The legislative framework

Article 169 of the Tax Code of the Russian Federation

An invoice is a document on the basis of which the buyer can accept the provided property rights, goods or services, the amount of tax contributions in the prescribed manner. Such a document can be prepared in paper or electronic form.

Invoices can be drawn up in digital form if there is mutual agreement between the parties to the transaction, as well as the possibility of using appropriate technical devices to familiarize themselves with the content of the completed documentation.

In essence, an invoice is a type of accounting documentation that confirms the fact that certain goods have been shipped, or specific services have been provided, taking into account their cost. Such certificates are needed to certify the amount of VAT on the sale of products or certain services and to confirm the purchase, as well as input VAT.

The content of the invoice consists of books in which transactions are recorded and VAT is taken into account in the territorial offices of the tax service. An invoice is provided to the buyer when he receives goods or certain services from the seller.

There are two main types of invoices:

- The standard is set by the seller when goods are shipped or services are provided after the agreed amount of means of payment has been paid in full.

- An advance invoice is issued upon making an advance payment. Information about the senders and recipients of the cargo is never indicated in such documents. However, such a certificate must always contain information regarding settlement and payment documentation.

- The basic rules for issuing an invoice are specified in Art. 169 of the Tax Code of the Russian Federation.

Preparation of invoices

Since when exactly can an organization not accept VAT refunds on invoices that do not indicate: payment order number, checkpoint, decryption of signatures of the manager and chief accountant?

According to paragraphs 1 and 2 of Art. 169 Tax Code of the Russian Federation

An invoice is a document that serves as the basis for accepting the presented VAT amounts for deduction or reimbursement.

Invoices compiled and issued in violation of the procedure established by paragraphs 5 and 6 of Art. 169 Tax Code of the Russian Federation

, cannot be the basis for accepting VAT amounts presented to the buyer by the seller for deduction or refund.

Failure to comply with invoice requirements not provided for

in paragraphs 5 and 6 of Art.

169 of the Tax Code of the Russian Federation cannot be a basis for refusing to accept for deduction the amounts of tax presented by the seller.

According to paragraph 5 of Art. 169

The invoice must indicate, in particular,

the number of the payment document

in case of receipt of advance or other payments for upcoming deliveries of goods (performance of work, provision of services).

This norm is valid from the date of entry into force of part two of the Tax Code of the Russian Federation, that is, from January 1, 2001

.

Please note that VAT payers have been required to prepare invoices since January 1, 1997

. (Clause 9 of the Decree of the President of the Russian Federation dated 05/08/1996 No. 685).

The Government of the Russian Federation, in pursuance of this Decree of the President of the Russian Federation, by Decree No. 914 of July 29, 1996, approved the Procedure for maintaining journals of invoices for calculations of value added tax.

In Appendix No. 1

The invoice form

is provided for the Procedure for maintaining invoice journals for value added tax calculations .

On line 4

“To payment and settlement document No. ______ dated _____” when making payments using settlement documents to which an invoice is attached, it was necessary to indicate

the details of the settlement document

: its number and date of preparation.

Thus, the details of payment and settlement documents in invoices had to be indicated from the moment the invoices themselves were introduced

, that is, from January 1, 1997.

Moreover, from January 1, 2001

The number of the payment and settlement document must be indicated

only

if payment for goods (work, services) preceded their shipment.

According to paragraph 5 of Art. 169 Tax Code of the Russian Federation

The invoice must also include the name, address and identification numbers of the taxpayer and the buyer.

About the need to indicate the checkpoint

It is not stated either in paragraph 5 or in paragraph 6 of Art. 169 of the Tax Code of the Russian Federation.

Therefore, according to paragraph 2 of Art. 169 Tax Code of the Russian Federation

the fact that the checkpoint is not indicated in the invoice

cannot be a basis for refusing a tax deduction for VAT

.

However, in practice everything is much more complicated.

According to paragraph 8 of Art. 169 Tax Code of the Russian Federation

The procedure for maintaining a log of received and issued invoices, purchase books and sales books is established by the Government of the Russian Federation.

