Basic Concepts

Primary documentation in accounting – what is it? It is called evidence of the fact of a business transaction reflected on paper. Currently, many documents are compiled in the automated 1C system. Processing of primary documentation involves registration and recording of information about completed business transactions.

Primary accounting is the initial stage of recording events occurring in an enterprise. Business transactions are actions that involve changes in the state of the organization’s assets or capital.

Highlights ↑

According to the law, any business transaction must be accompanied by documents. Accounting must be maintained in an organization from the moment of its registration.

Based on the accounting, reporting is prepared for the tax office and other services. Business transactions must be reflected in the accounting register.

Primary documentation can be drawn up on paper or machine media. In the second case, the management of the enterprise must make paper copies for other participants in the operation.

While working with primary documentation (PD), errors may be made. For example:

- a form is used that was not approved by order;

- there are no details in the documents;

- there are no persons who have the right to sign PD;

- cash documents contain amendments;

- the recording is made in pencil;

- free columns do not contain a dash;

- no seal.

When receiving accounting data, the following occurs:

- Preliminary work before completing documentation.

- Registration of PD.

- Their statement.

- Processing of primary data.

The primary document displays:

- name of the enterprise;

- legal address (location);

- account number and other information.

Requirements:

| The document must be drawn up | During or after the operation |

| Required details | Date, name of the organization and document, content of the operation and its measures, responsible persons and their signatures |

| The form must be standard | Approved by the statistics service |

| Corrections | Not allowed in documents |

| Storage is required | — |

The date in the primary documents is the same as the day the transaction was carried out. It can be one-time or cumulative.

One-time primary documentation (calculations, payments) is used once to confirm the operation, after which it is sent to the accounting department.

Cumulative (cards, orders) is used for a month or quarter if operations are repeated. After the document is accepted, the information from it is transferred to the register.

If documents are lost for any reason, you must:

| Using an order to appoint a commission | Which will investigate the reasons for the loss. If necessary, investigative authorities can be involved |

| Take measures to restore documents | For example, take account statements from the bank or ask for agreements and acts from counterparties |

If the documents could not be restored, it is not necessary to notify the tax office about this. In any case, a fine cannot be avoided.

The taxpayer is offered several options:

- restore at least some documents;

- make corrective entries in the income tax return;

- during a tax audit, provide the inspector with the opportunity to determine the amount that will have to be paid to the state budget.

To properly maintain the documentation list, there is a document flow schedule. They determine the timing of movement and the procedure for transferring documents.

An accountant has the right to make copies of documents, but only in the presence of representatives of the tax authorities. To do this, you need to give them a reason.

Only tax authorities are allowed to seize primary documents. It must be carried out in the presence of the governing bodies of the institution.

Definitions

| Primary accounting | The initial stage of perception of registration of transactions that characterize the actions taking place in the company |

| Primary document | A document that contains information about a business transaction carried out at an enterprise. This document confirms its implementation |

| Business transaction | An event on the basis of which changes occurred in the structure of assets and capital of the organization |

| Processing of primary accounting documents | This is a check of the documentation for correct formatting, filling in details and other information. |

| Accounting register | Special sheets of paper necessary for recording and processing data and recording them. Information in the register is a trade secret |

| External documents | Those that come from other institutions, for example, from a bank, tax service. These are payments, bills |

| Domestic | Issued at the enterprise |

What is included in primary documents?

Primary documents are divided into several types - organizational and administrative, supporting documents and accounting documents.

The first includes orders from superiors, instructions and various instructions. Required to authorize operations. Justification – invoices, demands, acts.

Such documentation reflects the fact of operations. The information they contain is entered into the Register. Some documents may be both permitting and exculpatory.

Documents that come to the accountant are checked for:

| Form | Correct formatting and filling, accuracy of details and data |

| Arithmetic calculations | — |

| Content | For the presence of contradictions and discrepancies |

The primary documents must indicate:

- title of the document and date of its preparation;

- name of the institution on behalf of which the document was drawn up;

- content of a business transaction;

- list of persons responsible for the operation;

- signatures.

