What is a tax deduction

There is a personal income tax (NDFL), which is 13%. It is charged, for example, from your official salary. An ordinary employee doesn’t even have to deal with this, since an accountant at your company handles the accruals and you usually receive your salary with tax deducted. This money goes to the state budget and then the money received is distributed for various needs, including the payment of child benefits, salaries for doctors, teachers, police officers, firefighters, deputies and other public sector employees.

In some cases, which will be discussed in this article, the state allows not to collect this tax, or to return the previously transferred personal income tax. Thus:

A tax deduction is a certain amount of income that is not taxed, or a refund of part of the personal income tax you previously paid in connection with expenses incurred under certain tax code categories, which include, for example, expenses for the purchase of residential property, education, treatment, purchase of medicines, etc.

Example

Your company has awarded you 100,000 rubles in salary for the year. Personal income tax will be 13% of this amount. You will receive 100,000 – 13% = 87,000 rubles. But now you have issued a deduction for your child’s education in the amount of, say, 50,000 rubles. We subtract this amount from total income: 100,000 – 50,000 = 50,000 rubles. This is your tax base after deductions.

And you receive a completely different amount in your hands: 100,000 – (50,000 * 0.13) = 93,500 rubles.

The difference between these totals in the amount of 6,500 rubles can be received at the beginning of the next year in one amount or in parts, starting from the next month. Read about two ways to apply for a deduction in the corresponding chapter below.

By providing deductions, the state encourages citizens to work officially, without any “salaries in envelopes,” and at the same time redirects additional funds from citizens to construction, education and healthcare. There are also deductions for all employees who have children or are involved in certain events. Read more about each type of benefit below.

A tax deduction is provided only if all conditions established by law are met. Each type of deduction has its own package of documents that must be provided to the tax authorities. There are also limitations.

Types of tax deductions

All deductions enshrined in Russian tax legislation are divided into four types:

- Standard;

- Social;

- Property;

- Investment;

- Professional.

Let's take a closer look at each of the deductions:

Standard tax deduction

The essence of the standard deduction is that each month a certain amount of income is not subject to tax. It is provided either to the taxpayer himself for participation in certain events (military operations, liquidation of the Chernobyl accident, etc.), or to a child. Unlike other types of deductions, this one is usually issued by the employer, although it is also possible to declare it through the tax office. Regulated by Article 218 of the Tax Code of the Russian Federation.

1 Deduction of 3,000 rubles monthly (the recipient’s benefit is 13% of this amount – 390 rubles). The following have the right to it:

- Liquidators of the accident at the Chernobyl nuclear power plant and victims of this accident (radiation sickness).

- Liquidators of the consequences of nuclear tests and accidents.

- Disabled persons who received injuries, mutilations and illnesses in military service

- Disabled people of the Great Patriotic War.

2 Deduction of 500 rubles monthly (beneficiary benefit – 65 rubles). Provided:

- Heroes of the USSR and the Russian Federation

- Participants in combat operations (having the appropriate certificate)

- Disabled people (groups I, II, as well as disabled children)

- To other persons (the full list is in clause 2 of Article 218 of the Tax Code of the Russian Federation)

If it turns out that a person is entitled to two deductions at once (for example, the liquidator of the Chernobyl accident subsequently became a Hero of Russia), then the largest of them is applied.

3 Deduction for a child under 18 years of age (as well as for a full-time student, cadet, graduate student, resident or disabled person - up to 24 years of age) monthly until the recipient reaches an income of 350,000 rubles (for example, with a monthly salary of 40,000 rubles to achieve 350- thousandth limit will take 8 full months - during this time you will not pay income tax on the amount of the deduction). It is provided to parents, guardians, and adoptive parents upon their application, which is usually written in the employer’s accounting department. The deduction amounts in 2020 are as follows:

- For the first and second child - 1,400 rubles each (the recipient's monthly benefit is 13% of this amount - 195 rubles for each child).

- For the third and subsequent children - 3000 rubles. (recipient's monthly benefit is 390 rubles).

