What is primary documentation in accounting?

An example of a “primary document” in accounting is any document confirming transactions of a taxpayer. We are talking about transactions that are related to the economic activities of the organization and make economic sense.

All primary accounting documentation is described in Federal Law No. 402-FZ “On Accounting”. Documents must be collected and executed in accordance with this law in order to confirm expenses and prove to the Federal Tax Service the correctness of the calculation of the tax base.

The primary document must be drawn up at the time of the business transaction, since the document confirms its completion. Typically this is done by the supplier. The list of primary accounting documentation accompanying the transaction depends on the type of transaction and may differ. You need to be especially careful about the documents for transactions in which you are the buyer, since these are your expenses and you are more interested in the correct execution of documents than the supplier. The tax office may not credit the “primary” with errors.

What information should the forms of primary documents contain?

Despite the fact that there are currently no mandatory primary documents for all forms, the legislator has established requirements for the content of such documents. The list of mandatory details that must be contained in each primary document is given in paragraph 2 of Art. 9 of Law No. 402-FZ. These are, in particular:

- document's name;

- the date on which such document was drawn up;

- information about the person who compiled the document (name of the company or individual entrepreneur);

- the essence of the fact of economic life that was formalized by this document;

- monetary, numerical characteristics, measures of the event that occurred (for example, in what volume, in what units and for what amount were the products sold to customers);

- information about the responsible specialists who documented the event, as well as the signatures of such specialists.

If the primary source does not meet the requirements, the organization may also face tax consequences.

Get free access to K+ and learn about the most common complaints tax authorities have and how to counter them.

For information on how the right to sign is delegated, read the article “Order on the right to sign primary documents - sample.”

Storage of primary documents

The primary product must be stored for at least 5 years. During this period, the Federal Tax Service may request documents from you or your counterparties at any day in order to conduct an inspection. Documents will also be needed in case of legal disputes.

Previously, storing documents required racks, folders and a lot of paper. Now, to free up space in the office and save time and money, transfer the primary archive to electronic form. Accounting services help organize documents and store scans of them in an electronic archive - this makes it easier to search for documents. In the service list, it is easier to track the shortage of primary goods, closure, payment and transaction documents. Electronic documents are certified with an electronic signature.

If a company does not have a primary document whose mandatory storage period has not yet expired, it will receive a fine of 10 to 30 thousand rubles. Another problem with loss of documents is the inability to take into account expenses to calculate the tax base. In this case, the tax office will charge additional tax, and the company will have to pay extra.

How to make corrections to primary documents

If, after a document has been accepted for accounting, an error is discovered in it, it is no longer possible to replace it with a new one, you can only correct the existing one. An exception is invoices and UPD. Correction forms are provided for them.

To make a correction to a paper document, you need to follow these steps:

- Cross out the incorrect text or amount with one line. So that you can read the corrected one.

- Above the crossed out text, write the corrected text or amount.

- Confirm the correct data with the entry “Corrected” and the signatures of the persons who compiled the document being corrected, indicating their last names and initials (other details that allow identifying these persons), indicate the date the corrections were made.

The organization can decide for itself how to make corrections to electronic primary documents. The chosen method must be recorded in the accounting policy.

Primary documents are divided by business stage

All transactions of the company can be divided into three stages:

The first stage is an agreement on the terms of the transaction . The result will be an agreement and an invoice for payment.

The second stage is payment for the transaction . Primary documents confirming payment:

- Cash payments - cash receipt, receipt for cash receipt order, strict reporting form. Organizations rarely pay each other in cash, since the amount of payments through the cash register is limited to 100 thousand rubles. Employees usually receive advances or accountable money in cash.

- Electronic payments, including acquiring, payment systems or transfers from a current account - bank account statement.

The third stage is receiving products . Confirmation is required that the buyer has received the product or service, and the seller has received payment. Without supporting documents, the tax office will not allow you to include the funds spent in expenses. Receipt is confirmed:

- waybill;

- sales receipt;

- act of work performed or services rendered.

Primary documents and accounting registers

How can primary accounting documents be classified?

