In the process of producing goods and services and performing work, the generation of waste is inevitable. Their composition is determined by the type of activity of the company. The rules for handling industrial waste are determined by Federal Law-89 dated June 24, 1998. Industrial waste is goods and materials obtained during the processing of initial raw materials, which have lost their consumer properties and are no longer suitable for their intended use. One of the stages of handling them is recycling.

When is it necessary to conclude an agreement for the management of MSW ?

Legislative regulation

The main provisions and responsibilities for waste management are contained in Federal Law-89. Responsibility for waste disposal lies with the original owner, the organization where it was generated.

Production waste is divided into irrecoverable and returnable. The first are materials with completely lost original useful properties. Their implementation or reuse is not possible. The latter can be used in production or sold for further use.

Is there a list of goods, packaging of goods that are subject to disposal after they lose their consumer properties?

Irrevocable waste is not reflected separately in the balance sheet. These are production (technological) losses, the standard of which is included in the consumption rates of raw materials when calculating the cost of the finished product: shrinkage, volatilization, waste, evaporation. According to the “Basic provisions for calculating the cost of products” clause 27 (approved 20/07/70, valid document), irrecoverable waste is not subject to assessment. This means that the accountant does not need to determine their value and create postings. We can say that indirectly their disposal is paid for by the company itself through the mechanism for calculating production costs. All that is required is their technological accounting.

Returnable waste can be disposed of directly. Federal Law 89 defines waste disposal as its use in the production of products, services, and work. At the same time, for accounting purposes, residues of materials that have retained all their consumer properties and are transferred to other departments and workshops are not recognized as waste (Article 254-6 of the Tax Code of the Russian Federation).

What are the standards for recycling waste from the use of goods?

Accounting data in the field of waste management - comments on completion

In fact, keeping a waste log is not difficult at all. The difficulty lies in the accounting process as it is formed, processed, disposed of, transferred, disposed of…. In fact, in large enterprises this is a huge job. Need to remember:

- Accounting must be compiled no later than January 25.

- The waste log is kept in tons - waste of hazard classes 1, 2,3 must be shown with an accuracy of three decimal places, waste of hazard classes 4 and 5 with an accuracy of 1 decimal place;

- if the generation of a specific waste did not occur within the specified period, “0” is entered in the line, the name of the waste must be written;

- waste is summarized by hazard class and in general;

- accounting is kept for the enterprise as a whole, and for objects of negative impact on the environment.

Remember that accounting in the field of waste management for supervisory authorities is very often the evidentiary basis for describing a violation.

Accounting data should overlap with other enterprise reports in the field of waste management.

During supervisory activities, they have the right to request accounting data from you for the last 5 years!

If supervision, during an inspection of the territory of the enterprise, discovered and recorded the fact of waste generation, but this waste is not included in the accounting data, this constitutes a violation.

If your accounting data contains waste of hazard class 1-4, but you cannot provide a waste passport, this will also be a violation.

If you are an enterprise of category II NVOS, you calculate waste generation standards and limits on their disposal based on accounting data.

If accounting data shows that you have accumulated waste for more than 11 months, this will also be a violation. Transfer waste in a timely manner!

If during the inspection you provided a certificate of completion of work for the transfer of waste, but the generation of this waste was not recorded in the accounting data, then this is a violation.

In fact, this is the easiest way to attract registration, since officials often fill it out inattentively and do not take into account all the nuances.

Disposal procedure

The owner can go two ways.

- Entrust removal and further disposal to a specialized company. To do this, you will need accounting data on waste volumes recorded in documents. Hazardous waste (Article 4.1 of Federal Law-89) requires a disposal license.

- Independently take into account waste and make decisions about its disposal, for example, about transferring waste to production.

