What to do if it is impossible to collect a claim

In certain cases, it is impossible to obtain amounts of penalties and fines. Such situations include:

- lapse of time;

- the court's decision;

- liquidation of the debtor;

- reaching agreement through negotiations.

The amounts of claims are written off from account 76 to the account of the reserve for doubtful debts or to financial results (clause 77 of the Accounting Regulations, approved by order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n).

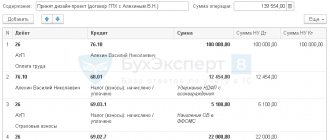

Gamma LLC entered into a purchase and sale agreement for materials with Delta LLC for a total amount of 100,000 rubles. Delta LLC is not a VAT payer.

In accordance with the terms of the agreement, Gamma LLC transferred a 50% advance to:

Dt 60 Kt 51 - 50,000 rub. (advance paid).

After the materials were delivered to the buyer, it turned out that the goods were worth 10,000 rubles. defective. The seller received a claim for this amount:

Dt 76/2 Kt 60 - 10,000 rub. (a claim has been made).

The management of Delta LLC got acquainted with the buyer’s requirements and decided to satisfy them, but not in full, but only for the amount of 8,000 rubles, since the goods were worth 2,000 rubles. was not defective, the buyer’s comments to it were unfounded:

- Dt 51 Kt 76/2 — 8,000 rub. (received based on the submitted claim);

- Dt 60 Kt 76/2 — 2,000 rub. (a claim not satisfied by the seller has been written off).

Debit 76 Credit 51

An accountant can post Dt 76 Kt 51 in the following cases:

- Payment has been made for property or personal insurance of personnel. Dt 76.1 Kt 51 - 10,000 rub. The accountant paid the insurance company the annual fee for the employee's insurance. Then, when receiving money from the insurance company upon the occurrence of an insured event, the Fastmil accountant will make a debit entry to account 51 in correspondence with account 76. And the accrual of insurance compensation to the employee will be reflected by entry Dt 76 Kt 73.

- The accounts payable to the counterparty has been repaid. A company can record settlements with suppliers both on account 62 and 76. In practice, accountants most often record on account 76 secondary counterparties, settlements with which occur infrequently.

- The supplier is paid for the claim or fine. In this case, mutual fines of 2 companies can be offset by posting Dt 76 Kt 76.

Example 2

I discovered that one of the archival shelves purchased from Bumazhny Dvor was deformed. And Bumazhny Dvor, in turn, filed a claim for the short supply of refrigerators.

According to the agreement between the parties, they are obliged to pay the counterparty a fine in the amount of 10,000 rubles. and remove the goods at your own expense. However, Bumazhny Dvor has the right to expect to receive monetary compensation from Fastmil for shortfalls in delivery. The fine is 5,000 rubles. The parties signed an act of mutual settlement for part of the mutual claims in the amount of 5,000 rubles.

In accounting it will be reflected as follows: Dt 76 Kt 76 - in the amount of 5,000 rubles. (mutual claims between are taken into account).

The paper yard accountant will make the following entries in accounting:

- Dt 76 Kt 76 - in the amount of 5,000 rubles. (part of the fine is offset against the due monetary compensation);

- Dt 76.2 Kt 51 - in the amount of 5,000 rubles. (a fine was paid for the supply of low-quality archival shelving).

Recognition of other income in accounting:

- Income related to the sale of own assets (with the exception of cash), interest payments to counterparties for the use of provided funds, participation in the authorized capital of third-party companies: income is accepted in the same way as revenue recognition. To do this, the following conditions must be met:

there is confirmation of the company’s right to receive this revenue (existence of an agreement);you can determine the full amount of revenue;

there is confidence that the company will receive economic benefits from this transaction: assets have been received as payment or there is confidence in their receipt in the future;

ownership of the sold products has been transferred to the buyer (the work has been completed and there is confirmation, for example, a document has been signed);

the costs associated with a given operation can be calculated.