- For each disabled child under 18 years old and for a full-time student, graduate student, resident, intern, student - up to 24 years old, if he is a disabled person of group I or II - 12,000 rubles. for parents and adoptive parents (monthly benefit for the recipient is 1,560 rubles) and 6,000 rubles. for guardians and trustees (monthly benefit for the recipient is 780 rubles).

A single parent or adoptive parent is entitled to a double amount of any standard deduction for children (but if a single mother, for example, gets married again, the deduction again becomes single).

Also, a double deduction can be received by one of the parents if the other renounces his right.

Example

Sergei Biryukov has a 12-year-old son and is raising him alone. Biryukov’s monthly salary is 47,000 rubles. From this amount, he must pay 6,110 rubles in personal income tax every month. At the beginning of the year, the taxpayer wrote an application to the accounting department of his enterprise for a standard deduction. His income will reach 350,000 rubles in August. Accordingly, Sergey receives the right to deduction from January to July. During this period, his savings on personal income tax will be (1400 * 7 * 0.13) * 2 = 2548 rubles.

Social tax deduction

Deductions of this type are partial compensation of individuals’ expenses for education and medical care. All social deductions are annually entitled to 120,000 rubles of tax relief - that is, this amount of your income will not be taxed (and if personal income tax has already been transferred, it will be returned at the end of the year). It's just a matter of little things: you need to meet all the requirements of tax legislation, work officially and spend a certain amount on paid medical or educational services.

1 Deduction for paid medical services.

The following expenses can be reimbursed through your personal income tax refund:

- Expenses for treatment of yourself or your children and parents. This includes paid medical care in a hospital, clinic, ambulance station, and paid medical center. Dental treatment and prosthetics (except cosmetic). Sanatorium-resort treatment (at your own expense, not from the trade union). The full list of services is contained in the Decree of the Government of the Russian Federation No. 201 of March 19, 2001.

- Expenses for medications prescribed during treatment.

- Costs for voluntary health insurance (if the policy is paid for by a citizen and not by an employer).

You can apply for a social deduction for the listed services if medical institutions have a state license and are registered on the territory of the Russian Federation. An agreement must be concluded for each medical service, and payment must be confirmed by receipts. When purchasing medicines, a prescription is required on forms in form N 107/u with a mark on submission to the tax office.

The difference between the social deduction for treatment and others is that there is a list of types of medical care, as well as medications that are considered expensive. Their use allows you to receive a tax deduction without restrictions on the amount - in the full amount of your expenses. Read more about the deduction for treatment with examples of real situations in our article: Tax deduction for treatment.

2 Deduction for paid educational services.

The Tax Code of the Russian Federation provides several grounds for issuing a deduction for training:

- Own training. This can be higher, secondary, additional education, short-term courses in any form (full-time, part-time, evening, distance learning). In this case, the educational institution must have a license for educational activities. You can also receive a deduction when studying abroad.

- Education of a child up to 24 years of age. But here only face-to-face training is allowed. A deduction can be obtained for a child’s education in a paid school, in a private kindergarten, in retraining courses, in additional education schools, and so on.

- Education of the ward until he reaches the age of 24 years. The rule of full-time education also applies. Starting from the age of 18, the term “former ward” is used in the application and declaration.

- Tutoring a brother or sister until they are 24 years old. A mandatory requirement is full-time study. A brother or sister can be either full-blooded (from the same mother and father) or half-blooded.

Unlike the medical deduction, there is no tax benefit for a spouse's education. You cannot receive a deduction for the education of aunts, uncles, grandparents, nephews, grandchildren and other non-close relatives.

The amount of the deduction for education is no more than 120,000 rubles, if we are talking about one’s own education, as well as the education of a brother/sister. For the education of children, as well as wards, the maximum deduction is 50,000 rubles.

All information about the tax deduction for education with real-life examples is in our article: Tax deduction for education.

3 Deduction for financing a future pension. Regulated by clause 4 of Art. 219 of the Tax Code of the Russian Federation. Those who contribute the following contributions to the formation of pension payments are entitled to:

- To non-state pension funds.

- To insurance companies (voluntary pension insurance and life insurance for more than 5 years).

