Who is the payer of the tax collection fee?

Payers of the fee for negative environmental impact (NEI) are organizations and individual entrepreneurs that emit pollutants into the air through stationary sources, into water bodies or are engaged in the storage and burial (disposal) of waste (clause 1 of article 16, clause 1 Article 16.1 of the Law “On Environmental Protection” dated January 10, 2002 No. 7-FZ).

Decree of the Government of the Russian Federation dated September 18, 2020 No. 1496 contains a complete list of types of activities and other criteria for classifying objects into categories I–IV of environmental impact, in which the organization must pay for the environmental impact assessment. In particular, these include mining, metallurgical, chemical, food production, some agricultural companies, and municipal solid waste landfills.

If business activities are carried out only at category IV facilities, then there is no need to pay a fee for negative impact (Clause 1, Article 16.1 of Law No. 7-FZ).

Category IV includes facilities where:

- there are no releases of radioactive substances;

- there are no discharges of pollutants generated when water is used for industrial needs into sewers and the environment, surface and underground water bodies, as well as onto the earth's surface;

- there are discharges of pollutants resulting from the use of water for domestic needs;

- there are stationary sources of pollutant emissions, and their quantity is no more than 10 tons per year;

- There are only non-stationary sources of pollutant emissions.

Thus, the use of motor transport in business activities does not lead to the need to pay for negative impacts, since payment is made only for stationary objects, to which it (motor transport) does not apply (Clause 1, Article 16 of Law No. 7-FZ).

IMPORTANT! The obligation to pay the fee does not depend on the tax regime applied by organizations or individual entrepreneurs that are payers of the fee for negative impact, as well as on whether activities are carried out at their own or leased facilities that lead to a negative impact on the environment.

Payers of the fee must submit an application to Rosprirodnadzor for each polluting facility and receive a certificate of registration indicating the polluting category from I to IV.

IMPORTANT! If the process of activity generates only production and consumption waste and there are no other negative impacts, then an application for registration under the NVOS is not submitted (letters of Rosprirodnadzor dated 02.21.2017 No. AS-06-02-36/3591, dated 10.31.2016 No. AS -09-00-36/22354). Since when carrying out trading activities and providing services, the functioning of offices, schools, kindergartens, administrative buildings, clinics, hospitals, etc., as a rule, only production and consumption waste is generated, we can conclude that registering with them there is no need to act as a payer of the Taxpayer Tax.

Payment for negative impact on the environment should not be confused with an environmental fee. These are different payments. You can read about the differences here.

Data on which fee calculation is based

Calculation of fees for negative impact on the environment (or fees for pollution) depends on many factors:

- nature of the source of pollution;

- type of pollutant (or its hazard class);

- volumes of actual emissions;

- the fact that there are no means of measuring emissions;

- presence of excess pollution above established standards;

- the fact that the contaminated object or territory is under special protection;

- expenses incurred on measures to reduce negative impacts.

Based on the first 2 indicators, the rate used in the calculation is determined. By multiplying it by the volume of actual emissions (if it does not exceed the maximum permissible) the amount of payment for pollution is determined. The following odds are applied to the bet amount:

- increasing, if we are talking about the lack of means of measuring emissions, exceeding permissible pollution standards, or the location of an object (territory) under special protection;

- reducing, depending on the hazard class of the disposed waste, the method of its generation and disposal.

The maximum multiplying factor (120) may arise in a situation where there are no means to measure volumes. Exceeding the standards leads to the application of coefficients equal to 5 (if the excess occurs during the period of planned reduction of discharges) or 25. For an object (territory) under special protection, a coefficient of 2 applies.

The specific size of the reduction factor can be determined by a combination of factors influencing it and range from 0 to 0.67.

The presence of expenses for measures to reduce negative impacts allows you to reduce the amount of accrued fees.

Also, the amount of amounts payable at the end of the year is influenced by the fact that advances on pollution payments were transferred during the year.