- Fines and penalties, compensation for losses by third-party organizations for non-compliance with the terms of contracts: income is accepted in the period when there is a court decision to recover damages or the counterparty recognizes the need for compensation on its part.

- Write-off of expired accounts payable: in the reporting period in which the statute of limitations expired (usually 3 years from the date of the last joint reconciliation of counterparties’ results).

- Revaluation of the company's assets - in the period to which the date of the asset revaluation operation relates.

- Other receipts are accepted as they are received and identified.

Accounting receivables posting

Let's consider the main transactions for settlements with debtors and creditors, in which receivables arise:

| Business transaction | Wiring | |

| D | TO | |

| The supplier has received an advance payment | 60 | 51 (51) |

| Products have been shipped to the buyer | 62 | 90 (sub-account “Revenue”) |

| Sickness benefits accrued at the expense of the Social Insurance Fund | 69 | 70 |

| Employees were paid an advance | 70 | 50 (51) |

| The employee was given a sum of money to report | 71 | 50 (51) |

| A loan was issued to an employee | 73 | 50 (51) |

| The founder's debt to pay into the authorized capital | 75 | 80 |

| Interest accrued on the loan issued | 76 | 91 (sub-account “Other income”) |

Postings for writing off receivables must be distinguished from postings for repayment. Upon repayment, the debtor fulfills his obligation to repay the debt. And when the debt is written off, it is included in the financial result of the company. Thus, repayment by the counterparty of the debt on shipped products is reflected in the following posting:

D 51 (52) K62.

And, for example, writing off a debt on a loan issued to an employee (debt forgiveness):

D91 (subaccount “Other expenses”) K73.

When a doubtful debt for which a reserve was created is written off, the posting will be as follows:

D63 K62 (60).

Characteristic

As has already become clear, account 76 is used for settlement transactions with debtor and creditor counterparties, which are not subject to accounting in accounts 60-75. The special account 76 itself is active-passive, that is, on the reporting date plan it can have both a debit and a credit balance. If there is a debit balance, it means that the amount of liabilities has increased. If there was a balance on the loan, then the obligations were repaid. In this situation, the account is active and this opening balance based on debit and credit turnover also determines its ending balance.

Important! If the increase occurred in debit, then the balance is debit; if in credit, then the balance is credit. When there is a loan balance on the account, the register itself behaves as passive

Thus, the final balance is formed by the side of position 76 on which the increase was recorded. With a debit increase, the final balance is formed from the Dt of the account, and the credit balance - from the Kt.

Examples of accounting entries for account 76

The following transactions can be made with this account:

| Debit | Credit | Name |

| 76 | 20, 23, 29 | Write-off of part of the costs of main, auxiliary or servicing production to other debtors or creditors |

| 76 | 21 | Sales of our own semi-finished products |

| 76 | 28 | Write-off of losses from marriage |

| 76 | 41 | Returning defective goods to the supplier |

| 76 | 43 | Reflection of the debt of other debtors for shipped commercial products |

| 76 | 50 | Payment of accounts payable in cash from the cash register |

| 76 | 50 | Return of funds from the cash register to the buyer (other creditor) |

| 76 | 51, 52, 55 | Payment of accounts payable with money from a current account, foreign currency account or from special accounts |

| 76 | 60 | Accounts payable for other transactions are reflected |

| 76 | 68/VAT | Reflection of VAT debt |

| 76 | 70 | Unpaid wages have been deposited |

| 76 | 86 | Targeted funding received from the budget |

| 76 | 86 | Membership (entrance) fees have been charged to the partnership |

| 76 | 91 | Interest accrued on bonds |

| 76 | 08 | Writing off work that did not bring the desired result |

| 76 | 91/1 | Reflection of income from other sales |

| 76 | 91/2 | Write-off of receivables that are not collectible |

| 04 | 76 | The company's positive business reputation is reflected |

| 08 | 76 | Reflection of costs for exclusive copyright of a computer program |

| 10 | 76 | Materials purchased from another supplier |

| 15 | 76 | Reflection of costs for procurement of materials |

| 19 | 76 | Reflection of input VAT on work (services) of another creditor |

| 20 | 76 | Inclusion of costs for other operations in production costs |

| 23 | 76 | Inclusion of costs for other operations as part of costs for auxiliary production |