In pursuance of this provision of the Tax Code of the Russian Federation, the Government of the Russian Federation approved the Rules for maintaining logs of received and issued invoices, purchase books and sales books when calculating value added tax (Resolution of the Government of the Russian Federation dated December 2, 2000 No. 914).

Appendix No. 1 to the Rules of Maintenance... provides the form of the invoice

.

changes were made to this form of invoice

, according to which

line 2b

of the invoice must indicate not only the TIN, but also

the seller’s KPP

, and

line 6b

- not only the TIN, but also

the buyer’s KPP

.

Therefore, tax authorities, relying on the Rules of Conduct

..., object to the deduction of VAT amounts based on invoices that

do not indicate the seller’s (buyer’s) checkpoint

.

As we noted above, this position of the tax authorities contradicts paragraph 2 of Art. 169 Tax Code of the Russian Federation

.

In addition, clause 8 of Art. 169 Tax Code of the Russian Federation

determines that the Government of the Russian Federation establishes the procedure for maintaining

a log

of received and issued invoices,

purchase books

and

sales books

, but does not give the Government of the Russian Federation the authority to establish the form and composition of

invoice

.

To confirm their position, officials refer to the order of the Ministry of Taxes of the Russian Federation dated March 3, 2004 No. BG-3-09/178 “On approval of the procedure and conditions for assigning, applying, as well as changing the taxpayer identification number and forms of documents used for registration, deregistration of legal entities and individuals,” according to which, in addition to the taxpayer identification number

(TIN) in connection with registration with various tax authorities on the grounds provided for by the Tax Code of the Russian Federation,

the reason for registration code (KPP)

is used .

Hence, officials conclude that the checkpoint is an addition to the TIN

.

Therefore, the changes made to the invoice form by Decree of the Government of the Russian Federation dated February 16, 2004 No. 84 on the need to indicate the checkpoint do not contradict the norm

of paragraph 5 of Art.

169 of the Tax Code of the Russian Federation , according to which the INN of the taxpayer and the buyer is included in the details of invoices.

This conclusion was made by the Ministry of Finance of the Russian Federation in a letter dated 04/05/2004 No. 04-03-11/54.

Note that although the checkpoint is assigned to the organization in addition

to the TIN, but is a separate,

independent code

.

Therefore, from a legal point of view, the statement

that an invoice that does not indicate the checkpoint does not comply with the requirements

of paragraph 5 of Art.

169 of the Tax Code of the Russian Federation on the need to indicate the TIN

is incorrect

.

Since the inspectors do not agree with this, taxpayers are forced to defend the right to deduct VAT on the basis of invoices that do not indicate the checkpoint in court

.

With the need to decrypt signatures

in invoices – the same situation as with checkpoints.

According to paragraph 6 of Art.

169 of the Tax Code of the Russian Federation, an invoice is signed by the head and chief accountant

of the organization or other persons authorized to do so by an order (other administrative document) for the organization or a power of attorney on behalf of the organization.

When issuing an invoice by an individual entrepreneur

the invoice is signed by the individual entrepreneur

indicating the details of the certificate of state registration

of this individual entrepreneur.

Not a word about decoding signatures.

The detail “(full name)” (that is, signature decoding) was introduced into the invoice form by the above-mentioned Decree of the Government of the Russian Federation dated February 16, 2004 No. 84.

According to officials, the additions made to the invoice form regarding the need to decipher the signatures of the head and chief accountant of an organization or individual entrepreneur do not contradict

Tax Code of the Russian Federation.

However, the courts, as a rule, side with taxpayers.

For example, the Federal Antimonopoly Service of the Ural District, in resolution No. F09-2174/05-S2 dated May 24, 2005, noted that deciphering the signatures of supplier officials is not

mandatory details of the invoice by virtue of

clause 6 of Art.

169 of the Tax Code of the Russian Federation .

“Signature” requisite

both the personal signature and its

decoding

(initials, surname) are included, reference is made to GOST R 6.30-2003 “Unified documentation systems. Unified system of organizational and administrative documentation. Requirements for the preparation of documents”, adopted by Decree of the State Standard of the Russian Federation dated 03.03.2003 No. 65-st.

