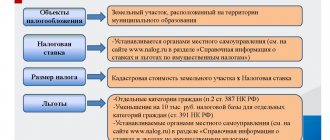

What is land tax for individuals?

Land tax is a tax levied on individuals who own land plots on the right of ownership, the right of permanent (perpetual) use or the right of lifelong inheritable possession.

The tax is not levied on individuals in relation to land plots held by them under the right of free use or transferred to them under a lease agreement.

Land plots of the following categories are not subject to taxation:

- included in the common property of an apartment building

- limited in circulation in accordance with the legislation of the Russian Federation, which are occupied by especially valuable objects of cultural heritage of the peoples of the Russian Federation, objects included in the World Heritage List, historical and cultural reserves, objects of archaeological heritage, museum-reserves

Land tax belongs to the category of local taxes and, as a consequence, rates are established by regulatory legal acts of representative bodies of municipalities.

In what cases are individuals beneficiaries?

For individuals at the federal level, a complete exemption from land tax has been established - in relation to the small indigenous population, provided that this population does not change their traditional way of life.

Other individuals who are taxpayers of land tax have the right to count on benefits that are established by reducing the tax base by a non-taxable amount. As a result, the tax payment may reach zero. Clause 5 Art. 391 of the Tax Code of the Russian Federation established that this amount should be equal to 10,000 rubles, and only certain categories of taxpayers can accept it for reduction. These include, for example, Heroes of the Soviet Union, WWII veterans, disabled people since childhood, as well as the first and second groups, “Chernobyl victims” and so on.

Municipal legislators are given the right to increase this amount, and they are also allowed to expand the list of categories of citizens who can be provided with such a benefit.

IMPORTANT! The benefit will be provided only upon presentation of supporting documents. The deadlines for filing these papers, as well as the rules for registration, are regulated by local regulations. However, going beyond February 1 of the year following the calculation year is prohibited.

***

Land tax is a local budget payment. That is, federal legislation establishes the general framework of tax rates and rules for providing benefits, and municipalities specify both the rates and preferential categories of organizations and individuals who are payers of land tax .

Similar articles

- We reflect the accrual of land tax in accounting - postings

- What are the deadlines for paying advance payments for land tax?

- Which budget is the land tax included in?

- Where and how to find out the land tax debt?

- How to calculate land tax: basic formula and nuances?

Calculation and rates of land tax

The land tax can be calculated using the formula: Land tax = KST * D * ST * KV KST - cadastral value of the land plot; D – size of the share in the right to the land plot; ST – tax rate; KV – land ownership coefficient (applies only in case of ownership of a land plot for less than a full year).

The cadastral value of a land plot is calculated by Rosreestr (Federal Service for State Registration, Cadastre and Cartography). The tax rate is established by regulations of the representative bodies of municipalities (laws of the federal cities of Moscow, St. Petersburg and Sevastopol). Thus, the tax rate differs in different localities (municipalities). For example, the land tax rate in Moscow is 0.025% for the so-called “dacha land”, while in the Moscow region the prevailing rate is 0.3%. In addition to the differences in the rate depending on the municipality of the site, the rate varies depending on the category of land. There is an upper limit on the tax rate fixed at the federal level. 0.3% for land plots:

- classified as agricultural lands or lands within agricultural use zones in populated areas and used for agricultural production;

- occupied by the housing stock and objects of engineering infrastructure of the housing and communal complex (except for the share in the right to a land plot attributable to an object not related to the housing stock and objects of engineering infrastructure of the housing and communal complex) or acquired (provided) for housing construction;

- purchased (provided) for personal subsidiary plots, gardening, market gardening or livestock farming, as well as summer cottage farming;

- limited in circulation in accordance with the legislation of the Russian Federation, provided to ensure defense, security and customs needs (Article 27 of the Land Code of the Russian Federation);

1,5%

in relation to other land plots. Detailed information about established tax rates and benefits can be found at any tax office or by using the following link.

