Procedure for deducting overpayment

First, you need to determine whether it is possible to withhold overpaid money from the employee. You can withhold money from an employee in the following situations (137 Labor Code of the Russian Federation):

- The employee did not work out the funds previously issued to the employee or did not return them. An example is failure to provide a report on a business trip or for accountable money. Or the employee was paid an advance, which he did not work off. In some cases, it is also possible to withhold vacation pay, for example, when the employee’s vacation was provided in advance and the employee resigns. It is important to remember that vacation pay cannot be withheld if an employee quits due to layoffs or conscription into the army;

- The employee was overpaid due to an accounting error. Or, due to an accounting error, the employee received a large amount of vacation pay or benefits.

In what cases is this possible?

Article 137 of the Labor Code of the Russian Federation provides for only a few cases when the employer has the right to recover excessively accrued wages from an employee. So, these include:

- Presence of a counting error;

- Establishing the employee’s guilt in failure to fulfill the required work plan;

- Identification of illegal actions that resulted in overpayment of wages.

You may find the following information interesting: is it possible to pay wages ahead of schedule?

So, if everything is extremely clear with the last two points, then questions often arise about the first. The fact is that the legislation does not have an interpretation of the concept of “counting error”. At the same time, as judicial practice shows, this term means any arithmetic miscalculation, typo or clerical error, including an error resulting from a program malfunction, etc. (Determination of the RF Armed Forces dated January 20, 2012 No. 59-B11-17).

The total amount of deduction should not exceed 20% of the salary (in some cases provided for by law, 50% is allowed). This condition is reflected in Article 138 of the Labor Code of the Russian Federation.

Accountant mistakes

Let's consider which errors can be considered countable and which cannot:

| Counting errors | Countless mistakes |

| Incorrect initial data was entered into the accounting program, for example, salary, date of employment, date of dismissal, percentage for calculating bonuses, etc.; The accounting program crashed, resulting in wages being calculated incorrectly; When calculating wages, large indicators were taken into account regarding the volume of work performed | During one pay period, the salary was transferred twice; The employee’s salary was transferred to the card, and he received it at the cash desk; The employee was provided with a personal income tax deduction without justification; When calculating the average salary, excluded payments were taken into account; An incorrect algorithm was entered into the program to calculate benefits or sick leave; When calculating benefits, the employee's insurance length was incorrectly calculated; The salary was transferred to an employee who quit last month; At the direction of the labor inspectorate, the employee’s salary was accrued, and then the court declared the order illegal |

Counting error and judicial practice

The presence of a counting (arithmetic) error is the most common argument of the employer when withholding overpaid amounts of wages. However, judicial practice in this area most often does not work in favor of organizations.

Example: The Moscow Regional Court, in its ruling No. 33-19764 dated 10/12/10, expressed the opinion that an overpayment cannot be a counting error, but is a consequence of the employer’s incorrect application of labor legislation. According to the judges, the overpayment cannot be attributed to the amounts of unjust enrichment (Civil Code of the Russian Federation, Art. 1109). The employee is not obliged to return the funds overpaid to him. In addition, not all courts recognize a malfunction in an accounting program as a counting error.

Example: The Sverdlovsk Regional Court, in its ruling in case No. 33-7642/2016 dated 04/21/16, did not recognize a technical counting error, but the Samara Regional Court in its ruling No. 33-302/2012 dated 01/18/12 did.

Judicial practice on the application of Art. 137 of the Labor Code clearly indicates that the following cannot be recognized as a counting error:

- payment for a longer vacation than the employee is entitled to by law;

- payment of a larger bonus;

- erroneous payment of double wages for the period.

This is evidenced by numerous decisions of courts of all levels, up to and including the Supreme Court (definition No. 59-B11-17 of 01/20/12).

On a note! Rostrud, in its letter No. 3044-6-0 dated 09-08-07, expresses the point of view according to which, even if there is an undeniable accounting error, the employee’s written consent is required to repay the difference at his expense.

Procedure for reimbursement of overpayment

Depending on the situation in which the overpayment arose, the algorithm for its compensation will vary:

- The employee received a payment in an amount greater than what was due due to his own fraud (for example, the submitted documents contained deliberately false data) or the overpayment arose due to the fact that the employee did not report the advance payment or did not work it out. In this case, you first need to determine whether the employee agrees to the deduction, and also find out whether more than one month has passed from the date the overpayment was established. If the employee does not agree to withhold the overpayment, the employer only has the right to go to court. If the employee gives his consent, then the overpayment must be withheld from his salary. In this case, it is necessary to observe the rule of 20% withholding, that is, no more than 20% can be withheld from wages at a time (138 Labor Code of the Russian Federation).

