December salary payment deadline: options

Employers can choose different options for paying the second part of their December 2021 earnings. So, let’s say, you can pay the second part of your salary ahead of schedule - in December 2021. However, this payment may take place in January 2021. The solution to this issue depends, among other things:

- on the content of employment contracts and internal labor regulations regarding the timing of salary payments;

- from the employer’s desire to pay wages for December 2021 ahead of schedule.

Please note that December 31, 2021 is Sunday, which is a day off in a five-day work week. After this weekend, the New Year holidays will begin. The first working day in 2018 is January 9 (Tuesday). Also see “Salary payment deadlines for December 2021“.

Deadline for personal income tax payment in 2021 for legal entities

The employer company must comply with the deadlines for paying personal income tax in 2021. Otherwise, you may face fines. This article will describe in detail when it is necessary to submit personal income tax reports, as well as transfer this personal income tax in 2021.

What are the deadlines for paying personal income tax on wages in 2017?

It is worth noting that in 2021. the new rule came into force. According to it, personal income tax must be paid no later than the day following the day the income is paid. Now it has become unimportant exactly how the money is transferred (to the employee’s separate account/from the cash register/other methods), what is important here is the fact of payment of wages, that is, remuneration. Additionally, you need to know that personal income tax should be paid no later than the next day of final payment for the month. There is no need to pay personal income tax while retaining the advance. All of the above is given below as a clear example.

Thus, I made payments to employees on March 20, 2017. advance payment for March in the amount of 200,000 rubles. Next 04/05/2017 The final payment for April was made in the amount of 300,000 rubles. The accountant withheld personal income tax and paid it on April 6, 2017. in full from the entire amount for the month of March. Thus, the amount of personal income tax for March was 65,000 rubles ((200,000 + 300,000) X 13%). This amount was paid on 04/06/2017.

If money to pay wages is withdrawn in cash from a bank, then personal income tax must be withheld on the day when employees actually receive the payment. It is necessary to transfer the tax to the budget no later than the next day after the transfer of money. It turns out that there is no need to pay personal income tax on deposited wages (those that were not received on time).

If personal income tax was not withheld from the employee’s income and was not paid on time, then sanctions will be imposed (according to Article No. 123 of the Tax Code of the Russian Federation, sanctions are set at 20% of the amount of tax that is subject to withholding/transfer).

In addition, if the tax payment has not been made, for each day of delay the tax authorities charge a penalty on the basis of Article No. 75 of the Tax Code of the Russian Federation. The table below shows the rules for paying personal income tax on wages, as well as other types of payments.

Personal Income Tax (Personal Income Tax, Income Tax)

- 02/08/2017 Violation by the taxpayer’s counterparty of its tax obligations does not in itself constitute evidence that the taxpayer received an unjustified tax benefit. A tax benefit may be considered unjustified if the tax authority proves that the taxpayer should have been aware of violations committed by the counterparty, in particular, due to the relationship of interdependence or affiliate of the taxpayer with the counterparty.

- 08/22/2016 The courts came to a reasonable conclusion that the tax authority lawfully determined the date of actual receipt of income by individuals and the obligation of the Enterprise to transfer personal income tax to the budget as the day of payment of income to the taxpayer and the date of actual receipt of income (amounts subject to tax on income of individuals), and from which the Enterprise withheld this personal income tax (not including advances). B obliged

- 08/01/2016 The court, taking into account the conclusions set out above regarding personal income tax (in terms of revenue), as well as the fact that when a taxpayer is transferred to another taxation system retrospectively based on the results of a tax audit, all documents confirming the right to deduct VAT are subject to accounting, regardless from the fact that these deductions were not declared in the prescribed manner, recognized the entrepreneur’s calculation of tax obligations for VAT, set out in the statement of claim, as justified

What the Labor Code says about wages for December

If the deadline for paying wages for the second half of December is set from January 1 to January 8, 2021, then the employer is obliged to pay employees for December no later than December 29 (Part 8 of Article 136 of the Labor Code of the Russian Federation). It is simply impossible to issue salaries in January 2021 in such a situation, so as not to violate the requirements of the Labor Code of the Russian Federation.