If the primary document was issued by the company itself, then it can belong either to the group of internal or to the group of external. A document that is drawn up within the company and extends its effect to the compiler company is an internal primary document. If the document was received from the outside (or compiled by the company and issued to the outside), then it will be an external primary document.

The company's internal documents are divided into the following categories:

- Primary administrative documents are those with which a company gives orders to any of its structural units or employees. This category includes company orders, instructions, etc.

- Executive primary documents. In them, the company reflects the fact that a certain economic event has occurred.

- Accounting documents. With their help, the company systematizes and summarizes information contained in other administrative and supporting documents.

After a business event has been documented as a primary document, it is then necessary to reflect the event in the accounting registers. They, in fact, are carriers of ordered information; they accumulate and distribute the characteristics and indicators of business transactions.

The following registers are distinguished by their appearance:

- books;

- cards;

- free sheets.

Based on the method of maintaining the register, the following groups are distinguished:

- Chronological registers. They record the events that happened sequentially - from the first in time to the last.

- Systematic registers. In them, the company classifies completed transactions by economic content (for example, a cash book).

- Combined registers.

According to the criterion of the content of information reflected in the registers, the following are distinguished:

- synthetic registers (for example, a journal order);

- analytical registers (payroll);

- combined registers, in the context of which the company carries out both synthetic and analytical accounting.

For more information about accounting registers, see the article “Accounting registers (forms, samples)” .

Primary documentation in accounting list of documents 2020

Transactions vary significantly from company to company. Despite this, there is a list of primary documentation that is required in accounting:

- Agreement.

- An invoice for payment.

- Payment documents: cash receipts, strict reporting forms.

- Packing list.

- Certificate of work performed or services provided.

- Invoice.

This list of transaction documents is not exhaustive; it can expand depending on the types of transactions and accounting features in the organization.

Design rules

According to the Decree of the State Statistics Committee of the Russian Federation dated March 24, 1999 No. 20, primary documents in the accounting department can be combined. The organization has the right to take the regulated form as a basis and add the necessary lines to it.

All forms of primary accounting used in the daily activities of the company must be approved by its accounting policies. If the counterparty with whom the company cooperates also uses forms of its own design in its work, then this must also be indicated in the accounting policy.

Important! By law, an organization can use any form of primary documentation, but according to information from the Ministry of Finance of the Russian Federation No. PZ-10/2012, strict reporting cash forms must only have a unified form.

Receipt cash order

Formation of primary accounting documentation

The rules for maintaining primary documentation allow for its compilation using independently developed or unified forms (Article 9 No. 402-FZ). But remember that only a document containing all the necessary details has legal force:

- Title of the document.

- Date of creation.

- The name of the organization or the name of the entrepreneur of the compiler.

- Contents of a document or business transaction.

- Natural and monetary indicators.

- Data of responsible persons.

- Signatures of the parties.

The primary forms that the organization uses are fixed in the accounting policies. In the process of work, there may be a need to update or supplement forms - this is also recorded in the accounting policy.

Let's look at the primary documents in more detail.

The role of the primary document in accounting

Primary documents are documents with the help of which the company formalizes the economic events that occurred at the enterprise (Clause 1, Article 9 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ).

The first thing that accountants of any organization should clearly understand is that today there is no specific mandatory list of forms for primary accounting documents. Any company determines for itself the forms of primary documents depending on the purpose of their use.

However, for such documents a list of mandatory details is legally established (Clause 2, Article 9 of Law No. 402-FZ).

IMPORTANT! The forms used in accounting must be fixed in the accounting policy of the organization (clause 4 of PBU 21/2008, approved by order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106n).

For information about how long primary documents need to be stored, read the material “What is the period of storage of documents in an organization’s archive?”

Please note that as of October 26, 2020, new sanctions for improper storage of documents apply. Read more about this in ConsultantPlus. Trial access to the system is provided free of charge.

Agreement

When concluding a transaction, the parties enter into an agreement between themselves, which stipulates all the conditions and details of future business transactions: terms of shipment of goods, performance of work or provision of services, time for payment, payment method, etc.

Additionally, the contract records data on the subject of the transaction and the price. The rights and obligations of the parties also need to be spelled out to make it easier to resolve possible disputes in court.

