Receiving a bill of exchange from the buyer

When receiving a bill of exchange as payment for goods (work, services), when calculating VAT, please take into account:

- the amount of debt paid by the bill;

- interest or discount on the bill (if provided).

Determine the moment at which VAT must be charged on the cost of goods (work, services) paid for by bill of exchange.

VAT must be charged for payment to the budget in relation to all transactions recognized as an object of taxation, the moment of determining the tax base of which relates to the corresponding tax period (clause 4 of Article 166 of the Tax Code of the Russian Federation).

The moment of determining the tax base for the purpose of calculating VAT is the earliest of the following dates:

- day of shipment (transfer) of goods (performance of work, provision of services);

- day of payment, partial payment on account of upcoming deliveries of goods (performance of work, provision of services).

This is stated in paragraph 1 of Article 167 of the Tax Code of the Russian Federation.

Thus, VAT must be accrued for payment to the budget either on the day of shipment (transfer) of goods (performance of work, provision of services), or on the day of their payment - depending on which of these events occurred earlier.

If the goods were shipped (work performed, services provided) before the transfer of the bill of exchange, calculate VAT at the time of shipment (fulfillment, provision). At the same time, make the following entry in accounting:

Debit 90-3 (91-2) Credit 68 subaccount “VAT calculations”

– VAT is charged on sales proceeds.

For more information on how to calculate VAT on sales proceeds, see How to calculate VAT on the sale of goods (works, services).

If the bill of exchange was received before the goods were shipped (work performed, services provided), the procedure for calculating VAT will depend on which bill of exchange was received: the buyer’s (customer’s) own bill of exchange or a third party’s bill of exchange.

Optimization of VAT using bills of exchange

Magazine "Financial Director" No. 2, August, 2002www.fdir.ru https://www.fdir.ru/article/1246.htmlAuthor: Sergey Aldokhin (Head of Tax Consulting Department, BrokerCreditService Consulting LLC)

Most businesses need to pay VAT on a monthly basis. Therefore, an important element of tax planning for VAT is not only reducing the amount of this tax, but also regulating the timing of its payment to the budget. The use of bills allows the seller to carry out such regulation, and the buyer to timely apply the tax deduction.

When purchasing a product, the buyer usually pays the seller its cost, including VAT. After the transfer of ownership of the paid goods1, the buyer has the right to present the VAT paid to the seller for deduction, that is, to reduce the amount of tax payable to the budget (clause 2 of Article 171 of the Tax Code of the Russian Federation).

The seller (whose accounting policy for the purpose of calculating VAT is set “on payment”), when receiving funds from the buyer for goods (work, services) sold, is obliged, after the expiration of the tax period (month), to increase the amount of VAT due to the budget by the amount of tax paid by the buyer . However, it is not always profitable for the seller to pay VAT within these deadlines. To solve this problem, the “bill scheme”2 is used.

Settlements with bills of exchange: who benefits from it?

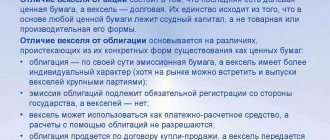

The buyer can pay the seller using bills of exchange. Payments by bill of exchange are always associated with the transfer of ownership of the bill of exchange, which is usually transferred under an agreement, for example, a purchase and sale agreement.

In transactions of purchase and sale of bills of exchange (which are securities), there is no subject to VAT (subclause 12, clause 2, article 149 of the Tax Code of the Russian Federation).

At the same time, settlements with bills of exchange are not always beneficial for the seller and the buyer from a tax point of view. To see this, consider the tax consequences of settlements with a buyer's bill of exchange and a third party's bill of exchange.

Payments by buyer's bill

According to tax legislation, the buyer’s obligations to pay for purchased goods terminate after payment (clause 2 of article 167 of the Tax Code of the Russian Federation). In particular, payment is considered to be a set-off of mutual claims.