The maximum deduction amount is 120,000 rubles, but you need to take into account that this is a general figure for all social tax benefits. That is, if you have already issued a deduction for your child’s education for 50,000 rubles, then the most you can count on in the same year when applying for a deduction for voluntary pension insurance is 120,000 - 50,000 = 70,000 rubles (refundable - 13% from this amount – 9100 rubles).

It is not necessary to enter into agreements to finance a future pension in your favor; you can form pension contributions for your spouse, parents/adoptive parents or disabled children.

4 Deduction for charity. You can return 13% of your donations to the following organizations:

- List item

- List item

- List item

To receive a deduction, you must submit an agreement with a charitable organization or NPO. The deduction should not exceed 25% of the income received during the tax period.

Example

Ivanov M.M. transferred 300,000 rubles to the Open Heart Foundation (an NGO that finances operations for sick children). Ivanov’s official annual income is 480,000 rubles. Accordingly, the deduction cannot exceed 480,000: 4 = 120,000 rubles (13% of this amount to be refunded: 15,600 rubles).

There are cases in which the deduction is not provided:

- If the money was transferred not to the organizations listed above, but to the funds established by them.

- If it was not money that was transferred, but goods or services (items implying a benefit) - for example, premises were transferred, advertising services were provided, and so on.

- If the money was transferred to another individual. Unfortunately, direct assistance to the families of sick children is not subject to deductions, since the possibility of abuse is high.

Please note that charitable activities are regulated by Federal Law No. 135-FZ of August 11, 1995.

Property tax deduction

From the name of the benefit it is clear that it is provided for certain actions performed with property. Since most often we are talking about large amounts of personal income tax refunds, such deductions are processed primarily through the tax office. Unlike social deductions, property deductions unused in the current year can be carried over to the next year.

You can return personal income tax (13% of the amount of expenses) for the following actions:

1 Sale of property.

When selling residential real estate and shares in it, as well as land plots, the maximum tax deduction is 1,000,000 rubles. This amount will be deducted from the cost of the apartment you sold, and you will pay personal income tax only on the balance. That is, if you sold an apartment for 2.2 million rubles, without deductions you would pay 286,000 rubles in income tax (13% of the amount received from the buyer). And using the deduction, you will pay personal income tax only on 1.2 million rubles (2,200,000 - 1,000,000), that is, 156,000 rubles. That is why sellers often offer to include in the purchase and sale agreement not the real cost of the apartment, but precisely 1 million rubles - so that, taking into account the deduction, they do not have to pay personal income tax at all. But the tax service saw through this trick a long time ago, and such transactions are now receiving increased attention.

For other property (cars, garages, non-residential premises) a deduction of 250,000 rubles is established. These amounts apply to all properties sold during the past year combined. Having sold three cars for a total amount of 600,000 rubles, you will still only receive a deduction for 250,000 rubles. When selling property that was in shared or joint ownership (for example, between a husband and wife), the deduction is divided into two parts - in proportions that the owners set themselves.

Please note: property that you have owned for more than 3 years is not subject to personal income tax upon sale. The exception is residential real estate. From May 1, 2021, it is not subject to income tax upon sale if it has been in your property for more than 5 years (except for those received under a gift agreement, under a maintenance agreement with a dependent, or just privatized - in these cases the three-year period still applies).

2 Purchase of an apartment, isolated room, house, dacha, land plot (or a share in any of these objects).

The deduction can be obtained for both finished and under construction objects. Until 2014, it was possible to return personal income tax for only one purchased object, now - for as many as you like, until the deduction amount reaches 2 million rubles. However, those who exercised their right under the old rules will not be able to re-issue the deduction.

Repair and finishing of housing purchased in a rough finishing state (both materials and work are deductible). Organization of electricity, water, gas supply and sewerage. Development of project documentation. The main condition is the presence of all supporting documents: contracts, checks, receipts. Read more about this type of deduction using the link below:

- Tax deduction when buying an apartment

3 Interest on the mortgage loan taken for the purchase of the above properties, as well as interest on the loan for refinancing the mortgage.

