article 169 of the Tax Code 23 . Please note that re-issuing an invoice is sometimes the only possible way to make corrections. For example, in the case of correcting a large number of errors, when there is simply not enough free space in the invoice to make corrections. Nevertheless, the right to deduction by re-issuing an invoice will most likely have to be defended in court.

Basic rules for making corrections

Changes to the Purchase Ledger Once a corrected invoice has been received from the seller, the buyer must make appropriate adjustments to the purchase ledger. To do this, in an additional sheet of the purchase book for the tax period in which the invoice was registered before corrections were made to it, he needs to make an entry about the cancellation of the erroneous invoice 24. In this case, in the “Total” line of the additional sheet, you need to transfer the total data from the purchase book for the period in which the invoice to be canceled was registered, and in the next line - the data of this invoice itself. Then, from the “Total” line indicators, you need to subtract the data of the invoice to be cancelled. The result obtained is reflected in the “Total” line of the additional sheet of the purchase book and is subsequently used to make changes to the VAT return for the tax period to which the error relates. An additional sheet is filed with the purchase book for the tax period in which the erroneous invoice was originally registered. According to officials, changes to the purchase book must be made regardless of whether the error in the tax amounts is corrected or only in the invoice details 25 . All that matters is that the adjustment is made to an invoice that was previously recorded in the purchase ledger.

We recommend reading: All Postings in Budget Accounting in 2021

In this case, taxpayers retain the right to a deduction, since inspectors can find out the name of the goods from the specified agreement (resolution of the Tenth Arbitration Court of Appeal dated 04/09/12 No. 10AP-301/12).

Errors in buyer details

To avoid any doubt about the identification of the buyer who will accept the amount of “input” tax for deduction, information about him must be correctly indicated in the invoice. We are talking about the following details: name (line 6); address (line 6a); taxpayer identification number (line 6b).

Let us remember the rules by which these details are filled out.

On line 6 indicate the full or abbreviated name of the buyer in accordance with the constituent documents.

If the goods are supplied to separate divisions of buyers, then line 6 indicates the name of the parent organization (letter of the Ministry of Finance of Russia dated May 4, 2016 No. 03-07-09/25719).

Minor typos (capital letters instead of lowercase letters and vice versa, extra dashes, commas, etc.), which do not interfere with the identification of the buyer, are not grounds for refusal to deduct (letter of the Ministry of Finance of Russia dated May 2, 2012 No. 03-07-11/130).

But if, instead of the name of the organization, the full name of the employee is indicated, the buyer is deprived of the right to deduction (letter of the Federal Tax Service of Russia dated January 9, 2017 No. SD-4-3 / [email protected] ).

The location of the buyer is indicated on line 6a in accordance with the constituent documents.

If the invoice indicates an outdated legal address of the buyer, the right to deduction is retained (letter of the Ministry of Finance of Russia dated 08.08.2014 No. 03-07-09/39449). The actual address, which differs from the legal address, can be indicated additionally (letter of the Ministry of Finance of Russia dated December 21, 2017 No. 03-07-09/85517).

Abbreviations, replacing capital letters with lowercase letters, and rearranging words in street names are minor changes. They do not prevent deductions (letter of the Ministry of Finance of Russia dated January 17, 2018 No. 03-07-09/1846).

If the goods are supplied to separate divisions of buyers, then line 6a indicates the location of the parent organization (letter of the Ministry of Finance of Russia dated May 4, 2016 No. 03-07-09/25719).

If the goods are delivered to separate divisions of the buyer, then in line 6b you must indicate the TIN of the parent organization and the checkpoint of the division (letter of the Ministry of Finance of Russia dated May 4, 2016 No. 03-07-09/25719).

If the buyer's TIN and KPP are indicated incorrectly or not indicated at all, tax authorities will try to deprive the buyer of the right to deduction.

