What are monetary documents

Today in Russia there is no normative definition for the concept of “monetary documents”.

A unified register of monetary documents has not been developed either. Regulatory legal acts indicate only the main features and examples of such documents (see instructions approved by order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n; hereinafter referred to as Instruction No. 157n). It is generally accepted that monetary documents in budget accounting are understood as objects of a certain nominal value that are purchased and stored in an institution, but services for them have not yet been provided. The most famous examples of this kind of documents are coupons for gasoline or food, postage stamps, envelopes with stamps, notices for postal orders, vouchers to sanatoriums or children's health camps, etc. These assets also include payment cards for mobile communications, IP-telephony for long-distance, international calls, Internet access, airline and railway tickets, public transport tickets, etc.

There is a category of documents that have a value, but for accounting purposes are not recognized as monetary documents. In particular, these are:

- shares that were purchased from shareholders;

- securities;

- strict reporting forms (see “Budget accounting: how to store, account for and write off BSO in a budgetary institution”);

- documents for intangible assets.

How to reflect monetary documents in accounting policies

The answer to the question of exactly which assets will be considered monetary documents must be fixed in the institution’s accounting policies. The procedure for their accounting, storage and write-off is also prescribed there. All these procedures are regulated by several instructions and orders of the Russian Ministry of Finance, a full list of which you can see below.

The main documents that regulate the work of a budgetary institution with monetary documents:

- Instructions for the application of the Unified Chart of Accounts for public authorities (state bodies), local governments, management bodies of state extra-budgetary funds, state academies of sciences, state (municipal) institutions (approved by order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n);

- Instructions for the use of the Chart of Accounts for Budget Accounting (approved by order of the Ministry of Finance of Russia dated December 6, 2010 No. 162n);

- Instructions for the use of the Chart of Accounts for accounting of budgetary institutions (approved by order of the Ministry of Finance of Russia dated December 16, 2010 No. 174n);

- Instructions for the use of the Chart of Accounts for accounting of autonomous institutions (approved by order of the Ministry of Finance of Russia dated December 23, 2010 No. 183n);

- Order of the Ministry of Finance of Russia dated March 30, 2015 No. 52n “On approval of forms of primary accounting documents and accounting registers used by public authorities (state bodies), local government bodies, management bodies of state extra-budgetary funds, state (municipal) institutions, and guidelines for their application."

We have collected in a table examples of wording that can be used in an organization’s accounting policies:

| Chapter | What to write in the accounting policy |

| Organization of accounting | The list of positions of employees who have the right to receive monetary documents and funds on account for the purchase of goods (payment for work, services) is given in Appendix No.... to this Accounting Policy. The issuance of funds and monetary documents for reporting is carried out in accordance with the relevant Regulation No.... to this Accounting Policy |

| Inventory procedure | To confirm accounting data and annual financial statements, an inventory of property and financial liabilities is carried out:

|

| Accounting for financial assets | The following are taken into account as part of monetary documents (at the institution’s choice):

Monetary documents are accepted into the institution's fund office and are accounted for at actual cost. |

For each type of monetary documents, it is necessary to develop separate local regulations (LNA) - regulatory authorities are always interested in them during regular and extraordinary inspections. Each LNA should indicate the positions of employees who have the right to receive the corresponding type of monetary document, as well as the mandatory conditions and rules for its use.

A correctly drafted local regulatory act should justify the advisability of using monetary documents in a budgetary institution. To do this, you need to carefully define the algorithm by which employees will confirm their expenses.

RULES FOR STORING CASH AND VALUABLES

111. Heads of communication organizations are obliged to ensure the safety of cash at the cash desk, as well as when delivering cash from the bank or depositing it at the bank, and are responsible in cases where, through their fault, the necessary conditions were not created to ensure the safety of cash.

The head (deputy head) of the post office is obliged to organize proper storage and ensure complete safety of cash and valuables located in the post office.

112. To store cash and valuables, vaults are equipped in the main cash registers, and storage rooms in post offices.

In the storage room of the main cash register of the communication organization, safes are installed in the required quantity for storing cash and monetary documents, storing (separate from cash) canvas bags with cash received or prepared for shipment, and metal cabinets for storing valuables.

