Simplified income minus expenses and BCC

Using the simplified taxation system “income minus expenses” in his business activities, a businessman has a number of economic advantages. They are as follows:

- Minimum tax payments.

- The minimum amount of reporting documentation.

Using this mode, you can avoid paying taxes such as personal income tax, VAT, income tax, and property tax. No matter how tempting this tax regime may be, not all commercial organizations can use it.

There is a certain limit on employees, on enterprise profits, on fixed assets, exceeding which no longer allows the use of the Simplified Taxation System. As a rule, this mode is used in small and medium-sized businesses. Therefore, most often, simple businessmen who understand little about accounting reporting fill out the payment form and indicate the KBK according to the simplified tax system.

To simplify their task in searching for the current BCC, when paying tax, you can provide a table of codes in which a simplifier can select their current BCC:

| What payment is being paid? | —-STS (income reduced by expenses). | —-STS (income). |

| Mandatory tax. | — 18210501021011000110 | — 182 1 0500 110 |

| Penalties for mandatory tax. | — 18210501021012100110 | — 182 1 0500 110 |

| Fines. | — 18210501021013000 10 | — 182 1 0500 110 |

Is there a special KBK for paying penalties on the minimum tax?

When paying penalties, you must also remember about the minimum tax that simplifiers pay with the object “income minus expenses.” It is equal to 1% of income for the tax period, if the tax according to the simplified tax system for the year is less than the minimum amount.

The BCC for it from 2021 coincides with the BCC of the regular simplified tax system with the object “income minus expenses”. Accordingly, the BCC for penalties accrued from 2021 is the same: 182 1 0500 110. The minimum tax (and penalties) accrued at the end of 2016 was paid under the same BCC.

Penalties incurred in the period 2011–2015 should have been transferred to BCC 182 1 0500 110.

KBK for paying taxes according to the simplified tax system for individual entrepreneurs

| Decoding the code | Budget classification code |

| Tax levied on taxpayers who have chosen income as the object of taxation (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0500 110 (original code) 18210501011011000110 (short code) |

| Tax levied on taxpayers who have chosen income as an object of taxation (penalties on the corresponding payment) | 182 1 0500 110 (original code) 18210501011012100110 (short code) |

| Tax levied on taxpayers who have chosen income as the object of taxation (interest on the corresponding payment) | 182 1 0500 110 (original code) 18210501011012200110 (short code) |

| Tax levied on taxpayers who have chosen income as an object of taxation (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0500 110 (original code) 18210501011013000110 (short code) |

| Tax levied on taxpayers who have chosen income as the object of taxation (for tax periods expired before January 1, 2011) (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0500 110 (original code) 18210501012011000110 (short code) |

| Tax levied on taxpayers who have chosen income as the object of taxation (for tax periods expired before January 1, 2011) (penalties on the corresponding payment) | 182 1 0500 110 (original code) 18210501012012100110 (short code) |

| Tax levied on taxpayers who have chosen income as the object of taxation (for tax periods expiring before January 1, 2011) (interest on the corresponding payment) | 182 1 0500 110 (original code) 18210501012012200110 (short code) |

| Tax levied on taxpayers who have chosen income as an object of taxation (for tax periods expired before January 1, 2011) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0500 110 (original code) 18210501012013000110 (short code) |

| Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled payments) | 182 1 0500 110 (original code) 18210501021011000110 (short code) |

| Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) (penalties on the corresponding payment) | 182 1 0500 110 (original code) 18210501021012100110 (short code) |

| Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) (interest on the corresponding payment) | 182 1 0500 110 (original code) 18210501021012200110 (short code) |

| A tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) (the amount of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0500 110 (original code) 18210501021013000110 (short code) |

| Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0500 110 (original code) 18210501022011000110 (short code) |

| Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (penalties on the corresponding payment) | 182 1 0500 110 (original code) 18210501022012100110 (short code) |

| Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (interest on the corresponding payment) | 182 1 0500 110 (original code) 18210501022012200110 (short code) |

| Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0500 110 (original code) 18210501022013000110 (short code) |

| Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) | 182 1 0500 110 (original code) 18210501030011000110 (short code) |

| Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (penalties on the corresponding payment) | 182 1 0500 110 (original code) 18210501030012100110 (short code) |

| Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (interest on the corresponding payment) | 182 1 0500 110 (original code) 18210501030012200110 (short code) |

| Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0500 110 (original code) 18210501030013000110 (short code) |

| Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (payment amount (recalculations, arrears and debt) for the corresponding payment, including canceled ones) | 182 1 0500 110 (original code) 18210501050011000110 (short code) |

| Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (penalties on the corresponding payment) | 182 1 0500 110 (original code) 18210501050012100110 (short code) |

| Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (interest on the corresponding payment) | 182 1 0500 110 (original code) 18210501050012200110 (short code) |

| Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) | 182 1 0500 110 (original code) 18210501050013000110 (short code) |

simplified tax system income minus expenses

When choosing the simplified taxation system for income minus expenses, a commercial structure has a number of advantages. This primarily affects the maintenance of documentation and the tax itself, which is reduced. The usual rate for this tax regime is 15%, but at the regional level it can be reduced to 5%.

Initially, when you get acquainted with this system, it may seem that there is no more comfortable system for paying taxes in Russia. However, the attractiveness of the system can be said after a certain period when the entrepreneur has worked in business.

You can consider in more detail how attractive the system will be for your specific case. To calculate what tax a businessman will have to pay under KBK 18210501021011000110, he will need to subtract the company's expenses from the profit.

Of course, there is a risk that tax authorities will not accept a specific expense declared in the declaration. And then a fine and penalties in the amount of 20% of the unpaid amount of the debt will be imposed.

For example, let’s look at how tax is calculated according to this taxation system. LLC "Vesna" on the simplified tax system (income minus expenses), in the declaration indicated a profit in the amount of 500,000 and expenses for the development of the enterprise amounted to 250,000. The total, according to the taxpayer, the tax was:

500,000-250,000*15% = 37,500. The following items were included in expenses:

- Office rent – 50,000;

- Warehouse rental – 100,000;

- Employee communications – 10,000;

- Purchase of materials for production – 90,000.

The taxman did not include employee communications as expenses, so the tax amount was 39,000 rubles. The arrears amounted to 300 rubles (1500*20%). Therefore, in addition to the amount of the basic tax, you will also need to pay the arrears.

Now the company will have to fill out a payment order for arrears and penalties. They have their own BCCs, which are indicated on the receipt.

If a commercial structure is interested in decoding in 2021, KBK 18210501021011000110, then you can look at the classification codes in the directory, and there you will see that this tax is paid by simplifiers who have chosen the income minus expenses system to calculate the tax.

Penalty simplified taxation system income minus expenses

Often in a businessman’s entrepreneurial activity, not everything goes smoothly and smoothly. Errors, punctures and various force majeure situations happen. But government agencies do not forgive carelessness and mistakes. If you receive a letter demanding to pay tax, and KBK 18210501021012100110 is indicated, then you have found a mistake in the company, and you need to urgently deal with it.

What to expect in 2021 simplified tax system

Every year we expect innovations, and this year was no exception. First of all, this will affect the income limit for the transition to a simplified system. Online cash registers will be introduced, new reporting forms will be added, and probably the biggest change will be the change of regulatory authorities.

Now the reporting of the Pension Fund and the Social Insurance Fund will go to the tax authorities. This will naturally lead to a change in the BCC in the payment order. And mandatory insurance contributions that were paid to the pension fund and social security. fear (except for injuries) will need to be paid to the tax office.

Therefore, all commercial structures will need to be extremely careful when paying fees and taxes. Carefully check the BCC in the payment slip so that the transfers reach the regulatory authority without delays or delays. So that the company does not face additional sanctions and unnecessary financial expenses.

The relevance of classification codes can be checked in a special directory, which is published on the official website of the tax service. There you can learn about new changes in legislation.

Why are the BCCs different for the simplified tax system?

Each classification code is responsible for its structure, for a certain type of tax, for state. the authority where the money is sent, and for many things upon closer examination. Therefore, those who simplify the system (income minus expenses) can use the BCC given in the table.

Almost every year, legislators make various changes to laws. And changes that concern the classification codes themselves do not remain aside. They are the current account of each budget organization; with the help of this set of numbers, funds quickly reach the recipient.

When filling out the next payment document for payment of the main tax, a merchant can use either one or the second BCC, and this will be considered correct. There is no doubt that the money will arrive. But, if you don’t want to tempt fate, then it’s worth checking the relevance of the current BCC in a special directory of classification codes.

In addition, there is no need to confuse what is being paid at the moment, tax, fine or penalty. This is where an error may occur if you enter just one digit incorrectly. Then, on the basic tax, there may be a fine for late payment and penalties will be charged for each day of delay.