The maximum deduction for mortgage interest paid is RUB 3,000,000. It can be provided only after filing a deduction for the purchase of housing (maximum - 2,000,000 rubles), so in fact the deduction limit for purchasing an apartment with a mortgage is 5,000,000 rubles. This means that the state can theoretically return your personal income tax in the amount of 690,000 rubles.

A property deduction can be issued only if the property is located on the territory of Russia and is intended for human habitation.

Read more about the property deduction for purchasing a home with a mortgage with real examples here:

- Tax deduction for mortgage

Investment tax deduction

An investment tax deduction can be obtained in three cases:

- Deduction for income from the sale of securities held for more than three years. This type of deduction does not include transactions made on an individual investment account (hereinafter referred to as IIA);

- Deduction from the amount of funds deposited into an IIS within three years. The deduction is limited to the amount of 400,000 rubles. per year, or 1.2 million rubles. for three years. In one year you can return 13% of 400,000 rubles, or 52,000 rubles. This type of deduction is only suitable for employed individuals with official “white” wages;

- Deduction from income received from transactions in securities carried out on an individual investment account within three years. This type of deduction is not tied to salary and can be used by everyone, including individual entrepreneurs, as well as non-working people (for example, a family of two, where the husband works and the wife does not work, who can open an IIS in her name, but credit there the husband’s salary, or any other funds, including child subsidies and benefits).

What securities can you buy:

- stock;

- bonds;

- units of mutual investment funds; ETFs (units of foreign investment funds) traded on the Moscow Stock Exchange;

- foreign currency;

- futures and options.

Professional tax deduction

This type of deduction stands somewhat apart. In fact, we are talking about a benefit not so much for personal income tax, but for the income tax of an entrepreneur. However, since this entrepreneur is an individual and formally pays income tax, the deduction falls into the general category of others provided for individuals.

Professional tax deduction is provided for the following types of income:

- Income of individual entrepreneurs under the general tax regime (OSNO).

- Income of privately practicing notaries, lawyers and representatives of other professions who earn money in private practice.

- Income from civil contracts (contracts, services, etc.).

- Royalties, as well as remunerations for the performance or other use of works of science, literature and art. In this case, authors and inventors must be personal income tax payers.

A professional deduction is provided for the full amount of expenses (confirmed by contracts and receipts). If an individual entrepreneur is unable to confirm expenses, he can claim a deduction in the amount of 20% of the income received. For some types of remuneration (author's fees, for the performance of works, etc.), in the absence of documents confirming expenses, a cost standard has been established (the full list is in paragraph 3 of Article 221 of the Tax Code of the Russian Federation). For example, creators of video products - feature films or music videos - can claim a deduction in the amount of 30% of their income, and the authors of music for these films - in the amount of 40% of their income.

Limits on property tax deductions

Property tax deduction is provided both for the acquisition of property and for its sale under certain conditions.

The deduction for the purchase of property consists of the following expenses:

- 260,000 rubles = a limit of 13% of the amount up to 2,000,000 rubles spent on new construction or the acquisition of residential real estate (shares in them), land plots for their construction in Russia;

- 390,000 rubles = limit of 13% of the amount up to 3,000,000 rubles spent on repaying interest on targeted loans (mortgage loans) received from Russian organizations or individual entrepreneurs, actually spent on new construction or purchase of housing in Russia (shares in German), a plot of land for its construction. A similar limit on the property tax deduction applies to the repayment of interest on loans received to refinance a mortgage.

In addition, there are tax deductions for income received by the taxpayer from the sale of real estate, provided that such an object was owned by the taxpayer for a minimum period of ownership of the real estate object or more (3 years for real estate acquired before 1.01. 2016, and 5 years for real estate acquired after January 1, 2016).

- 1,000,000 rubles is the maximum amount of tax deduction by which income subject to taxation at a rate of 13%, received from the sale of apartments, rooms, residential buildings, garden houses, dachas, land plots, as well as shares/shares in the specified property.

- 250,000 rubles is the maximum amount of tax deduction by which income received from the sale of other (movable and immovable) property, the list of which includes, for example, vehicles, non-residential premises, garages and other items, can be reduced.