Let us now consider the situation when payment is made by a buyer's bill. Let us note that when issuing its own bill of exchange, the buyer does not have obligations to calculate and pay any taxes. If the buyer pays with his own bill of exchange (or with a bill of exchange of a third party received in exchange for his own bill of exchange), then the goods are considered paid:

- from the seller - at the time the buyer repays his bill of exchange (that is, upon presentation of the bill of exchange for payment) or at the time of transfer of this bill of exchange by the seller to a third party by endorsement (clause 4 of Article 167 of the Tax Code of the Russian Federation);

- from the buyer - at the time of repayment of his own bill (clause 2 of article 172 of the Tax Code of the Russian Federation).

Thus, the very fact of the buyer transferring his own bill of exchange (or a bill of exchange of a third party received in exchange for his own bill of exchange) to pay for goods does not give him the right to apply a tax deduction for VAT (clause 2 of Article 172 of the Tax Code of the Russian Federation).

For the seller, this situation is ambiguous. On the one hand, he has a deferment in calculating tax for the entire time the bill is in his possession, or until the bill is paid (clause 4 of Article 167 of the Tax Code of the Russian Federation), and on the other hand, until the bill is redeemed or sold, he does not receive money for goods sold.

Payments by bill of exchange of a third party

If the buyer pays for the purchased goods with a bill of exchange from a third party, then after transferring the bill of exchange, the buyer can accept VAT as a deduction (clause 2 of Article 172 of the Tax Code of the Russian Federation). In this case, the amount of tax deduction is determined based on the book value of the bill.

The seller, upon receipt of a bill of exchange from a third party, must charge VAT for payment to the budget (clause 2 of Article 167 of the Tax Code of the Russian Federation), although the money on this bill has not been received by him. Obviously, settlements with a third party bill of exchange are not profitable for the seller.

Thus, when paying by bill of exchange directly between the buyer and seller, the interests of both parties (from the point of view of tax optimization) do not coincide: either the buyer cannot accept VAT as a deduction, or the seller is obliged to charge VAT for payment to the budget (although the money from the transaction does not go to him arrived).

However, a transaction option is possible when the interests of both the buyer and the seller are taken into account. The scheme discussed below allows the buyer to legally claim tax as a deduction, and the seller, upon actual receipt of payment, to avoid immediate tax accrual3.

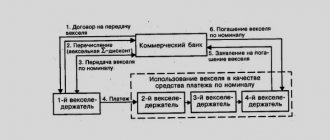

VAT optimization scheme using bills of exchange

The scheme involves the seller of goods, the buyer, as well as two organizations “A” and “B”, used as so-called settlement centers. These can be firms specially created to carry out such operations, or firms that make money from the sale of bills (making a profit on the difference between the purchase price and the sale (redemption) of the bill)4.

So, the buyer purchased the goods, but did not pay for it (see figure, action 1). In this case, ownership of the goods passed to the buyer, he had accounts payable (10), and the seller had accounts receivable.

Further calculations are carried out as follows. The seller, as the drawer of the bill, draws up his own promissory note in the name of enterprise “A” (as the holder of the bill, 2). This enterprise sells the bill to the buyer (3). The buyer pays for the purchase of a bill of exchange (in fact, this is payment for the purchased goods, 4). Enterprise “A” transfers the funds received from the buyer to the seller for the issued bill of exchange (5). Thus, the seller actually received payment for the goods sold, while the receipt of funds did not lead to the formation of any obligations to pay taxes. Enterprise “A” also does not have any tax obligations.

Next, the buyer, under the purchase and sale agreement, sells the bill received from enterprise “A” to enterprise “B” (6), and also transfers the debt to the seller in compliance with all the conditions established by law (§ 2 of Chapter 24 of the Civil Code of the Russian Federation) (7).

