Correction in primary documents

Important! An accountant may make a mistake when drawing up primary accounting documents, accounting registers, various forms of accounting or tax reporting and calculations. It should be remembered that not every document can be corrected. In certain cases, it will need to be compiled again.

In accordance with Law No. 402-FZ “On Accounting” (Part 7, Article 9), corrections in primary documents are possible only if “unless otherwise established by federal laws and regulations of state accounting regulatory bodies.”

Documents that are not allowed to be amended include:

- Cash documents (expenses and receipts cash orders). Other documents that are drawn up when conducting cash transactions are subject to correction. For example, corrections are allowed in the cash book.

- Strict reporting forms . This document must be filled out legibly and clearly and corrections are not allowed. The damaged BSO must be crossed out and attached to the book of document forms for the date on which it was filled out.

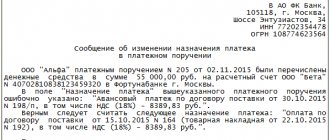

- Bank documents . Corrections and errors in banking documents are unacceptable. Corrections will be perceived as a violation of the integrity of the order in the funds transfer. Such errors cannot be corrected.

What documents are prohibited from editing?

Corrections made to documents issued electronically are prohibited. If the institution has an electronic document management system, corrections can only be made with a new electronic document. This is established in clause 4.7 of Directive No. 3210-U.

If we consider the types of documents in more detail, then the documents that are subject to a complete ban on making corrections include:

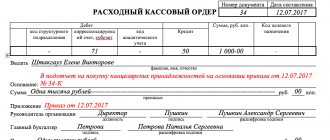

- Receipt and expense cash orders;

- Bank orders reflected on paper (payment requests, orders or orders).

Which documents can be corrected?

Now let's figure out which documents can be corrected. In all cases not related to those listed above, the source documents can be corrected. In this case, the correction must contain the date of correction, the signature of the persons who compiled this document and an indication of the surname and initials, as well as other details that allow identification of the person. At the same time, the main questions regarding corrections in primary documents include: How to correctly correct an error, can it simply be covered up with a proofreader? Who signs the correction if the employee who made the error is absent? (

Primary documents on paper

Methods for making changes to documents drawn up with errors must be enshrined in the accounting policies of the enterprise or organization.

If you find an error or typo:

- incorrect amounts or document details are crossed out;

- the correct number or text is written at the top;

- put the inscription “corrected”;

- this inscription is endorsed by all those employees who originally signed the document;

- if necessary, stamps are affixed.

An erroneous entry is crossed out once (it must be readable); proofreaders cannot be used, or the error cannot be shaded or cleaned up.

Important

The correction must be made to all copies of the primary document, since the tax office, when checking one business entity, can check its counterparty, who has another copy. If discrepancies are identified, penalties usually follow.

If there are many corrections or they make the document details unreadable, then it is necessary to issue a new copy. Corrections are not allowed in cash and bank orders and payment orders; they are redone by filing both copies (new and damaged) into accounting documents.

The accounting policy of an organization or enterprise can provide for both methods of making corrections to primary accounting documents or choose the most suitable one for accounting.

What to do if the correction cannot be signed by the author of the document

Situations can be different, and the employee who compiled the primary document could quit, get sick, or be on vacation or a business trip at the right time. Regulatory documents do not provide for a procedure in this case, so companies can develop the method and procedure by which correction is carried out independently. Persons who have the right to sign primary documents are approved by the head of the company and coordinate this issue with the chief accountant. This list may also include persons who are authorized to sign these documents. For example, corrections can be signed by a person authorized to sign primary documents (

Errors in documentation: how to fix? Two ways to make changes to the primary document.

No person can be absolutely sure that he does everything correctly. Even an accountant. No matter how scrupulous, neat and pedantic he may be. Sometimes, due to an insidious case, inaccuracies can arise unexpectedly without any intent. As practice shows, errors in document flow are not uncommon. An oversight can occur even when using specialized software designed to automate document flow and prepare primary documents, on which, in fact, all accounting is based.

According to Russian legislation, any document with false information loses its legal significance. Consequently, the organization does not have the right to use it as confirmation of the fact of conducting its financial activities in the future.

However, not all details are “inviolable”.

In accordance with the explanations of the Ministry of Finance, a significant error is unreliable data contained in the primary document in the title, content, date of preparation, position and full name of the executor or signatory, values (in kind and monetary). In other words, any clerical errors/miscalculations in the information listed above give every reason to consider a particular document invalid from the point of view of the law until the errors in the primary documents are corrected.

The most common and frequently written primary documents are:

- Acts on the provision of services;

- Expense reports;

- Invoices.

