Who needs to read the balance sheet and why?

A balance sheet is a basic accounting report that is only a few pages long.

There are no illustrations and little text; it is filled with many numbers. Nevertheless, the information hidden in the numbers brings a lot of benefits to those who know how to read it. This document is carefully studied by a huge number of people (managers and owners of companies, investors, bankers, tax authorities and other interested parties). The balance sheet is not a commercial secret, can be published in print for public viewing and is available to anyone.

You will find a line-by-line procedure for filling out a balance sheet with examples in the Guide from ConsultantPlus. If you do not already have access to this legal system, a full access trial is available for free.

Why read the balance sheet? The answer is obvious: to make the right financial decisions. And it doesn’t matter whether it is compiled in a traditional form or a simplified one - the usefulness of the information obtained from it does not decrease.

Read about who has the opportunity to prepare simplified reporting in this article.

Reading a balance sheet does not require higher financial education, but you cannot do without certain knowledge and techniques.

How to read a balance sheet

To be able to read means to know the basics of the alphabet. For financial statements, this basis is an understanding of the terms reflected on the balance sheet lines. Some of them are clear to many (for example, “fixed assets”, “inventories”, etc.), but some terms require additional explanation.

For example, deferred tax assets (DTA). The term ONA denotes a part of the income tax that is deferred in time: the income tax will be reduced by this amount in subsequent reporting periods (clause 14 of PBU 18/02, approved by order of the Ministry of Finance of Russia dated November 19, 2002 No. 114n). The reflection of IT in the first section of the balance sheet is due to the fact that for the company it is an asset, and its useful life is more than a year.

NOTE! Information about IT and IT (deferred tax liability) may not be shown on the balance sheet by companies that are classified as small (clause 2 of PBU 18/02).

You can find out more about how to apply PBU 18/02 from 2021 after changes have been made to it in the Ready-made solution from ConsultantPlus. Trial full access to the system can be obtained for free.

Or, for example, what does the phrase “cash equivalents” mean? This concept appeared on the balance sheet relatively recently and means highly liquid financial investments (demand deposits, short-term bills, etc.), which can quickly and easily be converted into money.

Thus, before you start reading the balance sheet, it is worth understanding what the indicators and its components are.

SOS package

Available for tariffs with a subscription fee. As soon as the account balance becomes negative, it turns on automatically and operates:

- on tariffs with a daily fee - within 1 day;

- on tariffs with a monthly fee - within 3 days.

It allows you to use the Yandex.Maps and Yandex.Navigator applications for free and, what is especially important for those who are left without communication, the WhatsApp messenger.

You can find out whether the “SOS package” is available to you in the description of the tariff you use on the website, as well as in your personal account on the website or in the My Tele2 mobile application.

Accounting for beginners from postings to balance sheet: reading a balance sheet using an example

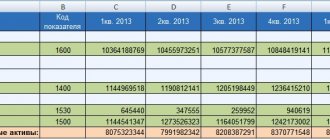

How to read a balance sheet using an example? Let's look at this using the data from the report of Prestige LLC.

| Indicator name | Line code | As of 12/31/2020 | As of 12/31/2019 | As of 12/31/2018 |

| I. NON-CURRENT ASSETS | ||||

| Fixed assets | 1150 | 750 | 779 | 810 |

| Financial investments | 1170 | 50 | – | – |

| II. CURRENT ASSETS | ||||

| Reserves | 1210 | 112 | 118 | 116 |

| Accounts receivable | 1230 | 56 | 49 | 51 |

| Cash and cash equivalents | 1250 | – | 10 | 12 |

| BALANCE | 1600 | 968 | 956 | 989 |

| III. CAPITAL AND RESERVES | ||||

| Authorized capital | 1310 | 10 | 10 | 10 |

| Reserve capital | 1360 | 4 | 3 | 2 |

| retained earnings | 1370 | 511 | 478 | 315 |

| V. SHORT-TERM LIABILITIES | ||||

| Accounts payable | 1520 | 443 | 465 | 662 |

| BALANCE | 1700 | 968 | 956 | 989 |

A fleeting glance at the balance sheet - and the first conclusions: the company does not apply PBU 18/02 - SHE and IT are absent from the balance sheet (perhaps the legal entity is related to a small business). The balance sheet currency has not changed sharply over the past 3 years (fluctuation 1–3%), no borrowed funds were attracted, profits grew steadily, which indicates the financial stability of the organization.

Attention - on the balance sheet asset

Basic asset principle: the lower the line, the faster the assets reflected in it can be converted into money (liquidity principle).

