Who is required to submit the Declaration and pay for the NVOS?

The declaration is submitted by tax payers. If your organization, in accordance with Federal Law No. 7-FZ, is not required to pay a fee for the tax assessment, then you do not need to submit a Declaration of payment for the tax assessment.

And yet, who is obliged to pay for the NVOS ? At the moment, we can say with confidence that the payers are legal entities and individual entrepreneurs carrying out economic activities on objects of categories I – III, and that objects of category IV are exempt from paying for the tax assessment. At the same time, business entities are exempt from paying for the disposal of municipal solid waste (MSW), the fee for which is paid by regional MSW management operators. In addition, it is possible for a number of waste disposal facilities (WDO) to obtain a decision from the territorial body

Rosprirodnadzor on eliminating negative impacts on the environment, allowing to reduce the amount of fees for the organization as a whole.

It would seem that we have gone through the procedure for registering NVOS objects, received a category and then everything, as in Federal Law No. 7-FZ, but not everything is so simple. Rosprirodnadzor has repeatedly clarified that calculations of fees for environmental impact assessment are not directly related to the definition of the facility providing environmental assessment, i.e. with registration of objects of the NVOS. Therefore, it is not yet clear what to do for objects that have been refused registration as not providing NVOS. The situation is aggravated by the fact that in 2016 there were no regional MSW management operators. Federal Law No. 486-FZ of December 28, 2016 “On Amendments to Certain Legislative Acts of the Russian Federation” established a transition period until January 1, 2019 for the introduction of public services for the management of solid waste and the establishment of a unified tariff on the territory of the constituent entities of the Russian Federation. Thus, until the date of approval of the unified tariff and the signing of agreements between the constituent entities of the Russian Federation and regional MSW operators, payment for the placement of MSW is carried out by business entities whose activities generate municipal solid waste.

What do we have as a result? With a high degree of probability, it can be argued that in 2021, all business entities must pay the fee for the 2021 IEE, regardless of the registration of IEE objects and the categories assigned to them. An exception may be small offices where the lease agreement clearly states that the payment for waste removal is paid by the lessor, who has entered into contracts for waste removal and is the payer of the fee for the NVOS.

Who is the payer of the tax collection fee?

Payers of the fee for negative environmental impact (NEI) are organizations and individual entrepreneurs that emit pollutants into the air through stationary sources, into water bodies or are engaged in the storage and burial (disposal) of waste (clause 1 of article 16, clause 1 Article 16.1 of the Law “On Environmental Protection” dated January 10, 2002 No. 7-FZ).

Decree of the Government of the Russian Federation dated September 18, 2020 No. 1496 contains a complete list of types of activities and other criteria for classifying objects into categories I–IV of environmental impact, in which the organization must pay for the environmental impact assessment. In particular, these include mining, metallurgical, chemical, food production, some agricultural companies, and municipal solid waste landfills.

If business activities are carried out only at category IV facilities, then there is no need to pay a fee for negative impact (Clause 1, Article 16.1 of Law No. 7-FZ).

Category IV includes facilities where:

- there are no releases of radioactive substances;

- there are no discharges of pollutants generated when water is used for industrial needs into sewers and the environment, surface and underground water bodies, as well as onto the earth's surface;

- there are discharges of pollutants resulting from the use of water for domestic needs;

- there are stationary sources of pollutant emissions, and their quantity is no more than 10 tons per year;

- There are only non-stationary sources of pollutant emissions.

Thus, the use of motor transport in business activities does not lead to the need to pay for negative impacts, since payment is made only for stationary objects, to which it (motor transport) does not apply (Clause 1, Article 16 of Law No. 7-FZ).

IMPORTANT! The obligation to pay the fee does not depend on the tax regime applied by organizations or individual entrepreneurs that are payers of the fee for negative impact, as well as on whether activities are carried out at their own or leased facilities that lead to a negative impact on the environment.

Payers of the fee must submit an application to Rosprirodnadzor for each polluting facility and receive a certificate of registration indicating the polluting category from I to IV.

IMPORTANT! If the process of activity generates only production and consumption waste and there are no other negative impacts, then an application for registration under the NVOS is not submitted (letters of Rosprirodnadzor dated 02.21.2017 No. AS-06-02-36/3591, dated 10.31.2016 No. AS -09-00-36/22354). Since when carrying out trading activities and providing services, the functioning of offices, schools, kindergartens, administrative buildings, clinics, hospitals, etc., as a rule, only production and consumption waste is generated, we can conclude that registering with them there is no need to act as a payer of the Taxpayer Tax.