Rates applied for calculation for 2021

The rates used to calculate pollution charges are established by Decree of the Government of the Russian Federation dated September 13, 2016 No. 913 (as amended on January 24, 2020). It shows rates for 2016-2018. And in 2021, the rates of 2021 are applied with a coefficient of 1.08 (Resolution of the Government of the Russian Federation dated September 11, 2020 No. 1393).

ConsultantPlus experts explained how to calculate the fee for the NVOS at the end of the year. To do everything correctly, get trial access to the system and go to the Ready solution. It's free.

Depending on the type of polluting object, they are divided into 3 groups related to objects:

- stationary, producing emissions into the atmosphere;

- those carrying out discharges into water bodies;

- producing production and consumption waste.

For the first 2 groups, specific rates are indicated in relation to each of the names of the pollutant. For waste, the rate is tied to a specific hazard class.

In order to encourage legal entities and individual entrepreneurs to take measures to reduce the negative impact on the environment and introduce the best available technologies, when calculating fees for environmental assessments, the coefficients specified in paragraphs are applied to the rates of such fees. 5 (from 2020) and 6 tbsp. 16.3 of Law No. 7-FZ.

On the return of overpaid funds for NVOS

In an information message, Rosprirodnadzor reminded organizations and individual entrepreneurs that currently the procedure for returning overpaid funds for negative impacts on the environment is not established by current legislation.

At the same time, the department notes: in order to confirm overpaid amounts, it is necessary to reconcile the calculations for the payment for the tax assessment.

The specified reconciliation of calculations should be carried out as part of the consideration of the Declaration of payment for the NVOS for 2021, based on the results of which an act will be drawn up.

At the same time, according to the norms of Resolution No. 255, control over the calculation of fees for environmental impact assessment is carried out by Rosprirodnadzor within 9 months from the day the declaration on payment for environmental assessment was submitted.

In a letter dated March 27, 2017 No. AA-06-02-36/6198, Rosprodnadzor provided the forms of documents relating to the administration of fees for NVOS:

- requirements for additional charges and payment;

- act of monitoring the calculation of fees;

- requirements for providing explanations and (or) making corrections to the declaration of payment for the tax assessment;

- requirements for the submission of documents confirming the actual expenses incurred for the implementation of measures to reduce the negative impact on the environment and measures to ensure the use and utilization of associated petroleum gas;

- applications for credit and refund of overpaid fees;

- decisions to refuse credit and return of overpaid amounts;

- applications for a joint reconciliation of calculations of the amounts of fees for the NVOS;

- act of reconciliation of calculations of payment amounts for the new tax assessment;

- decisions on offset and return of overpaid amounts of fees for the NVOS.

The specified document forms are recommended for use, but are not mandatory.

Let us remind you that in 1C programs the NVOS declaration with the ability to upload in 1.7 format is implemented. An example of filling out the Declaration of Fee for Environmental Impact Assessment for 2021 can be found in the article “Declaration of Fee for Negative Environmental Impact for 2021: Example of Filling Out”.

Reporting form and deadlines for submission

The entire procedure for calculating pollution fees is reflected in the declaration, issued once a year, upon its completion. For 2020, this report is compiled according to the form approved by Order of the Ministry of Natural Resources of Russia dated December 10, 2020 No. 1043 (Appendix No. 2).

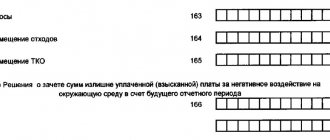

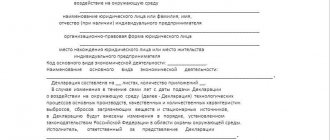

The declaration consists of:

- from the title page reflecting information about the reporting entity;

- section in which the final calculated amounts of payments generated by sections are combined into a single amount, which is successively adjusted to the values to be paid or returned to the payer by taking into account the costs of measures to reduce the negative impact and advances paid;

- three sections, separated by the main types of pollution sources, in which, in fact, the calculation of payments for each source is carried out.

The tables of sections intended for calculation provide for the reflection in them of all the data necessary for calculating the amount of the board:

- permissible and actual volumes with the allocation of excess amounts;

- rates;

- applied coefficients;

- components of the calculated amount of the fee and its final value.