Current standards

According to Federal Law No. 129 of November 21, 1996 “On Accounting”, primary documents must be stored for a period of at least 5 years.

Based on Article 18 of the Law “On Accounting”, in case of refusal to maintain accounting records, one faces criminal or administrative liability.

Article 120 of the Tax Code of the Russian Federation states that a fine of 5 thousand rubles is imposed for violating the accounting of income and expenses.

Article 9 of the Law “On Accounting” does not allow the correction of errors in the primary accounting documentation.

Processing of primary documentation in accounting: example of a diagram

As a rule, in enterprises the concept of “working with documentation” means:

- Obtaining primary data.

- Pre-processing of information.

- Preparation of documents.

- Approval by management or specialists authorized by order of the director.

- Re-processing of primary documentation.

- Performing actions necessary to conduct a business transaction.

Examination

The procedure for processing primary accounting documents is a formal check, consisting of several stages.

Correspondence

According to established standards and norms, the form of the document is verified and the details are correctly written. The timely completion of all papers and their submission to the accounting department must be checked.

Content Accuracy

The accuracy of reflected business transactions is taken into account, in accordance with legal standards and the requirements of the enterprise.

Arithmetic calculation

Filling out columns indicating tariffs and prices, as well as reconciling the total amounts for accuracy, are subject to mandatory control.

Classification

There is one-time and cumulative primary documentation. The processing of information contained in such papers has a number of features.

One-time documentation is intended to confirm an event once. Accordingly, the procedure for processing it is significantly simplified. Cumulative documentation is used for a certain time. As a rule, it reflects an operation performed several times. In this case, when processing primary documentation, information from it is transferred to special registers.

Stages of processing primary accounting documentation

Each enterprise has an employee on staff responsible for working with primary information. This specialist must know the rules for processing primary documentation, strictly comply with legal requirements and the sequence of actions.

The stages of processing primary documentation are:

- Taxation. It represents an assessment of the transaction reflected on paper, an indication of the amounts associated with its implementation.

- Grouping. At this stage, documents are distributed depending on common features.

- Account assignment. It involves the designation of debit and credit.

- Extinguishing. To prevent repeated payments, the accountant puts o.

What are primary accounting documents

It is necessary to understand what is generally meant by this definition. So, primary accounting documents are confirmation of business transactions carried out at the enterprise that brought some economic effect. This is a supporting document - for example, some kind of invoice.

These documents are important not only for accounting purposes. They are necessary to comply with tax laws and confirm all transactions. Using primary documents, you can determine the scope of the company's obligations to the state. The tax office will require these certificates to verify the accuracy of the calculations.

Primary documents must be drawn up immediately at the time of the operation, or immediately after its completion. But the latter is only possible if it is not possible to deal with paperwork during the process.

And it is worth remembering that such delays are highly discouraged and are allowed only in exceptional situations.

What is "primary"

This type of document is the one that confirms already completed business actions. For example, buying a new lathe. Without primary documentation capable of confirming this or that action, it is impossible to enter expenses/income or the receipt of anything in the accounting book.

Primary documents can be either electronic or paper - there is no difference. The only peculiarity of such electronic document management is that an electronic signature is required for confirmation. However, some businesses may limit their use of digital capabilities. According to the terms of the contract or in some cases regulated by law, it is possible to require the provision of only a paper “primary” document.

The primary accounting document must contain all the necessary information for accounting for business activities. Otherwise, tax problems may arise. If you cannot confirm any expense or income, the amount of deductions may increase.

Such a document is proof of the fact that some action was taken in the organization’s economy that affected the economic situation.

List of accounting documents

Interestingly, the law does not regulate specific documents, so you can choose from many acceptable options. This will allow you to adjust the convenience of reporting. But what kind of “primary” is there anyway?