Payment for negative impact on the environment should not be confused with an environmental fee. These are different payments. You can read about the differences here.

Declaration form and electronic submission to the Rosprirodnadzor portal?

On February 22, 2021, Order of the Ministry of Natural Resources dated January 09, 2017 No. 3 “On approval of the Procedure for submitting a declaration on payment for negative impact on the environment and its forms” was registered with the Ministry of Justice and published, i.e. came into force.

The fee for the IEE must be paid no later than March 1 . Starting from 2021, a penalty in the amount of 1/300 of the key rate of the Bank of Russia .

The fee is paid separately for four environmental components: emission fee, APG emission fee, discharge fee and waste disposal fee. Each with its own BCC (budget classification code). It should be taken into account that if advance payments were made and, for example, there was an overpayment for waste, then it cannot be automatically included in the payment for emissions, because These components are paid according to different BCCs. The calculated total amounts of the fee for payment for the reporting period (lines 151 - 154 of the Declaration) are subject to payment; the amounts of the fee for return and/or offset (lines 161 - 164) should not affect the amount of the current payment .

Order of the Ministry of Natural Resources No. 3 determines the form of the Declaration itself, which must be submitted no later than March 10 .

The declaration can be submitted on paper or in the form of an electronic document. Starting from 01/01/2017, the Rosprirodnadzor portal pnv-rpn.ru stopped accepting reports; it will only be available for viewing previously submitted reports until 06/30/2017. Now the State Services portal located at lk.fsrpn.ru is used to receive reports. To submit reports, you must have an account on the State Services portal.

SME: environmental report (due date)

SMEs in each region may have their own deadlines for receiving the report. Also remember that waste supervision in one region can be carried out by several authorities, depending on the location and importance of the facility, and it is likely that the enterprise will have to submit reports on several facilities to different departments and on different dates.

Initially, the deadline for submitting the SME report to Rosprirodnadzor was established by order of the Ministry of Natural Resources and Environment dated February 16, 2010 No. 30:

- until January 15 of the year following the year in which the waste was generated and moved (clause 5 of the Report Submission Procedure).

This period is valid, for example, for all objects located in Moscow, as well as for objects of federal significance located in the Moscow region, which are supervised by the regional Ministry of Ecology (Order of the Moscow Government dated December 23, 2014 No. 487). At the same time, for all other facilities located in the Moscow region, the deadline for submitting the SME report in 2021 is set until February 20 (Order of the Ministry of Ecology of the Moscow Region dated 02/05/2016 No. 80-RM).

In a number of other constituent entities of the Russian Federation, the time for submitting a report may be even longer. Thus, in the Republic of Tatarstan, St. Petersburg and the Leningrad Region, SMEs’ reports on facilities located in these territories are submitted before March 1 - this is precisely the deadline established by regional regulations.

When to submit the SME report in 2021, if similar documents have not been issued at the regional level? In this case, representatives of small and medium-sized businesses should focus on the provisions approved by Order of the Ministry of Natural Resources of the Russian Federation dated February 16, 2010 No. 30 and submit the SME report to Rosprirodnadzor before January 15, considering January 14 as the last day of the deadline.

Please note that the Procedure for Submitting a Report for SMEs does not provide for the postponement of the deadline if it coincides with a non-working day. From which it follows that for organizations and entrepreneurs submitting an SME environmental report before January 15, the deadline for submission for 2021 will last no longer than until January 12, 2018 inclusive, since the 13th and 14th fall on weekends.

We can't find fee rates for pollutants

New payment rates were approved by Resolution No. 913, which brings the rates into line with the Order of the Government of the Russian Federation dated 06/08/2015 No. 1316-r “On approval of the list of pollutants for which state regulatory measures in the field of the environment are applied.”

The currently available permits for emissions and discharges were issued without taking into account Order No. 1316-r, which significantly reduces the list of pollutants and, as a consequence, the payment rates for them. For emissions and discharges of pollutants for which there are no payment rates, starting in 2021, you do not need to pay, even if these pollutants are indicated in the permits.