Correcting errors in the documents listed above is possible, but this must be done strictly in accordance with the standards.

The most common document flow mistakes

In order to prevent cases where a particular document loses its legitimacy, we recommend that you consider the following aspects when filling out various primary documents.

Acts

These primary documents must have a name that can be determined at the organizational level. The date of compilation is also required, because Many people mistakenly believe that by indicating in the contents of the act the period during which the work or services were performed, they relieve themselves of the responsibility to indicate the date the document was drawn up.

Be sure to check the TIN of your counterparty. Reconciliation should be done not only with the registration card of the organization, but also with the data contained in the Unified State Register of Legal Entities. The name of the service must be spelled out in detail and not raise questions from the tax office. If the act is certified by the signatory under a power of attorney, it is necessary to indicate the details of the power of attorney and attach a copy of it to the document.

Invoices

The invoice must contain information such as date and number, as well as the position and full name of the signatories.

Expense reports

In these strict reporting documents, the required details are the date, information about the accountant (full name, position) and expense items with explanations.

Two ways to correct errors in documents

When an error is detected in a document, you should first of all classify whether it is significant or not. If an inaccuracy invalidates the legitimacy of a document, then it should be corrected promptly. There are rules governing adjustments in the primary document, according to which it is necessary to indicate the date when the change was made, as well as information about the employee (full name, position) who made these changes.

The law provides two main paths that can be followed if corrections are necessary in the primary documentation:

- Edits in the original document;

- Creating and sending a corrective document.

Let's take a closer look at each of them.

Corrections to the original document

The first way to correct errors in a document is to directly edit the data. On the one hand, this is the simplest option of all possible, because you only need to correct incorrect data. However, there are certain difficulties, for example:

- If the document flow error is complex, then you will have to make changes to a larger number of papers. This is inconvenient and, moreover, can give rise to new inaccuracies;

- Also, in the case of several edits in one document, it simply becomes unreadable. The counterparty may not understand the corrections and may not understand what data should be trusted. The same questions may be asked by the tax inspector who will check these primary documents;

- Inapplicability for electronic documents, because in this case the integrity of the containers and the cryptographic signature will be violated, which will automatically make the paper illegitimate;

- Difficulties in bilateral corrections - if errors in the document flow were discovered after the mutual exchange of copies with the counterparty, then it will be necessary to accurately verify that the corrections to the errors in the documents were accurately made. In this case, you can also ask the counterparty to destroy the existing version and send him a new paper with corrections made by hand.

As you can see, the first method has many limitations that are not convenient from an operational point of view, take a lot of time and resources and, most importantly, can give rise to new inaccuracies and inconsistencies.

Corrective documents

The most modern, convenient, transparent way to correct document flow errors is the second method: creating a new, correct document. At the legislative level, this method is not clearly regulated; therefore, each enterprise can independently develop rules for this procedure and enshrine them in norms and accounting policies.

There is only one limitation - only the party that issued the primary documentation can make corrections in the electronic document management system, even if the inaccuracy was identified by the counterparty.

To effectively work with documents in an organization, increase the speed of turnover and approval of papers, and reduce the number of errors, we recommend that you use the VLSI Electronic Document Management system. To work in it, you will need an electronic digital signature, which can be purchased at our Digital Signature Center.

Contact us to order VLSI Electronic Document Management or ask any questions you may have.

Rate this article:

Correction in invoices

The procedure by which corrections in invoices occur is determined by Resolution No. 1137 of December 26, 2011. Depending on what error was made, the company will need to issue a corrective invoice or make corrections to the erroneous document. If it is discovered that there is an error in the invoice, but it does not prevent the tax authorities from identifying the seller, buyer, property rights, name of goods, their value, etc., then new invoices may not be issued. For example, if the name of the product is indicated incorrectly on the invoice, then a new document will need to be drawn up, since in this case the taxpayer will lose the right to deduct VAT.

Important! The corrected invoice is signed by the head of the company and the chief accountant, or authorized persons.

How to correct a paper document?

When making corrections to a paper document, it is necessary to cross out the erroneous data, indicating the correct ones, and also reflect the date of the correction, position and signature of the person who made it. Corrections may only be carried out in the manner established by the accounting policy of the institution. If we consider in more detail the process of making changes, the following actions must be taken:

- Detect an error or clerical error (incorrect details, incorrect amount);

- Cross out erroneous data;

- Place it next to the place where the adjustment is made;

- Sign the corrective inscription by all employees whose signatures appeared in the erroneous document;

- If available, mark it with a stamp.

When performing this algorithm, it is worth remembering that you only need to cross out the corrected entry once, since all data is required to be read. The use of correctors, strokes, and erasures is prohibited.