IMPORTANT! A sample agreement on industrial waste disposal from ConsultantPlus is available here

In order to have grounds for reflecting recycling in accounting and accounting records, it is necessary to create an internal waste write-off commission. It includes technical specialists, economic service employees, and the manager. The commission determines the inventory items to be disposed of. The decision of the commission is formalized in an act.

Accounting

Due to the variety of types of waste and methods of their disposal, various posting and accounting schemes can be used. Let us dwell on the most significant aspects of waste management by the original owner and by a company working in the field of recycling.

From the owner

Control over the movement of returnable waste and its disposal begins with the owner building detailed analytical records: by type of product, location of waste generation, information on its qualitative and quantitative composition. To calculate the generated waste, actual measurements, weighings are used, or a calculation method is used according to standards per unit of production.

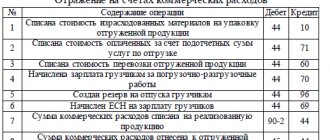

When recycling by selling returnable waste externally, the following transactions can be generated:

- Dt 10/6 Kt 20, 23 – waste was capitalized from production;

- Dt 62 Kt 91/1 – revenue from the sale of returnable waste is recorded;

- Dt 91/VAT Kt 68/VAT – tax is charged on revenue;

- Dt 91/2 Kt 10/6 – written off from the cost of returnable waste;

- Dt 51 Kt 62 – payment received;

- Dt 90/9 Kt 99 – profit was received from the sale of returnable waste.

The owner can dispose of waste by transferring it to production within his organization. For this purpose, the reverse wiring to that given above is used: Dt 20.23 Kt 10/6 - transfer of waste to production.

In a specialized company

Disposal costs here relate to ordinary activities in accordance with PBU 10/99. Expenses are recognized in the accounting system in accordance with clause 18 of the specified document, depending on whether the cash method of income recognition is used or not.

If returnable waste is purchased for use in your own production, count 10 applies.

Postings:

- Dt 10 Kt 60, 76 – secondary raw materials from the supplier were capitalized;

- Dt 60, 76 Kt 50, 51 – payment to the supplier for secondary raw materials.

If the acquisition was made for further resale, the raw materials act as goods (41).

Let the organization use a common BUT system. The implementation transactions will be as follows:

- Dt 62 Kt 90/1 – sales revenue;

- Dt 90/VAT Kt 68/VAT – VAT is charged on sales;

- Dt 90/2 Kt 41 – written off from the cost of waste sold;

- Dt 51 Kt 62 – money received for sold raw materials;

- Dt 90/9 Kt 99 – profit from the resale of raw materials.

There are often cases when a company enters into an agreement with an organization or a network of retail outlets for the free transfer of waste and garbage, for example, used paper and wooden containers for the purpose of recycling on its own. The terms of the agreement may provide for payment by counterparties. In such cases, the key account will be 98/2 - “deferred income, gratuitous receipts.”

Postings:

- Dt 10, 15 Kt 98/2 – free receipt of goods and materials, in market (contractual) valuation;

- Dt 20, 23 Kt 10 – raw materials sent for processing;

- Dt 98/2 Kt 91/1 – non-operating income from gratuitous receipt of goods and materials;

- Dt 76 Kt 90/1, 91/1 – processing services, revenue from sales (work) is reflected;

- Dt 90/VAT, 91/VAT Kt 68/VAT – charge of VAT on processing services;

- Dt 50, 51 Kt 76 – payment for processing services;

- Dt 40, 43 Kt 20, 23 – production of finished products, the result of waste disposal.

Disposal can be documented with the following primary documents:

- act of acceptance and transfer;

- invoice for the release of materials to the third party;

- packing list;

- processing report;

- certificate of completion;

- demand-invoice;

- limit fence card.

When recycling waste with the help of a specialized company, an agreement is concluded (on disposal, on waste processing).

By the way! When processing customer-supplied raw materials, the customer is the owner of the generated waste. Returnable waste either reduces the cost of the original raw materials transferred for processing, or reduces the cost of the processor's services.

