Translation of goods into materials and back in the program “1C: Enterprise Accounting 8”

Biryukov Sergey, head of consulting department — 01.02.2009

Attention: all examples are shown in the program “1C: Enterprise Accounting 8”, edition 1.6.

In the software product "1C: Enterprise Accounting 8" there are two ways to convert goods into materials and materials into goods. By translation we mean the transfer of a quantitative and total expression from CT account 10 to DT account 41 and, conversely, from CT account 41 to DT account 10. This need arises if an organization sells the same type of item that it uses in production . For example, an organization is engaged in the sale of boards and at the same time the production of any products from the boards. During the purchasing process, it is impossible to determine for sure how many boards need to be credited to account 10 and which to account 41, due to the fact that the needs of trade and production may vary, and therefore there is a need for adjustment. In the standard functionality there is no separate document for performing this operation, and therefore you need to proceed as follows:

1st method

This method is the most correct - in the current month, you should correct the documents for the receipt of materials/goods (the document “Receipt of goods and services”), correcting the accounting accounts in them retroactively. After this, the documents should be re-posted. This method can only be used in the current open month. If you need more materials, then you need to find the latest documents for the receipt of goods in the current month and change the accounting accounts to 10 and again re-post the documents. Thus, the goods will be capitalized as materials.

2nd method

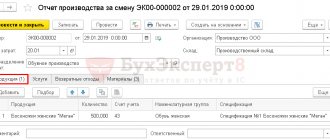

To convert goods into materials and vice versa, use the document “Movement of goods” (Warehouse → Movement of goods). On the “Products” tab, materials or goods are indicated. The sending and receiving warehouse is the same. In the column “account desp. (BU)" will indicate from which account the goods/materials are sent, and in the column "account received. (BU)” manually indicate the account to which you want to transfer the goods/material. Similar actions are performed for NU accounts.

Example: An organization moves goods into materials:

Postings are generated in BU and NU:

If the accounting policy of the enterprise establishes that the organization applies shipment without VAT and/or VAT with 0%, then there is also a movement through the accumulation register “VAT on inventory lots” using the resources “Account” and, if necessary, “Warehouse”, taking into account VAT on additional expenses, if any:

And in conclusion: Some consultants advise using the document “Request-invoice” for the above purposes, indicating in it instead of a cost account the account for the receipt of goods or materials (10 or 41). However, using the “Demand-invoice” document to move the quantitative-cumulative expression of a certain item from account to account, in our opinion, is irrational and may be associated with a number of certain inconveniences and inaccuracies, namely:

1. In the “Request-invoice” document, you can move only one type of product to the material and back. 2. If the organization applies shipment without VAT and/or VAT with 0%, then in the accumulation register “VAT by inventory lots” there is an expense for this item, which indicates that in the future the program will not keep records for the item tied to this item VAT amount. This will most likely cause errors in the implementation of this item when including VAT in the cost of this item, writing off VAT on expenses, etc.

Have fun and productive work!

Is it possible to reclassify materials into goods and vice versa?

Question: An organization purchases materials for production. Some of these materials are not used. Is it possible to move them from account 10 to account 41 and sell them as goods? Does the organization have the right to sell materials purchased for production? And is it possible to perform the reverse operation: to use in production goods intended for sale?

Answer: An organization can reclassify materials recorded on account 10 into goods recorded on account 41, and vice versa. The organization has the right to sell materials purchased for production.

Rationale: Materials listed on account 10 “Materials” and goods reflected on account 41 “Goods” belong to the same category of assets - inventories <*>.

As a rule, materials recorded on account 10 are considered inventories, i.e. inventories used in production <*>. In turn, goods posted to account 41 are assets that are recognized as the organization’s reserves and are acquired for the purpose of further sale, i.e. intended for sale <*>.

However, the owner organization has the final say on how to use said assets.

Over time, the direction of their use may change due to various circumstances. Thus, an asset purchased for sale (goods), but not sold due to, for example, lack of demand, can be used in production, management, etc. Conversely, an asset purchased for production purposes or the needs of the organization can be sold.

In this regard, by decision of the manager, the organization can reclassify assets: transfer assets from account 10 to goods in account 41 and, conversely, include goods from account 41 in materials in account 10. This business operation is documented with a primary accounting document, for example, an act on transfer of goods into materials (materials into goods). Such a document must contain mandatory details <*>.