Thus, you should decide for yourself what is best for your organization: indicate the decryption of signatures (or, for example, checkpoint) in the invoice or prove your case in court.

We also note that the conclusions of officials regarding both the indication of the checkpoint of the taxpayer and the buyer, and regarding the need to decipher signatures on invoices, are not without logic.

So, if an organization’s TIN is assigned only once

, then the checkpoint is assigned

to each separate division

of the organization, as well as

when the location of the organization changes

.

This data is necessary for tax authorities to carry out tax control.

As for decrypting the signature

, then not only tax authorities are interested here, but also buyers.

After all, the Tax Code establishes that the invoice must be signed by the manager and chief accountant (or other authorized

faces).

If the signature is not decrypted, then it is impossible to understand who signed the invoice.

That is, from a legal point of view

It is not necessary to indicate checkpoints and decryption of signatures on invoices.

But from a logical point of view, the tax authorities’ demands also have the right to life.

To the question about the date of entry into force of Government Resolution No. 84 dated February 16, 2004

, to which the details “KPP” and “(full name)” were added to the invoice form, the tax authorities answer unequivocally.

In their opinion, this Resolution was officially published in the Collection of Legislation of the Russian Federation on February 23, 2004, and therefore comes into force on March 2, 2004.

However, the Constitutional Court of the Russian Federation in its resolution dated October 24, 1996 No. 17-P

indicated that the day on which the release of the “Collection of Legislation of the Russian Federation” is dated

cannot be considered the day of promulgation of the normative act

, since the date of release of the Collection of Legislation ... coincides

with the date of signing the publication for publication

, and, therefore, from that moment it is not yet possible to actually obtain information about the content of the normative act by its addressees.

In our case, the Decree of the Government of the Russian Federation introducing changes and additions to Resolution No. 914 was officially published in Rossiyskaya Gazeta on March 2, 2004.

This day should be recognized as the day of its official publication.

Therefore, invoices using the new form should be applied from March 10, 2004.

(7 days after official publication).

Why do you need to prepare such documents?

Invoice: sample

VAT is considered a very significant component of regular accounting reporting for every enterprise operating and providing tax contributions according to a standardized system. To use the right to deduct a specific tax, each agent will have to issue an invoice in accordance with the rules established by law.

Such documents are considered as basic for the application of the right of deduction, despite the fact that in fact they do not constitute evidence of acceptance and transfer of goods or provision of the service specified in the document. For this purpose, a TTN is specially drawn up, as well as a document indicating the acceptance or transfer of goods, documents or the provision of certain services.

Article 169 of the Tax Code of the Russian Federation states that an invoice can be defined as the main accounting document, since it contains a complete list of indicators necessary for this, about and the Tax Code of the Russian Federation.

In specially compiled journals, it is necessary to keep track of the existing list of invoices. When preparing tax reports, the combined VAT figures indicated in such journals are taken into account. Based on such reports, the total amount of tax contributions that must be paid to the state budget is determined.

Starting from 2021, all commercial organizations and enterprises interacting with invoices are required to comply with the established standards for filling out, and also use the form defined by the RF PP dated December 26, 2011 No. 1137 with adjustments from 2014.

Blog about taxes by Vladimir Turov

Good afternoon, colleagues.

A well-worn topic: your organization or you, as an individual entrepreneur, working for OSN, transferred money to a counterparty including VAT. All your supporting documents are in order, but for one reason or another you did not receive the invoice back. Question: can you deduct VAT?

Tax officials at every step, referring to Articles 171, 172 of the Tax Code of the Russian Federation , in particular, paragraph 2 of Art. 171, paragraph 1, art. 172 and at Art. 169 of the Tax Code of the Russian Federation, they tell us: “No, you can’t, because there is no invoice.” But you have fulfilled your obligation to transfer VAT, however, you cannot deduct it. But you gave the VAT and all supporting documents to the supplier, but you cannot deduct VAT.