It is also worth remembering that corrections made must be made in all copies of the previous document. Tax authorities quite often use the method of counter audits in their activities. If there is a discrepancy between the data of the same primary accounting document in different organizations, administrative liability may arise.

If it is necessary to make a large number of corrections, which in turn make the document completely unreadable, you should resort to creating a new copy. In this case, the previous one must also be preserved and filed together with the newly created one. This method is widely used when working with PKO - RKO, as well as bank orders. These are the only documents that do not tolerate any corrections to the original version of the document. Therefore, they can only be corrected by creating a new instance. When developing accounting policies, it will be useful to take into account all options for possible corrections.

Reporting correction

Reporting documents that cannot be corrected using a proofreader or similar means include calculations of insurance premiums and tax returns:

- according to VAT;

- on income tax;

- on property tax;

- on transport tax;

- for tax paid in connection with the application of the simplified tax system;

- according to UTII for certain types of activities.

Important! No corrections are allowed in the personal income tax return.

In the calculation of accrued and paid insurance premiums for compulsory health insurance against NS and occupational diseases, corrections are made as follows:

- an incorrect indicator value is crossed out;

- enter the correct value of the indicator;

- The correction is signed by the policyholder or his representative, as well as the date of correction.

If the company uses a seal, then corrections must be certified by it.

How to correct an electronic document?

If the primary document, compiled in the form of an electronic document signed with an electronic signature, contains errors, then a new electronic document is created. An erroneous electronic primary may be recalled. The specific procedure for making corrections to an electronic source document will depend on the operator through which the electronic documents are exchanged.

Quite often questions arise about how to correctly make corrections to primary documents, and how such corrections are reflected in accounting and reporting. We will talk about this in this article.

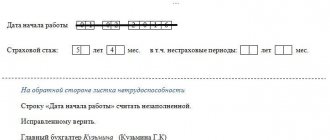

In accordance with clause 7 of Article 9 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” (hereinafter referred to as Law No. 402-FZ), corrections are allowed in the primary accounting document, unless otherwise established by federal laws or regulations acts of state accounting regulatory bodies. The correction in the primary accounting document must contain the date of the correction, as well as the signatures of the persons who compiled the document in which the correction was made, indicating their surnames and initials or other details necessary to identify these persons.

Errors in primary accounting documents are corrected as follows: the incorrect text or amounts are crossed out and the corrected text or amounts are written above the crossed out. Crossing out is done with one line so that the correction can be read. In this case, the correction of an error in the primary document must be indicated by the inscription “corrected” (clause 4 of the Regulations on Documents and Document Flow in Accounting, approved by the Ministry of Finance of the USSR on July 29, 1983 No. 105).

Thus, the mechanism for making corrections to primary accounting documents, set out in paragraph 7 of Art. 9 of Law No. 402-FZ is not strictly regulated. These provisions of Law No. 402-FZ establish only the minimum requirements for the content of the corrected primary accounting document: mandatory indication of the date the corrections were made, as well as identifying information about the persons who made the correction.

However, in practice, correction of incorrectly completed primary documents is also used by completely replacing them with new documents with the same details, indicating the date of the corrections.

It should be noted that current legislation and regulations do not prohibit the use of such a correction procedure. At the same time, the legality of such a procedure for correcting primary accounting documents, including for tax purposes, is also confirmed in private clarifications of the Ministry of Finance of the Russian Federation, for example, based on Letter No. 07-01-09/2235 dated January 22, 2016, it follows that, on the one hand On the other hand, Law No. 402-FZ does not provide for the replacement of a primary accounting document previously accepted for accounting with a new document if errors are detected in it. On the other hand, taking into account parts 2 - 4 art. 8 of Law No. 402-FZ, as well as the Accounting Regulations PBU 1/2008 “Accounting Policy of the Organization”, approved by Order of the Ministry of Finance of Russia dated October 6, 2008 No. 106n, the organization has the right to independently develop ways of making corrections to the primary accounting documents compiled on on paper and in the form of an electronic document, based on the requirements established by Law No. 402-FZ, regulatory legal acts on accounting, and taking into account the peculiarities of document flow.

Currently, arbitration practice has developed in similar situations, according to which the legislation of the Russian Federation does not prohibit making changes to primary accounting documents, including by replacing them with properly executed ones, without changing indicators affecting the volume and content of business transactions (for example, Resolution FAS Moscow District dated May 21, 2008 N KA-A41/4238-08 in case No. A41-K2-14877/07, Resolution of the Ninth Arbitration Court of Appeal dated October 7, 2009 in case No. A40-51820/08-14-203 (FAS Resolution Moscow District dated January 15, 2010, this Resolution was left unchanged), the Resolution of the Fourteenth Arbitration Court of Appeal dated March 28, 2013 in case No. A13-9242/2012, which stated that, as well as the Resolution of the Nineteenth Arbitration Court of Appeal dated February 21, 2013 in case No. A64-3569/2012).