It is optimal if each transaction is formalized in a separate agreement. But companies often enter into one general agreement with regular counterparties for a number of similar transactions at once. Draw up two copies of the agreement with seals and signatures of the parties on each.

A written form of agreement is not always necessary. For example, for a purchase and sale transaction, the document confirming the conclusion is a cash receipt or sales receipt.

Approval of primary documentation forms

Non-unified primary documentation can be developed by business entities independently. For such forms, the main criterion for compliance with legal norms is compliance with the standards of Law No. 402-FZ in terms of mandatory details:

- Title of the document;

- date of registration;

- information about the company drawing up the form, by which the company can be identified;

- the content of the displayed business transaction indicating the valuation of the subject of the transaction;

- bringing natural measures and quantitative values;

- presence of signatures of responsible officials (with mandatory indication of their position and full name).

REMEMBER! To use independently developed templates as primary documentation, they must be approved by a local act of the enterprise.

Cash and payment documents belong to a group of strictly regulated forms. Enterprises, by their order or any other order, are not authorized to remove rows, cells from them, or change the structure. Enterprises can make their own adjustments to non-unified templates, add and remove information blocks. When independently developing new forms, you can take standard samples as a basis.

Forms of primary accounting documentation for recording cash transactions , for recording inventory results

To approve the primary statement, you can include its examples in a separate appendix to the accounting policy. The second option is that for each form the manager issues an order for the enterprise. The text of the order specifies information about the introduction of new forms of documentation into accounting, which must be drawn up according to a single template. The forms themselves are included in the order as separate attachments.

If an organization is going to use standard forms recommended by the relevant departments to reflect individual transactions, then these forms do not need to be approved by internal regulations. To record such a decision, it is enough to make an entry in the accounting policy about the use of standardized templates.

When introducing new forms of documents into the document flow system, it is advisable to approve them by order.

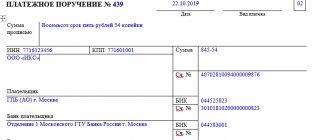

An invoice for payment

An invoice is a document in which the seller sets the price for his services or goods.

The buyer agrees to the supplier's terms and conditions at the time of payment. The legislator does not establish the form of the invoice, so each company draws it up in its own way. The invoice specifies the terms of the transaction, terms, payment and delivery procedures, etc.

The signature of the director or chief accountant on this document is not required (Article 9 No. 402-FZ). But to avoid any questions from the tax authorities or counterparties, it is better not to neglect them. An invoice for payment does not provide an opportunity to present demands to the supplier - it only records the purchase price. The buyer retains the right to demand a refund in case of violation of the terms of the contract or illegal enrichment of the supplier.

List of possible primary accounting documents

The list of primary accounting documents in 2020-2021 may be as follows:

- Packing list. This is a document that reflects the list of transferred inventory items. The invoice is issued in 2 copies and contains information that is subsequently reflected in the invoice. The invoice is signed by representatives of both parties involved in the transaction and certified by a seal (if the company uses it in its practice).

Read about its most commonly used form in the article “Unified form TORG-12 - form and sample.”

- Record of acceptance. It is drawn up upon completion of certain works (services) to confirm that the result of the work meets the original requirements of the contract.

See a sample of such an act here.

- Primary documents for payment of wages to personnel (for example, pay slips).

For more information about these statements, see the article “Sample of filling out the payroll statement T 49” .

- Documents related to the presence of fixed assets - here the company can draw up such documentation from the list of primary accounting documents:

- Certificate of acceptance and transfer of fixed assets in the OS-1 form - upon receipt or disposal of an object not related to buildings or structures.

For more information about this act, see the material “Unified Form No. OS-1 - Certificate of Acceptance and Transfer of OS” .

- If the fixed asset is a building or structure, then its receipt or disposal is formalized by an act in the OS-1a form.

For more information, see the article “Unified form No. OS-1a - form and sample” .

- The write-off of an asset is formalized by an act in the OS-4 form.

For more details, see the material “Unified Form No. OS-4 - Act on the write-off of an asset” .

- If it is necessary to document the fact of the inventory carried out, an inventory list of the fixed assets is drawn up in the INV-1 form.