Please note that if a taxpayer sold several pieces of property at once in one year, then the above limits are applied in the aggregate for all sold objects, and not for each property individually.

Who is entitled to a tax deduction?

Only those who paid it can return personal income tax. According to the Tax Code of the Russian Federation, the following are entitled to receive an income tax deduction:

- citizens of the Russian Federation working under an employment or civil contract and paying personal income tax;

- pensioners who continue to work or worked during the reporting tax period;

- foreigners who spend more than 180 days a year in Russia and pay personal income tax to the budget of the Russian Federation;

- citizens of the Russian Federation and foreign residents of the Russian Federation who sold property that was owned for less than three or five years (see above in the chapter “Property tax deduction”).

Where to go to get a deduction

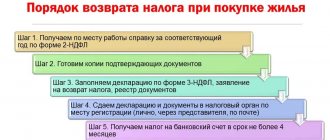

In Russian legislation, there are two ways to return personal income tax: through the tax office or through the employer. Each of these methods has its own order of execution.

Method #1. Tax refund through the Federal Tax Service

It is more convenient to receive a deduction from the tax office at your place of registration if you need the entire annual deduction amount at once. The benefit can be applied for at any time after the end of the reporting year. For example, if you bought an apartment in 2021, you can declare your desire to receive a deduction starting from January 1, 2021.

Income tax will be refunded for the reporting year in full in the amount of personal income tax you paid, but not more than 13% of actual expenses.

The procedure for applying for a deduction is simple. Its order is as follows:

- Collection of documents. Some of the paperwork is common to all deductions, while some is specific to each type of benefit. A detailed list is provided below in the relevant chapter.

- Submission of documents to the Federal Tax Service at the place of registration. This can be done in person, by post, through an authorized representative or via electronic communication channels through the website nalog.ru. If you do not know the actual address of your inspection, the easiest way to find it is on special services - for example, here: https://service.nalog.ru/addrno.do.

- Desk check. Over the course of several months, your documents are checked to ensure they meet formal requirements. All data in the provided papers must match the information in other documents.

- Income tax refund to your bank account.

Method #2. Tax refund through employer

In this case, you receive a deduction in parts: personal income tax is not withheld from your salary, the entire amount accrued by the accounting department is receivable. Another feature of this method is that you do not need to wait until the end of the year; you can receive money already in the current one. And in January of the next year, you have the right to file the remaining deduction through the Federal Tax Service and receive the entire remaining amount of personal income tax paid in the previous year at once.

Example

Alexander D. completed public procurement training courses in August-September 2021, spending 43,000 rubles on them and performed dental prosthetics in the amount of 214,000 rubles. Immediately after completing the courses, he filed a deduction with his employer and from October began to receive his salary in full, without withholding personal income tax (the amount of official non-taxable income was 24,800 rubles/month). Thus, for October, November and December, the deduction used amounted to 74,400 rubles. The maximum amount of social deduction is 120,000 rubles. At the end of 2021, Alexander D. exercised the right to return through the Federal Tax Service the balance of the income tax he paid in 2021 (January-September). D.’s income for 9 months of 2021 amounted to 24,800 *9 = 223,900 rubles, but personal income tax was returned to him only from 45,600 rubles (120,000 - 74,400 rubles already used in 2021)

To return personal income tax through an employer, you must do the following:

- Prepare a package of documents. The list differs from the similar one when registering a deduction through the Federal Tax Service. A detailed list is in the chapter “Documents required for tax deduction.”

- Submit documents to the tax office. This is done in the same way as when filing a deduction through the Federal Tax Service: in person, by mail, electronically through your personal account on nalog.ru or through a proxy. Within 30 days, the Federal Tax Service is required to issue you a notice to your employer that you have the right to a tax deduction.

- Next, you need to transfer the tax notice received to your employer. An application for a deduction must be attached to the tax paper (sample is on the website nalog.ru). You will receive your salary without personal income tax withholding from the month the notice is submitted until the deduction is exhausted or the year ends. Next year you need to go to the Federal Tax Service again to receive a notification for the employer.

What documents are needed to obtain a tax deduction?