Taking into account the above, as well as the established arbitration practice, it seems possible to draw the following conclusion.

Correction of primary accounting documents is allowed both by making changes to existing documents and by issuing new ones in the above order - i.e. with the same date under the same number, indicating in the source document (or in the accompanying letter) the date of the correction. At the same time, the implementation of the first of these correction methods is associated with lower tax risks.

It is not allowed to make unilateral changes to primary accounting documents. In this case, one should take into account the established arbitration practice, for example, Resolution of the Tenth Arbitration Court of Appeal dated January 16, 2015 No. 10AP-14763/2014 in case No. A41-53651/14, according to which unilateral change of information in primary documents without the mutual will of the parties is contrary to the law and does not entail legal consequences, as well as the Resolution of the First Arbitration Court of Appeal dated June 30, 2015 in case No. A43-27322/2014.

The procedure for correcting errors in accounting and reporting is regulated by Order of the Ministry of Finance of Russia dated June 28, 2010 No. 63n “On approval of the Accounting Regulations “Correcting Errors in Accounting and Reporting” (PBU 22/2010)” (hereinafter referred to as PBU 22/2010) and depends on the significance of the error and the moment it was discovered.

The organization determines the criteria for the materiality of an error independently, taking into account clause 3 of PBU 22/2010.

We will consider the most difficult case from the point of view of making corrections - the discovery of an error after the presentation of financial statements and after their approval.

In accordance with paragraphs. 1 clause 9 PBU 22/2010 a significant error of the previous reporting year, identified after the approval of the financial statements for this year, is corrected by entries in the corresponding accounting accounts in the current reporting period. In this case, the corresponding account in the records is the account for retained earnings (uncovered loss).

According to paragraphs. 2 clause 9 PBU 22/2010, when correcting a significant error of the previous reporting year, identified after the approval of the financial statements for this year, in addition to making corrections to the accounting, the comparative indicators of the financial statements for the reporting periods reflected in the financial statements of the organization for the current reporting year are adjusted. Restatement of comparative financial statements is carried out by correcting the financial statements as if the error of the previous reporting period had never been made (retrospective restatement). Retrospective restatement is carried out in relation to comparative indicators starting from the previous reporting period presented in the financial statements for the current reporting year in which the corresponding error was made.

At the same time, clause 10 of PBU 22/2010 provides that in the event of correction of a significant error of the previous reporting year, identified after the approval of the financial statements, the approved financial statements for the previous reporting periods are not subject to revision, replacement and re-presentation to users of the financial statements.

In accordance with paragraph 14 of PBU 22/2010, an error of the previous reporting year that is not significant, discovered after the date of signing the financial statements for this year, is corrected by entries in the corresponding accounting accounts in the month of the reporting year in which the error was identified. Profit or loss arising as a result of correcting this error is reflected as part of other income or expenses of the current reporting period.

Tax audits are becoming tougher. Learn to protect yourself in the Clerk's online course - Tax Audits. Defense tactics."

Watch the story about the course from its author Ivan Kuznetsov, a tax expert who previously worked in the Department of Economic Crimes.

Come in, register and learn. Training is completely remote, we issue a certificate.

Accounting information

If an error was made in the accounting accounts when recording a business transaction, then an accounting certificate is issued, which will indicate that corrections were made to the entries. The reason for this is that, according to the Law “On Accounting”, the data reflected in the accounting registers is produced on a primary basis. This certificate is necessary in order to correct the data, as well as to confirm that an error was made. The correct data is transferred to the accounting registers based on the certificate.

A certificate is drawn up in free form with the obligatory indication of the details specified in the law.

Correction of accounting entries

Primary accounting documents are systematized by creating accounting entries and registers. Before creating them, an accounting employee is required to check the document that serves as the basis for reflecting the amounts in accounting.

If an error is detected after an accounting operation, for example, following an inventory count, then the data can be changed in two ways:

- If the amount is underestimated and a surplus is formed, an additional entry is made for the amount of the discrepancy;

- When the posted amount is higher than the actual amount, the accountant reverses the transaction (enters the transaction amount with a negative value) and posts a new amount. This adjustment is called “red reversal”.

Important

Once the annual reporting has been approved, it is prohibited to make corrections to it. Regulatory entries are made on the date the error is discovered.