Note that before paying wages, the employer must first close the time sheet and only then calculate wages. This logic follows from Part 4 of Article 91 of the Labor Code of the Russian Federation. If so, then it would be correct to accrue December salaries only in January 2021.

But, as we have already said, employees may need to pay wages in advance, since the payment deadline falls on weekends and holidays (Part 8 of Article 136 of the Labor Code of the Russian Federation). If you pay the second part of the salary for December later, the employer faces an administrative fine of up to 50,000 rubles. (Part 6 of Article 5.27 of the Code of Administrative Offenses of the Russian Federation). Thus, there is some uncertainty in labor legislation. On the one hand, you need to wait until the end of the month and close the timesheet, and on the other hand, you need to make the payment before the end of the month.

In our opinion, if the payment deadline falls from January 1 to January 8, 2021, then the salary for December 2017 must be calculated and paid in December. Moreover, you don’t need to wait until December 29, 2021. Of course, it is possible that in the last days of December workers may get sick or even miss work. And then an overpayment occurs. However, accruing and paying wages before the end of December will be better than being subject to the above-mentioned administrative fine of 50,000 rubles. Moreover, for late payment, the employer may be required to pay monetary compensation to the employees.

We also note that, at the initiative of the employer, it is possible to pay wages for December 2021 ahead of schedule. However, in this case, it will be necessary to issue an order for early payment and familiarize employees with it. See “Order on early payment of salaries for December 2021.”

The legislative framework

First of all, it is necessary to understand that personal income tax is directly related to those who, in fact, are this person. But at the same time, knowledge of the legislative framework, which is directly related to these taxes, may be necessary for other categories of taxpayers.

The procedure for calculating and paying personal income tax should be well known and understood by legal entities, since they are tax agents. First of all, this is due to the fact that they are the ones who are engaged in withholding taxes from individuals who are paid monthly wages.

According to Article 232 of the Tax Code of the Russian Federation . tax agents must provide certain information to the Federal Tax Service, namely:

- the amount of personal income tax that was not only accrued, but also withheld, and also transferred to the budget for a certain tax period;

- about the profit of an individual within the expired period.

It is also worth noting that, according to the Tax Code, the deadline for paying personal income tax is limited to April 1 of the year following the reporting year.

If payment deadlines are delayed, the employer bears administrative responsibility.

When the Tax Code of the Russian Federation requires withholding personal income tax

The Tax Code of the Russian Federation provides that the tax agent (employer) is obliged to:

- calculate personal income tax on the date of receipt of income (clause 3 of article 226 of the Tax Code of the Russian Federation);

- withhold on the day of payment of income (clause 4 of article 226 of the Tax Code of the Russian Federation).

It turns out that the date of receipt of income in the form of salary for December is December 31, 2021 (Clause 2 of Article 223 of the Tax Code of the Russian Federation). But how to apply this rule if the salary was transferred on the last working day of 2017 - December 29? After all, it turns out that on December 29, 2021, the employee has not yet received income in the form of a salary, but the employer has actually already paid him the money.

Based on the results of the analysis of the above norms of labor and tax legislation, it can be concluded that they cannot be “adequately” applied to wages for December. If we talk about other months, then there are no problems: the month is over, the accountant took information from the working time sheet, calculated and issued wages, and withheld personal income tax. But you won’t be able to do this with December salaries, since they may need to be paid out before the end of December. But what then? We offer a solution.

Taxation of “severance” money

The issue of taxation of the final payroll does not arise. The entire salary that is due to a specialist for the time actually worked should be subject to income tax. Please note that if an employee is entitled to tax deductions, then apply them in the general manner.

Calculated vacation compensation upon dismissal is subject to personal income tax in the same way as regular vacation and wages. A rate of 13% is applied to compensation money; if there is a right to a tax deduction, the taxable amount is reduced by the amount of the deduction in the general manner.