Or another example: you issued money for reporting, your employee bought gasoline, fuel and lubricants, and brought you a sales receipt, where VAT is allocated. Or he provided an online check to KKM, where VAT is also highlighted as a separate line. But the tax authorities say: “No, you can’t deduct VAT because there is no invoice.” Fine. Here is a letter from the Ministry of Finance dated November 26, 2021 No. 03-07-11/91521 , which talks about the deduction of VAT when purchasing fuels and lubricants for cash without invoices.

“In the case of the acquisition of these goods (works, services) to carry out transactions subject to VAT, after registration of such goods (works, services) on the basis of invoices issued by sellers, documents confirming the actual payment of VAT amounts, as well as documents confirming the payment of VAT amounts withheld by tax agents”, VAT can be deducted if there are invoices.

What if there are no invoices? Let's look at the opinion of the Ministry of Finance and decide how much it corresponds to the logic of the Tax Code of the Russian Federation and judicial and arbitration practice. For example, according to paragraph 7 of Art. 171 of the Tax Code of the Russian Federation , VAT can be deducted without having invoices, if you went on a business trip, bought round-trip tickets, etc. In this case, you do not have an invoice, but you can deduct VAT on the basis of strict reporting forms issued to the posted employee, highlighting the VAT amounts on a separate line. And if you buy fuel and lubricants in cash, and you have a sales receipt with a separate line for VAT and a KKM receipt, then the Ministry of Finance still says that without invoices, deducting VAT is impossible.

But the main thing here is that when the Ministry of Finance issues such letters, it acts strictly on a formal basis. And even if you paid VAT and you have all the evidence of this, then you can deduct it, but only if you received an invoice. In this case, the Ministry of Finance always writes the same thing: in accordance with the letter of the Ministry of Finance of Russia dated August 7, 2007 No. 03-02-07/2-138 : “The specified letters are of an informational and explanatory nature on the application of the legislation of the Russian Federation on taxes and fees and do not prevent tax authorities, taxpayers, payers of fees and tax agents from being guided by the norms of legislation on taxes and fees in an understanding that differs from the interpretation set out by the Ministry of Finance of Russia.” Why is there such a link? Yes, very simple. From the point of view of logic, Article 21 of the Tax Code of the Russian Federation and judicial and arbitration practice, if the reality of this transaction is proven, you really paid VAT and there are supporting documents, then you have the right to deduct VAT, even if there is no invoice. That is why the Ministry of Finance says that this is simply their opinion and that it is possible to use legal norms that differ from the interpretation set out in the letters of the Ministry of Finance. For example, a letter saying that nothing can be done without an invoice. This is just a formal approach. But, most likely, you will have to prove your case in court, guys.

Thank you and good luck with your VAT deductions.

Link to documents:

Letter of the Ministry of Finance of Russia dated August 7, 2007 No. 03-02-07/2-138

Letter of the Ministry of Finance of Russia dated November 26, 2021 No. 03-07-11/91521

SIGN UP FOR A TAX SEMINAR

(Visited 1,546 times, 1 visits today)

Vladimir Turov

Head of legal practice, practicing and leading specialist in tax planning, building individual tax schemes and holdings, optimizing financial flows.

Distinctive features of an invoice

Invoice journal

Some businessmen do not understand the difference between invoices and ordinary delivery notes. The difference between such a document and a regular invoice is that the invoice must be provided exclusively to sellers or official suppliers of certain services who pay VAT.

Each representative of his organization must understand that an invoice is considered a mandatory type of accounting documentation, drawn up by a staff accountant on the basis of a purchase and sale agreement or for the provision of certain services.

Each supplier needs an invoice to be able to draw up reports in obtaining the right to a tax deduction approved by law; the invoice is provided to the customer himself to pay for the agreed services and material assets provided.

Also, Article 169 of the Tax Code of the Russian Federation states that the issuance of an invoice and delivery note is carried out upon the conclusion of one agreement. However, form, function and content have certain differences. The invoice must be drawn up only in accordance with the specified sample, while the invoice is drawn up in any form.