Among the assets, fixed assets turned out to be the most “heavy” - 77% of the balance sheet currency. It can be assumed that the company has significant overhead costs, and if sales volumes fall, it will be difficult for it to maintain its financial stability without borrowing funds.

A gradual decline in the indicators of the line “Fixed assets” (annually by 3–4%) may indicate that management is not investing in the modernization of production. As a result, demand for products may fall - they will be replaced by more advanced analogues of competitors. As a result, revenues and profits may decline.

Stable indicators in the “Inventories” line can confirm the good work of suppliers maintaining the necessary stock for production, or, conversely, indicate that there are unused raw materials and materials in warehouses.

An empty Cash and Cash Equivalents line should raise red flags, although an empty line does not always mean there is a complete shortage of cash. Perhaps financiers invested them profitably (the line “Financial investments” appeared), and soon you can expect good income (for example, in the form of interest).

For information on what conclusions an analysis of the movement of inventories can lead to, read the article “Analysis of the effectiveness of inventory management.”

Eight Types of Waste - Lean Six Sigma Tools

One of the most obvious ways to increase profits is to increase enterprise productivity. However, in the pursuit of productivity, top managers often forget that the amount of a product that consumers are willing to buy is determined by market demand.

Suddenly, a moment comes when a product that was so in short supply just yesterday accumulates in the warehouse (for some reason, such a moment always comes suddenly, regardless of whether we are talking about seasonal fluctuations in demand or changes in market conditions). Sales managers are forced to bend over backwards to sell stale or damaged goods.

What a profit! The costs would be compensated or, worse, to minimize losses! The strangest thing in all this is that this state of affairs is considered normal - the consumer, you can’t guess him! And it is considered normal to incur certain losses due to changes in demand (but on the wave of demand they made a big profit).

Is it possible to exclude such losses altogether? Can. And the solution to the problem is by no means as utopian as it might seem at first glance. What do you need:

- produce only on time and only what the client wants (in fact, work only “to order”);

- produce goods in small batches that are guaranteed to be sold (if demand falls, quickly switch to another type of product);

- to reduce losses during equipment changeovers, reduce changeover time to a minimum, making production in small batches profitable.

All this means that the time has come to forget about the profitability of large-scale production. Today's clients are demanding. They need variety. What, not profitable? Is it profitable to suffer losses due to storing illiquid assets, due to excessive consumption of raw materials, or due to problems with clients?

Loss 2: Transportation

Any more or less complex production is a sequence of operations to transform raw materials or semi-finished products into the final product. But all these materials need to be moved between operations. Procedures for moving valuables are present even in conveyor production. After all, you need to bring raw materials to the conveyor or take finished products to the warehouse.

Of course, transportation is an integral part of production, but unfortunately it does not create value at all, although it requires costs for fuel or electricity, for maintaining a transport fleet, for organizing transport infrastructure (roads, garages, overpasses, etc.). In addition, transportation is time consuming and risks damaging the product.

In order to reduce transportation losses, you should create a map of vehicle routes and conduct a thorough analysis of the feasibility of a particular movement.

After this, you should try to eliminate unnecessary transportation through redevelopment, redistribution of responsibility (so that you don’t have to travel through two workshops for the controller’s signature), eliminating remote stocks (stocks should be gotten rid of altogether, but if they are, let them be at hand), etc. P.

In addition, a system will not interfere in the matter of transportation: each movement of valuables must be justified by the appropriate regulatory document, and there is no amateur activity.

Loss 3: Waiting

Losses associated with waiting for the start of processing of material (parts, semi-finished products) indicate that the planning process and the production process are not coordinated with each other. This state of affairs is not uncommon for domestic enterprises. The planning process itself is quite complex, since it requires the analysis of a large number of factors. Such factors include: the structure of consumer orders, the state of the market for raw materials, equipment performance, shift schedule, etc.

Truly optimal planning requires serious mathematical training and refined interaction between sales, purchasing and production services. It is perhaps rare for any enterprise to be engaged in planning by a scientist who is able to systematize all the factors and find the best solution to the problem. As a rule, the planning process is pseudo-optimal in nature and is based on the subjective approach of people with some experience in production.

A priori, we can assume that there is always an opportunity to improve the planning process.

In addition to suboptimal planning, losses associated with waiting are significantly affected by uneven equipment throughput. In this case, a backlog of products awaiting processing may occur in front of the lowest throughput operation. The productivity of such operations should be improved. If this is not possible, flexible scheduling of equipment or redistribution of personnel between operations should be considered.

