Business lawyer > Accounting > Accounting and reporting > How to correctly write off materials and document the process

The main activity of the enterprise is practically impossible without the acquisition of special materials. They are important not only for production, or in the sale of goods and services, but also for meeting the needs of the administrative apparatus.

In a warehouse, the storekeeper or the head of the department is responsible for storing such valuables. For accounting, an account of 10 is usually used. The situation changes after the so-called departure of materials from the warehouse. In this connection, the write-off procedure is applied.

Description of accounting entries

First, let's decide where exactly the purchased materials can be sent. They are capable of performing many functions, which are determined by the current needs of the enterprise:

Write-off in accounting

- Be the basis in production processes

- Function of auxiliary type parts for production

- They are used to create finished product packaging

- Application in the implementation of management processes, while meeting the needs of the administration

- Assistance when fixed assets are being liquidated and are being taken out of service

- Application in construction, after which fixed assets are created

Postings depend on how and why materials are released from the warehouse. Several notations are used for this.

Debit has the following signs:

- 91.2

- 44

- 26

- 25

- 23

- 20

Credit, accordingly, is indicated by just one digit – 10.

Sometimes it happens that materials are listed as property, but are actually missing, which leads to shortages. Such situations require the following designation - debit 94 and credit 10.

Write-off: how to register

Business transactions must always be accompanied by the documentation used in primary accounting. The rule makes no exceptions to the write-off procedure. In any organization, the manager has the right to determine for himself which papers will be used to organize primary accounting. Therefore, specific registration rules may differ from company to company.

The main thing is that the accounting policy contains information about the approved documentation. And monitor the presence of the mandatory details specified in the current legislation.

There are several standard forms, the use of which is permissible when writing off:

Warehouse write-off

- Invoices for the release of materials to third parties.

- Salary cards with certain limits.

- Invoice forms with a description of the requirement.

The organization can choose for itself which details are not needed and which ones will definitely be needed in a particular process.

The use of invoices with requirements allows you to organize accounting for the internal movement of material assets, with the participation of responsible persons or structural divisions.

Registration of invoices is the responsibility of the persons who deal with valuables. Only two copies are needed. The write-off is processed by one, and the second is needed for capitalization.

Write-off procedure

The procedure consists of 8 stages:

- A commission is created. The head of the organization can also join the commission if he so desires. An order is issued on the creation of the commission. It provides a list of the persons who make up the commission, and also contains an indication of the need to compile a list of valuables to be written off.

- The commission examines the values themselves, establishes the reasons for write-off: breakdown, damage, natural loss, identifies those responsible and further actions in relation to written-off material assets.

- The commission examines and analyzes documents confirming the state and composition of values: work reports, lists, expense reports, calculations, etc.

- The commission fixes the volume that needs to be written off, approves the list and sums up the amount and book value.

- All this data is reflected in a document signed by all members of the commission.

- The act is submitted to the manager for approval.

- Accounting makes the necessary entries and notes in accounting, financial and reporting documents.

- The commission exercises control over the destruction of written-off property, if necessary.

If a guilty person is identified, he may also be involved in the work of the commission. In this case, a note is made in the act on the procedure for reimbursing the organization’s expenses.

The accounting department records valuables at the actual cost of their acquisition, while indirect taxes paid to the supplier are not reflected in the final amount. The write-off method must be established in the accounting policy (at the cost of each unit, according to average cost indicators).

The write-off method approved in local regulatory documents cannot be changed during the write-off process. Sometimes the act is drawn up in the presence of third-party organizations, for example, with the participation of sanitary or fire inspectors.

Specifics of write-off for production

The need to write-off from warehouse to production arises for enterprises that are engaged in production activities. Such an act must reflect the following information:

- Date of completion;

- information about the sender of the document (name of the structural unit and its type of activity);

- information about the recipients (also the name of the specific structural unit and the type of its activity);

- why the property is written off, the purpose of this action (for example, for the production of accessories);

- the name of the property being written off, allowing it to be identified indicating the item number;

- unit of measurement of materials being written off;

- the amount of materials written off, that is, released into production;

- price.

What document should I use to document the transfer of materials to production?