KBC in 2021-2021: table of insurance premiums

Our KBK table in 2021-2021 reflects information regarding insurance premium codes that are most in demand among payers.

KBK for insurance premiums for employees

| Payment type | KBK | ||

| Contributions accrued for periods before 2021, paid after 01/01/2017 | Contributions for 2017-2021 | ||

| Contributions to compulsory pension insurance | contributions | 182 1 0200 160 | 182 1 0210 160 |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions to compulsory social insurance | contributions | 182 1 0200 160 | 182 1 0210 160 |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions for compulsory health insurance | contributions | 182 1 0211 160 | 182 1 0213 160 |

| penalties | 182 1 0211 160 | 182 1 0213 160 | |

| fine | 182 1 0211 160 | 182 1 0213 160 | |

| Contributions for injuries | contributions | 393 1 0200 160 | |

| penalties | 393 1 0200 160 | ||

| fine | 393 1 0200 160 | ||

KBK for insurance premiums of individual entrepreneurs

| Payment type | KBK | ||

| Contributions accrued for periods before 2021, paid after 01/01/2017 | Contributions for 2017-2021 | ||

| Fixed contributions to the Pension Fund, including contributions | contributions | 182 1 0200 160 | 182 1 0210 160* *Unified BCC for the fixed part and contributions from income over 300,000 rubles. valid from 04/23/2021 |

| Contributions to the Pension Fund of the Russian Federation 1% on income over 300,000 rubles. | contributions | 182 1 0200 160 | |

| penalties | 182 1 0200 160 | 182 1 0210 160 | |

| fine | 182 1 0200 160 | 182 1 0210 160 | |

| Contributions for compulsory health insurance | contributions | 182 1 0211 160 | 182 1 0213 160 |

| penalties | 182 1 0211 160 | 182 1 0213 160 | |

| fine | 182 1 0211 160 | 182 1 0213 160 | |

Budget classification codes for taxes for 2021-2021

The BCCs for the taxes indicated in the tables below have not changed in recent years (the same for 2021 and 2021). So that you can easily and quickly find the CBC you need (among the most popular ones), we have divided them into groups:

KBK table for personal income tax for 2021-2021

| Personal income tax on employee income | 182 1 0100 110 |

| Penalties for personal income tax on employee income | 182 1 0100 110 |

| Personal income tax fine on employee income | 182 1 0100 110 |

| Personal income tax on individual entrepreneur income on OSNO | 182 1 0100 110 |

| Penalties for personal income tax on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

| Personal income tax fine on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

KBK income tax table

| Purpose of payment | Mandatory payment | Penalty | Fine |

| To the federal budget (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the federal budget (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 11 |

| When implementing production sharing agreements concluded before October 21, 2011 (before the law of December 30, 1995 No. 225-FZ came into force) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations not related to activities in Russia through a permanent representative office | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies |

KBK for VAT

| Payment type | Tax | Penalty | Fine |

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

What to do if KBK made a mistake when paying a tax or contribution? Find out the answer to this question in the Ready-made solution from ConsultantPlus by receiving free trial access to the system.

BCC 2021-2021 for special regimes (simplified taxation, imputation, patent, agricultural tax), trade tax and tax on gambling business will be as follows:

| Name KBK 2021-2021 | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Single tax under the simplified tax system “income” | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax under the simplified tax system “income minus expenses” (including minimum tax) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| UTII | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Unified agricultural tax | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Trade fee | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (city district budget) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (municipal district budget) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (for residents of Moscow, St. Petersburg, Sevastopol) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Gambling tax | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

BCC for property taxes (transport, land, property tax)

| Name of KBK | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Transport tax for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Transport tax for individuals | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for legal entities (for Moscow, St. Petersburg, Sevastopol) | 182 1 06 06 031 03 1000 110 | 182 1 06 06 031 03 2100 110 | 182 1 06 06 031 03 3000 110 |

| Land tax within the boundaries of urban districts for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of inter-settlement territories for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of rural settlements for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of urban settlements for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of urban districts with intra-city division for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of intracity districts for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax for individuals (for Moscow, St. Petersburg, Sevastopol) | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of rural settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of urban settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of organizations (not included in the unified gas supply system) | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of organizations included in the unified gas supply system | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

There are a number of changes in the BCC for excise duties, but the main codes remain the same:

| Name of KBK | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Excise taxes on ethyl alcohol produced in Russia from food raw materials (except for those listed in the following paragraphs) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol produced in Russia from food raw materials (distillates of wine, grape, fruit, cognac, Calvados, whiskey) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol produced in Russia from non-food raw materials | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian-made alcohol-containing products | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian beer | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian alcoholic products with an ethyl alcohol content of more than 9% (except for beer and various wines) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian alcoholic products with a share of ethyl alcohol up to 9% (except for beer and various wines) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian wines | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian motor gasoline | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian diesel fuel | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

What is the budget classification code for TC activities

Regardless of the specific type of activity for which the trade tax (TC) is paid, be it, for example, stationary or delivery trade, the same BCCs are used.