The current practice of using fee rates for pollutants with similar characteristics is unlawful . Thus, in the Letter of Rosprirodnadzor dated January 16, 2017 N AS-03-01-31/502 “On consideration of the appeal” it was said that “...substances such as abrasive dust, carbon (soot), iron oxide, due to their physical properties , related to solid particles, it is advisable to take into account the emissions as suspended substances.” This and the requirements previously applied by the administrators of the fee for the NVOS to pay for pollutants that are not in Resolution No. 344 are recognized by the courts as illegal. As an example, we can cite the decision of the Arbitration Court of the Khanty-Mansiysk Autonomous Okrug dated January 31, 2014 in case No. A75-2131/2013.

Where can I get maximum permissible values and VAT for sources of emissions and discharges?

The new form of the annual Declaration provides for calculations of pollutants in the context of emission sources and wastewater discharges. This significantly increases the amount of work involved in calculating the fee. In addition, we needed MPE, VAT and VAT, VSS of pollutants for each source and release separately. The permitting documentation approves the data for the facility as a whole. To obtain data in the context of sources and releases, you need to raise the project documentation, namely the standardization section.

How to calculate relief to relief?

People still ask how relief is calculated. The fee for the so-called stormwater drainage system was canceled back in 2014 (or rather, it was never approved and its application was unlawful). The discharge of wastewater is regulated by legal acts that define the relationship between subscribers and water supply and sewerage organizations (WSS) and water utilities. The methodological instructions of V.I. Danilov - Danilyan for calculating fees for unorganized discharge of pollutants into water bodies are not currently used. Payment must be made only for the discharge of pollutants and microorganisms into water bodies .

How to fill out the form, example of filling

Calculation of the amount to be contributed to the budget

Calculation of the amount to be contributed to the budget includes indicators of payment amounts, including by type, for each facility providing NVOS. This declaration sheet is filled out for each municipality separately. When filling out, you must indicate the serial number of the page.

Line 010 indicates the code of the corresponding municipality - OK.

Line 020 is general. It indicates the total amount of payments, without taking into account adjustments to their size. The indicator is defined as the amount of fees for all types of tax assessments and includes payments calculated:

- within the limits of permissible emissions standards (APE),

- permissible discharge standards (VAT),

- limits on emissions of pollutants and limits on discharges of pollutants exceeding such standards, limits, emissions and discharges (including emergency),

- within the limits for the disposal of production and consumption waste and above the specified limits.

The fee for each type of NVOS is determined as the amount of the fee for each pollutant for which the rate is established.

The amount for line 020 in the table is determined in the following order: line 020 = line 021 + line 022 + line 023 + line 024

Lines 021, 022, 023 and 024 indicate the components of the payment amount by type of tax assessment, the values of which are taken equal to the value of the indicator of the corresponding line:

- page 021 = page 040

- page 022 = page 060

- page 023 = page 080

- page 024 = page 100

Line 031 indicates OKTMO of stationary sources specified in Section 1 “Calculation of the amount of payment for a negative impact facility for emissions of pollutants into the air by stationary facilities.”

Line 040 reflects the amount of payment for emissions of pollutants into the air by stationary objects, calculated for each stationary source, without adjusting its size.

The amount for line 040 in the table is determined in the following order: line 040 = line 041 + line 042 + line 043 .

indicator 040 = total according to column 17 of Section 1, line “Total for stationary sources”.

Indicators on lines 041, 042 and 043 are decipherable to the amount reflected on line 040 . All data for filling them out is contained in Section 1.

Line 041 reflects the amount of payment for emissions within the maximum permissible limit; the amount must correspond to the total in column 14 of Section 1, line “Total for stationary sources.”

Line 042 reflects the amount of payment for emissions within the limits for emissions of pollutants (VER), the amount must correspond to the total in column 15 of Section 1, line “Total for stationary sources”.

Line 043 reflects the amount of payment for emissions in excess of the emission limit; the amount must correspond to the total in column 16 of Section 1, line “Total for stationary sources.”

Other lines of the Calculation are filled in similarly. Each indicator must correspond to the total amounts of calculations for the corresponding Section.

Lines 060 to 063 reflect the amounts of fees for emissions of pollutants during flaring and/or dispersion of associated petroleum gas, calculated for all stationary sources (flares, dispersion installations).