Traditionally, independently developed or unified forms are used to document the transfer of materials to production: requirements-invoices, limit-fence cards, invoices for internal movement, etc. These documents are drawn up when transferring materials to production from a warehouse.

If purchased materials are directly delivered to a department or an on-site warehouse, bypassing the organization’s warehouse, drawing up documents for the movement is often impractical. In this case, a materials write-off act will help document the fact of transfer and use of inventory items in production.

How to confirm the actual use of materials?

When assessing material costs, you can use inventories of remaining materials in production indicating the name, quantity and cost of materials or other similar documents.

Instead of the documented result of recalculation of balances, as well as in the event that there are no balances and the transferred materials are fully used for production purposes, it is convenient to use the materials write-off act.

Write-off with disposal

After drawing up an act confirming that material assets are recognized as written off, the accountant needs to make the following entries:

- Dt 94 Kt 10. In this posting, the accountant reflects the book value of written-off inventory items, the data is taken directly from the act;

- Dt 20 Kt 94. It reflects the cost of shortage, loss or damage of materials within the limits of their maximum loss. Such information can also be provided in the act, or it should be requested separately and documented in a special accounting certificate. If the natural loss limit is exceeded, you cannot post from the Dt 20 account; you must additionally create subaccounts.

These are the main transactions; in some cases you will need to specify other accounts. For example, in the event of damage to property as a result of a natural disaster, a posting is made Dt 99 Kt 100. When generating data on accounts and registering transactions for the movement of inventory items, data from the act is used.

What to do if not all materials are used?

It is usually assumed that after release the materials will be used immediately for their intended purpose, and therefore the operation is accompanied by the postings that were already mentioned earlier.

But this doesn't always happen. Especially if the enterprise is quite large. It happens that the transferred values are not used immediately. Then the new storage location replaces the old one. When releasing the bases, it is worth noting that they do not always know exactly in which production process the sources are used.

Warehouse with materials

Valuables that have already been released from the warehouse, but have not yet been consumed, cannot be classified as expenses for the current period. This applies to both accounting and tax reporting. Therefore, actions are required in a slightly different order than usual.

This situation leads to the fact that the issue and registration of materials become internal processes. By applying a separate subaccount to account 10, which may be called, for example, “Materials in the workshop.” When the month comes to an end, another document is drawn up. Usually this is an act with information about material costs. There you can already indicate the direction of use of the values. At the same time as this action, write-offs are being carried out. Thanks to such tracking, accounting reports become more reliable. There are fewer errors when calculating income taxes.

The rules apply not only to what is used for production processes, but also to property of any kind. For example, to stationery that is used by the administration. There is no need to issue materials “in reserve”; they need to be used immediately.

The materials were used, but not written off... How to fix it?

Question: During the inventory of materials carried out as of November 1, 2018 before the preparation of annual financial statements for 2021, it was revealed that account 10 “Materials” continues to include materials actually used to create a fixed asset (FPE) item in the previous months of 2018.

How to reflect corrective entries in an organization's accounting records?

Answer: Materials actually used to create an asset in the previous months of 2021 must be included in the initial cost of this asset, and additional depreciation must be added and changes must be made to tax accounting data.

Rationale: During the inventory, the presence, condition and assessment of assets and liabilities (including unaccounted for) are documented by:

— comparisons with accounting data;

— identifying assets and liabilities that have partially lost their original purpose (consumer properties) and are morally obsolete;

— identifying excess and unused assets and liabilities for the purpose of their accounting and subsequent sale or write-off;

— checking obligations in order to correctly formulate income and expenses of future periods, reserves for future expenses, as well as the reliability of the amounts of receivables and payables, etc.;

— checking the formation and use of sources of own funds, targeted financing, etc. <*>.

The initial cost of fixed assets created in an organization is determined in the amount of actual direct and distributed variable indirect costs for their creation, with the exception of cases established by law <*>.

Actual costs associated with the creation of fixed assets, installation, assembly of fixed assets and bringing them into a state suitable for use are reflected in the accounting accounts:

D-08 “Investments in long-term assets”

Kit 10 “Materials”,

60 “Settlements with suppliers and contractors”,

69 “Calculations for social insurance and security”,

70 “Settlements with personnel for wages”,

76 “Settlements with various debtors and creditors”, etc.