If a specialist is entitled to severance pay, then the taxation procedure depends on the type and amount of payment. For example, benefits in case of staff reduction or liquidation of a company are not subject to income tax, but if an employee is paid a bonus as severance pay, it will have to be subject to income tax. All rules for taxation of this type of payment are in a separate material “Is severance pay subject to personal income tax?”

Travel expenses should not be subject to income tax if the daily allowance does not exceed the limit established in Article 217 of the Tax Code of the Russian Federation. So, if the daily allowance is more than 700 rubles per day for trips around Russia, and 2,500 rubles for trips abroad, then calculate deductions from the excess amount in the general manner. In this case, payment of personal income tax upon dismissal (terms) does not differ from the generally established ones.

How to determine the date of personal income tax transfer

When should personal income tax be transferred to the budget if salaries were paid to employees in the same month for which they were accrued (for example, for December in December)? It all depends on what was given: an advance or the final salary for the month. But how to distinguish an advance from a salary? You can issue wages for settlement no earlier than the last day of the month, since in order to accrue earnings, you must have a closed time sheet. And it is closed only on the last day of the month. Therefore, consider payments until the last day of the month as an advance.

If the organization issues wages, then transfer the personal income tax no later than the day following the day when the employees received the money (clause 6 of Article 226 of the Tax Code of the Russian Federation). Apply it also if the salary for the current month was paid on the last day of the month. For example, for December they paid on December 31st. Then transfer personal income tax on the first working day of January.

If you give an advance, then you do not need to withhold personal income tax from it. Do this on the last day of the month when income in the form of wages arose (clause 2 of Article 223 of the Tax Code of the Russian Federation). And transfer the tax to the budget no later than the next working day (clause 7, article 6.1 of the Tax Code of the Russian Federation). In the case of December salaries, the deadline for paying personal income tax is again the first working day of January.

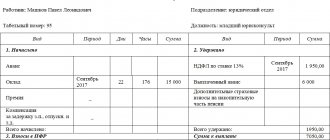

Innovation No. 7. The emergence of a new reporting form - annual 6-NDFL

This is an important answer to the question, personal income tax reporting in 2021: what changes have occurred. In 2021, companies submitted annual form 6-NDFL to the fiscal authorities for the first time. The deadline for submitting the form is 04/03/17 (April 1 is a non-working day, so the deadline is postponed to April 3).

All organizations and individual entrepreneurs that paid wages (or other forms of income) to individuals at least once during 2016 must submit the form. Even if the transfer was made once in January, after which there was no activity, an annual report is prepared.

The procedure for compiling the annual 6-personal income tax is similar to the formation of the quarterly one. The form states:

- all types of employee income;

- the deductions they receive;

- the amount of personal income tax accrued and paid to the budget throughout the state.

Tax officials will verify data from reporting forms submitted at the end of the year. Therefore, check whether the 2-NDFL report in 2017 is correct (changes must be taken into account) and whether its data matches the information in 6-NDFL.

If a company has not paid wages to anyone during the calendar year, it is not considered a tax agent and is not required to file 6-NDFL. This conclusion is contained in the explanations of the Federal Tax Service. In her opinion, there is no need to inform regulatory authorities about the reasons for failure to submit the document.

6 Personal income tax zero: to hand over or not?

Experts still advise you to play it safe and write to “your” Federal Tax Service a letter in any form (indicating the name of the organization, Taxpayer Identification Number, legal address), which will state the reason for failure to submit the form - the lack of payments to individuals in the reporting period. This will help avoid unnecessary questions and proceedings.

An accountant who wants to organize his work correctly and in accordance with the law must know everything about personal income tax in 2017: what changes (rate, deadlines, reporting) have occurred, how to take them into account in current activities. Keep your finger on the pulse of innovations, and you can avoid problems and disputes with regulatory authorities.