| 41 | 76 | Receipt of goods from other creditor |

| 44 | 76 | Inclusion of costs for other operations as part of sales expenses |

| 50 | 76 | Received payment from other debtor in cash to the cash desk |

| 51, 52, 55 | 76 | Payment received from another debtor to a current account, foreign currency account or special account |

| 57 | 76 | Reflection of a transfer that has not yet been received from another debtor |

| 58 | 76 | The purchase of shares and securities is reflected |

| 62 | 76 | Settlement of debt |

| 91/2 | 76 | Reflection of other expenses |

| 97 | 76 | Reflection of deferred expenses |

Write-off of accounts receivable in accounting and tax accounting

Important! If the mortgage period is 45-90 days, then it is included in the reserve in the amount of 50%. 100% of the debt is included in the reserve only if the debt period is more than 90 days.

Accounts receivable can be written off using created reserves for doubtful debts. This transaction is reflected in accounting with the following entries:

D63 K62(76) – accounts receivable are written off against the reserve.

An organization can use the created reserve only within the limits of its size. If the written-off debt exceeds the amount, the difference is taken into account as part of other expenses. This transaction will be reflected by the following posting:

D91-2 K62 (76) - write-off of accounts receivable that the reserve did not cover.

Important! Even if a receivable is written off, this does not mean that it is cancelled. The entire amount written off should be reflected in off-balance sheet account 007 “Debt of insolvent debtors written off at a loss.” This operation is formalized by the following posting: D007 – written off receivables are reflected.

In tax accounting, two methods are used to write off receivables:

- Write-off from the reserve for doubtful debts.

- Reflection of debt as part of non-operating income.

The amount of receivables that was not covered by the reserve is included in non-operating income. But only organizations that calculate income taxes using the accrual method can write off debt as expenses.

If you use the cash method, it will not be possible to take debts into account as expenses. If payment is not made, then the obligation is not considered fulfilled, and therefore expenses cannot be recognized. Uncollectible accounts receivable in full, including VAT, reduce taxable income.

Account 76: accounting for settlements with subsidiaries (dependent) companies

Organizations that have subsidiaries can make a variety of settlements with them. However, do not forget: a subsidiary and a dependent company are not the same thing.

Simply put, subsidiaries include those economic entities where the main enterprise has more than 50% of the shares (authorized capital), and dependent ones are those in which the main enterprise owns 20% or more of the shares (authorized capital).

Let's consider the entries used when accounting for settlements of an enterprise with subsidiaries and dependent companies (for this, a subaccount 76.5 can be opened to account 76):

- Dt 08 (10, 41...) Kt 76.5 - the enterprise acquired fixed assets, materials, goods from a subsidiary;

- Dt 76.5 Kt 90, 91.1 - the enterprise sold property to a subsidiary;

- Dt 91.2 Kt 76.5 - the enterprise included the losses of the subsidiary, which it is obliged to repay, into other expenses;

- Dt 76.5 Kt 51 - the enterprise transferred funds to repay the losses of the subsidiary.

A significant part of business transactions between the main enterprise and a subsidiary (dependent) company is reflected by correspondence using not only account 76, but also account 58.

Example 1

Payment of a share in the authorized capital of a subsidiary by transfer of property.

To begin with, the main enterprise, on account 76, registers the formation of a payable debt corresponding to the amount of debt for a contribution to the authorized capital of a third-party organization: Dt 58 Kt 76.5.