In vaults, cash and valuables are stored in metal cabinets or safes, which are locked with a key and sealed after the main cash register is closed. It is allowed to store cash and foreign currency in one metal cabinet or safe, provided they are placed separately.

Keys to metal cabinets and safes, stamps are kept by operators (cashiers). Leaving keys in the keyholes of metal cabinets and safes, designated places, handing them over to unauthorized persons, or making unaccounted for duplicates is not permitted.

The premises of the main cash desk of a communication organization must be isolated, and the doors to the cash desk must be locked from the inside during transactions. Leaving keys in the holes of safes, metal cabinets and vaults during cash transactions is not allowed. Access to the premises of the main cash desk of a communication organization for persons not related to the work there is not allowed.

(as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

The requirements stipulated by parts two to five of this paragraph to ensure the safety of cash and valuables are also applied to the equipment of post office storerooms.

The main cash desks of communication organizations must be equipped with security and fire alarms and alarm buttons with output to the centralized monitoring console of territorial internal affairs bodies.

Requirements for technical strengthening and equipping the premises of the main cash desks of communication organizations with technical means of security, alarm and fire alarms are determined with the participation of representatives of communication organizations and competent government bodies in accordance with the law.

In the storerooms of post offices, cash and valuables are stored in safes or metal cabinets, which, at the end of the post office's work, are locked with a key and sealed with a clear seal or sealed with an unauthorized opening label with a calendar stamp and signatures of the persons involved in closing the safes and metal cabinets.

Storage of consumer goods, newspapers, magazines is carried out on racks in the storerooms of communication departments.

The keys to safes with cash are kept by the head (deputy head) of the communications department, the keys to metal cabinets with valuables are kept by the persons to whom these valuables are issued on account.

113. Upon completion of work, checking the cash register and the balance of valuables in the main cash register of the communication organization, all storage facilities are closed by the head (operator) of the main cash register of the communication organization with locks and sealed with control seals.

(as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

Safes and metal cabinets located in the storage facilities of communications organizations are sealed with a control seal, and the entrance doors to the main cash desk of a communications organization, after being locked, are sealed with two seals: insurance and control.

When closing the main cash desk of a communications organization by two employees, the control seal, keys to safes, metal cabinets and keys to the remaining locks of the vault doors are kept by the head of the main cash office of a communications organization (the person replacing him). The insurance seal and the key to the internal lock of the front door are kept by the second employee, who signs in the log of receipt and delivery of the insurance seal and key in the form in accordance with Appendix 19 to these Instructions, indicating the date and time of their receipt and delivery.

(Part three, paragraph 113 as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

When closing the main cash register of a communications organization by one employee, the keys, control and insurance seals are kept by the employee who completes operations at the main cash register of a communications organization.

(part four of paragraph 113 as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

114. All copies of spare keys (duplicates) are deposited with the head of the communications organization:

at the main cash desks of communication organizations - from the entrance doors and all internal premises, from safes and metal cabinets;

for other postal facilities (post offices, postal service points and other departments) - from all entrance doors (including emergency exits), storerooms (storages) where postal items, valuables are stored, from safes and metal cabinets.

(as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

Before delivery to the head of the communications organization, all spare copies of keys (duplicates) are packed in a bag, which is lined with fabric and sealed with a seal or tamper evident label.

In communications organizations and post offices, safes and metal cabinets are numbered in sequence. The numbering of keys for each post office is carried out separately. Tags indicating numbers in the form of a fraction are attached to spare copies of keys (the numerator is the serial number of the key, the denominator is the serial number of the safe or metal cabinet).

The number indicated on the tag is reflected in the inventory of spare copies (duplicates) of keys to entrance doors, vaults, safes, metal cabinets of the main cash desk of the communication organization and postal offices (hereinafter referred to as the inventory) in the form in accordance with Appendix 20 to this Instruction. The inventory is filled out in two copies. The first copy of the inventory along with the keys is included in the package, the second copy (copy) of the inventory with a receipt from the head of the communications organization about acceptance of the package is kept by the head of the main cash desk of the communications organization or the head of the communications department.