At the moment of debt transfer, the buyer loses his obligation to the seller and becomes a debtor of organization “B”. In other words, now the obligation to pay for the goods received binds the buyer to organization “B”. However, enterprise “B” incurred a debt to the buyer for the purchased bill. Carrying out netting (a bill of exchange in exchange for a debt gives the buyer the right to apply a tax deduction for VAT for the amount of the book value of the transferred bill of exchange (clause 2 of Article 172 of the Tax Code of the Russian Federation).

In other words, now the obligation to pay for the goods received binds the buyer to organization “B”. However, enterprise “B” incurred a debt to the buyer for the purchased bill. Carrying out netting (a bill of exchange in exchange for a debt gives the buyer the right to apply a tax deduction for VAT for the amount of the book value of the transferred bill of exchange (clause 2 of Article 172 of the Tax Code of the Russian Federation).

As a result of the above transactions, enterprise “B” received a bill of exchange from the seller and a debt to him for the goods delivered to the buyer.

Now, at the moment when the seller has available funds to pay tax payments, as well as the desire to pay them, enterprise “B” presents the bill for redemption (9) with subsequent offset of mutual claims (10). When carrying out offset (10), the seller’s receivables associated with the supply of goods are repaid and the obligation to charge VAT5 arises.

If enterprise “B” does not make a profit from its operations, then it does not have tax consequences from participating in this scheme. Otherwise, it will have to pay tax on the profits received. As a result, the seller, in agreement with organization “B”, determines the timing of payment of VAT to the budget (regardless of the moment of actual payment for goods sold). The period within which the buyer will be able to accept VAT for deduction depends on the moment at which the buyer decides to offset with organization “B”.

Let's look at the above diagram using a specific example.

Example

For convenience, the example considers only the calculation of VAT (without taking into account income tax), and therefore the transfer of the bill is carried out at face value. The accounting policy for VAT purposes for the seller and the buyer is established as funds are received.

The buyer, under a purchase and sale agreement, acquired ownership of goods from the seller in the amount of 120,000 rubles. (including VAT - 20,000 rubles) (1).

If the tax scheme is not used, then:

- the seller, after receiving payment for the shipped goods, charges VAT payable to the budget in the amount of 20,000 rubles;

- After paying for the purchased goods, the buyer has the right to a VAT deduction in the amount of 20,000 rubles.

Obviously, with this method of payment, the seller is in a “disadvantageous” position, since he is obliged to pay VAT in the tax period in which payment for the goods supplied was received.

We apply the tax scheme

The seller draws up his own interest-free promissory note with a nominal value of 120,000 rubles in the name of organization “A”. and transfers it for 120,000 rubles. (2). The due date for a bill of exchange can be determined “at sight”.

When receiving funds for the transfer of a security (bill of exchange) (5), VAT will not have to be paid (subclause 12, clause 2, article 149 of the Tax Code of the Russian Federation).

Organization “A”, under an agreement for the purchase and sale of securities (by endorsement - endorsement), sells the seller’s bill of exchange (3) to the buyer for 120,000 rubles. (4).

Since the sale of securities is a transaction not subject to VAT, there are no tax consequences.

The buyer, with the consent of the seller (creditor), enters into an agreement with organization “B” for the transfer of debt to the seller in the amount of 120,000 rubles. (7) with the simultaneous sale of the seller’s bill of exchange at a nominal value of RUB 120,000. (6).

When transferring the debt and transferring the seller’s bill of exchange to enterprise “B” (that is, during offset, the buyer can make a tax deduction on the purchased goods in the amount of 20,000 rubles.

Organization “B”, having a debt to the seller in the amount of 120,000 rubles, presents the seller (the drawer) with a bill for repayment in the amount of 120,000 rubles. (9). Since organization “B” and the seller have homogeneous (monetary) claims against each other, offset of these claims is possible (10). In this case, no tax consequences arise, since the operation of repaying the bill of exchange is not subject to VAT.

For the seller, the period for offset is the moment of determining the tax base for VAT in the amount of 20,000 rubles.