The data to be filled out is contained in Section 1.1 “Calculation of the amount of payment for an object of negative impact for emissions of pollutants into the atmosphere during flaring and (or) dispersion of associated petroleum gas without exceeding the volume corresponding to the maximum permissible value of the combustion indicator” and Section 1.2. “Calculation of the amount of payment for an object of negative impact for emissions of pollutants into the atmospheric air during flaring and (or) dispersion of associated petroleum gas when the volume corresponding to the maximum permissible value of the combustion indicator is exceeded.”

page 060 = page 061 + page 062 + page 063.

Amount for line 060 = total for column No. 17 of Section 1.1 + total for column No. 12 of Section 1.2.

Amount for line 061 = total for column No. 14 of Section 1.1.

Amount for line 062 = total for column No. 15 of Section 1.1.

Amount for line 063 = total for column No. 16 of Section 1.1 + total for column No. 8 of Section 1.2.

Lines 080, 081, 082, 083 reflect the amounts of fees for discharges of pollutants into water bodies, calculated for each release. The data to be filled out is contained in Section 2 “Calculation of the amount of payment for an object of negative impact for the discharge of pollutants into water bodies.”

page 080 = page 081 + page 082 + page 083.

Amount for line 080 = total for column No. 18 of Section 2, line “Total for all issues.”

Amount for line 081 = total for column No. 15 of Section 2, line “Total for all issues.”

Amount for line 082 = total for column No. 16 of Section 2, line “Total for all issues.”

Amount for line 083 = total for column No. 17 of Section 2, line “Total for all issues.”

Lines 100, 101, 102 indicate the entire amount of the fee for waste disposal. The data to be filled out is contained in Section 3 “Calculation of the fee amount for the disposal of production and consumption waste” and Section 3.1 “Calculation of the fee amount for the disposal of municipal solid waste”.

page 100 = page 101 + page 102.

Total for line 100 = total for column No. 25 of Section 3 + total for column No. 8 of Section 3.1.

Total for line 101 = total for column No. 23 of Section 3.

Total for line 102 = total for column No. 24 of Section 3.

Lines 110, 111, 112, 113, 114 indicate the amounts of funds for environmental protection measures (the amount of adjustment of the fee planned for offset) as part of emission reduction plans, discharge reduction plans and/or for the implementation of projects for the beneficial use of associated petroleum gas, which is taken into account when adjusting the size of the fee.

page 110 = page 111 + page 112 + page 113 + page 114.

Line 111 indicates the amount of funds for the implementation of environmental protection measures as part of emission reduction plans, which is accepted for credit when adjusting fees for emissions of specific pollutants by stationary facilities (excluding flare combustion plants and sources of dispersion of associated petroleum gas).

The amount is determined based on documents and calculations confirming the actual use of funds for environmental protection measures that are included in emission reduction plans.

Line 112 indicates the amount of funds for the implementation of projects that reduce flaring and dispersion of associated petroleum gas, which is taken into account when adjusting the payment for pollutant emissions during flaring and dispersion of associated petroleum gas.

The amount is determined based on documents/calculations confirming the actual disbursement of funds for the implementation of activities that are included in the project for the beneficial use of associated petroleum gas.

Line 113 indicates the amount of funds for environmental protection measures as part of discharge reduction plans, which is accepted for credit when adjusting fees for discharges of specific pollutants.

The amount is determined based on documents/calculations confirming the actual use of funds for environmental protection measures that are included in the discharge reduction plans.

Line 114 indicates the amount of funds for the implementation of environmental protection measures as part of an environmental action plan or an environmental efficiency improvement program, which is accepted for credit when adjusting the fee for the disposal of waste of a particular hazard class.

The amount is determined based on documents/calculations confirming the actual use of funds for environmental protection measures that are included in plans for reducing emissions and discharges.

Lines 120, 121, 122, 123, 124 indicate the amount of the fee, taking into account the adjustment of its size to the actual costs of implementing environmental protection measures as part of plans to reduce emissions and discharges and/or for the implementation of projects for the beneficial use of associated petroleum gas.

page 120 = page 121 + page 122 + page 123 + page 124.

Line 121 indicates the amount of payment for emissions of specific pollutants by stationary facilities (excluding flares and sources of dispersion of associated petroleum gas), the reduction of the negative impact of which on the environment is carried out through the implementation of environmental protection measures as part of plans to reduce emissions and discharges.