The same can be said about the organizational and legal form of business. BCC for individual entrepreneurs and legal entities under the vehicle are the same. The BCC of the trade fee in 2021 is as follows:

- for the main payment: 18210505010021000110;

- penalty: 18210505010022100110;

- fine: 18210505010023000110.

The specified codes are subject to application in Moscow and other cities of federal significance (if they collect a trade tax in 2021, but there are no official statements about this from the authorities yet).

Correct indication of the 2021 BCC trade fee in the payment order (field 104) is highly desirable. Let's explore why.

How to calculate and pay the trading fee is described in the ready-made solution “ConsultantPlus”. You will receive even more relevant information if you sign up for a free trial access to K+.

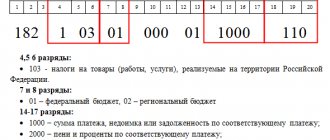

Decoding of KBK 18210501012010000110 in 2021 and 2021

In the article we will look at KBK 18210501012010000110: what tax entrepreneurs will be able to transfer under it, what codes to indicate when paying fines and penalties

The code represents information responsible for the reason for transferring the payment: main, penalty or fine. The decoding of KBK 18210501012010000110, presented in the table, will help determine what tax a businessman can transfer to the budget

| Digit p/p | What is encoded | Decoding |

| 1–3 | payment receiver | 182 - Federal Tax Service |

| 4 | cash receipt group | 1 - income |

| 5–6 | tax code | 05 - tax on total income |

| 7–11 | state budget item code | 01012 - taxes according to the simplified tax system “income” until 2011. |

| 12–13 | budget ownership | 01 — Federal budget |

| 14–17 | reason for payment | 0000 - combined form to clarify the reason for the transfer:

|

| 18–20 | state budget income category | 110 - tax |

It follows from the table that the BCC is used to transfer tax under the simplified tax system “income”.

KBK 18210501012010000110 was canceled in 2011 for application for subsequent periods; what code is now in effect for transferring tax, fines and penalties, see the table:

| Year | Tax | Penalty | Fine |

| 2021 | 18210501011011000110 | 18210501011012100110 | 18210501011013000110 |

| 2021 | 18210501011011000110 | 18210501011012100110 | 18210501011013000110 |

Other KBK from this category:

| 18210501011011000110 | Tax levied on taxpayers who have chosen income as the object of taxation (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210501011012100110 | Tax levied on taxpayers who have chosen income as an object of taxation (penalties on the corresponding payment) |

| 18210501011012200110 | Tax levied on taxpayers who have chosen income as the object of taxation (interest on the corresponding payment) |

| 18210501011013000110 | Tax levied on taxpayers who have chosen income as an object of taxation (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210501012011000110 | Tax levied on taxpayers who have chosen income as the object of taxation (for tax periods expired before January 1, 2011) (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210501012012100110 | Tax levied on taxpayers who have chosen income as the object of taxation (for tax periods expired before January 1, 2011) (penalties on the corresponding payment) |

| 18210501012012200110 | Tax levied on taxpayers who have chosen income as the object of taxation (for tax periods expiring before January 1, 2011) (interest on the corresponding payment) |

| 18210501012013000110 | Tax levied on taxpayers who have chosen income as an object of taxation (for tax periods expired before January 1, 2011) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210501021012100110 | Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) (penalties on the corresponding payment) |

| 18210501021012200110 | Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) (interest on the corresponding payment) |

| 18210501021013000110 | A tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (including the minimum tax credited to the budgets of the constituent entities of the Russian Federation) (the amount of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210501022011000110 | Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210501022012100110 | Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (penalties on the corresponding payment) |

| 18210501022012200110 | Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (interest on the corresponding payment) |

| 18210501022013000110 | Tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses (for tax periods expired before January 1, 2011) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210501030011000110 | Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (payment amount (recalculations, arrears and debt on the corresponding payment, including canceled ones) |

| 18210501030012100110 | Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (penalties on the corresponding payment) |