Each of the sections allocated depending on the type of pollution source is completed only if the reporting person has the data for this.

The rules that should be followed when entering information into the declaration are set out in detail in the text of the order of the Ministry of Natural Resources of Russia dated December 10, 2020 No. 1043, in the notes to the form of the form approved by it. In them you can also find the values of the necessary coefficients and ways to check the correctness of data entry for each section. In addition, the calculation procedure for each type of polluting object is described in detail in Decree of the Government of the Russian Federation dated March 3, 2017 No. 255.

For step-by-step instructions on filling out the declaration, see ConsultantPlus. Get free demo access to K+ and go to the Ready Solution to find out all the details of this procedure.

The deadline for submitting the declaration is established by clause 5 of Art. 16.4 of the Law “On Environmental Protection” dated January 10, 2002 No. 7-FZ. Its deadline is defined as March 10 of the year following the reporting year. In 2021, this is a working day, so no questions will arise with the deadline for submitting the declaration for 2021. But if this day falls on a weekend, you need to take into account that Law No. 7-FZ does not establish the possibility of postponing the deadline. Therefore, you need to submit the declaration the day before. For example, this was the case in 2021. March 10 was a Sunday, and the Friday before was a non-working holiday (March 8). Therefore, reporting for 2021 should have been done no later than Thursday, 03/07/2019.

Errors made in the submitted declaration and identified by the payer himself can be corrected by him by submitting an adjusted report. But this can be done without consequences only before the deadline set for submitting the original declaration expires, that is, until March 10. Therefore, you should not postpone reporting until the last few days.

You can learn how to submit an updated declaration on payment for negative environmental impact from the Ready-made solution from K+ experts. Get free trial access to the system and proceed to recommendations.

When do you need to pay?

As for the timing of payment, if previously this fee was collected once a quarter, recently it has become annual, and it must be paid before March 1 of the following billing year. That is, the fee for 2021 will need to be paid before March 1, 2018.

It has become clear that the existing fee must now be paid once a year. As is clear from the principle of calculating the fee, its meaning is not only to finance the state’s environmental measures to restore nature from the economic activities of citizens and factories associated with environmental pollution, but also to generally limit such activities, especially in those places where it is extremely undesirable, be it environmentally unfavorable regions or individual territories that have received the status of environmental protection zones. Wanting to conduct some kind of activity in such places, an entrepreneur will have to take measures to ensure that the damage from his activities is as small as possible, and that protective equipment and filters are as modern and perfect as possible. Sometimes this can be cheaper than paying fees and fines for causing damage to nature.

One of the responsibilities of a responsible state is to protect the natural heritage and pass on to descendants a more or less clean country, in which living will be pleasant and not harmful to health.

Procedure for payment for negative impact

Based on the results of the calculations given in the section of the declaration reflecting the adjustment of the calculated fee values, the amount is paid at the end of the year. That is, its value is determined as the total amount of the fee for the year minus the costs of measures to reduce the negative impact and advances paid. Such payment must be made before March 1 of the year following the reporting year (Clause 3, Article 16.4 of Law No. 7-FZ of January 10, 2002).

Based on the total amount of payment for negative impact made in 2021, the amount of advance payments for 2021 can be determined. The amount of each of them can be equal to ¼ of the total amount of the negative impact fee actually paid for 2021.

But this is only one way to pay advances. From 2021 they can also be determined:

- in the amount of 1/4 of the fee calculated based on the volume or mass of emissions (discharges) of pollutants within the limits of standards, temporarily permitted emissions (discharges) or limits on the disposal of production and consumption waste;

- by multiplying the payment base, which is determined on the basis of industrial environmental control data on the volume or mass of emissions (discharges) or the mass of disposed production and consumption waste in the previous quarter, by the corresponding payment rates for environmental waste using the coefficients provided by law.

Advance payments are made 3 times a year, at the end of each of the first three quarters of the year, no later than the 20th day of the month following the next quarter.

IMPORTANT! Small businesses do not pay advance payments (Clause 3, Article 16.4 of Law No. 7-FZ).