Line 121 = total for column 17 of Section 1, line “Total for all stationary sources for those pollutants for which the fee is adjusted.”

Line 122 indicates the amount of payment for emissions of pollutants when flaring (dispersing) associated petroleum gas, the reduction of the negative impact of which on the environment is associated with a reduction in the flaring of associated petroleum gas through the implementation of relevant projects.

Line 122 = line 022 - amount of payment for emissions in the absence of measuring instruments*

*Meeting the requirements established by the Ministry of Energy of the Russian Federation, measuring the volume of associated petroleum gas actually produced and flared and/or dispersed.

Line 123 indicates the amount of payment for discharges of specific pollutants, the reduction of the negative impact of which on the environment is carried out through the implementation of environmental protection measures as part of discharge reduction plans.

Line 123 = total for column No. 18 of Section 2 for the line “Total for all releases for those pollutants for which the fee is adjusted.”

Line 124 indicates the amount of payment for the disposal of specific types (hazard classes) of waste, the reduction of the negative impact on the environment is carried out through the implementation of environmental measures as part of an environmental action plan or an environmental efficiency improvement program.

Line 124 = the sum of the data on the corresponding lines for specific types (hazard classes) of waste in column 25 of the tables of Section 3 or the sum of the data on the corresponding lines for specific types (hazard classes) of waste in column 25 on the line “Total, including” for Section 3 in in general.

Line 130 indicates the amount of fees payable to the budget system for all types of negative impact on the environment.

page 130 = page 131 + page 132 + page 133 + page 134

page 130 = page 020 – page 110 with page 120≥ page 110

or

page 130 = page 020 – page 120 with page 120 ≤ page 110

Line 131 indicates the amount of payment for emissions of pollutants by stationary facilities to be entered into the budget system.

page 131 = page 040 – page 111 with page 121≥ page 111

or

page 131 = page 040 – page 121 with page 121 ≤ page 111

Line 132 indicates the amount of payment to be made to the budget system for emissions of pollutants during flaring and dispersion of associated petroleum gas.

page 132 = page 060 – page 112 when page 122 ≥ page 112

or

page 132 = page 060 – Section 1.2 (TOTAL for column 8 – TOTAL for column 12).

Line 133 indicates the amount of payment to be entered into the budget system for discharges of pollutants into water bodies.

page 133 = page 080 – page 113 at page 123 ≥ at page 113

or

page 133 = page 080 – page 123 with page 123 ≤ page 113

Line 134 indicates the amount of payment for waste disposal to be entered into the budget system.

page 134 = page 100 – page 114 when page 124 ≥ page 114

or

page 134 = page 100 – page 124 with page 124 ≤ page 114

Line 140 indicates the amount of advance quarterly payments made in the reporting period to the budget system for all types of negative impact on the environment and for each quarter separately.

page 140 = page 141 + page 142 + page 143 + page 144

Line 141 indicates the amount of quarterly advances for emissions of pollutants by stationary facilities.

Line 141 = the sum of the values for the lines “1st quarter”, “2nd quarter”, “3rd quarter”, which are accepted in accordance with the amounts of advances specified in payment orders for their transfer.

Line 142 indicates the amount of quarterly advances for emissions of pollutants during flaring and/or dispersion of associated petroleum gas.

Line 142 = the sum of the values for the lines “1st quarter”, “2nd quarter”, “3rd quarter”, which are accepted in accordance with the amounts of advances specified in payment orders.

Line 143 indicates the amount of quarterly advances for discharges of pollutants into water bodies.

Line 143 = the sum of the values for the lines “1st quarter”, “2nd quarter”, “3rd quarter”, which are accepted in accordance with the amounts of advances specified in payment orders.

Line 144 indicates the amount of quarterly advances for waste disposal.

Line 144 = the sum of the values for the lines “1st quarter”, “2nd quarter”, “3rd quarter”, which are accepted in accordance with the amounts of advances specified in payment orders.