The head of the communications organization indicates the packages with spare copies of keys accepted for storage in the list of packages with spare copies (duplicates) of keys to entrance doors, vaults, safes, metal cabinets of the main cash desk of the communications organization and postal offices, which are in the custody of the head (supervisor) ( hereinafter referred to as the list), in the form in accordance with Appendix 21 to these Instructions.

Checking the availability and compliance of spare copies of keys in storage is carried out at least once a year, as well as during a documentary check and, without fail, when changing the head of a communications organization, the head of the main cash desk of a communications organization or the head of a communications department.

The transfer of packages with spare copies of keys when changing the head of the communications organization is carried out against a receipt for the acceptance and delivery of the packages in the list. In the temporary absence of the head of the communications organization (vacation, business trip, illness and other reasons), the transfer of packages with spare copies of keys to the person acting as the head of the communications organization is also carried out against a signature on the list.

The head of the communications organization issues packages with spare copies of keys to officials during an inspection or in other cases against a receipt in the journal for issuing packages with spare copies (duplicates) of keys for conducting checks at postal facilities in the form in accordance with Appendix 22 to this Instruction. The results of the inspection are noted on the reverse side of the first and second copies of the inventory.

In case of loss of keys or identification of other inconsistencies, an act is drawn up for opening the package with spare copies (duplicates) of keys to entrance doors, vaults, safes and checking the keys (hereinafter referred to as the act) in the form in accordance with Appendix 23 to this Instruction in two copies. One copy of the act, together with a package of spare copies of keys, remains at the main cash desk of the communications organization or the communications department, the second copy of the act, together with the inventory located inside the package, is transferred to the head of the communications organization. As soon as possible, it is necessary to take measures to eliminate the comments on the report, bring spare copies of keys into compliance, and ensure re-checking. In case of replacing a lock or making duplicate keys, the act indicates the total number of keys for this lock.

115. The opening of vaults and safes is carried out by the persons who closed and sealed them.

(as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

Before opening the premises of the main cash desk of a communications organization, storage rooms, safes, metal cabinets, the employee (employees) of the main cash desk of a communications organization is obliged to inspect the safety of locks, doors, window bars and seals, and make sure that the security alarm is in working order.

(as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

The main cash desk of the communication organization is removed from the security alarm, the alarm is turned on, the seals are not broken, but are cut off along with the cord. After opening and inspecting the storage facility, if there is no damage, the removed seals are stored until the end of the working day, after which they are destroyed.

The requirements provided for in parts one through three of this paragraph also apply to the opening of post office storerooms.

116. In case of damage or removal of the seal, if it is discovered that keys are lost, locks, doors, window bars are broken or the security alarm is malfunctioning, this is immediately reported to the head (deputy head) of the communications organization, who must notify the territorial internal affairs bodies about the incident and upon the arrival of their employees, take measures to protect the main cash desk of the communications organization.

The head of the communications organization, the chief accountant (deputy chief accountant, leading accountant) or their substitutes, the head (operator) of the main cash desk of the communications organization, after receiving permission from the territorial internal affairs bodies, check the availability of cash and valuables in the storage facility. The check must be carried out before the start of operations for receiving and issuing cash and valuables from the main cash desk of the communication organization. An act on the results of the inspection is drawn up in triplicate, which is signed by all persons participating in the inspection. One copy of the act is transferred to the territorial internal affairs bodies, the second is sent to a higher organization of the Ministry of Communications and Information, the third remains with the communications organization.

117. If it is necessary to open a storage facility in the absence of persons who participated in its closing and sealing, the head of the communications organization creates a commission that opens the storage facility and checks the cash and valuables in it.

118. During operations in post offices, cash and valuables are stored at the workplaces of operators (cashiers) in special metal boxes, cabinets or desk drawers, adapted for this purpose and having working locks.

Operators (cashiers) of shifts do not have the right to leave cash, valuables and monetary documents in desk drawers during temporary absence and at the end of operations, as well as transfer cash during the day to another operator (cashier) without documenting such a transaction.

During shift and round-the-clock operation, operators (cashiers), telephone office and telegraph workers transfer cash and monetary documents to the head (deputy head) of the communications department or a person authorized by him, against a receipt in the cash certificate of the MS-42 form.