Calculation of land tax when selling/purchasing a plot

In a situation where ownership of a land plot was for less than a full year, for example, when selling or buying a plot, the ownership coefficient is used to calculate the tax. The land plot ownership coefficient is the ratio of the number of full months during which this land plot was owned (permanent (perpetual) use, lifelong inheritable ownership) by the taxpayer to the number of calendar months in the tax (reporting) period - 12 months. When purchasing a plot of land

, the month is considered complete if ownership arose before the 15th (inclusive) of the month of purchase.

In the case of a sale

, a month is considered complete if ownership is terminated after the 15th of the relevant month. In other cases, the month is considered incomplete and is not taken into account when determining the ownership ratio.

How is land tax calculated?

The Federal Tax Service determines the amount for each land owner based on information from Rosreestr: cadastral value and category of land.

From April to September, tax officials send notifications to the registration address or the location of the site. The owner of the property must pay for the previous year by December 1 of the current year.

The amount is determined based on the length of time the land has been owned and the number of owners. When calculating, 4 options are used:

- For a full calendar year.

- For part of the year.

- For a share.

- According to the tax rate.

IMPORTANT! The owner is not exempt from paying unless he receives a receipt. The defaulter is issued a fine of 20% of the assigned amount. Tax officers have the right to demand payment of debt and penalties within three years from the date of purchase of real estate.

How to find out the cadastral value of a land plot?

You can find out the cadastral value of a land plot using the online service of Rosreestr called “Public Cadastral Map”. This site contains an interactive map of all subjects of the Russian Federation. After selecting the plot of land you are interested in, detailed information on it will be shown: type, cadastral number, status, address, category of land, form of ownership, cadastral value, area, etc. Searching for a site is possible using GPS coordinates, but this functionality does not always work correctly. All information about the land plot is available free of charge and without registration.

Calculation of land tax based on cadastral value

Rosreestr employees calculate the cadastral value of land every five years based on a number of factors:

- location;

- squares;

- socio-economic development of the region;

- soil quality;

- infrastructure;

- availability of amenities and residential buildings.

Information on the estimated cost is contained in the USRN database. It can be found on the Rosreestr website; to do this, you need to enter the cadastral number or address of the site. Or order a paid statement.

An electronic statement costs 250 rubles for citizens and 700 rubles for organizations, and a paper statement costs 400 rubles. and 1100 rub. respectively.

If the owner considers the cadastral value to be too high, he writes a statement to Rosreestr and asks to recalculate the price, and in case of refusal, he goes to court.

To independently calculate the land tax, you need to know two parameters: the cadastral price and the tariff rate. The tax rate is set by the state. Regional authorities, according to the Tax Code, have the right to reduce its size.

The law sets a rate of 0.3% for agricultural land and housing construction. To calculate the tax on other plots – 1.5%. The government has the right to reduce this figure to 0.1% or introduce benefits for individual citizens. The difference is compensated from the local budget.

ATTENTION! Indigenous residents of the Far East, Siberia and the Far North are exempt from paying taxes.

Land tax benefits for pensioners

In 2021, the President of the Russian Federation signed Federal Law No. 436-FZ “On Amendments to Parts One and Two of the Tax Code of the Russian Federation and Certain Legislative Acts of the Russian Federation.” In accordance with this law, a tax deduction is introduced that reduces land tax by the cadastral value of 600 square meters of land area. In fact, we are talking about the so-called 6 acres. All pensioners are eligible for this benefit.

, as well as the following categories of citizens: Heroes of the Soviet Union, the Russian Federation, disabled people of groups I and II, disabled people since childhood, veterans of the Great Patriotic War and military operations, etc. The tax for 2021, which will need to be paid in 2021, will be calculated based on this benefit.