Note It should be noted that in Appendices 10, 24 to Instruction No. 50 there is no entry: D-t 41 - K-t 10. However, if an organization carries out business operations in the course of its activities, the correspondence of accounts for which is not established by Instruction No. 50, has the right to make entries based on the content of the business operation <*>.

Thus, the reclassification of assets in our situation will be recorded in the following entries:

| Contents of operation | Debit | Credit |

| The transfer of an asset from materials to goods is reflected | 41 | 10 |

| The transfer of an asset from goods to materials is reflected | 10 | 41 |

At the same time, I would like to draw attention to the following. If an organization needs to sell materials, it is not necessary to reclassify them. You can simply show the implementation from count 10 <*>.

Read this material in ilex >>*

*following the link you will be taken to the paid content of the service

They decided to use the product as a material

When transferring goods to materials, you will also need an order from the manager. In the document, reflect the reason why this decision was made. After this, draw up unified primary documents provided for accounting for materials. This is a requirement-invoice in form No. M-11 and a materials accounting card in form No. M-17.

Let us recall that companies usually include in their materials property that meets the characteristics of fixed assets, but is valued within the established limit. Therefore, the rules discussed in this section will be exactly the same for both ordinary materials and low-value assets.

Accounting

The product that your company will use as material must be transferred to account 10 “Materials”.

The main thing to remember

1

To transfer goods to fixed assets or materials, you will need an order from the manager.

2

Expenses on account 41 “Goods” must be transferred to account 08 (07) or 10.

Additional information about fixed assets accounting

Document:

Articles , , and the Tax Code of the Russian Federation.

Biryukov Sergey, head of consulting department

—

01.02.2009

Attention:

all examples are shown in the program “1C: Enterprise Accounting 8”, edition 1.6.

In the software product "1C: Enterprise Accounting 8" there are two ways

converting goods into materials and materials into goods. By translation we mean the transfer of a quantitative and total expression from CT account 10 to DT account 41 and, conversely, from CT account 41 to DT account 10. This need arises if an organization sells the same type of item that it uses in production . For example, an organization is engaged in the sale of boards and at the same time the production of any products from the boards. During the purchasing process, it is impossible to determine for sure how many boards need to be credited to account 10 and which to account 41, due to the fact that the needs of trade and production may vary, and therefore there is a need for adjustment. In the standard functionality there is no separate document for performing this operation, and therefore you need to proceed as follows:

1st method

This method is the most correct - in the current month, you should correct the documents for the receipt of materials/goods (the document “Receipt of goods and services”), correcting the accounting accounts in them retroactively. After this, the documents should be re-posted. This method can only be used in the currently unclosed

month. If you need more materials, then you need to find the latest documents for the receipt of goods in the current month and change the accounting accounts to 10 and again re-post the documents. Thus, the goods will be capitalized as materials.

2nd method

To convert goods into materials and vice versa, use the document “Movement of goods” (Warehouse → Movement of goods). On the “Products” tab, materials or goods are indicated. The sending and receiving warehouse is the same. In the column “account desp. (BU)" will indicate from which account the goods/materials are sent, and in the column "account received. (BU)” manually indicate the account to which you want to transfer the goods/material. Similar actions are performed for NU accounts.

Example: An organization moves goods into materials:

Postings are generated in BU and NU:

If the accounting policy of the enterprise establishes that the organization applies shipment without VAT and/or VAT with 0%, then there is also a movement through the accumulation register “VAT on inventory lots” using the resources “Account” and, if necessary, “Warehouse”, taking into account VAT on additional expenses, if any:

In conclusion:

Some consultants advise using the document “Request-invoice” for the above purposes, indicating in it instead of a cost account the account for the receipt of goods or materials (10 or 41). However, using the “Demand-invoice” document to move the quantitative-cumulative expression of a certain item from account to account, in our opinion, is irrational and may be associated with a number of certain inconveniences and inaccuracies, namely:

1.

In the “Requirement-invoice” document, you can move only one type of product to a material and back.

2.

If the organization applies shipment without VAT and/or VAT with 0%, then in the accumulation register “VAT by inventory lots” there is an expense for this item, which indicates that in the future the program will not keep records for the item tied to this item VAT amount. This will most likely cause errors in the implementation of this item when including VAT in the cost of this item, writing off VAT on expenses, etc.

Have fun and productive work!

Is it possible to convert fixed assets into goods, and if so, how can this be justified? And why is such a translation needed at all? You will find answers to these difficult questions, examples from arbitration practice and explanations from officials in this publication.