Payment for negative environmental impact is carried out according to the following BCC:

| Payment name | KBC in 2020-2021 |

| Payment for emissions of pollutants into the atmospheric air by stationary facilities, with the exception of those generated during flaring and (or) dispersion of associated petroleum gas | 048 1 1200 120 |

| Payment for discharges of pollutants into water bodies | 048 1 1200 120 |

| Fee for disposal of industrial waste | 048 1 1200 120 |

| Fee for disposal of municipal solid waste | 048 1 1200 120 |

| Payment for emissions of pollutants generated during flaring and (or) dispersion of associated petroleum gas | 048 1 1200 120 |

As of 09/07/2019, the procedure for offset or return of overpayments under the Tax Inspectorate, as well as the forms of documents required for this, have been determined. There were problems with this before this date.

Violation of payment deadlines for negative impacts will result in an administrative fine. For organizations it varies from 50,000 to 100,000 rubles, and for officials - from 3,000 to 6,000 rubles. (Article 8.41 of the Code of Administrative Offenses of the Russian Federation).

Payment for NVOS: new rules for calculation and payment for the 2nd quarter. 2021

Persons obliged to pay a fee for negative environmental impact (NEI), with the exception of small and medium-sized businesses, must pay quarterly advance payments (except for the fourth quarter) no later than the 20th day of the month following the last month of the corresponding quarter. The deadline for paying taxes for the second quarter of 2021 expires on July 20. 1C experts have prepared a review of current materials—regulatory legal acts, letters from Rosprirodnadzor, bills—concerning the rules for calculating and paying fees for NVOS.

Calculation of fees negative impact of the new rules

By Resolution No. 255 of 03.03.2021, the Government of the Russian Federation approved new rules for calculating and collecting fees for negative impacts on the environment. At the same time, the previously existing rules, approved. Decree of the Government of the Russian Federation dated August 28, 1998 No. 632.

The new Rules take into account the changes (which entered into force on 01/01/2021) that were made to Federal Laws dated 01/10/2002 No. 7-FZ “On Environmental Protection”, dated 06/24/1998 No. 89-FZ “On Production and Consumption Waste” regarding payment for negative impact on the environment, and specify the provisions of these laws.

Note:

* All materials on changes to legislation on environmental impact assessments can be found in the section “Environmental payments, reporting to Rosprirodnadzor”.

The rules are in force from 03/17/2021, but apply to legal relations that arose from 01/01/2021 (clause 3 of Resolution No. 255). Thus, they must be taken into account when paying fees and submitting returns for the period from the beginning of 2021. Let's look at the most important points of the new Rules.

The procedure for calculating the fee in each case is determined

Clauses 17-21 of the Rules provide specific formulas for calculating fees for emissions (discharges) of pollutants and waste disposal. The features of the application of these formulas by small and medium-sized businesses in certain cases are also determined:

- in the absence of permits for emissions (discharges) of harmful substances;

- in the absence of documents approving waste generation standards and limits on their disposal

- in other cases (clauses 12-16, 22 of the Rules).

How Rosprirodnadzor controls fees for environmental assessments

The new Rules determined the procedure for the fee administrator (Rosprirodnadzor) to control its calculation, including checking the fee declaration and the procedure for challenging the administrator’s decision to incorrectly calculate the fee (clause 4, 37-49 of the Rules).

It has been established that control over the calculation of fees is carried out:

- within 9 months from the date of receipt of the payment declaration;

- when conducting state environmental supervision in accordance with Federal Law dated December 26, 2008 No. 294?FZ.

As part of such control, the accuracy of the calculation of the fee according to the submitted declaration, as well as the completeness and timeliness of its payment, will be checked.

The fee administrator has the right to require clarifications and (or) appropriate changes to be made within 7 working days if errors in filling out the declaration, contradictions or inconsistencies in the information provided and available are identified.

In addition, when adjusting the amount of fees for expenses associated with the implementation of measures to reduce the negative impact on the environment, inspectors have the right to request the necessary copies of the documents specified in paragraph 29 of the Rules (clauses 40, 42 of the Rules). In this case, the person obligated to pay the fee may send an objection to the administrator regarding his requirements (clause 41 of the Rules).