Tax deduction is provided only for the cadastral value of 6 acres. If the area of the land plot is larger, then the tax will be calculated for the remaining area. For example, if the area of a land plot owned by a pensioner is 20 acres, then the tax will be charged only for 14 acres. Another feature of this law is that the deduction will be applied only to one plot of land

at the choice of the “beneficiary”, regardless of the category of land, type of permitted use and location of the land plot. In order to independently select a land plot to which the benefit will be applied, you must contact any Federal Tax Service Inspectorate with a Notification of the selected plot. If the notification is not received from the taxpayer, the deduction will be automatically applied to one plot of land with the maximum calculated tax amount.

Methods of paying land tax

Paying taxes online will allow taxpayers to save time. Citizens who are not Internet users can use other options for paying contributions.

Payment via bank

You must first make sure that the bank accepts contributions to pay off tax debts. You must have with you the notice received from the Federal Tax Service.

After payment, the taxpayer receives a receipt confirming the fact of payment. Funds are credited on the day of the operation or a day later.

As an alternative, citizens have the right to pay the tax at the post office or at the local government office.

This payment option is accompanied by a long wait in line and an additional fee for the transfer.

Internet banking

Payment is made by non-cash method, the money is debited from the taxpayer's current account. To make a payment you need:

- Register on the credit institution’s website.

- Enter payment details. The data is reflected in the receipt received from the Federal Tax Service.

- Confirm the transfer of funds.

The payer prints out a document confirming the fact of transfer of money or saves it in electronic form.

Payment on the tax service website

On the official portal of the Federal Tax Service in the “Electronic Services” section (category “Pay taxes”), Russian citizens independently generate a payment document and transfer the accrued amount.

To make a payment, you need to fill in the fields of the receipt, indicate your personal data and Taxpayer Identification Number. Payment is debited from a bank card.

This method allows the payer to obtain details without visiting the tax office. The division of the Federal Tax Service to which the land plot belongs is selected automatically on the website.

Via payment terminal

To pay the tax you need:

- Insert a plastic card into the terminal and enter the security code (if you don’t have a card, you can pay in cash).

- Select the “Payments” category in the main menu, click “Search for recipients”, then “Search by TIN”.

- Enter the payer's identification number, select the department of the Federal Tax Service (transfer recipient) from the list.

- Bring the barcode of the payment notice from the tax office to the scanner.

- Check the payment details displayed on the terminal monitor.

- Deposit money.

IMPORTANT! Paying tax through the terminal does not involve charging a commission.

On the State Services website

To pay the tax contribution on the State Services website, you must register. Authorized users with access to their Personal Account must select the “Tax Debt” section on the main page. To search for unpaid contributions, there are two options: by TIN or by the index of the document received from the Federal Tax Service.

After entering the data, the system processes the information and produces a list of taxes. You need to select a land plot, review the amount of debt and click “Pay.” To make a payment, you will need your bank card information.

After the transfer is completed, the receipt is saved in your Personal Account. The document is available for printing.

IMPORTANT! Debt repayment information is updated two weeks after payment.

other methods

You can close the debt through the Yandex.Money service. Through the “Payment for services” tab, you need to find the “Taxes” category. To search for data on unpaid contributions, it is suggested to use the TIN or index from the receipt from the tax service.

After verification, the system will provide information about the debt and the amount due. Through the “Pay” link, the user is taken to the page for filling out the payment document. You are required to provide the taxpayer's personal information and select the payment type.

ADVICE! After the funds are transferred, a link to the receipt appears. It must be printed and kept until the tax debt data is updated. If payment is delayed or not received at all, a check will help resolve the problem and avoid penalties.

Citizens of Russia can pay land tax through the “Taxpayer Personal Account”. The service was developed by the Federal Tax Service; to register in the system you need to visit the inspection department. After receiving identification data, access to your Personal Account will be opened. On the main page, the total amount displays information about debt and tax charges.

After clicking on the “Pay Now” button, options for closing the debt appear (State, etc.). The payer selects the appropriate method, and the system fills out the columns of the payment document automatically.