It should be noted that in the above scheme, for making payments, you can use not only the seller’s own bills of exchange, but also bills of any other drawers (third parties).

In addition, for receivables accumulated by the seller to enterprise “B”, the seller can create a reserve for doubtful debts. Amounts of contributions to this reserve are included in non-operating expenses that reduce income for income tax purposes. The amount of the reserve depends on the period of occurrence of doubtful debts. Thus, for doubtful debts exceeding 90 days, the entire debt is included in the reserve amount; for debts from 45 to 90 days (inclusive) - only in the amount of 50%; and for debts less than 45 days, its amount does not increase the amount of the reserve. You also need to keep in mind that the amount of the created reserve cannot exceed 10% of the revenue of the reporting period (Article 266 of the Tax Code of the Russian Federation).

Scheme reliability assessment

Rustem Akhmetshin, partner of the legal

The disadvantage of schemes aimed at tax optimization is usually the same: they are based on imaginary or pretend transactions6. Thus, the main question when using the above scheme is how provable is the invalidity (based on the signs of pretense or imaginaryness) of the transactions being carried out.

First of all, we note that the scheme presented in the article fully complies with tax legislation. Proving the invalidity of transactions used in this scheme is not an easy task for the tax authorities.

Firstly, during a tax audit of the seller or buyer, the scheme itself is difficult to detect, because the seller’s bill of exchange is transferred to one organization (“A”), and returned through another organization (“B”), while the seller does not supply goods to organization “A”, nor organization "B". A similar situation with a bill arises for the buyer. This scheme is even more difficult to detect if it is not “put on stream”: the occasional use of the scheme against the backdrop of many unrelated transactions reduces the likelihood of its detection to almost zero.

Secondly, even if the inspection authorities suspect that any scheme is being used, they will have to check all four organizations participating in the scheme, which is very difficult to do.

Thirdly, the mere suspicion of a tax inspector (or a policeman) that a tax scheme is being applied is not enough both for the undisputed assessment of taxes and penalties (Clause 1 of Article 45 of the Tax Code of the Russian Federation), and for attracting the taxpayer to the tax office (and even more so criminal) liability (clause 7 of Article 114 of the Tax Code of the Russian Federation) - such decisions can only be made in court. This means that tax officials will have to prove in court the invalidity (imaginary or sham) of transactions carried out according to the scheme. In our case, they have to prove that transactions involving the transfer of the seller’s bill of exchange were concluded not for the purpose of creating bill of exchange legal relations, but for the purpose of tax optimization.

If the participants of the scheme are not interdependent persons (Article 20 of the Tax Code of the Russian Federation), and the organizations “A” and “B” participating in the scheme receive at least a small profit from transactions with the bill of exchange (they sell the bill of exchange for more than they purchase), then prove the invalidity of these transactions almost impossible.

1 The buyer’s ownership of a thing arises from the moment of its transfer, unless otherwise provided by law or contract (Article 223 of the Civil Code of the Russian Federation). 2 To simplify the scheme, operations for the sale of goods will be considered, however, the recommendations given are also valid for the sale of work or services. 3 It should be noted that the scheme is applicable only to enterprises with an accounting policy for the purpose of calculating VAT as funds are received. 4 This article does not consider a similar situation, since in this case an object of taxation for profit tax arises (Article 247 of the Tax Code of the Russian Federation), and this tax is not the subject of analysis in this scheme. 5 See clause 39.3 of the order of the Ministry of Taxes of Russia of December 20, 2000 No. BG-3-03/447. 6 On the concept of an imaginary and feigned transaction, see the article “Tax planning = tax optimization”, “Financial Director”, 2002, No. 1, p. 31.