The procedure for accounting waste by department

The accounting system assumes a division of responsibility. Accordingly, different divisions of one organization may be responsible for maintaining tax, statistical and accounting records. All types of waste generated at the enterprise are subject to primary accounting.

The responsible person is required to keep a “Record Book”. It is filled out monthly, indicating data for each type of waste separately. Every quarter, the department must provide a journal report, this report includes the movement of waste and the movement of funds received from the sale or use of waste. The person in charge must have a special job description that spells out the rules for handling the magazine and the rules for filling it out. Disposal or write-off is also reflected in the documentation.

For each type of waste from hazard class 1 to 4, it is necessary to create an Industrial Waste Passport. Instructions for working with waste subject to removal state that they are subject to registration in the economic area, but only if they are planned to be moved to a city landfill.

Tax accounting

The above correspondence accounts show: waste disposal operations associated with their sale and processing are subject to VAT. The object of value added tax is any sale, i.e. transfer of ownership rights of both a paid and gratuitous nature (Article 146-1(1), 39-1 of the Tax Code of the Russian Federation). In particular, waste treatment services are equal to revenue from the sale of work. In a situation where the supplier transfers returnable waste to the work contractor free of charge, this operation is recognized as subject to VAT, as is the sale by reducing the cost of services by the cost of the waste. VAT is required to be charged on these transactions.

Starting from this year, operations for the disposal of scrap metal and waste paper are subject to VAT (FZ-424 dated November 27, 2018). The tax agent here will not be the seller, but the buyer, i.e. third party organization, specialized processing company. The seller must have the status of a VAT payer, and the buyer, a tax agent, can apply both the general regime and the “simplified” regime, and other special regimes - he is still obliged to calculate and transfer tax to the budget. Agency responsibilities are also assigned to those buyers who are exempt from VAT (Article 145 of the Tax Code of the Russian Federation). The seller will be obliged to charge tax only if he sells waste to an individual or has not specified VAT in the agreement with the waste buyer, being its payer.

For NU purposes, returnable waste must be included in income tax calculations:

- are valued at market prices (possible sale prices) upon disposal through sale;

- at a reduced price, compared to the original inventory items, if they are disposed of by transferring them into production.

In the latter case, it is taken into account that the product yield will be underestimated, and the consumption of secondary raw materials will be higher than the usual norm (according to Article 254-6, 40 of the Tax Code of the Russian Federation, letter No. 03-03-06/4/49 of the Ministry of Finance dated 04/26/10 . and etc).

For the taxpayer, this first of all means the opportunity to reduce income tax costs by the market value of secondary waste.

Free receipt of waste is non-operating income. It must be recognized when waste is written off for processing.

Briefly

Accounting for waste disposal, both accounting and tax, is associated with the choice of disposal method: waste is disposed of on site or transferred externally. Transfer to a third party may be paid or gratuitous. In accounting, standard accounts and postings are used for accounting purposes for the sale of products and the transfer of inventory and materials into production.

When transferring to a third party free of charge, the score is 98/2. In NU, all operations related to the sale of waste, including free of charge, are subject to VAT. From this year, VAT is also levied on the disposal of waste paper and scrap metal. The tax agent is not the seller, but the buyer.

For the purpose of accounting for income tax, waste and operations with it are assessed according to the rules of Art. 254 Tax Code of the Russian Federation.