At the end of the working day, cash and monetary documents must be handed over to the main cash desk of the communications organization.

At the end of work, after checking and replenishing advances of valuables, operators (cashiers) are required to lock special metal boxes, cabinets and desk drawers with a key and seal them with control seals (kept by these employees) or tamper-evident labels.

119. The head (operator) of the main cash desk of a communications organization, the head (deputy head) of a communications department, or the operator (cashier) of a communications department is not allowed to:

delegate the fulfillment of their duties regarding cash transactions to other persons;

transfer cash and valuables to each other without issuing a receipt in the relevant documents (cashier’s book, cash certificates of the MS-42 form, etc.);

leave your workplace until the end of the transaction (customer service, etc.);

when temporarily absent from the workplace, leave cash, monetary documents, cash documents, valuables, seals, seals not locked in safes, metal cabinets or desk drawers;

leave keys in the keyholes of safes, metal cabinets, desk drawers intended for storing cash and valuables;

store personal money and valuables together with the cash and valuables of the communication organization.

120. In communication organizations with shift work on the eve of the day off, at the end of work (shift), the head (operator) of the main cash desk of the communication organization, when transferring cash, monetary documents and valuables of the main cash desk of the communication organization to the person replacing him, displays the balance of cash in the cash book money and monetary documents at the time of transfer.

The transfer of cash, monetary documents, and valuables is carried out according to a certificate of form MS-47, which is drawn up in two copies. The first copy of the MS-47 form certificate is transferred to the accounting service, the second remains in the main cash desk of the communications organization.

Further recording of transactions with cash and monetary documents in the cash book is made by the person who accepted the main cash desk of the communication organization.

Calculating the totals for the day and submitting the cash report of the head (operator) of the main cash register of the communication organization to the accounting service, checking the main cash desk of the communication organization is carried out by the last shift worker of the main cash desk of the communication organization.

During the shift transfer of cash, monetary documents and valuables of the main cash desk of a communications organization, the transfer of state postage stamps, marked envelopes and marked postcards, postcards, unmarked envelopes and unmarked art cards, and philatelic products is not carried out.

121. If it is necessary to temporarily replace (vacation, business trip, illness and other reasons) the head (operator) of the main cash desk of a communications organization, if there is only one employee on staff, the performance of his duties is assigned by order of the head of the communications organization to another employee. In this case, cash and valuables located in the main cash desk of the communications organization are counted by the employee to whom they are transferred, in the presence of the head and chief accountant (deputy chief accountant, leading accountant) of the communications organization or persons authorized by the head of the communications organization. An act signed by the indicated persons is drawn up regarding the transfer of cash and valuables.

(as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

In the temporary absence of one of the employees of the main cash desk of a communications organization, the reception and transfer of cash and valuables located in the main cash office of a communications organization are also carried out according to an act and in the presence of the head and chief accountant (deputy chief accountant, leading accountant) of the communications organization or persons authorized by the head of the organization communications.

(as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

122. Within the time limits established by the head of the communications organization, but at least once a quarter, as well as when there is a change in the head of the communications organization, an unscheduled inventory is carried out with a complete sheet-by-sheet (piece by piece) count of cash, monetary documents and valuables located in the main cash desk of the communications organization, in accordance with the general rules established in the Instructions for Inventory of Assets and Liabilities, approved by Resolution of the Ministry of Finance of the Republic of Belarus dated November 30, 2007 N 180 (National Register of Legal Acts of the Republic of Belarus, 2008, N 16, 8/17745).

123. Communication organizations conduct daily checks of the availability of cash and monetary documents in the main cash desk of the communication organization after the completion of transactions.

Based on the results of checking the main cash register of the communication organization, in the cash book, signed (signatures) of the employee (employees) of the main cash register of the communication organization, through carbon paper, an o or “The cash register has been checked, discrepancies have been established in the amount of ____________”, the amount of the actual cash balance in the main cash register of the organization is indicated communications, date and signatures are affixed.

In case of any discrepancies identified, a report is drawn up and submitted to the accounting service of the communications organization.