Loss 4: Inventory

There are probably few people who cannot answer the question - why are stocks bad? Inventories are frozen money, i.e. money taken out of circulation and losing its value. But for some reason, the presence of inventories in production is considered quite common, and most importantly, acceptable! After all, thanks to reserves, it is possible to compensate for surges in consumer demand.

Inventories allow the company to produce products during interruptions in the supply of raw materials. Finally, inventories help smooth out production flow. So is it possible to do without supplies if they are so useful? To answer this question, we need to look at the inventory problem from a different point of view.

Inventories seem to be needed, but: as already mentioned, inventories are frozen working capital;

- inventory needs maintenance (warehouse space, personnel, logistics, etc.);

- Inventories hide production problems: poor planning, strained relationships with suppliers, uneven production flow, etc.

In fact, inventories hide losses of other types, creating the impression of a prosperous production environment.

Loss 5: Defects

The release of products that do not meet consumer requirements entails obvious costs of raw materials, working time, labor, processing costs and disposal of defects. A traditional measure to reduce losses associated with the release of defective products is the organization of various control departments and services.

It is believed that such units must take timely measures to prevent the release of defects. Moreover, sometimes all responsibility for the marriage falls on the relevant services! But the fact that quality control services do not have the required leverage over production units is usually not taken into account.

It turns out that asking regulatory authorities is the same as treating the symptoms of a disease, and not its causes.

It is advisable to begin eliminating losses due to defective production by analyzing the effectiveness of the functioning of control units. This is not about finding out whether inspectors miss defects or not (this, of course, is also important). The main thing is to understand how much control services contribute to eliminating the causes of defective products. In any case, control is usually carried out only after the product has been manufactured. Consequently, inspectors do not have the opportunity to quickly influence the quality. The only way out of this situation is to integrate quality management procedures into the production process.

Loss 6: Overprocessing

As already mentioned, the consumer is willing to pay only for those properties of the product that are valuable to him. If a consumer needs, for example, a TV, then he expects to receive a product of appropriate quality, endowed with appropriate consumer properties for a certain price. Therefore, if you build, say, a holder for ski poles into a TV, while doubling the price, then it is not a fact that the TV will find its consumer. That's because the extra functionality doesn't add value to the TV. Another example.

If the consumer expects that the TV case should be black (white, silver, etc.), but you only have green plastic and after making the case you repaint it in the desired color - this is also a waste of unnecessary processing. After all, this requires time, people, equipment, paint, but the body, which really has value for the consumer, has already been manufactured. The losses of unnecessary processing should also include the maintenance of automatic equipment. For example, parts move along a conveyor that regularly stops due to their misalignment.

A special worker monitors the conveyor and corrects skewed parts. The labor of such a worker is also unnecessary processing.

Loss 7: Movement

Unnecessary movements that lead to losses could be called simply vanity, thereby emphasizing their unreasonableness and chaotic nature. From the outside, such movements may seem like a lot of activity, but upon closer inspection you will notice that, like the losses discussed earlier, they do not contribute to the creation of value for the consumer.

Secrets of the Balance Sheet Liability

In the liability, the lines are arranged in a special way: the lower the line, the faster the specified obligation must be returned (to counterparties, bankers, owners or other creditors).

The line “Retained earnings” shows an annual growth trend, but its rate has noticeably decreased (from 52 to 7%). Perhaps the effectiveness of managers has fallen, and therefore there is reason to think about the reasons. The presence and growth of reserve capital are assessed positively (the company's equity capital is strengthened).

The significant amount of short-term debts (46% of the balance sheet currency) is alarming. If this is arrears of wages and taxes, there is cause for concern: this is a sign of the company’s insolvency, and material losses are possible (sanctions for late payment).

Read about how such sanctions are calculated in this material.

Results

There are many ways to read a balance sheet. Some people trust only numbers: they calculate special coefficients, conduct horizontal and vertical analysis. But for some it is more important to research and compare different indicators and see how assets relate to liabilities and where reserves and losses are hidden. And to do this, you need to read the balance sheet with reference to other reports and explanations.

Each user builds a suitable methodology for himself and draws conclusions.

The main thing is to see the overall picture of the company’s property and financial position and, using all available methods of analysis, to correctly assess possible prospects and threats. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

***

Balance Sheet Analysis

helps to calculate the problem areas and directions of the company, to understand whether efforts need to be made to correct the situation, where positive trends should be maintained. Analytical work can be carried out either independently or using appropriate software.

Similar articles

- Increase in working capital: calculation

- Analysis of the structure of assets and liabilities of the balance sheet

- Assets on Balance Sheet

- Rules for filling out form No. 1 Balance sheet

- Conducting balance sheet liquidity analysis