- The overpayment occurred as a result of an accounting error. In this case, it is necessary to find out whether the accounting error is counting. If this is the case, then the overpayment is withheld from the employee’s salary, but not more than 20% of the salary at a time. If the error is uncountable, then the employer can withhold the overpayment only if the employee does it himself.

Reasons for overpayment of wages upon dismissal and grounds for returning money

Please note that the overpayment is indeed refundable. However, this is not possible in all cases. The first thing you need to do is find out why the employee was credited with an “extra” amount of money. As a rule, this determines whether the subordinate should return it.

There can be two reasons for overpayment:

- A simple mistake was made when calculating wages. For example, the accountant mixed up the numbers or even added an extra zero;

- overpaid wages were accrued voluntarily in the absence of a calculation error. For example, an employee did not have the right to receive any substantial increase in salary, and due to the erroneous classification of his position as a citizen who is entitled to additional payment, he was awarded extra money.

It is worth noting that in the first case the person will have to return other people’s money. This is due to the fact that a counting error when calculating funds entails the obligation to return the amount in full. Excessive wages paid to a dismissed employee must also be returned without fail.

Withholding from employees' salaries to pay off their debt to the company where they work can be carried out by order of the boss to return amounts overpaid to subordinates. This can only be done if there are no disputes with employees.

Conditions for withholding overpayments

In order to withhold an overpayment from an employee’s salary, the following conditions must be met:

- The employee agrees to the retention;

- At least one month must pass from the date that was set for the return of the advance or for repaying the debt.

Both conditions must be met simultaneously. If at least one of them is not fulfilled, the money can only be recovered in court. You will also need to go to court if the employee provided false information, or if some information affecting the salary was hidden.

If retention is not possible

It happens that it is impossible to return the wrongly paid salary. For example, an employee quit and left. In such cases, it is impossible to recover the amount of overpayment, and it is recognized as a bad receivable. The amount of debt is written off from the reserve for doubtful debts (if any) or, if the reserve has not been created, it is attributed to a loss by including it in other expenses.

In accounting, the write-off of salary debt is reflected by the following entries:

- D/t 76 K/t 73 – overpaid wages are written off;

- D/t 91-2 K/t 76 – salary debt written off, unrealistic for collection

For example, the employee did not agree to the deduction or upon his dismissal, 20% of the “severance” payments were not enough to pay off the entire debt. Then it is possible to recover wages and equivalent payments from the employee in court only in three cases:

- a counting error was made;

- there were dishonest actions of the employee;

- the court finds the employee guilty of failure to comply with labor standards or downtime (if excessive payments are collected from the employee for downtime and underperformance).

In the absence of such circumstances, courts generally refuse to allow employers to recover excess payments from employees.

How to return an overpayment of wages due to the fault of an accountant

Once an error is discovered, the manager must be notified about it. To do this, a memo is written indicating that a counting error was made when calculating wages (benefits or vacation pay). After this, the employee can be asked to contribute money voluntarily, or withhold it from their salary. An order must be issued to withhold funds. Confirming his consent to withhold money from his salary, the employee puts his signature on the order. This will constitute the employee’s written consent to withhold the overpayment (

Report on detection of a counting error, notification to the employee, order to deduct from wages

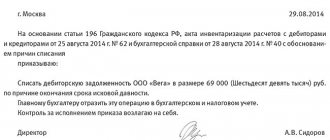

To record the legal fact of a counting error, a commission act is drawn up. The commission can include a chief accountant, a payroll accountant, etc.

The act indicates where, when and by whom the error was discovered, the reason for its commission, and the amount of overpaid wages. The act is drawn up in 2 copies, it is signed by all members of the commission.

One copy of the act is given/sent to the employee along with a notification of the need to return the excess salary received. The notice specifies the amount and date by which the debt must be repaid.

In response to the notification received, the employee deposits money into the organization’s account or gives his consent to deduction from salary to repay the debt.

Within a month after the expiration of the period given for the voluntary deposit of funds into the cash register / into the company’s current account, the employer issues an order to deduct from wages (Part 2 of Article 137 of the Labor Code of the Russian Federation).