Published according to legal information: https://www.fd.ru/info/1533.html

Buyer's own bill

The buyer’s (customer’s) own bill of exchange, received before the shipment of goods (performance of work, provision of services), is not considered receipt of payment (including advance payment (partial payment)). In this case, VAT will be charged only when one of the following events occurs:

- actual payment has been received on your own bill of exchange;

- own bill of exchange is transferred to a third party;

- goods (work, services) have been shipped (performed, provided).

This procedure follows from paragraph 1 of Article 154 and paragraph 1 of Article 162 of the Tax Code of the Russian Federation. This is explained by the fact that your own bill only confirms the obligation to pay the resulting debt (Article 815 of the Civil Code of the Russian Federation) and (or) delays the date of payment (Article 823 of the Civil Code of the Russian Federation). Until the buyer's own note is paid (or transferred to a third party), the payment obligation is considered outstanding.

Attention: some courts recognize that, having received the buyer's own bill of exchange as an advance, the seller must charge VAT. Subsequently, if the contract is terminated and the seller returns the bill, he will have the right to deduct the VAT paid on the advance payment. Such conclusions are contained, in particular, in the resolution of the Federal Antimonopoly Service of the Moscow District dated May 30, 2013 No. A40-85003/12-20-462.

VAT on interest and discount received on a bill of exchange

Question: Is interest charged to VAT on a commercial loan issued to a buyer, executed by a bill of exchange?

Answer: According to Art. 162 of the Tax Code of the Russian Federation, amounts received in the form of interest (discount) on bills of exchange, interest on a trade loan in the part exceeding the amount of interest calculated in accordance with the refinancing rate of the Central Bank of the Russian Federation are subject to VAT. When applying this provision, it should be taken into account that amounts received in the form of interest (discount) in excess of the amount of interest calculated in accordance with the refinancing rate of the Central Bank of the Russian Federation are subject to taxation.

The definition of interest (discount) for tax purposes is enshrined in Art. 43 of the Tax Code of the Russian Federation:

“Interest is recognized as any pre-declared (established) income, including in the form of a discount, received on a debt obligation of any type (regardless of the method of its execution). In this case, interest is recognized, in particular, on income received from cash deposits and debt obligations.”

Based on the analysis of this norm, it follows that the main criterion in determining interest is the sign of preliminary declaration of income.

In fact, an additional tax rule has been introduced in relation to bills of exchange as a type of securities, since in accordance with sub-clause. 12 paragraph 2 art. 149 of the Tax Code of the Russian Federation, the sale of securities and derivatives instruments (including forwards, futures contracts, options) is exempt from taxation.

Consequently, carrying out ordinary transactions for the purchase (receipt as payment) and sale of bills of exchange with the receipt of income that was not declared in advance does not entail the payment of VAT.

In addition, the obligation to tax income in accordance with Art. 162 of the Tax Code of the Russian Federation applies only to those receipts that are associated with the formation of the taxable base for VAT in accordance with Art. 153-158 of the Tax Code of the Russian Federation. If these receipts are related to transactions that are not subject to taxation, then the provisions of Art. 162 of the Tax Code of the Russian Federation should not be applied.

For example, an enterprise will purchase a bill of exchange from a bank with the interest indicated on it and, when the due date arrives, present the bill for redemption. In this case, the obligation to pay VAT does not arise, since the receipt of interest is not related to payments for goods (work, services), but relates to a borrowing transaction, which, in accordance with subparagraph. 12 clause 2 and sub. 15 clause 3 art. 149 of the Tax Code of the Russian Federation is exempt from taxation. If in the same case the bill is interest-free, but upon its redemption additional income is received, then it is also not subject to VAT.

In the case when an enterprise receives a bill of exchange with the interest specified in it from its buyer in connection with the supply of goods subject to VAT, then the specified interest income is subject to taxation in the prescribed manner (in comparison with the rate of the Central Bank of the Russian Federation). If in the same case the bill is interest-free, but upon its repayment additional income is received, then the VAT tax base should be increased by the amount of this income.