(clause 123 as amended by the resolution of the Board of the National Bank dated May 29, 2014 N 352)

CHAPTER 9

How to store, use and write off

Since the institution has already paid, but has not yet redeemed the monetary documents, they must be kept in the cash register. These documents are reflected in the stock register if:

- purchased by bank transfer;

- purchased for cash by one person, but will be spent by another person;

- are issued to employees in parts, and the balance is kept in the cash register.

Please note: if an accountable person purchases monetary documents and immediately spends them, then they are written off according to the advance report and do not go through the cash register.

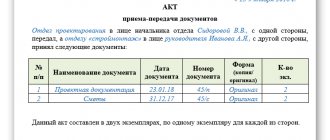

To record the receipt of monetary documents at the cash desk and their release from the cash register, you need to use incoming cash orders (form 0310001) and outgoing cash orders (form 0310002). These forms were approved by Order of the Ministry of Finance of Russia dated March 30, 2015 No. 52n (hereinafter referred to as Order No. 52n). On the orders it is necessary to make the inscription: “Stock”, and then record them in the journal for registering incoming and outgoing cash documents. These records should not overlap with those reflecting cash flows.

For the stock cash register, you should keep a separate cash book with continuous numbering and the mark “Stock” on each sheet. Entries are made to it after receipt or issuance of monetary documents for each stock order. Please note: the lines “including wages” and “total cash balance in the cash register at the end of the day” in this cash book remain blank.

Control over monetary documents in a budgetary institution is carried out as part of regular checks of the cash register. Based on the results of the audit, an inventory list (matching sheet) of strict reporting forms and monetary documents is compiled (form 0504086). The rules for filling it out are regulated by Order No. 52n.

The head of a budget institution is responsible for compliance with the requirements for the storage, use and accounting of monetary documents in a budgetary institution. It determines the procedure and timing of control activities.

Rules for storing money in the cash register

To make cash payments, organizations must have a cash register and maintain a cash book in the prescribed form.

To store funds, each organization must be equipped with a cash desk - an isolated room designed for receiving, issuing and temporary storage of cash. The cash register should be in the central office, and in each pharmacy the functions of the cash register are performed by the manager's office or a material room in which there is a safe for temporary storage of cash. The safe stores cash during the working day, and the cash limit is also locked in the safe at night. In addition to revenue, the safe stores cash for change (change). Cash must be stored in a fireproof safe, and the cashier does not have the right to store valuables that do not belong to the organization in the cash register of the organization. The keys to the safe and cash drawer are kept only by the cashier and cannot be given to anyone. Upon completion of work, safes are locked with a key and sealed with the cashier's seal. If, during a tax audit, it turns out that the amount in the cash register exceeds the amount shown in the documents, then in this case the organization will face a fine.

Limit

An organization, when selling goods to the public, receives proceeds from sales mainly in cash, which are accepted at the cash desk and then subject to delivery to the bank for subsequent crediting to the organization’s account. The amount of cash that an organization can leave in the cash register at the end of the working day is limited. This restriction is called the cash balance limit at the cash register; the size of the limit is set annually by the manager; all pharmacy managers are familiar with the order if there are several pharmacies in the organization. Organizations, regardless of the general public fund and the field of activity, are required to store available funds in banks; they can have cash in their cash registers within the limit of the cash balance in the cash register.

Every year, to ensure the normal operation of the organization, taking into account the average daily revenue and cash consumption, the head of the pharmacy organization sets a limit on the amount of money in the cash register, as well as the procedure and timing for depositing proceeds into the bank. The limit on the balance of money in the cash register is approved by order, the document is stored in the organization. After setting a limit on the balance of money in the cash register, the organization sends a notification about this to the bank in which it has accounts.

Letter No. 18 of the Central Bank of Russia: enterprises are required to keep available funds in banks (revenue is deposited daily for collection). The bank issues the organization a document “Calculation for establishing a cash balance limit for the enterprise.” The amount of the cash limit is not established by law; it is determined based on the characteristics of the organization’s work; for one organization it is enough to have a limit of 500 rubles, and for another 10,000 rubles.

All cash coming into the organization must be deposited at the bank at the end of the day. There should be no excess amounts in the cash registers. If necessary, cash register limits are revised.