The order contains:

- instructions to the accountant to make deductions;

- Full name and position of the debtor employee;

- amounts of deductions;

- the basis for performing these transactions.

An employee’s refusal or silence in response to a notice does not give the right to deduct overpaid wages from him. In this case, the employer has only a judicial procedure for collecting the overpayment.

Adjustment of accounting, personal income tax and insurance premiums

If an error occurs in the payment of wages, you will need to recalculate personal income tax, contributions, and also correct accounting records. The postings will be as follows:

| Business transaction | Wiring | |

| D | TO | |

| An advance was paid to the employee | 70 | 51 |

| The overpaid amount was reversed | 20 | 70 |

| The employee is paid a salary | 20 | 70 |

| Insurance premiums paid on wages | 20 | 69 |

| Basic salary paid minus withholding amounts | 70 | 51 |

| Personal income tax withheld | 70 | 68 |

SAMPLE REPORT

SAMPLE ORDER

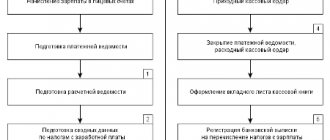

Procedure for refunding the accrued amount to the cashier

In the event of a refund of an overpayment through the organization's cash desk, the actions of the employee and employer must comply with the following instructions.

Step 1 – at the very beginning, the employer needs to establish the reason for the overpayment. For this purpose, a special commission is assembled and a report is prepared on the error made in calculating wages.

Step 2 – next, the employee must be notified that he has a debt to the company. A written notice is sent to his address, which indicates:

- An error resulted in an overpayment.

- Amount of debt.

- The period of time within which the employee must make a refund.

Step 3 - after receiving notice from the employer, the employee must write a statement of consent to collect the overpayment (if he does not object to this procedure). Otherwise, the issue can only be resolved in court.

The statement is written in any form, but must indicate that the employee has no objections to the withholding of overpaid wages.

Step 4 – the next step is to issue an appropriate order on behalf of the head of the employing organization. This document should reflect the following information:

- Purpose of the order (reimbursement of overpaid funds).

- Link to the consent statement written by the employee.

- An order to the accountant: about deduction (indicating the amount and month in which it should be made) and making corrections in accounting.

Step 5 – then he must return the overpaid amount of salary to the organization’s cash desk.

Step 6 - after the employee has returned the funds, the accountant draws up the appropriate entries and makes the necessary corrections in the accounting.

Registration of the act by the employer

As noted above, first of all, the employer needs to determine the nature of the error made when calculating wages, and also determine whether it can serve as a basis for deduction under the Labor Code of the Russian Federation.

For this purpose, a special commission is appointed , the members of which, as a rule, are:

- CEO.

- Head of HR Department.

- The cashier who issued the salary.

Read more: Protection of consumer rights between legal entities

After the investigation, a report is drawn up on the identified error made when calculating wages. It includes the following sections:

- The “header” of the document - at the very top is written the full name of the organization, the name of the paper, as well as the date of its preparation.

- The main part - the following information is presented sequentially: who identified the error (full name and position); in relation to whom (full name and position of the employee) and in what month the overpayment was made; a detailed description of the miscalculation; the amount of the overpayment; confirmation of the fact of an error on the part of the commission members.

- End of the document - at the end there must be signatures of the chief accountant, as well as all members of the commission.

Making up transactions

The return of the overpayment to the cash desk is processed using the following transactions:

- Dt 20: Kt 70 – accrual of incorrectly calculated wages to the employee;

- Dt 70: Kt 68 – withholding of personal income tax from accrued wages;/li>

- Dt 70: Kt 50 – salary is given to the employee in person;

- Dt 20: Kt 70 – repeated reflection of transaction No. 1, however, a “–” sign is placed in front of the numerical value (reversal);

- Dt 70: Kt 68 – reversal of the amount of personal income tax previously withheld from incorrectly accrued wages;

- Dt 73: Kt 70 – transfer of the overpayment amount to the account with other settlements;

- Dt 50: Kt 73 - a reflection of the amount of deduction that the employee paid through the organization’s cash desk.

Accounting error when calculating wages

For example, you can issue a notification like this:

Condition 2. The employee’s consent to withholding has been obtained

The employer has the right to decide to withhold excess payments from the employee’s salary only if the employee does not dispute the grounds and amount of the withholding (Article 137 of the Labor Code of the Russian Federation).