Bills of exchange and income tax

5.2.1. Tax accounting of amounts of “input” VAT that is not deductible under Art. 170 of the Tax Code of the Russian Federation, in the part related to transactions with securities

According to paragraph 2 of Art. 274 of the Tax Code of the Russian Federation, the taxpayer maintains separate accounting of income (expenses) for transactions for which, in accordance with this chapter, a different procedure for accounting for profit and loss is provided for.

In particular, Art. 280 of the Tax Code of the Russian Federation establishes the specifics of determining the tax base for transactions with securities.

According to paragraph 2 of Art. 280 of the Tax Code of the Russian Federation, expenses for the sale (or other disposal) of securities for tax purposes are determined in a special tax base based on:

— purchase price of a security, including expenses for its acquisition,

- costs for its implementation.

Expenses directly related to the acquisition and sale of securities may include expenses for the purchase of forms, payment for services of credit and other institutions, remuneration of intermediaries, payment for consulting and information services on transactions with securities, wages and maintenance of an employee’s workplace, including whose job responsibilities include working with the company’s securities, etc.

Since, for profit tax purposes, transactions with securities are a normal type of activity of the taxpayer aimed at generating income, then the economically justified part of the general business (administrative) expenses of the taxpayer, which falls on acquisition and sale operations, should be reflected as part of the expenses for transactions with securities valuable papers. A corresponding explanation is included in the Methodological Recommendations for the Application of Chapter 25 of the Tax Code of the Russian Federation.

According to paragraph 2 of Art. 170 of the Tax Code of the Russian Federation, the “input” VAT attributable to the specified general business expenses must be included in the cost of these goods (works, services). In other words, the indicated amounts of VAT do not create an independent expense item, but should be taken into account in the same way as accounting for goods (works, services) on which this VAT falls.

Thus, we believe that for profit tax purposes, the general business expenses in question and the “input” VAT attributable to them should be taken into account in the expenses of the special tax base for transactions with securities, formed in accordance with Art. 280 Tax Code of the Russian Federation.

This conclusion is also confirmed by the Letter of the Ministry of Taxes of the Russian Federation dated June 21, 2004 N 02-5-11 / [email protected] “On the application of the norms of Chapter 25 of the Tax Code of the Russian Federation.”

At the same time, according to clause 10 of Art. 280 of the Tax Code of the Russian Federation, taxpayers who received a loss (losses) from transactions with securities in the previous tax period or in previous tax periods have the right to reduce the tax base received from transactions with securities in the reporting (tax) period (carry forward these losses to the future) in in the manner and under the conditions established by Art. 283 Tax Code of the Russian Federation.

As already noted, all expenses associated with transactions with securities, including the corresponding part of general business expenses (and the “input” VAT attributable to them), cannot be taken into account as part of other expenses of the main tax base of the reporting period, since a special procedure is provided for these cases taxation (Article 280 of the Tax Code of the Russian Federation).

Thus, if the amount of expenses associated with the acquisition and sale of securities exceeds the income from such sale, such losses in the current tax period should not be taken into account for tax purposes. The taxpayer retains the right to carry forward these losses to the future (10 years).

However, the taxpayer also has the right, in order to minimize the accounting process, taking into account that these losses during the specified period with a high degree of probability will not be “covered” in whole or in part by profits from transactions with securities, to approve in the accounting policy a clause stating that these losses for the future are not transferred and are not taken into account for tax purposes.

Discount

Question: Should income be calculated for tax purposes in accordance with paragraph 1 of Art. 328 of the Tax Code of the Russian Federation on “discount” bills if these bills are on the balance sheet of the enterprise at the reporting date?

Answer: According to sub. 6 tbsp. 250 of the Tax Code of the Russian Federation, in particular, income in the form of interest received on securities and other debt obligations is recognized as non-operating income of the taxpayer.