The generated initial cost of fixed assets is reflected:

Dt 01 “Fixed assets”

Kit 08 “Investments in long-term assets” <*>.

Thus, the materials actually used to create the fixed asset in the previous months of 2021 should have taken part in the formation of the initial cost of the fixed asset.

The procedure for correcting errors is established by the norms of National Standard N 80.

Correction of errors is formalized by an accounting statement containing information established by the legislation of the Republic of Belarus for primary accounting documents <*>.

An error made in the reporting year and identified before its end is corrected in the month of the reporting year in which the error was identified by an additional or reversal entry(s) in the relevant accounting accounts. Income or expenses arising as a result of correcting this error are reflected in the income or expenses of the reporting year <*>.

If an error is discovered in determining the depreciable cost, standard service life or useful life of fixed assets, the error is corrected in the month it was discovered by recalculating the amounts of previously accrued depreciation and reflected in accounting in the prescribed manner <*>.

The organization should reflect in the month the error was discovered based on the accounting statement:

D-08 “Investments in long-term assets”

Kit 10 “Materials”

And

Dt 01 “Fixed assets”

K-t 08 “Investments in long-term assets” - materials are written off to the cost of the fixed asset;

Dt 20 “Main production”,

25 “Overall production costs”,

26 “General business expenses”, etc.

Kt 02 “Depreciation of fixed assets” - additional depreciation of fixed assets has been accrued.

Corrections to tax accounting data are made in accordance with the requirements of clause 8 of Art. 63 Tax Code and Instructions No. 42.

With regard to income tax, if incomplete information or errors are detected for the previous reporting period of the current tax period, changes (additions) are reflected in the tax return (calculation) submitted for the next reporting period of the current tax period.

About write-off standards for production

The legislation does not have strict and clear rules that would describe in detail the write-off process. It is usually said that it is necessary to rely on the volume of the production program and the standards according to the same document. The main thing is that the total amount of valuables does not become uncontrollable. And so that the norms themselves are officially approved.

Any expenses must be supported both economically and documented. The organization independently determines the standards according to which certain values are spent.

Write-off according to standards

For consolidation, you can use estimates, technological maps and similar documents. They are developed in departments that personally control the production process. After this, the papers are sent to the manager for approval.

A situation where existing standards are exceeded is acceptable, but each such case requires a separate indication of the reasons. For example, the explanation could be technological losses or the need to fix a defect.

It becomes the responsibility of managers and authorized persons to formalize decisions to exceed the current norm. To do this, a corresponding mark is placed on the primary accounting document. Otherwise, the write-off itself will not be recognized as legal. The cost price will be distorted, which leads to violations in accounting and tax reporting.

The nuances of writing off goods with rapid wear and tear and those that have already become unusable

While an organization is conducting its activities, it is often necessary to write off materials that have become completely unusable. The process is distinguished by its features in accounting policies. They depend on:

- Proof of the guilt of a specific employee or any other person that everything went wrong.

- Standards for writing off inventories. Are these standards exceeded or fully complied with?

Cleaning equipment

As for the price of damaged materials, it is written off within the limits of norms associated with natural loss. The process uses accounts that list production costs. The standards are exceeded if the presence of guilty persons is proven or there are additional costs.

The following addition is provided for those who work with the write-off of low-value, wear-and-tear goods. Accountants can write off the cost at the same moment when the object is put into operation. It is permissible to carry out so-called uniform accounting. But the application of the scheme is relevant in the case of items with a service life of 1 year or more. In the accounting policy it is necessary to write about which method is used in a particular case.

To distinguish between fixed assets and low-value assets, the legislation establishes a criterion for a price reaching up to one hundred thousand. But it does not work for accounting purposes. In this regard, in this regard, property whose value does not exceed 40 thousand rubles is considered to be of low value.

Inventory and household supplies are a group of items for which calculations are carried out using similar schemes. Legislatively, the composition of the group itself is not detailed. But in practice, this property includes:

- Equipment for cleaning the area, fire extinguishing equipment

- Electronic equipment such as cameras and video recorders

- Kitchen appliances

- Office furniture

Accounting methods for inventory items

Accounting methods are prescribed in Guidelines No. 119.