There is a common set of documents for all deductions and a list required in each specific case.

General list of documents:

- Copy of Russian passport

- The tax return in form 3-NDFL is filled out by the taxpayer. Examples, templates and samples here: https://www.nalog.ru/rn77/taxation/taxes/ndfl/nalog_vichet/primer_3ndfl/#t1 (not presented when receiving a deduction from the employer)

- Certificate of income from the main place of work (form 2-NDFL, not presented when receiving a deduction from the employer)

- Certificates of part-time income (if any)

- An application to the Federal Tax Service with the details (on bank letterhead with a stamp) to which the tax will be refunded.

List of documents for receiving deductions for relatives (children/parents/brothers/sisters/spouses):

- copies of birth certificates for yourself, children, brothers and sisters (confirmation of relationship);

- copy of marriage certificate

Standards for setting deadlines

The most common issues require separate coverage and emphasis.

From what year can I get it?

Let's find out for what period you can get a tax deduction for the purchase of an apartment. You can apply for the benefit one year after purchasing an apartment . For the employer - almost immediately, after registering the transaction and receiving the appropriate permission from the Federal Tax Service.

Statute of limitations

The legislation does not establish a period for prolonging the deduction for future tax periods . For past periods, refunds are assigned for no more than 3 years.

For what period of time is it issued?

Now it’s worth talking about for which years you can get a tax deduction when buying an apartment. Documentation for obtaining a deduction for the previous tax period .

When to submit a declaration?

The declaration in form 3-NDFL is submitted annually, until April 30 . It provides information for the past year.

Tax return in form 3-NDFL: form, example of filling.

List of documents for deduction for treatment/purchase of medicines

Treatment in a medical institution (hospital, clinic, ambulance station, paid medical center):

- Agreement with a medical institution - original and copy. The contract must indicate the cost of services.

- A certificate confirming payment under the contract (must contain the patient’s medical card number and TIN, as well as the treatment category code: “1” - ordinary, “2” - expensive).

- A copy of the license of the medical institution.

Purchase of medicines:

- Original prescription in form 107-1/у with the stamp “For tax authorities.

- Checks, receipts, payment orders (to confirm payment)

- A certificate confirming the absence of an expensive drug in a medical institution (prepared in case the patient independently pays for expensive drugs prescribed by a doctor).

Conclusion of a voluntary health insurance agreement:

- Copy of the voluntary insurance agreement

- Copy of insurance company license

- Receipt or check for payment of insurance premium

How long does it take to receive a deduction?

The timing of tax refunds depends on the method of registration.

When registering through the Federal Tax Service

You can receive a deduction through the tax office in about 4 months, starting from January 1 of the next year. That is, if, for example, you completed training at a driving school in 2021, then from January 1, 2020, you have the right to submit documents for a personal income tax refund. It takes three months for a desk audit of the 3-NDFL declaration. If everything is in order, you have another 30 days to transfer the refunded tax. If you apply for a deduction for the purchase of real estate, the four-month period is valid only in the first year. When the unused balance is transferred to the next tax period, the desk check of documents for deductions is much faster - if you submit a declaration in early January, you can receive the money already in February.

When applying through an employer

You can receive a deduction (in the form of a salary without personal income tax withholding) starting from the next month after submitting to the accounting department of your organization a notification from the tax office about the right to a deduction, as well as an application for the provision of this deduction. If we are talking about property deductions that carry over to the next year in case of incomplete use, then they can be issued from the employer in the future, but it is more logical to return the balance of personal income tax in one amount by submitting documents to the Federal Tax Service.

How many times can you

As for the property deduction when purchasing real estate, the number of times is limited depending on the year the property was purchased.

If an apartment or house was purchased before 2014, then the application can only be made once in a lifetime, regardless of the amount of the deduction. For properties purchased after the specified date, you can apply multiple times within the established limit. This means that until the taxpayer reaches a deduction of 260 thousand rubles, he has the right to apply for a benefit for each apartment purchased.

IMPORTANT!

Once the amount is exhausted, the taxpayer loses the right to deduction for subsequent real estate purchases.