Repayment of this debt can be made by different types of property:

- If these are funds, their transfer in favor of a subsidiary is shown by posting Dt 76.5 Kt 51.

- If this is an item of fixed assets (FPE) that was in operation, then the postings will be as follows: Dt 58 Kt 76.5 - reflects the cost of the transferred property, previously agreed upon by the parties;

- Dt 02 Kt 01 - reflects the write-off of accrued depreciation from the moment of commissioning of an asset until the moment of its disposal;

- Dt 76.5 Kt 01 - reflects the write-off of the residual value of the fixed asset.

If the residual value of the fixed assets is lower than that agreed upon by the parties in order to repay the debt on the contribution to the authorized capital, then the enterprise records other income: Dt 76.5 Kt 91.1. If higher - other consumption: Dt 91.2 Kt 76.5.

- If intangible assets (intangible assets) are transferred to the authorized capital, then the correspondence is applied: Dt 58 Kt 76.5 - accounts payable are reflected in the agreed value of the transferred intangible assets;

- Dt 05 Kt 04 - reflects the write-off of depreciation on assets accrued at the time of their alienation;

- Dt 76.5 Kt 04 - reflects the write-off of the residual value of intangible assets.

If the residual value of the intangible asset is less than the agreed value, other income is recorded: Dt 76.5 Kt 91.1. And if more - other expenses: Dt 91.2 Kt 76.5.

- If materials are transferred to the authorized capital, then the correspondence will be as follows: Dt 58 Kt 76.5 - accounts payable have arisen in the amount of the agreed cost of materials;

- Dt 76.5 Kt 10 - reflects the write-off of the actual cost of materials.

If the actual cost turns out to be lower than the agreed value, other income is recorded: Dt 76.5 Kt 91.1 If more, other expenses: Dt 91.2 Kt 76.5.

Example 2

The company acquired shares, but has not yet paid for them.

The fact of transfer of ownership of shares to an enterprise, if it has not paid for them by the time of such transfer, is reflected by posting Dt 58 Kt 76.5.

Example 3

The enterprise has made an advance payment for shares to which it will become entitled later:

- Dt 76.5 Kt 51 - reflects the amount paid for the shares;

- Dt 58 Kt 76.5 - the right to the shares transferred to the enterprise, the shares were registered.

Example 4

The company resells previously purchased shares to the public:

- Dt 76.5 Kt 91.1 - other income received from the sale of shares;

- Dt 91.2 Kt 58 - the cost of shares sold is written off;

- Dt 51 Kt 76.5 - payment received for shares sold.

Accounts receivable

In order to see and understand what accounts receivable is, you should create a balance sheet. The debit balance on settlement accounts (such as 60, 62, 66-70, 73, 75 and 76) will be the receivable, that is, the amount owed to the company by other firms, individuals and funds.

Let's look at what accounts receivable includes:

| Accounts receivable | On what account is it reflected? |

| Debts of buyers, customers | 62 “Settlements with buyers and customers” |

| Debts of suppliers and contractors for advances transferred to them (prepayments), as well as recognized claims | 60 “Settlements with suppliers and contractors” 76 “Settlements with various debtors and creditors” |

| Debts of insurance companies for insurance claims, issuers of securities owned by the company, for dividends, etc. | 76 “Settlements with various debtors and creditors” |

| Debts of budgetary bodies and extra-budgetary funds for excessively transferred taxes and contributions | 68 “Calculations for taxes and fees” 69 “Calculations for social insurance” |

| Debts of employees on accountable amounts, loans, compensation for damage, etc. | 70 “Settlements with personnel for wages” 71 “Settlements with accountable persons” 73 “Settlements with personnel for other operations” |

| Debts of founders and participants on contributions to the authorized capital | 75 “Settlements with founders” |

The composition of accounts receivable will depend on how exactly it was formed. It can form when:

- sale of goods (work or services) on an advance payment basis (that is, the goods have already been shipped to the counterparty, but payment for it has not yet been received);

- purchasing products (raw materials) on an advance payment basis;

- overpayment of taxes and fees;

- issuance of accountable money.