Varietal method

Accounting is carried out using grade-type cards. They record the presence of objects, as well as their movement. Paragraphs numbered 136-140 of the Methodological Instructions describe the features of the method. Accounting can be carried out in the following ways:

- Quantitative-sum . It is assumed that numerical and total accounting is simultaneously introduced in warehouses and accounting departments. In this case, inventory numbers of inventory items are used.

- Baldovy . It is assumed that exclusively quantitative accounting by type of inventory items is introduced in warehouses. Accounting uses total accounting. It uses monetary terms. Quantitative accounting is carried out on the basis of primary documentation. In this case, cards and books are used for warehouse accounting. After the end of the reporting year, the primary documentation must be submitted to the accounting department.

The varietal method is used when inventory items are stored by name and grade. In this case, the time of delivery of valuables and their cost are not taken into account. A separate inventory card is created for each item. One nomenclature differs from another in the following indicators:

- Product brand.

- Variety

- Unit of measurement.

- Colors.

The cards will be valid throughout the year. They must contain all the information about the accepted object. They must be registered in the appropriate register. After this, individual numbers are placed on the cards. Registration is required by employees of the accounting department. If the entire sheet of the card is filled, new sheets are opened. They must be numbered.

NOTE! All entries made on cards must be supported by primary documentation.

Pros and cons of the varietal method

The varietal method has the following advantages:

- Saving warehouse space.

- Quick management of inventory balances.

However, there are also significant drawbacks - difficulties in classifying goods of the same type at different prices.

Question: How is the provision of services under a warehousing agreement reflected in the custodian’s accounting, including the receipt of inventory items for safekeeping and their return at the end of the agreement? View answer

Batch method

The batch method involves an accounting procedure similar to the varietal method. The difference is that each batch of inventory items is registered separately. The batch method is described in paragraph 242 of the Directions. It is used both in the warehouse and in the accounting department. Assumes separate storage of each batch. Each shipment must have a corresponding transport document.

IMPORTANT! Products that were transported by one transport, goods with one name and simultaneous receipt from a single supplier - all this can be considered a single batch.

The batch must be registered in the goods and materials receipt journal. She is assigned an individual registration number. It is used to make marks in expenditure documentation. The registration number is placed next to the names of inventory items. You need to open two party cards. One will be used in the warehouse department, the other in the accounting department. The shape of the card is determined by the type of product.

Pros and cons of the batch method

The technique has the following advantages:

- Determination of batch consumption results without inventory.

- Increased control over the safety of inventory items.

- Reducing enterprise losses.

But there are also disadvantages:

- Irrational use of warehouse space.

- There is no possibility of operational control of inventory items.

The choice of a specific method will depend on the priorities of the enterprise and the size of the warehouse.

About the nuances of the write-off procedure

The cost of materials largely determines how much the work itself, where these objects are used, will cost. This is especially important for those objects that belong to the elite category. When an organization draws up an estimate, it is important to lay down certain standards associated with costs.

Inventory commission

Standards for estimates are a whole set of data on prices, where items are combined into separate categories. This is necessary in order to understand how much certain actions will cost.

The estimate norm is all the resources in the aggregate established for the adopted meter in various types of work. Estimated standards perform one main function - calculating the amount of resources that are normally required to complete a particular process.

But the documents are drawn up on the basis that normal conditions are observed during the implementation of the project, and that no external factors complicate this process. If any complications are present, then special coefficients are simply added to the documentation to the calculation results. The coefficients themselves are described in legislative norms.

Estimated standards are:

- Regional.

- Departmental.

- Federal.

Users can create their own database. To determine the cost in construction, several generally accepted methods are used. Some of them are transferred to other directions.

- Resource method. All costs in this method are simply summed up in physical terms with current prices. Among the indicators used, it is worth noting:

- Consumption of materials with components.

- The period during which machines are used in construction.

- Labor intensity.

An organization can use its own information to calculate the required level of parameters. It is allowed to rely on collections in the relevant industry, and standard prices on the corresponding basis.