An invoice must be issued after the means of payment have been provided as payment for the product or service. This document is considered confirmation for the possibility of deducting VAT. The invoice must be filled out after shipment of a certain group of goods to be able to document the action performed.

Based on the received invoice, the customer will be able to make specific claims to the service provider in case of disagreement.

Article 169. Invoice

1. In paragraph 1 of Art. 169 defines an invoice. The analysis shows that the invoice is:

1) this is a written document. It is prepared by the VAT taxpayer. At the same time, in almost all cases the taxpayer is obliged to draw up this document (with some exceptions specified in paragraph 4 of Article 169), regardless of whether he is exempt from performing the duties of calculating and paying VAT (see the commentary on this to Article 145 Tax Code) or not exempt (the first, when drawing up invoices, put a stamp in the appropriate column or make the inscription: “Without VAT tax”, see the commentary on this to Article 168 of the Tax Code);

2) serves as the basis for accepting the presented VAT amounts as a tax deduction (in accordance with the rules of Articles 171, 172 of the Tax Code, see the commentary thereto);

3) serves as the basis for VAT refund (in accordance with the rules of Article 176 of the Tax Code, see commentary thereto).

2. Analysis of the rules of paragraph 2 of Art. 169 allows us to draw a number of conclusions:

1) the procedure for drawing up an invoice specified in paragraphs 5 and 6 of Art. 169 must be strictly observed: the taxpayer does not have the right to deviate from this procedure based on “taking into account specific features,” “reasons of expediency,” etc.;

2) in cases where the taxpayer did not indicate in the invoice the information mentioned in paragraph 5 of Art. 169 (and equally if it does not contain the signatures of the persons specified in paragraph 6 of Article 169), this document:

- cannot serve as a basis for accepting VAT amounts presented to the buyer (customer) for deduction or reimbursement;

- cannot serve as a basis for making appropriate entries in the journal of accounts - invoices, the book of purchases and sales (see the commentary on paragraph 8 of Article 169 about this);

3) failure to comply with requirements not specified in clauses 5 and 6 of Art. 169, and established, for example, in the regulations of the Ministry of Taxation, is not a basis for refusing to accept for deduction the amount of VAT presented by the seller (manufacturer, contractor, performer).

3. Applying the rules of paragraph 4 of Art. 169, you need to keep in mind that:

1) as a general rule, the taxpayer is obliged (and not entitled!) to keep not only an invoice, but also a journal of issued and received invoices, a purchase book, a sales book (see below for more information). The taxpayer must purchase the forms (blanks) of these books and magazines independently;

2) the mentioned obligation must be fulfilled when the taxpayer commits:

- even one transaction that is recognized as a VAT subject in accordance with the rules of Art. 146 NK (see commentary to it);

- regardless of whether the transaction performed is one of those exempt from VAT taxation or not (see the commentary to Article 149 on this), taking into account the rules of paragraph 4 of Art. 169;

3) the taxpayer must draw up an invoice and maintain the mentioned books and journal in other cases specified in the Procedure for maintaining a journal of invoices, purchase and sales books established by the Government of the Russian Federation.

4. As an exception to the general rules, in paragraph 4 of Art. 169 it is established that invoices are not issued:

1) for transactions of sale (and not import into the customs territory of the Russian Federation) of securities (for example, shares, bonds, other issue-grade securities). However, this does not mean operations to provide:

- brokerage services. It must be borne in mind that in accordance with Art. 3 of the Securities Law, brokerage activity is recognized as the performance of civil legal transactions with securities as an attorney or commission agent acting on the basis of an agency or commission agreement, as well as a power of attorney to carry out such transactions in the absence of indications of the powers of the attorney or commission agent in the agreement;

- intermediary services. In accordance with Art. 4 of the Securities Law, an intermediary (dealer) activity is recognized as carrying out transactions of purchase and sale of securities on its own behalf and at its own expense by publicly announcing the purchase and/or sale prices of certain securities with the obligation to purchase and/or sell these securities at the announced prices. the person carrying out such activities, prices;

2) banks (as well as other credit organizations!) both for banking transactions and when banks perform other non-banking transactions (after Law No. 166 came into force). In this case, the list of banking operations should be determined in accordance with Art. 149 of the Tax Code, which establishes that these include, in particular:

— attracting funds from organizations and individuals to deposits;

— placement of raised funds from organizations and individuals on behalf of banks and at their expense;

— opening and maintaining bank accounts for organizations and individuals;

— making settlements on behalf of organizations and individuals, including correspondent banks, on their bank accounts;

— cash services for organizations and individuals;

— purchase and sale of foreign currency in cash and non-cash forms (including the provision of intermediary services for purchase and sale transactions of foreign currency);

— attraction of deposits and placement of precious metals;

— issuance of bank guarantees;

— issuance of guarantees for third parties, providing for the fulfillment of obligations in monetary form;

— carrying out transactions with precious metals and precious stones in accordance with the legislation of the Russian Federation;

— provision of services related to the installation and operation of the “client-bank” system, including the provision of software and training of personnel serving the specified system;

3) insurance organizations (i.e. insurers). It should be taken into account that legal entities that have permits (licenses) to carry out insurance of the relevant type (property, personal, etc.) can act as insurers. The requirements that insurance organizations must meet, the procedure for licensing their activities and the implementation of state supervision over these activities are determined by the laws on insurance (Article 938 of the Civil Code). In paragraph 4 of Art. 169 refers only to the operations of insurance organizations specified in Art. 149 NK, i.e. insurance and reinsurance operations, as a result of which the insurance organization will receive:

— insurance payments under insurance and reinsurance contracts, including insurance premiums, paid reinsurance commission (including bonus);

— interest accrued on the depot of premiums under reinsurance agreements and transferred by the reinsurer to the reinsurer;

- insurance premiums received by an authorized insurance organization that has concluded a coinsurance agreement in the prescribed manner on behalf of and on behalf of the insurers;

- funds received by the insurer under recourse claims from the person responsible for the damage caused to the policyholder, in the amount of the insurance compensation paid to the policyholder;

4) non-state pension funds. Latest:

— operate independently of the state pension system;

— pay pensions along with payments of state pensions (the amount, conditions and procedure for making contributions to these funds are determined in agreements between the funds and policyholders);

- does not have the right to engage in commercial activities (clauses 2, 3 of the Decree on non-state pension funds). The above non-state pension funds do not draw up invoices for transactions exempt from taxation in accordance with Art. 149 NK.

5. Analysis of the rules of paragraph 5 of Art. 169 shows that:

1) they are mandatory in nature: neither the taxpayer nor the tax authority has the right to establish other rules (for example, that some of those provided for in paragraph 5 of Article 169 may not be specified);

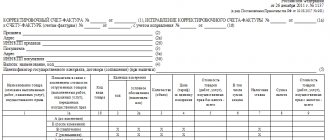

2) they prescribe that the invoice must indicate:

- serial number (it is carried out in accordance with the records management organized by the taxpayer) and the date of issue of the invoice (the calendar date (day, month, year) is indicated when the seller (manufacturer, executor, etc.) issues the invoice ;

- name (for commercial organizations - business name, for individual entrepreneurs - name), address (for individual entrepreneurs, place of residence, for legal entities - location) and taxpayer and buyer identification numbers. The specified information must be determined based on the norms of Art. 19, 20, 54 Civil Code and Art. 84 NK;

— name and address of the consignor and consignee (if the goods are intended to be transported from the seller to the buyer, for example, by rail);

- number of the payment and settlement document (for example, payment order, letter of credit, etc.) in the event that the buyer (contractor, performer) receives an advance or other payments (for example, a deposit) towards upcoming deliveries (or performance of work, provision of services);

- name of the goods supplied (using their generally accepted names and, where necessary, codes, for example, HS codes), types of work performed, services provided and units of measurement (in pieces, liters, tons, kilograms, etc.);

- quantity (volume) of goods, works, services supplied (shipped) on this invoice based on the units of measurement accepted for this document (for example, 20 tons, 40 liters, 50 meters, etc.);