Enterprises can have cash in their cash registers within limits (a certain amount), which is established by the manager. To make cash payments, each enterprise must have a cash register and maintain a cash book. In this case, the cash book is kept in the office by the chief accountant.

Storing money in the cash register in excess of the limit for issuing salary is carried out for the regions of the Far North for 5 days, and for other regions for 5 days, after which the unissued salary is returned to the bank.

Businesses are required to hand over to the bank all cash in excess of established limits. The bank does not accept banknotes of less than 100 rubles.

The procedure for registration, storage, destruction of the control cash tape

In addition, a control tape must be used on all cash registers, and a cashier-operator’s log certified by the tax authority must be kept for each cash register.

Control tapes, cashier-operator’s journal and other documents confirming,

carrying out cash settlements with buyers (clients) must be stored for the periods established for primary accounting documents, but not less than 5 years. The head of the organization is responsible for ensuring the storage of these documents. Violations of the above obligations identified during inspections may result in significant penalties.

According to the Regulations on the use of cash registers, checks, control tapes and other documents provided for by technical requirements and printed using cash registers in fiscal mode must have a distinctive feature specified in the technical requirements for fiscal (control) memory.

TOPIC 3. PROCEDURE FOR CONDUCTING CASH OPERATIONS

Lecture No. 2. Incoming and outgoing cash transactions. The procedure for conducting cash transactions. Return of goods by the public

Subtleties of analytical accounting of monetary documents

Analytical accounting of monetary documents is differentiated by their types in the card for accounting for funds and settlements (form 0504051). This is stated in paragraph 171 of Instruction No. 157n. The card begins with records of balances at the beginning of the year. New entries are made no later than one day after the transaction. Balances are summarized at the end of each month.

All transactions with monetary documents are recorded in the journal for other transactions. The basis for each new entry must be the cashier’s report and the documents attached to it (form 0504071). Just like an accounting card, the journal is opened with balances at the beginning of the period. It reflects turnover for the entire period and displays balances.

Accounting for strict reporting forms

Strict reporting forms are not inventories, therefore, an off-balance sheet account 03 is provided for accounting - the debit of this account reflects the receipt of forms.

In the accounting policy of the institution, it is necessary to indicate at what cost the forms are accepted for accounting: either at the real cost of the purchase, or at 1 ruble per form (in practice, the second option is more often used).

The institution maintains the above-mentioned journal for other transactions (form 0504071) in off-balance sheet account 03 “Strict reporting forms”. The journal must be filed along with primary documents indicating the movement of the forms.

More on the topic: Consultation line “Accounting in 1C: BSU”. Issue No. 52/20

Analytical accounting of strict reporting forms is maintained in the Book of Accounting of Strict Reporting Forms (form 0504045, approved by Order of the Ministry of Finance of Russia dated March 30, 2015 No. 52n) by type, series and number. It indicates the date of receipt or issue of forms, their quantity and cost. At the end of the reporting period, the data is analyzed and the balance is displayed. The pages of such books are numbered, and the books themselves must be laced and sealed.

Rules for accounting of monetary documents

All accounting operations for monetary documents and corresponding accounting records can be divided into two groups:

| Contents of operation | Debit | Credit |

| Receipt of cash documents | ||

| Receipt from the supplier to the cash register | 0 201 35 510 | 0 302 XX 730 |

| Spending by an accountable person or return to the cash desk of previously issued accounts | 0 201 35 510 | 0 208 XX 660 |

| Identification of surpluses during inventory | 0 201 35 510 | 0 401 10 180 |

| Disposal of monetary documents | ||

| Issue from cash register to reporting | 0 208 XX 560 | 0 201 35 610 |

| Return from the cash register to the supplier according to the terms of the contract | 0 302 XX 830 | 0 201 35 610 |

| Write-off of shortage | 0 209 82 560 | 0 201 35 610 |

| Write-off for emergency expenses (theft, damage, destruction) | 0 401 10 172 0 401 20 273 | 0 201 35 610 |

Please note: if an institution issues both cash and monetary documents to the same employees, then payments must be made in different accounts. For example, additional analytical codes can be added to the account “208 00”.