From this we can conclude that it is enough to notify the employee of the upcoming deduction, assigning him a deadline for submitting objections. And if no objections are received from him within this period, then you can safely issue an order (instruction) to withhold.

But no. According to Rostrud, expressed in 2007, and the courts, this is not enough, and as a sign of the absence of objections on the part of the employee, it is necessary to obtain written consent from him to withhold (Letter of Rostrud dated 08/09/2007 N 3044-6-0; Cassation rulings of the Supreme Court of the Udmurt Republic dated August 22, 2011 N 33-2856, Supreme Court of the Republic of Tatarstan dated March 14, 2011 N 33-2570/2011). Rostrud specialists still adhere to the same opinion.

From authoritative sources Shklovets I.I., Rostrud “When deducting from an employee’s salary the provisions provided for in Art. 137 of the Labor Code of the Russian Federation (with the exception of vacation pay for unworked vacation days) written consent should be obtained from the employee. This is confirmed by judicial practice.”

An employee can formalize his consent to retention as follows.

Condition 3: The withholding order is issued in a timely manner.

An order (instruction) on withholding must be issued no later than a month from the date of expiration of the period for the return of excess payments. And you can directly withhold money from the employee’s salary later (Article 137 of the Labor Code of the Russian Federation; Cassation ruling of the Supreme Court of the Udmurt Republic dated October 3, 2011 N 33-3519/11), that is, when paying the employee’s salary. Moreover, the withholding, taking into account the restrictions on its amount, can last for several months.

In the order, indicate the basis and amount of the withholding. And familiarize the employee with it against signature (Article 22 of the Labor Code of the Russian Federation).

Condition 4. The amount of deductions for each payment does not exceed 20%

For each salary payment (that is, from amounts after deducting personal income tax), you can withhold no more than 20% (Article 138 of the Labor Code of the Russian Federation). Do not forget to indicate the basis and amount of the deduction on the pay slip issued to the employee (Article 136 of the Labor Code of the Russian Federation).

Well, if the employee agrees to have more than 20% withheld from him, then you can deduct from his salary any amount indicated by him in his written statement. Indeed, in this case, the debt is repaid by the employee voluntarily, and not by order of the employer. Therefore, restrictions on the amount of deductions do not apply (Articles 130, 138 of the Labor Code of the Russian Federation). And there is no need to issue an order for such deduction; just one application from the employee is enough.

Condition 5. The order of deductions is observed

First of all, as you know, personal income tax must be withheld from your salary (Letter of the Ministry of Health and Social Development of Russia dated November 16, 2011 N 22-2-4852).

From the remaining amount, you withhold the employee’s debt under enforcement documents (writs of execution, court orders, etc.) (Article 138 of the Labor Code of the Russian Federation).

And only if you do not have executive documents in relation to the employee or the deductions for them amounted to less than 20% of the employee’s salary, you can deduct from it his debt to your company, of course, subject to the total amount of all deductions - no more than 20% of the salary.

Advice: Observe all the conditions listed above when holding. Indeed, if any of them is not observed, the employee may, through the court, declare the retention illegal. And then the amounts withheld from him will be recovered from your organization back - in his favor (Determinations of the St. Petersburg City Court dated 03/07/2012 N 33-2718, dated 01/16/2012 N 33-238; Kamchatka Regional Court dated 01/22/2009 N 33- 38/2009; Cassation rulings of the Supreme Court of the Udmurt Republic dated October 19, 2009 N 33-2803; Kaliningrad Regional Court dated August 3, 2011 N 33-3553/2011).

Types of excess payments

From the salary (Article 129 of the Labor Code of the Russian Federation), the employee is allowed to deduct:

- vacation pay for unworked vacation days . Such debt may arise if an employee is dismissed before the end of the working year for which he has already received annual paid leave. You can deduct the employee's debt from the “severance” payments due to him. However, upon dismissal for some reasons, overpaid vacation pay cannot be withheld. For example, upon dismissal:

- in connection with a reduction in staff or number of employees (Clause 2 of Article 81 of the Labor Code of the Russian Federation);

- the employee’s refusal to transfer to another job, which is necessary for him according to a medical certificate, or the employer’s lack of appropriate work (Clause 8 of Article 77 of the Labor Code of the Russian Federation);

- conscription for military service (Clause 1 of Article 83 of the Labor Code of the Russian Federation);

- reinstatement at work of an employee who previously performed this work (Clause 2 of Article 83 of the Labor Code of the Russian Federation);