For more information about such a primary document, see the article “Unified form No. INV-1 - form and sample” .

- If the inventory was carried out in relation to intangible assets, then the inventory will be compiled according to the INV-1a form.

For more information, see the material “Unified form No. INV-1a - form and sample” .

- A separate group of primary documents are cash documents. These include, in particular, the following list of primary accounting documents for 2020-2021:

- Receipt cash order.

For more information about its preparation, see the article “How is a cash receipt order (PKO) filled out?” .

- Account cash warrant.

For details about it, see the material “Cash expenditure order - form and sample.”

- Payment order.

Read about the rules for preparing this document here.

- Advance report.

Read about what to follow when drawing up such a document in this article.

- The act of offsetting mutual claims.

Read about the specifics of using this document here.

- Accounting information.

For information on the principles of its execution, see the material “Accounting certificate of error correction - sample”.

The above list does not exhaust the entire scope of primary documents used in accounting, and can be expanded depending on the characteristics of the accounting carried out in each specific organization.

You will find a complete list of primary documents in the Directory from ConsultantPlus. Get trial access to the system and proceed to the list.

IMPORTANT! They are not primary accounting documents from the list 2020-2021 - the list was proposed above:

- Agreement . This is a document that stipulates the rights, obligations and responsibilities of the parties involved in the transaction, the terms and procedure for settlement, special conditions, etc. Its data is used when organizing accounting for the analytics of settlements with counterparties, but it itself does not generate accounting transactions.

- Check. This document reflects the amount that the buyer agrees to pay by accepting the supplier's terms. The invoice may contain additional information about the terms of the transaction (terms, payment and delivery procedures, etc.), i.e. it supplements the contract.

- Invoice. This document is drawn up for tax purposes, since on its basis buyers accept for deduction the amounts of VAT presented by suppliers (clause 1 of Article 169 of the Tax Code of the Russian Federation). Thus, in the absence of other documents characterizing a particular transaction, it will be impossible to confirm expenses for this transaction with an invoice (letter of the Ministry of Finance of the Russian Federation dated June 25, 2007 No. 03-03-06/1/392, Federal Tax Service dated March 31, 2006 No. 02-3 -08/31, resolution of the Federal Antimonopoly Service of the East Siberian District dated April 19, 2006 No. A78-4606/05-S2-20/317-F02-1135/06-S1).

It should be borne in mind that the unified forms of primary accounting documents given in the list are not mandatory for use, since since 2013 (after the adoption of Law No. 402-FZ), forms of such forms can be developed independently. But in most cases they continue to be used. Therefore, in 2020–2021, the list of unified forms of primary accounting documents contained in the resolutions of the State Statistics Committee continues to remain relevant.

Bill of lading or sales receipt

Sales receipts are issued in two cases: when selling goods by individuals or when selling to individuals.

Invoices, as a rule, are used by organizations to document the sale of goods and their further receipt by the buyer.

Like the contract, the invoice is drawn up in two copies. One remains with the supplier to confirm the transfer of goods, and the second is received by the buyer to confirm receipt.

The data in the delivery note and invoice must match.

The person who releases the goods puts his personal signature and the company seal on the delivery note. And the buyer also certifies the document with a signature and seal.

Why do you need a supporting document? Why is it important?

Supporting documents are mainly necessary to:

- It was possible to prove to the State Revenue Service that your company calculated taxes correctly.

- It was possible to prove to the transaction partner that your company delivered (transferred) goods, provided services, or paid for goods and services.

Every Latvian enterprise is required to maintain accounting records. To register (conduct) a transaction or event in accounting registers (books), you need a document that meets certain requirements, which confirms that the transaction took place or the event occurred. If a document does not meet certain requirements, then the accountant does not have the right to register such a document, even if the transaction took place. For example, a manager or employee of an enterprise in a store buys office supplies necessary for the activities of the enterprise. Payment in cash and the purchase amount excluding VAT exceeds 29 euros. The electronic cash register receipt does not contain information about the buyer. Unfortunately, there is no right to use such a document as an accounting source document and there is no right to register it in the accounting books. To resolve the situation, you need to attach, for example, a receipt (additional document) to the cash register receipt, where the necessary details are indicated.