FAQ

– How does the amount of deduction compare with the amount of personal income tax returned? I'm confused about the calculations.

– To explain in simple words, a deduction is the amount of your income from which personal income tax will be returned to you when buying an apartment, training, treatment, etc. (this amount of income is deducted from the taxable income, hence the name - deduction). Since income tax in the Russian Federation is 13%, this percentage of the deduction amount declared in the 3-NDFL declaration will be returned to you. The deduction amount is equal to your expenses for education, treatment, purchase of housing, and so on. In this case, the deduction cannot exceed the maximum established by the Tax Code. For example, the limit for property deduction when purchasing a home is 2 million rubles. This means that even with a much more expensive purchase, they will return to you, at most, 13% of 2 million, that is, 260,000 rubles. And if the purchase cost less than 2 million, then they will return 13% of its full cost (this cost will be considered a tax deduction).

– Do the bank and type of account matter when applying for a personal income tax refund? Are there any restrictions?

– The Federal Tax Service works only with Russian banks (or Russian “subsidiaries” of foreign banks registered in the Russian Federation). The account must be in rubles. Otherwise, there are no restrictions: the money will be transferred to both the card and deposit accounts. Account details must be certified by the bank and submitted to the Federal Tax Service along with the tax refund application.

– Last year I bought an apartment and attended a driving school. Do I need to fill out two declarations or is one enough?

– One declaration is submitted for each year, in which you can indicate all your expenses for this period. You can claim a deduction for both the purchase of housing and education. Please note: only personal income tax paid can be returned to you, so if the deduction exceeds income, then it is better to declare the social deduction first - it cannot be carried over to the next tax period.

– I work three jobs. When submitting a declaration, am I required to attach three 2-NDFL certificates?

– How many certificates to submit is your decision. If the income from one job is enough to exhaust the deduction, other income does not need to be declared. But most often you have to indicate all income and submit to the Federal Tax Service all certificates in form 2-NDFL.

Application form

An application for a personal income tax refund can be prepared in three ways:

- In any form (by hand or in printed format).

- Using the form proposed by the Federal Tax Service.

- Using the “Legal Taxpayer” software, the instructions and download file of which are provided on the official portal of the Federal Tax Service in the “Software” section.

Custom format

When filing a deduction, a free form of request can be used, since there is no mandatory form for this procedure. The tax agent cannot refuse to register such an application, provided that it contains all the necessary information:

- name (or code) of the tax authority where the request is submitted;

- information about the applicant: full name, tax identification number, registration address, identification document details;

- grounds for receiving a deduction;

- bank details for making transfers;

- date, signature;

- copies of the required supporting documents.

Federal Tax Service form

The Federal Tax Service has proposed the KND form 1150058, which can be used to request a personal income tax deduction.

This form is also used to calculate overpaid taxes, contributions, fines and penalties. The form consists of three sheets that can be filled out manually or printed. The refund application form is divided into fields that must be filled out by the applicant and the tax officer. At the end of the form, on page 3, there are pointers that will make writing your request easier.

On the first page the applicant provides the following basic information:

- your TIN;

- application number (indicates the individual serial number of the taxpayer’s requests for the current year);

- code of the tax authority where the request is made;

- full name of the individual;

- grounds for receiving a deduction;

- the amount of the deduction;

- budget classification code (in this case, 182 1 0100 110 is used).

On the second page, bank details for receiving funds are entered. The third contains information about a document confirming the identity of an individual.

Sample filling:

"Taxpayer Legal Entity"

The Legal Entity Taxpayer software is designed to automate processes in the preparation of various documentation. The software will be an excellent assistant for individuals and legal entities and will simplify many tasks when generating applications, certificates, declarations, invoices, etc.

One of the functions of the program is the preparation of documents on personal income tax (2-NDFL, 3-NDFL, 4-NDFL, 6-NDFL and tax deductions). Using the software you can:

- automatically generate documents, while previously entered data is “pulled up”;

- generate paper or file for electronic transmission;

- save and restore data;

- fill out documents step by step using the “Wizard”.

You can download the software from the official portal of the Federal Tax Service at the link www.nalog.ru/rn77/program/5961229/.