- unearned salary advances . This debt may arise, for example, when an employee was paid an advance payment of wages for that month at the beginning of the month, and the employee, without having worked it, went on vacation at his own expense or on sick leave before the end of the month;

- unspent and unreturned accountable amounts , including those issued when sent on a business trip (Letter of Rostrud dated March 11, 2009 N 1144-TZ);

- payments for failure to comply with labor standards or idle time (Articles 155, 157 of the Labor Code of the Russian Federation). Such a debt will arise if you pay an employee for downtime or shortcomings on the basis that they occurred through your fault or for reasons beyond the control of both parties, and then it turns out that the employee was to blame. In this case, excess payments can be withheld only after you go to court and the court establishes the employee’s guilt in idle time or underperformance (Determination of the Moscow Regional Court dated December 15, 2011 N 33-25895);

- amounts overpaid due to an accounting error .

Moreover, this is not necessarily a salary. This also includes any amounts erroneously paid to an employee as part of or in connection with the employment relationship. Rostrud specialists also think the same.

From authoritative sources Ivan Ivanovich Shklovets, Deputy Head of the Federal Service for Labor and Employment “According to Art. 137 of the Labor Code of the Russian Federation, the employer may withhold from the employee’s salary (in compliance with the procedure provided for in this article) the debt of this employee in the form of amounts overpaid to him due to accounting errors. The range of these amounts is not limited by this article. Therefore, it is possible to deduct from the salary any payments and compensations overpaid to the employee due to a counting error, provided for by labor legislation, local regulations of the organization, collective or labor agreement, for example, benefits, financial assistance, payment for travel to the place of training, compensation for the use of the employee’s personal property, insurance provision of insurance against industrial accidents and occupational diseases, etc. Deductions can only be made from wages. According to Art. 129 of the Labor Code of the Russian Federation, wages are remuneration for work (salary, official salary, tariff rate), as well as compensation payments (additional payments and allowances of a compensatory nature, including for work in conditions deviating from normal, work in special climatic conditions and in territories exposed to radioactive contamination, and other compensation payments) and incentive payments (additional payments and incentive allowances, bonuses and other incentive payments).”

There is no definition of a counting error in the Labor Code. The courts and Rostrud believe that only arithmetic errors in calculations are countable, that is, errors made as a result of incorrect application of the rules of mathematics (Letter of Rostrud dated October 1, 2012 N 1286-6-1). Therefore, courts, as a rule, do not recognize the following errors as counting:

- the same amount was transferred twice due to a technical error (Determination of the RF Armed Forces dated January 20, 2012 N 59-B11-17);

- the previously paid amount is not taken into account in the calculation (Determination of the Sverdlovsk Regional Court dated 02/16/2012 N 33-2365/2012; Cassation Determination of the Krasnodar Regional Court dated 02/14/2012 N 33-3340/12);

- incorrect initial data were used in the calculation (for example, the wrong tariff or coefficient (Appeal ruling of the Oryol Regional Court dated June 20, 2012 N 33-1068), the wrong number of days (Cassation ruling of the Khabarovsk Regional Court dated 02/08/2012 N 33-847/2012) );

- the salary in the program was doubled due to an error in the calculation algorithm (Appeal ruling of the Bryansk Regional Court dated 05/03/2012 N 33-1077/12);

- when calculating, the norms of the organization’s local regulatory act were incorrectly applied (Appeal ruling of the Moscow City Court dated July 16, 2012 N 11-13827/12).

Courts reach other conclusions extremely rarely. For example, the Samara Regional Court indicated that counting errors include not only arithmetic errors, but also software failures (Determination of the Samara Regional Court dated January 18, 2012 N 33-302/2012).

And the Rostov Regional Court, reviewing a case in which “severance” payments were transferred to a dismissed employee by mistake, came to the conclusion that there was a counting error. Since the total amount of transfers exceeded the amount accrued in favor of the employee (Cassation ruling of the Rostov Regional Court dated September 12, 2011 N 33-12413).

We warn the manager If the employee was overpaid in amounts as a result of an uncountable error and he refused to return these amounts voluntarily, it will be possible to recover them from him only in court as unjust enrichment (Article 1102, paragraph 3 of Article 1109 of the Civil Code of the Russian Federation).

The fact that a counting error was made when calculating payments in favor of the employee must be documented. For example, an accountant may write a memo addressed to the manager. Or let a specially created commission from among the company’s employees draw up a report on the discovery of a counting error.