According to paragraph 1 of Art. 328 of the Tax Code of the Russian Federation, the taxpayer independently reflects the amount of income on bills of exchange in the amount due in accordance with the terms of issue or transfer (sale) of interest separately for each type of debt obligation. In this case, the amount of income in the form of interest on debt obligations is taken into account based on the yield established for each type of debt obligation and the validity period of such debt obligation in the reporting period as of the date of recognition of income.

According to paragraph 6 of Art. 271 of the Tax Code of the Russian Federation for loan agreements and other similar agreements (other debt obligations, including securities), the validity of which falls on more than one reporting period, for the purposes of this chapter, income is recognized as received and is included in the corresponding income at the end of the corresponding reporting period. In the event of termination of the agreement (repayment of the debt obligation) before the expiration of the reporting period, income is recognized as received and is included in the relevant income on the date of termination of the agreement (repayment of the debt obligation).

When applying these norms of the Tax Code of the Russian Federation, the following points must be taken into account.

In accordance with paragraph 3 of Art. 43 of the Tax Code of the Russian Federation, for tax purposes, interest is recognized as any pre-declared (established) income, including in the form of a discount, received on a debt obligation of any type (regardless of the method of its execution).

As such, tax legislation does not contain a definition of the concept “discount”. Considering that, by virtue of Art. 11 of the Tax Code of the Russian Federation in this case, institutions, concepts and terms of other branches of legislation of the Russian Federation are subject to use, in particular, in accordance with clause 11 of PBU N 15/01 “Accounting for loans and credits and the costs of servicing them” (approved by order of the Ministry of Finance of the Russian Federation dated 02.08 .2001 N 60n) costs associated with obtaining and using loans and credits, including, inter alia, interest, discount on bills and bonds due for payment. At the same time, in relation to the circulation of bills in this PBU, a discount is understood as the difference between the amount specified in the bill and the amount of cash or cash equivalents actually received when placing this bill.

Based on this, in accounting, the discount, which is the difference between the nominal value of the bill and the amount actually received by the drawer when placing the bill, also applies to interest on debt obligations. At the same time, it should be taken into account that for profit tax purposes, in order to classify a discount as interest, it is additionally necessary that the income in the form of a discount be declared (established) in advance.

Thus, not any difference between the face value of a bill of exchange and its purchase price can be recognized as interest on a security from a tax point of view, but only that which is predetermined:

- either directly in the text of the bill (stated interest),

- or when completing a transaction.

In the second case, one should take into account the peculiarity of the placement of bills of exchange by ordinary (non-banking) commercial organizations, namely, the fact that, unlike issue-grade securities (stocks, bonds), bills of exchange can be placed not by issues (subject to appropriate registration), but for the execution of specific business transactions .

For example, an enterprise can issue one bill of exchange to receive a certain amount of money from a specific lender, then in this case the discount, in our opinion, can be considered as pre-declared if

a) the issuance of a bill of exchange is based on an agreement between the borrower (the first bill holder) and the lender (issuer of the bill), the subject of which is the attraction of borrowed funds with the condition that the borrower issue his own bill to the lender. However, we note that the law does not establish any special requirements for the form and content of such an agreement. As a consequence, such an agreement can be equated with both a purchase and sale agreement of one’s own bill of exchange and a loan agreement, which provides for the issuance by the borrower of one’s own bill of exchange to the lender to ensure the return of borrowed funds.

b) the agreement indicates, firstly, the nominal value of the bill of exchange being placed, and secondly, the amount of money actually received by the borrower (issuer of the bill) when placing his own bill of exchange (loan amount).

By the way, we note that the law does not establish any special requirements for the form and content of such an agreement. As a consequence, such an agreement can be equated with both the purchase and sale agreement of its own bill of exchange (which, by the way, is most often concluded by the parties in such situations and determines the above conditions), and the loan agreement, which provides for the issuance by the borrower of his own bill of exchange to the lender to ensure the return of the borrowed money. Money.