- Agreement . Contains specific terms of a business transaction. It lists all the financial nuances and the responsibility of all parties involved for implementation.

- Packing list . Listing of all services provided or goods transferred. It is kept by each participant in the transaction - you will need to make copies.

- Transfer and acceptance certificate . Confirms that the service was performed in full and its quality satisfies the agreed upon. This act confirms the acceptance of the work performed and, accordingly, the full approval of the customer.

- Transfer and acceptance certificate No. OS-1 . Unlike the previous document, it is used in recording activities with the input and output of fixed assets.

- Check . Confirmation of willingness to pay for a product or service. The invoice may list additional conditions and prices for the services provided. This document also allows you to return money.

- Payslip . Used to solve business problems related to personnel. That is, these statements take into account all salary situations. It is necessary to include not only the salary itself in the payslip. But also all bonuses, overtime, incentives and other cash “infusions” into the employee.

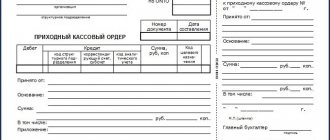

- Cash documents . Necessary for accounting for financial transactions for the sale of goods or services. This category includes not only the cash book, but also receipt and expense orders.

Naturally, all these documents are drawn up differently depending on the established rules and procedures. The basic rules are defined and must be followed when creating a primary.

Classification of primary documents

There are several ways to categorize accounting records. This significantly simplifies the definition and document flow itself. Grouping occurs according to certain principles and features.

So, the primary documents are divided:

- By appointment . There are administrative ones - powers of attorney and payment orders; executive/exculpatory – pay slips and certificates of work performed; accounting documents – statements, calculations and certificates; combined – cash orders, advance reports and claims; and strict reporting forms - subscriptions, receipt books, and so on.

- By volume of data content . The actual primary documents are included - cash orders and checks; and consolidated primary documents - cash reports for a certain period and statements.

- According to the method of reflecting business transactions . There are one-time reports - cash reports; and accumulative statements and limit cards.

- According to the place of compilation . Divided into internal (everything formalized by the organization) and external (received from suppliers, outsourcers, and so on).

This comprehensive classification reflects almost all primary documents that accounting may encounter when preparing reports.

Errors in documents

They can occur for various reasons. Basically, their appearance is caused by the employee’s careless attitude towards the work he performs, the specialist’s illiteracy, and equipment malfunction.

Correction of documents is highly discouraged. However, in some cases it is impossible to do without error correction. The accountant must correct any deficiencies in the primary documentation as follows:

- Cross out the incorrect entry with a thin line so that it is clearly visible.

- Write the correct information above the crossed out line.

- Put o.

- Specify the date of adjustment.

- Put a signature.

The use of corrective agents is not permitted.

Corrections in primary documents

1. If this is not a strict reporting form, then the document must be rewritten correctly and the damaged document must be destroyed.

2. Cross out the strict reporting form with a red oblique line from one corner of the sheet to the other and make the entry “cancelled.” Do not destroy the damaged form.

3. Acceptable corrections: cross out the incorrect entry with one thin line, make the correct entry at the top, write “Believe the corrected” next to it, put the signature of the official and the seal of the enterprise.

4. You can't! Completely cross out or shade the incorrect entry; it must be visible under the strike line.

What is a business plan, why is it needed and how to draw it up yourself, you can find out here.

A sample of a primary document - a waybill.

Working with incoming documents

The process of processing incoming papers includes:

- Determining the document type. Accounting papers always contain information about completed business transactions. For example, these include an invoice, an order for receiving funds, etc.

- Checking the recipient's details. The document must be addressed to a specific enterprise or its employee. In practice, it happens that documents for the purchase of materials are specifically issued to the company, although no agreement has been concluded with the supplier.

- Checking signatures and seal impressions. The persons signing the document must have the authority to do so. If the endorsement of primary documents is not within the competence of the employee, then they are considered invalid. As for stamps, in practice, errors often occur in those enterprises that have several stamps. The information on the print must correspond to the type of document on which it appears.