Similar articles

- KBK for personal income tax for employees

- How to reflect carryover vacation pay in 6 personal income taxes

- Personal income tax changes in 2021

- Deadline for submitting 2-NDFL (with sign 2) for 2021

- Reporting period for personal income tax - dates from 2021

Salary for December 2021, paid in December

Stella LLC accrued salaries for December 2021 in the amount of RUB 1,300,000. The amount of calculated personal income tax was 169,000 rubles. Salaries were issued on December 29, 2021.

The date when income in the form of wages arises is the last day of the month (Clause 2 of Article 223 of the Tax Code of the Russian Federation). Thus, the employee receives income in the form of salary for December on December 31, 2021. Since the salary was paid earlier than this date (December 29), this is an advance.

Please transfer your salary minus tax. However, according to the law, personal income tax must be withheld not on December 29, but on December 31 - the day when the income actually arose. The tax must be transferred to the budget the next day after the tax was withheld. That is, on the first working day after December 31, 2021 – January 9, 2021.

The maximum amount of advance payments to employees is not limited - a 100% advance can also be issued. Therefore, if an organization issues salaries for December on the 20th, then establish in the organization’s local documents that due to holidays, the amount of the advance payment can be increased to 100 percent. The main thing is that this order is enshrined in documents.

If the employer transfers wages for December to employees before the 29th day (for example, December 25, 26, 27 or 28, 2017). There should be no problems or ambiguities with the transfer of personal income tax. If, for example, the payment is made on December 25, then nothing will change. The tax must be transferred to the budget the next day after the tax was withheld. That is, on the first working day after December 31, 2021 – January 9, 2021.

Early transfer of personal income tax in December 2021

If the salary for December 2021 was paid in December 2017, then it is not necessary to wait until January 9, 2021 (the deadline for paying personal income tax) to transfer personal income tax. January 9, 2018 is the payment deadline. At the same time, there is no prohibition in the Tax Code of the Russian Federation on the transfer of withheld personal income tax before this date. Therefore, you can transfer personal income tax until the end of December 2021. It is impossible to fine a tax agent under Article 123 of the Tax Code of the Russian Federation for early transfer of personal income tax. After all, there is no offense for which liability is provided for in this article. The tax amount has been received by the budget and there is no arrears due to the tax agent. The Federal Tax Service of Russia does not object: it is illegal to fine organizations that pay personal income tax ahead of schedule (letter dated September 29, 2014 No. BS-4-11/19716).

Composition of the taxable basis and calculation

To understand when to pay personal income tax when dismissing an employee, you need to go through the entire chain of actions associated with determining the tax base and familiarize yourself with the features of calculating tax with compensation for unused vacation. Filling out instructions for transferring funds to the budget and the deadlines for paying personal income tax upon dismissal have also undergone changes.

Calculation procedure and calculation base

The basic personal income tax rate is 13%, it is used according to Art. 224, 225 Tax Code of the Russian Federation. Different tariffs apply to certain types of income. The formula for calculations is: (D―NV)*13%, where D is the monetary expression of income, NV is tax deductions. The transfer of the fee from the remuneration received by the dismissed employee is made according to form 6-NDFL, which displays the amounts of tax collected by type of income:

- salary and bonuses for actual working hours;

- compensation for unused vacation days;

- severance pay;

- subsidy for the period of searching for a new job;

- other debts.

The tax base is reduced through tax deductions. Calculating the fee when you have to fire an employee is no different from the procedure for monthly payroll. The discrepancy between the day of dismissal and the date of pay does not relieve the employer of the obligation to issue a paycheck within the prescribed period.

Non-taxable income and tax deductions

A number of subsidies were provided that are not part of the basis for calculating the fee. Most of them are financed from the state budget. The list of such benefits is as follows:

- unemployment benefits, pregnancy benefits;

- pensions, alimony and scholarships;

- subsidies for medical insurance of company employees. With a voluntary obligation, you can return the amount paid by filling out the 3-NDFL tax return, if the agreement was concluded by the employee himself;

- material assistance provided by the organization to the relatives of the deceased person;

- inheritance received and some donated items;

- income from personal farming.