The accounting procedure in the field of waste management

Individual entrepreneurs and legal entities operating in the field of waste management are required to maintain, in accordance with the established procedure, records of waste generated, disposed of, neutralized, transferred to other persons or received from other persons, as well as disposed waste. The accounting procedure in the field of waste management is established by federal executive authorities in the field of waste management in accordance with their competence; the procedure for statistical accounting in the field of waste management is a federal executive body that carries out the functions of generating official statistical information on social, economic, demographic, environmental and other social processes in the Russian Federation.

paragraph 1 of Article 19 of the Federal Law of June 24, 1998 No. 89-FZ “On Production and Consumption Waste”

Main nuances:

- Absolutely all generated waste must be accounted for;

- Waste accounting must be maintained by all legal entities and individual entrepreneurs that generate waste. And waste is generated by all legal entities and individual entrepreneurs... I remind you about fines for lack of accounting data;

- There is no waste log for the following types of waste: radioactive waste, biological waste, medical waste,

- the waste log does not take into account emissions of harmful substances into the atmosphere (not to be confused with captured dust from cyclones (GOU), discharges of harmful substances in wastewater into water bodies, substances that destroy the ozone layer (exception: substances that are part of products that have lost consumer properties).

- for objects of categories 1-4 - records are kept for each object + additionally for legal entities or individual entrepreneurs as a whole;

- for an uncategorized object - records are kept as a whole for legal entities or individual entrepreneurs;

- accounting is carried out based on the actual amount of generation and further waste management. In the absence of means to measure the actual amount of education, etc. waste, it is possible to carry out accounting by the calculation method, which uses information from technical (technological) documentation, data from working hours, accounting, waste generation standards, the capacity of waste accumulation sites, the capacity of waste management facilities and other data.

waste accounting is carried out as it is generated, processed, disposed of, neutralized, transferred to other persons or received from other persons, and waste is disposed of (note in the form of plates - a summary is written based on the results of the quarter and year) . Accounting data based on the results of the quarter and calendar year (as of 01/01) is summarized, no later than January 25.

- Waste accounting can be maintained both electronically and on paper.

- It is allowed to round off the amount of waste: for waste of hazard classes 4 and 5 - up to 0.0 t; for waste of hazard classes 1,2,3 - 0.000 t.

The results of waste accounting are the basis for:

- calculating waste generation standards and limits on their disposal;

- report on the organization and results of industrial environmental control;

- report 2-TP (waste);

- calculating fees for negative impacts on the OS.

Waste accounting should include accounting for waste generated, including waste accumulation sites, at capital construction sites where processing, disposal, and neutralization of waste are carried out, at waste disposal sites transferred to other persons or received from other persons.

Order of the Russian Ministry of Natural Resources No. 1028 dated December 8, 2020 describes the procedure for organizing the accounting of generated waste; in essence, this is a waste inventory.

identification of substances and materials that were formed during the production of products, performance of work, provision of services, including gas purification, wastewater and recycled water treatment, cleaning of equipment, territory, and pollution elimination.

identification of products that have lost their consumer properties when used for the production of products, performance of work, and provision of services.

assignment of waste to a specific hazard class (in accordance with the FKKO, if there is no waste in the FKKO - in accordance with Order of the Ministry of Natural Resources and Ecology of the Russian Federation dated December 4, 2014 N 536 “On approval of the Criteria for classifying waste into IV hazard classes according to the degree of negative impact on the environment."

- waste certification.

As a result, the composition of generated waste is identified, which is subject to accounting, which should contain information:

- on the name of the waste,

- FKKO code,

- waste hazard class,

- origin and conditions of formation of the waste type,

- state of aggregation and physical form of waste,

- chemical and (or) component composition of the waste.

Recommended table:

Composition of generated waste types subject to accounting:

In columns 2 and 3, additionally, for each type of waste, the details of the letter sent to the RPN to confirm the classification of waste types into a specific environmental hazard class are indicated.

Column 5 indicates belonging to a specific production or technological process.

Column 6 is filled out on the basis of the appendix to the Procedure for maintaining the state waste cadastre, approved by Order of the Ministry of Natural Resources of Russia dated September 30, 2011 No. 792 On approval of the procedure for maintaining the waste cadastre.”

Column 7 is filled out on the basis of information contained in technological regulations, technical conditions, standards, and design documentation. In the absence of information in the specified documentation, based on the results of quantitative chemical analyses. Both methods can be used.