- Checking the status of documents. If damage is detected on the papers or any sheets are missing, it is necessary to draw up a report, a copy of which is sent to the counterparty.

- Checking the validity of the event reflected in the document. Employees of the enterprise must confirm information about the fact of the transaction. Documents on acceptance of valuables are certified by the warehouse manager, and the terms of the contract are confirmed by the marketer. In practice, there are situations when a supplier receives an invoice for goods that the company did not receive.

- Determining the period to which the document relates. When processing primary papers, it is important not to take into account the same information twice.

- Definition of accounting section. When receiving primary documentation, it is necessary to establish for what purposes the supplied values will be used. They can act as fixed assets, materials, intangible assets, goods.

- Determining the register in which the document will be filed.

- Registration of paper. It is carried out after all checks.

Accounting document processing

⇐ PreviousPage 12 of 17Next ⇒During his work, an accountant deals with various documents. Primary documents include such as incoming and outgoing cash orders, an invoice, a bill of lading, a power of attorney to receive something, a payment order, a check from a checkbook, etc. According to the principle of continuity, accounting is carried out without interruption from the moment the enterprise is organized, and all facts of economic life are reflected in the accounting accounts on the basis of primary documents.

Proper execution and the ability to check primary documents are the basis for the qualified work of an accountant.

The primary document is drawn up, as a rule, at the time of the transaction or immediately after its completion on a standard form, printed, filled out by hand or using a computer. The document is usually drawn up in several copies, with free lines crossed out.

Each primary document reflects one completed business transaction. A business transaction is understood as a reflection in the accounting records of the movement of the property of an enterprise, carried out in cash using double entry. There are certain requirements for primary documents. The document has the required details:

1. name of the document;

2. name and legal address of the parties (entities) participating in the business transaction. In any transaction there are two parties - goods, services, funds move from one subject of the transaction to another. The parties, or subjects, mean individuals and legal entities. Individuals are citizens of this and other countries, legal entities are enterprises, organizations, their associations, each of which has its own charter, separate property, a separate balance sheet of income and expenses, bank accounts, the right to conduct contractual relations on its own behalf, a seal and various branded paraphernalia;

3. date of document preparation.

4. content of the business transaction. It is necessary to comply with the requirements of strict correspondence between the name of the document and the content of the operations carried out on it. In this case, the content of a business transaction follows from the name of the document in which it appears in general form.

5. meters of the operation being carried out;

6. names of officials responsible for the operation;

7. signatures of the persons who compiled the document and their transcript.

Documents must be drawn up clearly, legibly, by hand, using a typewriter or computer. Each document must be completed in the chosen manner from beginning to end. For documents, as a rule, standard forms are used, produced in the form of forms, samples of which are approved by the State Statistics Committee of the Russian Federation.

To correctly compile a document you must:

• fill out a document on a form (if it is not available, on a blank sheet of paper) with a pen, on a typewriter or using a personal computer;

• strictly adhere to the established form and details of the document;

• accurately state the contents of the document;

• write text and numbers clearly and legibly;

• cross out unfilled spaces in the document form;

• indicate the amount in monetary documents in figures and words;

• provide the document with the necessary legible signatures indicating the positions of the persons signing the document.

All documents must first be processed before they are recorded in accounts. The following stages of processing accounting documents are distinguished.

1. Document verification:

• checking compliance with the form and details;

• checking the legality of the transaction;

• arithmetic check.

2. Taxation (expressed in the conversion of natural measures into monetary ones).

3. Extinguishing.

4. Grouping of documents according to homogeneous characteristics (by cash register, current account).

5. Transfer of document contents to accounting registers.

6. Filing by groups of documents and submitting to the archive. Particular attention is paid to document verification. Upon receipt of a document, a check must be carried out for the completeness of its contents (formal check), arithmetic (account check) and substantive check (logical check).