Existing types of payments

So, when opening a bank deposit, a bank account agreement is signed between the company and the credit institution, according to which the latter undertakes to accept and accept financial resources received in the name of the client, carry out the instructions of the account owner to write off monetary resources from the account or issue them, as well as perform other operations according to the account. The bank receives a commission for cash and settlement services to clients.

Depending on the payment procedure chosen between the counterparties for a particular transaction, cash and non-cash payments are distinguished. In the first case, financial resources are used in kind, i.e. in the form of banknotes. As for non-cash payments, they are made through accounts opened with a credit institution.

If we talk about citizens of the Russian Federation, then this category has no restrictions in choosing the procedure for making payments. But with legal entities and individual entrepreneurs the situation is somewhat different. Thus, in accordance with current legislation, in each transaction carried out, the limit for settlements using cash today is 60.0 thousand rubles.

The Civil Code of the Russian Federation and other regulatory and legal acts regulating banking activities allow the use of four key forms of non-cash payments:

- settlements using payment orders, when, on the instructions of the account owner, funds within the balance on it are transferred in favor of a counterparty who can be serviced by the same or another financial and credit institution;

- letter of credit form of payment;

- collection form;

- payments by checks.

Taxation of intra-business expenses

The calculations under consideration assume tax accounting.

VAT

VAT for VR is determined on the basis of Articles 166 and 174 of the Tax Code of the Russian Federation. Journals of invoices, purchases and sales books must be maintained by structural branches. They are single magazines.

This order of relations between the isolated and the central subject is recommended:

- During the period, each branch accrues VAT. Entities can use deductions based on calculations recorded on the autonomous balance sheet.

- At the end of the period, the total turnover of VAT and deductions is sent to the balance sheet of the central office. The current sections of the purchase and sales books are also transferred there. An alternative option is the formation of a cumulative balance for tax payments.

- The central office is engaged in the formation of a set of information, and also creates and submits a VAT return.

- The central office also transfers the tax to the budget.

- The head office can carry out settlements with separate entities regarding the amounts of taxes on transactions included in the accounting.

The implementation of the latter option is possible only if the corresponding procedure is enshrined in local acts.

Income tax

Income tax is determined and paid to the company's address on the basis of paragraph 1 of Article 288 of the Tax Code of the Russian Federation. If a company’s division is located in another region, it needs to independently pay tax to the budget of the subject of the country. As part of this operation, the amount of tax is determined in a special manner. In particular, the amount of tax will not be established by calculating the amounts of all transactions carried out by the unit. When making calculations, you need to be guided by the share of fixed assets and the number of employees divided by labor costs.

If the company reflects stable/deferred assets and liabilities on the balance sheets of separate entities, it is recommended to send the total amounts of turnover in account 68 to the central office.

The determination of the current tax is carried out by the central office in any form of interaction. If net profit is generated by separate entities that are on a separate balance sheet, a tax adjustment is made. It is executed based on indicators received by the central office.

ATTENTION! Stable/temporary differences and associated obligations are established by each separate entity

IMPORTANT! The central office is responsible for dividing tax amounts between separate branches

IMPORTANT! The central office is responsible for dividing tax amounts between separate branches

Economics and finance news from St. Petersburg, Russia and the world

An assignment agreement is an agreement under which the original creditor (assignor) transfers the right to claim receivables to a new creditor (assignee).

The transaction must be compensated, so the value of the debt in the contract is usually lower than the amount of the transferred debt.