The courts have a different opinion. The buyer’s right to deduction is retained, since the buyer’s TIN is known to the tax authorities (Resolution of the Federal Antimonopoly Service of the Moscow District dated September 28, 2010 No. KA-A40/11365-10), and the checkpoint is not a mandatory requisite mentioned in paragraph 5 of Art. 169 of the Tax Code of the Russian Federation (Resolution of the Federal Antimonopoly Service of the Moscow District dated February 27, 2010 No. KA-A40/1164-10).

Name of goods, works and services

Abbreviations in the name

Recently, complete clarity has emerged as to whether it is possible to indicate the abbreviated name of the product on the invoice.

The Russian Ministry of Finance clarified that such a reduction does not prevent tax authorities from identifying the seller, buyer, price and other parameters of shipment. Consequently, an incomplete name of the product is not a reason for refusing a deduction (letter dated 05.10.11 No. 03-07-09/10). Despite this, tax authorities use reductions in invoices during audits as a reason to cancel deductions. But the courts invariably side with taxpayers and recognize that incomplete denomination is possible both for goods (resolution of the Federal Antimonopoly Service of the Moscow District dated 01/20/12 No. F05-14309/11) and for work (resolution of the Tenth Arbitration Court of Appeal dated 04/09/12 No. 10AP -1295/12).

Link to contract

There are special cases when in the corresponding line of the invoice, instead of the name of the work or services, a link to the contract is given. Officials believe that this option for issuing an invoice contradicts Article 169 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of Russia dated January 22, 2009 No. 03-07-09/02). Previously, the courts agreed with officials (see, for example, the resolution of the Federal Antimonopoly Service of the East Siberian District dated March 19, 2009 No. A33-17604/07-F02-936/09).

But after the new version of paragraph 2 of Article 169 of the Tax Code of the Russian Federation came into force, judges began to make decisions in favor of organizations and entrepreneurs. One of the main arguments is as follows: since the details of the contract are indicated in the invoice, nothing prevents the auditors from opening the contract and finding out the exact name of the work (resolutions of the Tenth Arbitration Court of Appeal dated 04/09/12 No. 10AP-301/12 and the Federal Antimonopoly Service of the Moscow District dated 08/24 .11 No. Ф05-8167/11).

Errors in naming

Another reason for claims are errors made by suppliers when indicating the names of goods, works or services on the invoice. Arbitration practice here is ambiguous: sometimes the courts support the tax authorities, sometimes the taxpayers.

Thus, an organization won in court by deducting VAT on an invoice in which the contractor incorrectly indicated the object of electrical installation work. The text of the court decision states: “An erroneous indication of the objects on which the work was performed cannot entail a refusal to deduct, since this does not prevent the tax authority from establishing the amount of tax charged to the applicant by the contractor” (Resolution of the Federal Antimonopoly Service of the Volga District dated 02/03/12 No. A65 -6805/2011).

But there are also decisions in favor of inspectors. One of them is the decision of the Twentieth Arbitration Court of Appeal dated November 28, 2011 No. 20AP-4364/11. The judges considered a situation where the invoice stated “garage repair work,” and the certificate of completion stated “railroad repair.” The court held that the contractor should have properly corrected the invoice, otherwise the right to deduction was lost.

Considering the contradictory nature of judicial practice, it is better for accountants to prevent a conflict in advance and ask the supplier to issue a corrected invoice in accordance with the rules approved by Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137. If the invoice was issued before April 1, 2012 on the old form, corrections can be included in the original document, certified by the signature of the manager and the seal of the seller (clause 29 of the rules approved by Decree of the Government of the Russian Federation of December 2, 2000 No. 914).

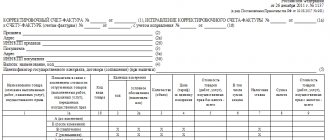

Invoice: adjustment or corrected?

If there are significant errors in the original invoice, a corrected document is drawn up. Significant errors prevent the buyer from exercising the right to deduct “input” VAT.

If the error is not recognized as such, changes may not be made to the invoice (clause 7 of the Rules).