When formal

verification checks whether all the necessary details are filled out, whether the document contains the necessary signatures, whether there are any erasures, blots, or unspecified corrections.

Counting

verification allows you to establish the correctness of arithmetic calculations and taxation results.

The purpose of substantive testing is

identify the legality of the business transaction recorded in the document. At the same time, it is checked whether this operation was actually performed and to the specified extent.

After this, the documents are grouped according to the homogeneous characteristics necessary for accounting. Then, on each primary document, corresponding accounts are indicated (account assignments are made) and the amounts of business transactions according to accounting entries are recorded in the accounting registers.

By cancellation

is called a mark on documents about their use. Cancellation occurs by crossing out the document or affixing a stamp (preferably in red ink) “received”, “paid” or “redeemed”. All monetary documents are subject to prompt cancellation in order to prevent their reuse. All documents are subject to accounting cancellation after they are recorded in the accounts in order to avoid erroneous re-entry and to prevent any abuse. This cancellation is carried out by placing a marking stamp on the documents.

Document flow concept

Since accounting is a structural division of an enterprise, accounting documents are part of the documentary fund of the organization as a whole and are included in the general document flow.

Document flow to the movement of documents in an organization from the moment they are created or received until the completion of execution or dispatch.

The movement of primary documents in accounting is regulated by a schedule. Accounting documents go through the same stages of processing as all other documents of the organization.

Figure 16 Simplified document flow diagram of an enterprise

The speed of decision-making ultimately depends on the clarity and efficiency of processing and movement of documents. Therefore, much attention is always paid to the rational organization of document flow, especially in accounting, where untimely processing of financial documents can lead to negative economic consequences.

All accounting documentation, like the enterprise as a whole, is divided into 3 document flows: 1. incoming (incoming) documents; 2. outgoing (sent) documents; 3. internal documents

In the technological chain of processing and movement of documents, the following stages are distinguished: reception and primary processing of documents; preliminary review and distribution of documents; registration; control over execution; execution of documents; dispatch.

Documents can be received by mail, received by teletype, fax, e-mail, delivered by courier or by a visitor.

Organization of work with documents is the creation of optimal conditions for all types of work with documents, from the creation or receipt of a document to its destruction or transfer to archival storage.

Table 6 Types of work with documents.

| Components | Office Operations | Document groups | ||

| internal | outgoing | inbox | ||

| Documentation | Drafting a document | Necessarily | Necessarily | not used |

| Coordination of the project with specialists | Maybe | Maybe | not used | |

| Checking the correctness of the document | Necessarily | Necessarily | not used | |

| Signing (approval) of the document by the manager | Necessarily | Necessarily | not used | |

| Registration | possible | possible; sending | possible; marking | |

| Organization of work with documents | Execution control | Maybe | Maybe | Maybe |

| Execution of documents | Necessarily | Maybe | Necessarily | |

| Formation of cases | Necessarily | Necessarily | Necessarily | |

| Current storage and use | Necessarily | Necessarily | Necessarily | |

| Transfer to archival storage | Maybe | Maybe | Maybe | |

| Review of documents by the manager (resolution) | Maybe | not used | Maybe | |

| Destruction of documents | Maybe | Maybe | Maybe |

Accounting documents may arrive in the general flow of documents addressed to the institution. In this case, they are received and processed by a specially designated employee (most often a secretary-assistant)

Transmitting documents by email poses the problem of verifying the authenticity of the signature (authorization of the document), i.e. application of a special “electronic signature” program and conclusion of a special authorization agreement with each correspondent.

Upon receipt of documents, after checking the correctness of their delivery, the envelopes are opened and the correctness of the attachment and integrity (number of pages, attachments) is checked.

For documents received by mail and overdue, envelopes are retained, because in this case, the stamp on the envelope serves as proof of receipt of the document. For such an expired document, an act for receiving the document is drawn up, which is signed by two employees of the enterprise and a postal worker. All received documents must have a receipt stamp. The requirements of the chief accountant regarding the procedure for registration and submission of necessary documents and information to the accounting department are mandatory for all divisions and services of the enterprise.