If the annual reporting is not approved or the reporting period is not completed, then:

- corrections are made on the date of the erroneous transaction;

- regulatory entries are made in December of the reporting year.

Example: in May 2021, the amount of goods received in the technical tax was incorrectly underestimated, the accountant did not notice the error in a timely manner and accounted for the cost according to the primary document. To adjust accounting data, the date the discrepancy was discovered is important:

- The difference was discovered during the annual inventory in November 2021. In this case, adjusting entries are made by the date of the transaction, that is, May 2021.

- Discrepancies were revealed by an audit in January 2021; annual reporting was not approved. In this case, the settlement will be carried out in December 2021.

- In mid-2021, the reporting of the previous period was checked, and then we noticed a difference in the amounts on the invoice and the goods actually received. The annual statements have already been approved, so the adjusting entry is made on the date the error is discovered.

note

Each time when adjusting accounting data, it is necessary to draw up an accounting certificate, which will be considered a justification for the changes made.

Responsibility for errors in accounting documents

If an error made by an accountant and entered into the accounting records is noticed by tax officials during an audit, this may lead to penalties. The amount of the fine can be 10,000 - 30,000 rubles, or 20% of the amount of unpaid tax or contributions to the Pension Fund, but not more than 40,000 rubles.

Tax authorities may consider documents with errors to be fake documents and the company may be held liable on this basis. In this case, the organization and officials may face:

- fine up to 80 thousand rubles;

- a fine in the amount of half a year's salary;

- corrective labor for 2 years, compulsory labor for 480 hours;

- arrest up to 6 months.

How to correct an error in accounting registers?

One of the methods is called “red reversal.”

The generalization of primary accounting documents occurs through accounting registers. To create such a register, all documents must be posted to the correct accounting accounts and contain correct entries.

Before forming these registers, employees of the accounting department carry out reconciliation with the concerned services. If an error is detected in the direction of underestimating the amount, additional entries are introduced into the system. It reflects the missing amount.

If an error is detected in favor of an increase, the accountant must reverse the difference between the actual amount and the one that needs to be reflected in the accounting records. The adjustment is made by an amount with a negative value. This method is called “red reversal”.

The exception to any actions aimed at adjusting amounts is the submission and approval of annual financial statements. In this case, correction is carried out on the day the inaccuracy is discovered. If the report is not approved, you can correct it by the date of the main transaction, but the postings can only be made in December of the reporting year.

Do not also forget that in order to correctly reflect the changes made in accounting programs, an accounting certificate has been developed (f. 0504833). All corrections are made through invoice correspondence and are justified by reference to the details of the document being corrected.

Answers to common questions

Question: If the person responsible for maintaining the document is absent, can an employee make corrections by proxy?

Answer: The fact is that a power of attorney is an instrument of civil law relations. According to labor legislation, the labor function must be performed by the employee personally, and in the Labor Code of the Russian Federation such a term as “power of attorney” is not used at all. When drawing up a power of attorney, it must indicate a specific person, but if the employment contract with the employee is terminated, this cannot be done. The procedure by which accounting is kept in the company is approved by the manager, so only he can decide who will sign the corrections in the event of the absence of the required employee.

Invoice adjustment

The rules for making corrections to the invoice are provided for in paragraph 7 of Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 (hereinafter referred to as the Rules for filling out the invoice). It is this document that should be followed.

Corrections to the invoice are made by the seller (including in the presence of notifications drawn up by buyers about clarification of the invoice in electronic form) by drawing up new copies of invoices or adjustment invoices.

Not every mistake requires correction. It is necessary to correct the invoice only if errors are detected that prevent the tax authorities from identifying:

- seller;

- buyer of goods (works, services), property rights;

- name of goods (works, services), property rights:

- cost of goods;

- tax rate;

- the amount of tax charged to the buyer.

If such inaccuracies are identified, the seller must supply a new (corrected) copy. In line 1a of the new invoice, you must indicate the serial number and date of changes (subparagraph “b”, paragraph 1, paragraph 7 of the Rules for filling out the invoice). Line 1 of the new invoice indicates the number and date of the original copy (clause 7 of the Rules for filling out the invoice). Next, the remaining details with the correct values are indicated.

The new copy is signed by the head and chief accountant of the organization (other authorized persons) or an individual entrepreneur, who also indicates the details of the state registration certificate (clause 7 of the Rules for filling out an invoice).

In the event that the cost of goods or their quantity (volume) has changed, and this is confirmed by other primary documents, it is necessary to issue an adjustment invoice (clause 10 of Article 172 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated August 23, 2012 No. AS-4-3 / [email protected] ).