| 18210501030012200110 | Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (interest on the corresponding payment) |

| 18210501030013000110 | Minimum tax credited to the budgets of state extra-budgetary funds (paid (collected) for tax periods expired before January 1, 2011) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

| 18210501050011000110 | Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (payment amount (recalculations, arrears and debt) for the corresponding payment, including canceled ones) |

| 18210501050012100110 | Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (penalties on the corresponding payment) |

| 18210501050012200110 | Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (interest on the corresponding payment) |

| 18210501050013000110 | Minimum tax credited to the budgets of the constituent entities of the Russian Federation (for tax periods expired before January 1, 2021) (amounts of monetary penalties (fines) for the corresponding payment in accordance with the legislation of the Russian Federation) |

Why do tax authorities impose fines?

Any simplified documentary reporting has a certain deadline for delivery. There are also deadlines for paying taxes and insurance premiums. And the first thing tax inspectors can fine you for is if the tax has not been paid or the declaration has not been submitted.

Every quarter, simplified taxpayers pay another tax; it is transferred every reporting quarter until the 25th. Before the 20th, a tax return is submitted, where the tax that must be paid is calculated. If you miss the deadlines, then you need to be prepared to accrue fines and penalties.

The penalty is charged immediately on the first day of delay. For example, if you need to pay a tax on the 25th of the reporting quarter, and its payment is made on another day, then starting from the 26th a penalty is accrued, and it accrues every day until the principal debt is repaid.

What tax 2021 KBK 18210501021012100110 should a taxpayer pay? The full decoding sounds like this - a tax levied on a simplified taxpayer who has chosen income to reduce expenses (tax penalties). So, now we know that under this BCC the organization needs to pay a penalty. How to calculate penalties correctly?

Correctness of penalty calculation

To correctly calculate penalties, you need to rely on the Central Bank refinancing rate.

This must be paid on the day when the next payment is planned to be made, so that penalties are not charged again. The calculation is taken inclusive of the day on which the principal debt is paid.

For example, you are 4 days late in payment. It was necessary to pay on the 25th, but the payment is made on the 29th, which means you also need to count the 29th.

But in addition to penalties, you will need to pay both a fine and basic tax. That is, you will have to fill out three payment orders, and there should be different BCCs everywhere. This must always be remembered.

KBK penalties

Explanation 2021 KBK 18210501021012100110 - what tax does it imply? This is a penalty for taxpayers who have failed. In field “104” (filled in on the payment slip) you will need to indicate this particular BCC. To fill out payment orders for simplifiers (income minus expenses) for taxes and fines, the following classification codes should be used:

- Code 18210501021011000110 – for payment of the basic tax for simplified people.

- Code 18210501021013000110 – transfer of sanctions in the form of a fine for late payment of tax.

Therefore, the taxpayer needs to be extremely careful when filling out payment documents. After all, any mistake in the KBK will already cause additional sanctions for the company. And it is advisable to comply with all the deadlines prescribed in the Tax Code, so as not to give rise to additional fines being applied to you.

Where are penalties and fines paid? After filling out the payment document, you can go to the bank, where the operator will accept your payment, or you can use the Client Bank, if it is connected to your organization. Through the client bank, payment documents and the amounts themselves are written off instantly. The program is configured so that it automatically checks all payment details without making errors.

In this case, you can be sure that even if you made a mistake, the program will report it and offer to correct it.

KBK penalties

Explanation 2021 KBK 18210501021012100110 - what tax does it imply? This is a penalty for taxpayers who have failed. In field “104” (filled in on the payment slip) you will need to indicate this particular BCC. To fill out payment orders for simplifiers (income minus expenses) for taxes and fines, the following classification codes should be used:

- Code 18210501021011000110 – for payment of the basic tax for simplified people.

- Code 18210501021013000110 – transfer of sanctions in the form of a fine for late payment of tax.

Therefore, the taxpayer needs to be extremely careful when filling out payment documents. After all, any mistake in the KBK will already cause additional sanctions for the company. And it is advisable to comply with all the deadlines prescribed in the Tax Code, so as not to give rise to additional fines being applied to you.

Where are penalties and fines paid? After filling out the payment document, you can go to the bank, where the operator will accept your payment, or you can use the Client Bank, if it is connected to your organization. Through the client bank, payment documents and the amounts themselves are written off instantly. The program is configured so that it automatically checks all payment details without making errors.

In this case, you can be sure that even if you made a mistake, the program will report it and offer to correct it.