- Basis-index calculations. In this method, the cost of construction is determined in its own way. To obtain the result, experts add up the prices of all types of building materials, which can be called consolidated. The resulting amount is multiplied by indices after recalculating the base prices into current ones.

- Resource-index methods. The resource method determines the total using basic prices. Then multiplication by indices is carried out, bringing the cost to the modern level.

- Basic compensation option. The cost of work and expenses is summarized at a basic level. To these are added additional costs associated with the fact that market indicators have changed quite significantly.

- Using data about objects that have already been built.

What happens if you don’t draw up an act

As mentioned earlier, if the valuables that are subject to withdrawal are written off from the warehouse based on the expired depreciation period or due to obsolescence, the TORG-16 form does not need to be used. In this situation, the act is drawn up in any form, indicating the serial number of the goods and the date of execution of the document.

The name of the legal entity, the full name of the director and the name of the department from which these values are written off are also required.

Listed below in order:

- name of all write-off units;

- their serial numbers;

- quantity;

- cost per unit of production;

- reason for write-off.

The last line will be the accounting value of warehouse inventory and the final figure that is subject to withdrawal. The act must be endorsed by all members of the commission, signed by the director of the organization and secured with the official seal of the enterprise.

However, in many organizations the timing of this activity may be delayed. Therefore, in exceptional situations, the manager may decide that there is no need to draw up such a document at all. Then it is recommended to take as an example systematic instructions on accounting for inventories (MPI) and on the preparation of initial documentation for the issuance of inventory and materials to various branches and departments of the organization.

To do this, the fact of transfer within the enterprise structure is recorded in the limit card of form M-8 or using the invoice forms F-11 and F-15.

To summarize, it should be noted that correct, timely written-off acts on valuable inventories significantly facilitate the dialogue between the organization’s management and tax service employees. It is, of course, better to prevent the consequences of audits, because representatives of the tax authorities are quite scrupulous in considering actions that are related to the company’s expenses.

Write-off of materials: detailed instructions

Materials are inventories that are purchased by an organization. These are the means to obtain products and service the production process. To display such reserves, account 10 is almost always used. Subaccounts are opened for it. To display the movement of fixed assets, you can also use accounts 15 or 16. Materials are written off if a shortage or damage is detected. Or when objects fail severely enough and are deemed unsuitable for further use.

Of the necessary devices for carrying out the operation, only the act of writing off materials is noted, together with a certificate of the corresponding content, transmitted to the accounting department.

When valuables are written off, the creation of a special commission is mandatory. It must include persons with standard financial responsibility. It is the members of this commission who draw up the write-off act. The following few points must be included in the document in any case:

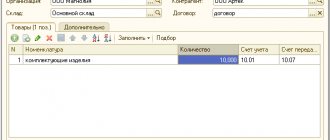

Write-off in the program

- Quantitative and price characteristics, amounts.

- The reason why valuables need to be written off.

- The name of the materials themselves.

- Personal information of each member of the commission.

In addition, all participants sign the document. You cannot do without indicating the date by which the procedure was carried out.

Separate entries are made when the materials are already considered written off.

- K94 – if everything happens within the limits of natural decline.

- D20 – information on main production.

- K10 – to reflect the value of materials on the balance sheet.

- D94 – Shortage, loss of specific properties of an item.

Making a write-off order

If the write-off process is associated with the fixed assets of the enterprise, then filling out the order becomes the next step after the inventory is completed. Based on the results of this procedure, it is necessary to clarify the list of valuable items, the further use of which is impossible. Usually these are items that are broken or obsolete.

An employee with appropriate authority is responsible for preparing the order. For registration, it is allowed to use company letterheads. The document is subject to mandatory registration.

The following items must be present on any form:

- Header with the name of the document itself.

- Clarification, indication of the reason why the commission was created.

- Information about the responsible persons and those who are members of the commission.

- Separate allocation of a responsible person appointed by the chairman of the regulatory body.

The order can describe the responsibilities that are transferred to employees checking material assets. After registration, the director approves the document and certifies it with his signature. All persons participating in the procedure must put their signatures on the order. The number along with the date of compilation is written at the top.

Top

Write your question in the form below