Line 150 indicates the amount of quarterly advances for all types of negative impact on the environment.

page 150 = page 151 + page 152 + page 153 + page 154

page 150 = page 130 – page 140 with page 130 ≥ page 140

Line 151 indicates the total amount of payment for emissions of pollutants by stationary facilities.

page 151 = page 131 page 141 when page 131 ≥ page 141

Line 152 indicates the total amount of payment for emissions of pollutants during flaring and (or) dispersion of associated petroleum gas.

page 152 = page 132 page 142 when page 132 ≥ page 142

Line 153 indicates the total amount of payment for discharges of pollutants into water bodies.

page 153 = page 133 page 143 when page 133 ≥ page 143

Line 154 indicates the total amount of the fee for waste disposal.

page 154 = page 134 page 144 when page 134 ≥ page 144

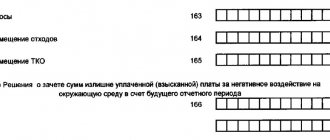

Line 160 indicates the total amount of the fee for the reporting period for refund from the budget or offset against the subsequent reporting period for all types of negative impact on the environment.

page 160 = page 161 + page 162 + page 163 + page 164

line 160 indicator is checked in the following order:

page 160 = page 140 – page 130 when page 140 ≥ page 130

Line 161 indicates the total amount of payment for the emissions of pollutants by stationary facilities for the reporting period for return from the budget or offset against the subsequent reporting period.

page 161 = page 141 page 131 when page 141 ≥ page 131

Line 162 indicates the total amount for the reporting period for return from the budget or offset against the subsequent reporting period, the amount of payment for emissions of pollutants during flaring and dispersion of associated petroleum gas.

page 162 = page 142 page 132 when page 142 ≥ page 132

Line 163 indicates the total amount of payment for the discharge of pollutants into water bodies for the reporting period for return from the budget or offset against the subsequent reporting period.

page 163 = page 143 page 133 when page 143 ≥ page 133

Line 164 indicates the total amount of payment for waste disposal for the reporting period for return from the budget or offset against the subsequent reporting period.

page 164 = page 144 page 134 when page 144 ≥ page 134

Procedure for payment for negative impact

Based on the results of the calculations given in the section of the declaration reflecting the adjustment of the calculated fee values, the amount is paid at the end of the year. That is, its value is determined as the total amount of the fee for the year minus the costs of measures to reduce the negative impact and advances paid. Such payment must be made before March 1 of the year following the reporting year (Clause 3, Article 16.4 of Law No. 7-FZ of January 10, 2002).

Based on the total amount of payment for negative impact made in 2021, the amount of advance payments for 2021 can be determined. The amount of each of them can be equal to ¼ of the total amount of the negative impact fee actually paid for 2021.

But this is only one way to pay advances. From 2021 they can also be determined:

- in the amount of 1/4 of the fee calculated based on the volume or mass of emissions (discharges) of pollutants within the limits of standards, temporarily permitted emissions (discharges) or limits on the disposal of production and consumption waste;

- by multiplying the payment base, which is determined on the basis of industrial environmental control data on the volume or mass of emissions (discharges) or the mass of disposed production and consumption waste in the previous quarter, by the corresponding payment rates for environmental waste using the coefficients provided by law.

Advance payments are made 3 times a year, at the end of each of the first three quarters of the year, no later than the 20th day of the month following the next quarter.

IMPORTANT! Small businesses do not pay advance payments (Clause 3, Article 16.4 of Law No. 7-FZ).

Payment for negative environmental impact is carried out according to the following BCC:

| Payment name | KBC in 2020-2021 |

| Payment for emissions of pollutants into the atmospheric air by stationary facilities, with the exception of those generated during flaring and (or) dispersion of associated petroleum gas | 048 1 1200 120 |

| Payment for discharges of pollutants into water bodies | 048 1 1200 120 |

| Fee for disposal of industrial waste | 048 1 1200 120 |

| Fee for disposal of municipal solid waste | 048 1 1200 120 |

| Payment for emissions of pollutants generated during flaring and (or) dispersion of associated petroleum gas | 048 1 1200 120 |

As of 09/07/2019, the procedure for offset or return of overpayments under the Tax Inspectorate, as well as the forms of documents required for this, have been determined. There were problems with this before this date.

Violation of payment deadlines for negative impacts will result in an administrative fine. For organizations it varies from 50,000 to 100,000 rubles, and for officials - from 3,000 to 6,000 rubles. (Article 8.41 of the Code of Administrative Offenses of the Russian Federation).