The tax deduction is provided for in Art. 218–221 Tax Code for Heroes of the Russian Federation, disabled people of the Second World War and workers with minor children. The reduction amount for the first and second child is 1400 rubles/month. In the event of an accounting error or failure to provide a tax deduction to an employee, sometimes an excessive fee is paid. Typically, the refund is made by crediting the amount in the next reporting period.

Features of taxation of vacation compensation

When an employee leaves, he almost always retains some of the unused vacation time. Some changes have been made regarding the deadline for transferring personal income tax from compensation upon dismissal. The latest is a letter from the Ministry of Finance dated May 23, 2016, which explains that income is not always taxed: its amount must be no less than three times the average monthly salary, and for workers of the Far North - six times. When establishing the terms for withholding the fee from reimbursement of unused vacation, they are guided by the following provisions:

- Compensation is paid to the dismissed employee on the final day of work along with salary and other amounts due.

- The date of receipt of final payments, including lost vacation, is the control date for calculating personal income tax.

- Tax should be withheld from the employee’s income on the date of actual payment of dismissal amounts, i.e. on the last day of work.

You can transfer the fee withheld from the issued invoice to the budget on the same date or a day later. When filling out form 6-NDFL, the date of receipt of income is recorded in line 100, and the day of deduction is written in 110. It is better that both of these numbers coincide, indicating the simultaneity of events.

Filling out a payment document

The transfer of calculated taxes is carried out by submitting a payment order to the bank. You cannot make mistakes when entering information. To make the task easier, the purpose of some document fields is given by number:

- 101, payer status: organization - code 02, individual entrepreneur - 09;

- 104, KBK budget classification code: company that is a tax agent - 1821 0100 110, individual entrepreneur - 1821 0100 110;

- 107, the period for which the fee is paid: no number is given, only the month when the income was actually received.

You can fill out the payment form using the free Federal Tax Service service on the inspection website. If the deadline for paying personal income tax upon dismissal coincides with a weekend, then the transfer is postponed until the first working day.

Main innovations

The employer is a tax agent and is obliged to calculate and withhold personal income tax from the worker and transfer it to the budget. When a citizen is dismissed, the period from the last payment of the fee to the employee’s final paid day is determined for calculations. There are several innovations, the following are of practical importance for non-specialists:

- Personal income tax must be transferred no later than 24 hours after the day of final payment.

- Employees have the right to apply for deductions for treatment and training from their employer without waiting for the end of the tax period (calendar year). A notification from the Federal Tax Service department is submitted to the accounting department, which indicates the amount for each type of social deductions, and an application to the head of the company. Starting from the current month, the tax base will decrease until the withholding is reset to zero.

Innovation regarding accounting: a new form of the annual report 6-NDFL is presented in March. Its preparation is similar to a quarterly document, it indicates: the types of income of employees and deductions that they receive, the amount of tax across the entire state - accrued and paid. It is recommended to check the data in the new report with Form 2-NDFL.

Salaries issued in January 2017

Perhaps the organization's salary payment deadline falls on the period from the 9th to the 15th of the next month. In this case, you are not required to pay your December salary until the beginning of 2021. But if you want to give employees their salaries ahead of schedule, then you need to issue an order for early payment. See “Order for early payment of wages for December 2021: sample.”

If in January 2021 you pay your salary for December 2017, then personal income tax will be withheld when paying the salary. Income tax must be transferred to the budget no later than the day following the day on which the salary was transferred (clause 6 of Article 226 of the Tax Code of the Russian Federation). Therefore, if the salary for December 2021 was paid on January 9, 2021, the tax must be transferred to the budget no later than January 10, 2021.

Procedure and terms of self-payment

In order to independently pay personal income tax, a person must fill out a tax return in Form 3-NDFL according to the results of the tax year.

If the tax is paid in connection with receiving profit from working as a “freelancer”, this must also be indicated in the appropriate column.

The personal income tax form itself is a form, which includes 19 pages.

You can fill it out yourself or contact qualified lawyers. Lawyer services for this type of work cost about 300 rubles.