Instructions for working with accounting documentation recommend that the submission of primary documents to the accounting department be regulated by a document flow schedule drawn up by the chief accountant and approved by the manager. The schedule establishes a rational workflow, i.e. provides for the optimal number of units and executors for each primary document to pass through, and determines the minimum period for its presence in the unit. The document flow schedule should help improve all accounting work in the organization, strengthen the control functions of accounting, and increase the level of automation of accounting work. The schedule is drawn up either in the form of a diagram or in the form of a list of works on the formation, verification and processing of documents filled out by each department, as well as specific performers, indicating their relationship and deadlines for completing the work.

Documents created in accounting are its internal documents. They make up most of the accounting documents (order books, etc.).

Further processing of accounting documents has its own specifics and takes place in the accounting department. In accordance with the distribution of job responsibilities specified in the job description, the received document is transferred to the accounting employee to whom this area of work is assigned (time sheet - to the payroll employee). All primary documents received or compiled by the accounting department are subject to mandatory verification in form (completeness and correctness of filling in details) and in content (legality, logical linking of indicators). Next, the documents are systematized in chronological order and documented in accounting registers (Article 10 of Federal Law No. 129)

Accounting registers are kept in special books (journals) on separate sheets and cards, as well as on computer media. Transactions are recorded in registers in chronological order according to the corresponding accounting accounts. Organizational and administrative documents of the accounting department are processed with all documents of the enterprise by the secretary.

When sending, it is necessary to check the correctness of the document: presence of a signature; availability of date; presence of a title; correctness of addressing; availability of all pages and applications. An incorrect or incomplete document will be returned for revision.

Figure 17 Organization of document flow.

Employees of production and functional services fill out and submit documents related to the scope of their activities according to this schedule. For this purpose, each performer is given an extract from the schedule. It lists the source documents, the deadlines for their submission and the departments in which they should be submitted.

The chief accountant monitors compliance with the document flow schedule.

⇐ Previous12Next ⇒

Didn't find what you were looking for? Use Google search on the site:

Working with outgoing papers

The processing process for this type of documentation is somewhat different from the above.

First of all, an authorized employee of the enterprise creates a draft version of the outgoing document. Based on this, a draft paper is developed. It is sent to the manager for approval. However, another employee who has the appropriate authority can approve the draft document.

After certification, the project is drawn up according to the established rules and sent to the recipient.

Document flow planning

This stage is necessary to ensure prompt receipt, sending and processing of documentation. For proper organization of document flow, the enterprise develops special schedules. They indicate:

- Place and deadline for processing primary papers.

- Full name and position of the person who compiled and submitted the documents.

- Accounting records made on the basis of papers.

- Time and place of storage of documentation.

Features of document recovery

Currently, the regulations do not contain a clear procedure for the restoration of papers. In practice, this process includes the following activities:

- Appointment of a commission to investigate the reasons for the loss or destruction of documents. If necessary, the head of the enterprise can involve law enforcement agencies in the procedure.

- Contacting a banking organization or counterparties for copies of primary documents.

- Correction of income tax return. The need to submit an updated report is due to the fact that undocumented expenses are not recognized as expenses for tax purposes.

In case of loss of primary documentation, the Federal Tax Service will calculate the amounts of tax deductions based on the available papers. In this case, there is a possibility that the tax authority will apply penalties in the form of a fine.

Common mistakes in the process of preparing primary papers

As a rule, those responsible for maintaining documentation commit the following violations:

- Fill out forms that are not unified or approved by the head of the enterprise.

- They do not indicate details or display them with errors.

- They do not endorse documents with their signature or allow employees who do not have the authority to sign documents.

Documentation confirming the facts of business transactions is extremely important for the enterprise. Its design must be approached very carefully. Any mistake can lead to negative consequences.