- price (tariff) per unit of measurement under an agreement (contract) without including VAT and in cases of application of state regulated prices (tariffs) (in accordance with Decree of the Government of the Russian Federation N 239 of March 7, 1995, see more about it in book: Guev A.N. Article-by-article commentary of the Civil Code of the Russian Federation (Part I, Article 1 - 453). M., "YUKANG", 1995. P. 926 - 930), including VAT, taking into account this tax;

- the cost of goods (work, services) for the entire quantity supplied (shipped) according to the invoice - invoice of goods (work, services) - without including VAT;

- the amount of excise taxes (only for excisable goods, see the commentary on this to Article 181 of the Tax Code);

— tax rate (its amount is determined in accordance with Article 164 of the Tax Code, see commentary to it). Moreover, if a zero rate is set, then this must also be indicated;

- the amount of VAT offered to the buyer (customer) of goods (work, services), determined on the basis of the applicable tax rates (see the commentary on this to Articles 154 - 159, 162, 168 of the Tax Code);

- the cost of the total quantity of goods (work, services) supplied (shipped) according to the invoice, including the amount of VAT;

- the amount of sales tax (if provided by law) if the invoice was issued before the entry into force of Law No. 166;

- country of origin of the product (if it is a domestic product, then there is no need to indicate - Russian Federation);

— number of the cargo customs declaration (if the goods were imported into the customs territory of the Russian Federation).

When selling goods whose country of origin is not the Russian Federation:

— columns 13 and 14 of the invoice must be filled in;

- the taxpayer is responsible only for ensuring that the information indicated by him (in his invoice) corresponds to the information specified in the invoice (received by him from the seller) and documents of title (for example, invoices, bills of lading, etc.).

6. Analyzing the rules of paragraphs 7 and 8 of Art. 169, you need to take into account that:

1) when carrying out foreign economic transactions (for example, when concluding a contract for supply to another country), the obligation is expressed in foreign currency, then the VAT amounts can be expressed in foreign currency. In the practice of legal clients, a question arose: are there any contradictions between the rules of paragraph 3 of Art. 45 of the Tax Code (stating that in the cases mentioned in the law, the obligation to pay tax can be fulfilled in foreign currency) and the rules of paragraph 7 of Art. 169?

The contradiction is apparent: in paragraph 7 of Art. 169 we are talking about the information indicated in the invoice and the procedure for drawing up this document, and in paragraph 3 of Art. 45 of the Tax Code - on the possibility of paying tax in foreign currency;

2) the procedure for maintaining a log of received and issued invoices, purchase books and sales books must be established by the Government of the Russian Federation. In this regard, it is necessary to take into account that:

- it is necessary to proceed from the norms of the Government of the Russian Federation No. 914 of December 2, 2000 “On approval of the rules for maintaining a log of received and issued invoices - invoices of purchase books and sales books for VAT calculations.” However, the latter are subject to application only to the extent (this especially applies to the provisions of Appendix No. 1, dedicated to the contents of the invoice: it significantly diverges from the provisions of paragraph 5 of Article 169) in which they do not contradict the rules of Art. 169;

- in Art. 33 of Law No. 118, the Government of the Russian Federation is ordered to bring its regulatory legal acts (including the above-mentioned Resolution No. 914) into compliance with Part 2 of the Tax Code. On the other hand, there is no deadline for such compliance.

7. Rules of subclause 11, clause 5, art. 169 must be applied taking into account the rules of paragraph 5 of Art. 168 that when selling goods (work, services), transactions for which are exempt from VAT, as well as when the taxpayer is exempt (in accordance with Article 145 of the Tax Code) from fulfilling the obligation to change and pay VAT, in the corresponding column of the invoice you need to put a stamp (make an inscription): “Without VAT tax.”