In the accounting records of the assignor, transactions for the creation and sale of receivables are reflected in the accounting accounts in the following order:

Dt62 - Kt90-1 - goods were sold, receivables arose;

Dt90-3 - Kt68 subaccount "VAT Calculations" - VAT is charged on proceeds from the sale of goods; Dt90-2 - Kt41 - the cost of purchased goods is written off; Dt90-9 - Kt99 - profit from the sale of goods is reflected; We assign the right to claim receivables:

Dt76 - Kt91-1 - assignment of the right of claim is reflected;

Dt91-2 - Kt62 - the buyer's receivables are written off; Dt99 - Kt91-9 - the loss from the sale of receivables is reflected; Dt51 - Kt76 - funds were received from the assignee. In the accounting records of the assignee, transactions for the acquisition of receivables are reflected as follows:

Dt58 subaccount “Assignment of claims” - Kt60 (76) - reflects the amount for which the receivables were purchased;

Dt58 subaccount “Assignment of claims” - Kt60 (76) - reflects the costs associated with the acquisition of receivables (for example, legal services); Dt60 (76) - Kt51 - reflects the amount of payment to the original creditor (assignor) and the organization for the provision of services; Dt51 - Kt91-1 - reflects the repayment of debt by the debtor; Dt91-2 - Kt58 subaccount “Assignment of rights of claim” - reflects the write-off of the original cost of receivables. The VAT base is the difference between the income received and the costs of acquiring receivables. VAT is determined at the rate of 18/118. The following entries are made for the amount of accrued VAT:

Dt91-2 - Kt68 subaccount “Calculations for VAT” - reflects the accrual of VAT on the difference between the income and expenses of the assignee;

Dt91-9 - Kt99 - income from the transaction is included in profit. VAT. The assignor does not have VAT obligations when selling receivables to a third party (clause 1 of Article 155 of the Tax Code of the Russian Federation). For the assignee it is somewhat more complicated. If a new creditor exercises the right of claim to a third party or if the debtor repays an obligation, the VAT base is determined in accordance with clause 2 of Art. 155 of the Tax Code of the Russian Federation, as the amount of excess income received by the new creditor upon subsequent assignment of the claim or repayment of the obligation over the costs of its acquisition. Accordingly, if the obligation is not repaid by the debtor, no VAT base arises. The specifics of determining the tax base for income tax upon assignment (assignment) of the right of claim are prescribed in Art. 279 Tax Code of the Russian Federation. In particular, if the creditor assigns the right to claim the debt before the payment deadline under the agreement, then the resulting loss will reduce his income tax base. The amount of loss should not exceed the amount of interest that the assignor would have paid taking into account the requirements of Art. 269 of the Tax Code of the Russian Federation for a debt obligation equal to income from the assignment of the right of claim, for the period from the date of assignment until the moment of repayment of the debt (clause 1 of Article 279 of the Tax Code of the Russian Federation). So, the maximum amount of interest that the organization could take into account in expenses if it took out a loan is calculated, in the amount of proceeds from the assignment of the claim. The result obtained is compared with the amount of loss from the assignment. The amount that turns out to be less can be recognized as an expense for profit tax purposes. And if the assignment of the right to claim receivables occurs after the due date for payment, then the negative difference between the income from the sale of the debt and the cost of the goods (works, services) sold will be recognized as a loss, but it will not be included in expenses for the purpose of calculating income tax at a time. At the time of assignment of rights, 50% of the amount of loss is taken into account in expenses; after 45 calendar days from the date of sale of the debt, taxable profit will be reduced by the remaining 50% of the amount of loss. The new creditor (assignee) has the right to reduce income from the acquisition of receivables by the price of these property rights and for the amount of expenses associated with their acquisition and sale (subclause 2.1, clause 1, article 268 of the Tax Code of the Russian Federation).

Select the fragment with the error text and press Ctrl+Enter

We discuss the news here. Join us!

What subaccounts are used?

The following sub-accounts can be opened for account 76:

- 76.1 Personal and property insurance - accounting of insurance transactions here occurs only in relation to the listed types of insurance; other accounts are used for compulsory pension, medical, social insurance. This subaccount is used both to record insurance premiums and to collect information on insurance claims. Transactions on life and health insurance of company employees are also recorded here. Analytics is carried out by type of insurance and insurers.