Legal basis of land tax

Land tax is a local tax payable in the respective regions.

The main provisions of land tax are determined by Ch. 31 Tax Code of the Russian Federation. At the same time, regions adopt their own laws in relation to it, by which they have the right to independently regulate a number of issues:

- establish and differentiate tax rates, provided that they do not exceed those given in the Tax Code of the Russian Federation;

- determine the procedure and deadlines for paying taxes by organizations, taking into account the restrictions existing in the Tax Code of the Russian Federation;

- introduce additional (in comparison with the Tax Code of the Russian Federation) tax benefits.

What other taxes need to be paid to the local budget, read the material “Federal, regional and local taxes in 2017.”

Why am I not receiving a receipt?

The most common reason for this is relocation. A person in a hurry forgets to notify the tax office about a change of address. Other explanations for this:

- You have not registered the land plot in the Russian Register;

- the subject has some benefits that exempt him from paying taxes;

- The amount to pay is less than one hundred rubles.

If you used to receive receipts, but now they don’t, you need to take care of resolving this issue. It is recommended to find out this information directly from the tax department; it is not always possible to find the answer through Internet technologies.

What is an object?

In paragraph 1 of Art. 389 of the Tax Code of the Russian Federation it is noted: an object should be understood as land plots located within a municipal formation (federal cities of Moscow and St. Petersburg), on the territory of which a land tax has been introduced. Under the land plot in accordance with Art. 11.1 of the Land Code of the Russian Federation is understood as a part of the earth’s surface, the boundaries of which are determined in accordance with federal laws.

Consequently, the object of taxation arises only when a specific land plot is formed (see also paragraph 2 of Resolution No. 54).

Now let's say a few words about tax calculation.

Who is not recognized as land tax payers?

Since the Tax Code establishes categories of land tax payers, the same regulatory act also creates a list of legal entities and individuals who are not subject to the payment of the tax burden.

This list is formed in Chapter 31 of the Tax Code of the Russian Federation and is exhaustive, that is, subject to change only in cases of adjustment to the current legislation.

According to this list, the following categories of participants in land legal relations will not be considered payers of land tax:

- Legal entities and individuals whose land plots are provided on a leasehold basis;

- Organizations and individuals who use certain land plots under the right of free, fixed-term use;

- Organizations involved in protecting the State Border of the Russian Federation;

- State-owned enterprises whose responsibilities include ensuring uninterrupted transport links within the Russian Federation (if such an exemption is established by the relevant regulatory act on the establishment of such a state organization);

- State organizations and enterprises providing storage of material assets included in the reserve fund for ensuring the stability of the Russian Federation;

- Institutions and bodies related to the penal system, divisions of the Ministry of Justice, as well as other government bodies ensuring the security of the Russian Federation;

- Divisions of the Ministry of Defense and equivalent organizations, whose responsibilities include monitoring compliance with legislation and protecting the interests of the Russian Federation;

- Research and educational organizations engaged in the preparation of scientific materials for the development of the economy and industry of Russia, as well as the preparation of a personnel reserve to improve the state of the scientific apparatus of various research centers.

This exemption from payment of land tax for these participants in land legal relations is due to their implementation of activities aimed at improving the situation of the state.

The land surveying of a garden plot is practically no different from the land surveying of any other type of plot. In what cases does the easement of a land plot terminate? Find out about it here.

Under certain conditions, you can receive a tax deduction when purchasing a plot of land. This is discussed in detail in our article.

Where can I get the details?

The method of obtaining all the details necessary for payment also depends on what category the payer belongs to - legal entities or individuals.

Therefore, these methods will be considered separately:

Legal entities

This category of landowners is obliged to independently calculate the amount of tax payable and transfer the necessary amounts quarterly throughout the year. An enterprise can obtain payment details from the tax office in whose jurisdiction the land plot is located, or in the corresponding section of the official website of the Federal Tax Service.