8. Describing the rules of paragraph 6 of Art. 169, you need to pay attention to a number of important points:

1) the invoice must be signed by:

- Head of the organization. In this case, it is necessary to indicate the name of this body in full accordance with the constituent documents of the organization (for example, general director of an OJSC, director of a general partnership, etc.). If a sole executive body has been created in the organization, then he signs the invoice; if the organization has a collective executive body (and there is no sole executive body), then the invoice is signed by the person heading the collective executive body of the organization (for example, the chairman of the board of a general partnership, etc.);

- chief accountant of the organization. In accordance with Art. 7 of the Accounting Law, the chief accountant (accountant, in the absence of a chief accountant position on the staff) is appointed and dismissed by the head of the organization. He reports directly to the head of the organization and signs documents, in particular, invoices. Without the signature of the chief accountant, monetary and settlement documents (including invoices) are considered invalid.

In the practice of legal clients, a question arose: what to do if an organization (small enterprise) does not have a chief accountant, and his functions are performed directly by the head of the organization (which is allowed by Article 6 of the Accounting Law)?

In paragraph 6 of Art. 169 NK - a gap, there is no answer to this question. In this regard, the invoice is signed either by the manager alone, or by him and another employee of the organization (empowered with such powers in accordance with the order of the head of the organization);

2) other persons (employees of the organization) also have the right to sign an invoice instead of the manager and (or) chief accountant, because only for them are the orders and instructions of the manager obligatory, Article 18, 127 of the Labor Code (see the commentary on this in the book: Guev A.N. Article-by-article commentary of the Labor Code of the Russian Federation (ed. 4), M., BEK, 2001), authorized to do so by order of the head of the organization. It should be noted that in paragraph 6 of Article 169 the clearly unsuccessful phrase “other officials” is used : the thing is that this ignores:

— definition of an official (it is given in Note 1 to Article 285 of the Criminal Code: officials are persons who permanently, temporarily or by special order carry out the functions of a representative of government or perform organizational and administrative functions, administrative and economic functions in government agencies, local governments , state and municipal institutions, as well as in the Armed Forces of the Russian Federation, other troops and military formations of the Russian Federation);

- the fact that, along with officials, there are “persons performing managerial functions in commercial and other organizations” (these are persons who permanently, temporarily or by special order perform organizational and administrative responsibilities in commercial organizations, regardless of the form of ownership, as well as in non-profit organizations that are not government agencies, local governments, state or municipal institutions, Article 201 of the Criminal Code). It turns out that it is impossible to entrust the latter with the authority to sign an invoice (although this is not the case). The legislator needs to return to this issue;

2) if the invoice is issued by an individual entrepreneur, the latter signs this document, indicating the number and date of issue of the certificate of state registration of this individual entrepreneur.

In the practice of legal clients, a question arose: should private detectives issue an invoice (we recall that in accordance with Articles 3 - 6 of the Law on Private Detective Practice and Security Activities, private detectives do not receive a certificate of state registration as an individual entrepreneur, but they are issued license to carry out such activities).

Systematic analysis of the provisions of Art. 11 and paragraph 6 of Art. 169 of the Tax Code shows that:

- in paragraph 6 of Art. 169 refers specifically to individuals who have undergone state registration as an individual entrepreneur without forming a legal entity (i.e., subject to the rules of Article 23 - 25 of the Civil Code). Private detectives in paragraph 6 of Art. 169 are not meant;

— there is a gap in clause 6 of Art. 169, until it is eliminated by the legislator, one must proceed from the literal text of paragraph 6 of Art. 169. In other words, an invoice is drawn up or issued by an individual entrepreneur (and not by private detectives and other persons equated (for tax purposes) to individual entrepreneurs by the rules of Article 11 of the Tax Code).

For judicial practice, see Bulletin of the Supreme Arbitration Court. 2000. N 5. P. 7.

What defects will make the document unusable?

A document in which:

- information about the persons indicated in it is missing or fundamentally incorrect;

- it is impossible to unambiguously determine the object of sale;

- the sales price, rate and amount of tax are missing or are given with errors (letters of the Ministry of Finance of Russia dated 04/19/2017 No. 03-07-09/23491, dated 09/18/2014 No. 03-07-09/46708, dated 05/30/2013 No. 03-07 -09/19826);

See also : Arithmetic Error on Invoice Will Void Deduction .

- the currency is missing or incorrectly indicated (letter of the Ministry of Finance of Russia dated March 11, 2012 No. 03-07-08/68).