- 76.02 Claims - this sub-account summarizes information about emerging claims regarding the quality of the goods supplied, claims for violation of the terms of concluded contracts in relation to timing, volume, etc. Accrued fines and penalties provided for in agreements are taken into account here. Analytics is carried out on debtors and submitted claims.

- 76.3 Dividends - here is a generalization of information about accrued income due to the organization as a founder, as well as their payments. Analytics is carried out for each source of such income. See step-by-step instructions: how to pay dividends to the founder.

- 76.4 Deposited salary - is intended to account for wages not received on time, which are sent by the enterprise to the current account marked “Deposited”. Analytics is carried out on employees who did not receive their salaries on time.

- Calculations based on writs of execution - designed to summarize information on deductions made by an employee based on documents received from bailiffs - alimony, other deductions, etc. Analytics is carried out on debtor employees and received writs of execution.

- Settlements with other buyers and customers - this account records transactions that are not included in the main activities of the company. For example, payment of duties, settlements with a notary, etc. may be reflected here.

Depending on the specifics of conducting transactions, on account 76, in addition to the main sub-accounts recommended by the standard Chart of Accounts, similar ones can be opened, but for accounting for transactions in foreign currency.

For example, 76/6 - Settlements with other buyers and customers in rubles and 76/26 - Settlements with other buyers and customers in foreign currency.

Attention! If the list of subaccounts to be opened differs from the standard one, then it must be indicated in the adopted accounting policy of the organization

Accounts receivable: accounting accounts

In accordance with Section VI “Calculations” of the Chart of Accounts and the Instructions for its application (Order of the Ministry of Finance dated October 31, 2000 No. 94n), synthetic and analytical accounting of the organization’s receivables is maintained on the following accounts:

- 60 “Settlements with suppliers and contractors”;

- 62 “Settlements with buyers and customers”;

- 68 “Calculations for taxes and fees”;

- 69 “Calculations for social insurance and security”;

- 70 “Settlements with personnel for wages”;

- 71 “Settlements with accountable persons”;

- 73 “Settlements with personnel for other operations”;

- 75 “Settlements with founders”;

- 76 “Settlements with various debtors and creditors”;

The above accounts are active-passive, i.e., allowing for the presence of both debit and credit balances. Accordingly, accounts receivable means the formation of a debit balance on settlement accounts.

Application of account 76: shared construction agreements

Another area of application of account 76 is legal relations in the field of shared construction contracts. Let's look at the entries in the developer's accounting, compiled using escrow accounts - according to the new payment scheme between the investor and the developer, mandatory for use after 07/01/2019:

- Dt 009 subaccount “Funds of shareholders in escrow accounts” - the shareholder transferred funds to the escrow account;

- Dt 51 Kt 67 - the bank issued a targeted loan for the construction of a real estate property;

- Dt 91.2 Kt 67 - interest was accrued for using the loan;

- Dt 20 Kt 60 - the cost of work carried out by the contractor is included in construction costs;

- Dt 43 Kt 20 - reflects the book value of the property;

- Dt 76 “Settlements with shareholders” Kt 43 - the apartment was transferred to the investor after the property was put into operation;

- Dt 76 “Settlements with equity holders” Kt 90 - revenue from the sale of housing is recorded;

- Dt 67 Kt 76 “Settlements with shareholders” - funds from shareholders credited to the escrow account are used to repay the loan and interest;

- Dt 51 Kt 76 “Settlements with shareholders” - the balance of funds of shareholders was received from escrow accounts after repayment of the loan and interest;

- KT 009 “Funds of equity holders in escrow accounts” - completion of settlements through an escrow account.

Tags: asset, balance sheet, accountant, currency, capital, loan, tax, order, expense, write-off