If, as a result of checking the declaration (documents, information, explanations) submitted by the payer, the fee administrator determines that there are errors in the fee declaration and (or) contradictions between the information in the submitted documents, an act of monitoring the calculation of the fee is drawn up.

The form of the act and the procedure for filling it out must be approved by Rosprirodnadzor (clause 44 of the Rules).

The act indicates all the basic information about the control measures taken - dates, information about the persons being checked and the data and documents provided, facts of errors (contradictions), as well as conclusions and proposals for eliminating them (clause 45 of the Rules).

If the amount of the fee paid for the negative impact is underestimated, the inspector enters this into the report and issues a demand to the payer to pay additional fees and penalties (clause 46 of the Rules). This must be done within 10 calendar days. If the amount of the fee is overestimated, the payer can offset the overpayment against a future reporting period or return it (clause 48 of the Rules).

On the return of overpaid funds for tax assessments

In an information message, Rosprirodnadzor reminded organizations and individual entrepreneurs that currently the procedure for returning overpaid funds for negative impacts on the environment is not established by current legislation.

At the same time, the department notes: in order to confirm overpaid amounts, it is necessary to reconcile the calculations for the payment for the tax assessment.

The specified reconciliation of calculations should be carried out as part of the consideration of the Declaration of payment for the NVOS for 2021, based on the results of which an act will be drawn up.

At the same time, according to the norms of Resolution No. 255, control over the calculation of fees for environmental impact assessment is carried out by Rosprirodnadzor within 9 months from the day the declaration on payment for environmental assessment was submitted.

In a letter dated March 27, 2021 No. AA-06-02-36/6198, Rosprodnadzor provided the forms of documents relating to the administration of fees for NVOS:

- requirements for additional charges and payment;

- act of monitoring the calculation of fees;

- requirements for providing explanations and (or) making corrections to the declaration of payment for the tax assessment;

- requirements for the submission of documents confirming the actual expenses incurred for the implementation of measures to reduce the negative impact on the environment and measures to ensure the use and utilization of associated petroleum gas;

- applications for credit and refund of overpaid fees;

- decisions to refuse credit and return of overpaid amounts;

- applications for a joint reconciliation of calculations of the amounts of fees for the NVOS;

- act of reconciliation of calculations of payment amounts for the new tax assessment;

- decisions on offset and return of overpaid amounts of fees for the NVOS.

The specified document forms are recommended for use, but are not mandatory.

Let us remind you that in 1C programs the NVOS declaration with the ability to upload in 1.7 format is implemented. An example of filling out the Declaration of Fee for Negative Environmental Impact for 2021 can be found in the article “Declaration of Fee for Negative Environmental Impact for 2021: an example of filling out”.

The procedure for calculating advance payments for new construction materials may be changed

The provisions of Article 16.4 of Law No. 7-FZ concerning the procedure for calculating advance payments for the new tax assessment and making payments may be adjusted. The corresponding bill was published on the Unified portal for posting draft legal acts.

According to the amendments, persons obligated to pay quarterly fees for the NVOS will be able to choose one of three ways to determine the amount of the quarterly advance payment in the amount of:

- 1/4 of the amount of the fee for the NVOS paid for the previous year;

- 1/4 of the amount of payment for the NEE, calculated on the basis of established standards for permissible emissions, discharges of pollutants, temporarily agreed upon emissions, temporarily agreed upon discharges and limits on the disposal of production and consumption waste;

- equal to the amount of payment for environmental impact assessment calculated for the actual negative impact on the environment in the past quarter based on industrial environmental control data.

In the declaration of payment for the tax assessment, you will need to indicate which method is chosen.

The norms of the currently valid Law No. 7-FZ establish only one method for calculating advance payments - in the amount of 1/4 of the amount of the fee for the tax assessment paid for the previous year. This procedure for calculating advance payments for new tax assessments can lead to overpayments for organizations and individual entrepreneurs.