Let us remind you that an adjustment invoice is issued when the cost of goods already shipped, work performed, services rendered, or transferred property rights is changed. A price change is possible if:

- after the goods are shipped, their price is changed;

- specify the quantity of goods shipped.

In addition, before issuing an adjustment invoice, the seller must:

- notify the buyer of changes in the cost of shipped goods;

- receive from the buyer a document as a fact of notification of a change in the terms of the transaction, confirming his consent. This could be a contract, agreement or any primary document.

As a rule, in the event of a technical error, such documents are not issued. And since the supplier will not have a single document confirming the change in the price of the goods, he cannot issue an adjustment document. He will have to issue a corrected invoice.

Errors in Invoices Do Not Prevent Deduction 2021

The presence of typos in the buyer's name in the invoice (lowercase letters are replaced by capital ones or vice versa, the presence of extra symbols (commas, dashes), etc.), which do not interfere with identifying the necessary information, cannot serve as an obstacle to accepting tax amounts for deduction.

Errors in invoices that do not interfere with obtaining a VAT deduction

The right to deduction is retained if the indicated signatures are placed later, during the inspection, for example, (Resolution of the Federal Antimonopoly Service of the Moscow District No. KA-A41/1262-11 dated 03/04/11). Full name decoding is not a mandatory detail specified in clause 5 of Art. 169 of the Tax Code of the Russian Federation, therefore its absence does not deprive the taxpayer of the right to a deduction (Resolution of the Federal Antimonopoly Service of the Volga District No. A65-17919/2021 dated 04/19/12). If there is no chief accountant on staff, his signature is not required (resolution of the Ninth Arbitration Court of Appeal No. 09AP-20994/2021 dated 09.23.11).

It is important to keep in mind that corrected and adjusted invoices are prepared in different situations. The seller (contractor, performer) issues an adjustment invoice if the cost of previously shipped goods (work performed, services provided) changes due to an increase or decrease in price or clarification of quantity (volume). Moreover, in order to issue this invoice, the parties draw up a document confirming their agreement to change the cost of goods, work or services. The adjustment invoice must be issued within five days from the moment the buyer signs the document (clause 3 of Article 168 and clause 10 of Article 172 of the Tax Code of the Russian Federation). If arithmetic or technical errors are detected in the indication of cost, as well as other shortcomings that do not affect the total cost of goods, work or services, corrected invoices are drawn up. This is also confirmed by the Federal Tax Service of Russia in letter dated August 23, 2021 No. AS-4-3/ [email protected]

The courts make both positive and negative decisions for taxpayers. Let's start with the negative ones. In particular, the resolution of the Federal Antimonopoly Service of the Central District dated 04/05/2021 No. A68-2733/11 states the following. The indication in invoices of TINs that are assigned to other taxpayers or are fictitious indicates that these documents do not comply with the requirements of paragraph 5 of Art. 169 of the Tax Code of the Russian Federation. Therefore, it is unlawful to deduct VAT on such invoices. Similar arguments are also set out in the decisions of the Federal Antimonopoly Service of the Central District dated 07/18/2021 No. A62-3966/2021 and the Volga District dated 02/04/2021 No. A55-1176/2021.

Can I get a deduction on a corrected invoice?

In the corrected invoice, which the seller draws up in case of detection of significant errors, indicate the serial number and date of the invoice drawn up before the correction was made to it (clause 1, 7 of the Rules).

Therefore, the corrected invoice must be prepared using the form in effect on the date of the original invoice.

The corrected invoice drawn up by the seller upon discovery of a significant error and issued to the buyer must be registered in the sales book in the manner prescribed by paragraph 11 of the Rules.

Thus, the Ministry of Finance of Russia has once again confirmed its position: those errors in invoices that do not prevent tax authorities from identifying the seller of goods (works, services, property rights) are not grounds for refusal to deduct VAT (clause 2 of Article 169 Tax Code of the Russian Federation).

Expert “NA” S.M. Lvovsky