It is worth noting that all pages must be numbered, otherwise troubles may arise, including a fine.

Personal income tax is submitted at the place of registration of the taxpayer, and if necessary, accompanying documents can be attached to it (which ones will be indicated by the tax authorities themselves).

If we talk about the deadlines for paying personal income tax . then the last day is considered to be the 15th day after the end of the reporting period.

In the event that income is paid for which the tax agents did not withhold tax, then this is done 2 times exactly half the amount - no later than 30 calendar days from the date of receipt of the notification from the tax office. In this case, the second payment must be no later than one month from the date of the first payment.

Table. Deadlines for personal income tax payment in 2021

Conclusion

Next, we summarize the conclusions about the timing of personal income tax transfers from the December salary in the table.

| December salary paid in December | December salary paid in January |

| Transfer personal income tax to the budget on January 9 (the first working day after December 30), 2021. The fact is that personal income tax cannot be withheld until the end of the month. The date of receipt of income in the form of salary is considered to be the last day of the month, even if the entire salary was paid in advance on December 29 | Transfer personal income tax to the budget no later than the day following the day the salary is issued. For example, if employees were paid money on January 9, 2021, the tax must be transferred to the budget no later than January 10, 2021. |

How to issue a personal income tax payment order if the next day is a non-working day

The deadline for paying income tax for a dismissed employee is postponed if the date of transfer of personal income tax upon dismissal in 2021 coincides with a weekend or holiday. For example, an employee’s last working day is April 30. A full settlement has been made with him, and the calculated amount is withheld from payments. But it will not be possible to pay it, because the next day is May 1, the official holiday of all workers. May 2–5, according to the production calendar, are non-working days in 2020. As a result, the payment for personal income tax upon dismissal is dated Wednesday, May 6, the first working day after weekends and holidays.

Personal income tax in 2021 from salary - changes

This year, the percentage for withholding from any payments has remained unchanged. Its size is 13% in minimum terms. In some cases, the tax can be calculated using increasing factors, but the maximum value today is 35%. In 2017, every Russian citizen who officially receives a salary is required to remit income tax at a flat rate of 13%. This requirement is basic, but it does not apply to individual entrepreneurs and non-residents.

Since 2010, another obligation has been established for the employer, which is to independently transfer income tax from the salary paid out. It turns out that the employee can count on profit, already with the deduction of a fixed income tax. In addition, the expected salary in concluded employment agreements is indicated in advance with a designated deduction.

Deadline for transferring personal income tax from wages in 2021

In accordance with Article 221, the formal employer must transfer a fixed amount of income tax from the paid salary no later than the 1st day of the current month. In this case, the calculation is made from the final amounts, without stage-by-stage transfers. Previously, organizations were required to make payments from the advance salary issued.

Accordingly, the total deduction was divided into two parts: both parts amounted to 6.5%. Today, organizations do not have such an obligation, so they draw up all deductions from the total amount. Transfers can be made almost any time in the last week of the month, but no later than the 1st. This rule is established for the purpose that new deductions will need to be transferred in the new month. It is more convenient and expedient to fulfill your tax obligations on a monthly basis.

What amount is not subject to child tax when calculating wages?

Any amounts are subject to formal income tax. If an employee receives targeted financial assistance for a child, then this amount only reduces the estimated tax base.

In accordance with Article 224, a specific example :

if an employee receives, for example, 5,000 rubles, and child support is 1,000 rubles. then in this case the total tax base will be 4,000 rubles. If you calculate the expected rate on the calculator, it will be 520 rubles. Without children, a conditional employee enjoys the right to a deduction in the amount of 400 rubles in his respect. Accordingly, the base in this case would already be 4,600 rubles. It turns out that the end screen will be expected to cost 598 rubles.

Accordingly, the material assistance received only reduces the tax base without affecting fixed interest . In 2021, personal income tax on wages for children always remains unchanged.

Download the text of Article 224 of the Tax Code of the Russian Federation