It is expected that amendments to Law No. 7-FZ will come into force on 01/01/2021.

Source: https://buh.ru/articles/documents/57347/

Recognition of expenses for NVOS

In accounting

The payment for the NVOS, in accordance with clause 5 of PBU 10/99 “Expenses of the organization” (approved by order of the Ministry of Finance dated 05/06/1999 No. 33n), is included in the costs of ordinary activities and is displayed in the debit of expense accounts (20, 23, 25 , 26, 44).

The payment for the tax assessment is not a tax payment, therefore, account 68 “Calculations with the budget” is not used for accounting purposes. The occurrence and repayment of obligations for “negative impacts” is recorded in account 76 “Settlements with other debtors and creditors”.

In tax accounting

The payment for the NVOS within the limits of the standards relates to material costs (subclause 7, clause 1, article 254 of the Tax Code of the Russian Federation).

Payments for negative impacts on the environment in excess of these amounts are not taken into account in expenses (clause 4 of Article 270 of the Tax Code of the Russian Federation).

In letter dated 06/07/2018 No. 03-03-06/1/39148, the Ministry of Finance of the Russian Federation notes that the Tax Code does not establish a deadline for recognizing material expenses in the form of a fee for the tax assessment. For enterprises and individual entrepreneurs under the general taxation system, officials recommend recognizing expenses in the form of a fee for tax assessment on the last day of the tax period for which it is made. Officials also recommend recognizing quarterly payments as expenses on the last day of the reporting period for which they are made (letters of the Ministry of Finance of the Russian Federation dated 08/15/2016 No. 03-03-06/1/47690, dated 08/08/2016 No. 03-03-06/1/ 46432).

For organizations and individual entrepreneurs on a simplified taxation system with the object “income minus expenses,” the fee for the tax assessment (within the limits of the standards) can be taken into account as part of material income (subclause 5, clause 1, article 346.16 of the Tax Code of the Russian Federation). Expenses in the form of fees for the tax assessment are recognized at the time of debiting from the current account (subclause 1, clause 2, article 346.17 of the Tax Code of the Russian Federation).

Results

The procedure for calculating the annual pollution fee for 2021 remains the same as in 2021. The calculation itself is made in specially designated sections of the declaration, allocated depending on the type of polluting object. The fee accrued for these sections is then adjusted to the amount of expenses for measures to reduce the negative impact and to the amount of advances paid during the year.

Sources:

- Federal Law of January 10, 2002 No. 7-FZ

- Decree of the Government of the Russian Federation dated June 29, 2018 No. 758

- Decree of the Government of the Russian Federation dated March 3, 2017 No. 255

- Decree of the Government of the Russian Federation of September 13, 2016 No. 913

- Decree of the Government of the Russian Federation of September 28, 2015 No. 1029

- Order of the Ministry of Natural Resources of Russia dated 01/09/2017 No. 3

- Tax Code of the Russian Federation

- Order of the Ministry of Finance of Russia dated May 6, 1999 No. 33n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Basis and legal basis

A fee for negative environmental impact is usually referred to colloquially as an environmental fee or an environmental fee.

It is required to be paid by all those who, due to the nature of their activities, have a negative impact on the environment. The responsibility for this fee lies with everyone who operates on the territory of Russia, regardless of their legal form and form of ownership. The procedure for calculating and collecting fees for negative impacts on the environment is established by Russian Government Decree No. 632 of August 28, 1992, which has undergone major changes, as well as by Federal Law No. 7-FZ of January 10, 2002. It defines the types of pollution for which a fee is charged and the basic standards for calculating the environmental fee.

It should be noted that from January 1, 2021, when calculating fees for environmental pollution, it is necessary to be guided by the Decree of the Government of the Russian Federation of September 13, 2016 N 913 “On fee rates for negative environmental impacts and additional coefficients.”

Starting from 2021, payment of the environmental fee and submission of a calculation of the amount of the environmental fee are carried out annually - until April 15 of the year following the reporting period. The key change for 2017 is that the reporting period for this tax is now a year rather than a quarter.