In a situation where a bill of exchange is transferred from the first bill holder to the second bill holder (i.e. in the situation considered in the question), in our opinion, it is unreasonable to say that the discount can be declared (established) in advance (except in cases when the interest is indicated directly in the text of the bill).

Thus, in our opinion, tax legislation does not contain a requirement for the need to calculate for tax purposes non-operating income in the form of interest on securities in accordance with clause 6 of Art. 250 and paragraph 1 of Art. 328 of the Tax Code of the Russian Federation in relation to bills of exchange of third parties purchased by a taxpayer (not the first bill holder) at a price below par if these bills are on the balance sheet of the enterprise as of the reporting date.

At the same time, tax authorities may take a different position.

So, when commenting on paragraph 6 of Art. 250 of the Tax Code of the Russian Federation, the Ministry of Taxation of the Russian Federation indicates that “the concept of debt obligations for the purposes of Chapter 25 of the Tax Code of the Russian Federation is given in Art. 269 of the Tax Code of the Russian Federation,” the application of which is explained in section 5.4.1. Methodological recommendations for the application of Chapter 25 “Income Tax of Organizations”, Part Two of the Tax Code of the Russian Federation (approved by Order of the Ministry of Taxes of the Russian Federation dated December 20, 2002. N BG-3-02/729). It states, in particular, that for the purposes of Chapter 25 of the Tax Code of the Russian Federation, when applying the provisions of Art. 269 of the Tax Code of the Russian Federation, borrowed funds are understood as borrowed funds received under one’s own debt obligations, issued in the form of securities. At the same time, it is clarified that securities are understood as “bills of exchange, bonds and other debt securities, for which, according to the terms of the placement, the accrual of interest (discount) income is provided.”

An expense is recognized (paragraph 2 of subclause 2 of clause 1 of Article 265 of the Tax Code of the Russian Federation) only the amount of interest accrued for the actual time of use of borrowed funds (the actual time that the specified securities are held by third parties) and the yield established by the issuer (lender). In case of early repayment of a debt obligation, interest is determined based on the interest rate stipulated by the terms of the agreement, taking into account the provisions of Article 269 of the Tax Code of the Russian Federation and the actual time of use of borrowed funds. The above procedure applies to early repayment of own debt obligations, including discount bills.

For discount bills with a maturity date of “at sight, but not earlier,” the expense (discount) in the form of interest is determined from the date the bill is drawn up. To calculate the discount on bills of exchange with the clause “upon sight, but not earlier”, the estimated maturity of the bill of exchange, determined in accordance with bill of exchange legislation, is used as the circulation period on the basis of which the discount at the end of the reporting period is determined (365 (366) days plus the term from the date of drawing up the bill of exchange to the minimum date of presentation of the bill of exchange for payment).

In other words, in our opinion, the specified clarifications of the tax authorities relate only to the circulation of bills in the connection “the drawer - the first bill holder”, therefore, in our opinion, in the situation given in the request, they should not be applied.

However, for example, in the Letter of the Ministry of Taxes of the Russian Federation dated September 5, 2003 No. VG-6-02 / [email protected] “On issues related to the application of Chapter 25 of the Tax Code of the Russian Federation,” the following is literally explained:

“Thus, for secondary bill holders, the pre-declared income on discount bills will be the income calculated based on the purchase price and the face value of the bill.

Since this income is equivalent to interest, it must also be accounted for on an accrual basis by taxpayers using the accrual method when forming the tax base in accordance with the provisions of Chapter 25 of the Tax Code.”

Bills and Art. 40 Tax Code of the Russian Federation

Question: When carrying out financial and economic activities, the JSC receives, in payment of debt, interest-free bills of various issuers with a maturity date of “at sight” at a price below their face value (“discount” bills). In this case, part of the bills received in this way is transferred by the joint-stock company to its counterparties in payment of accounts payable at the purchase price. Part of the bills remains with the JSC on its balance sheet without movement during the tax (reporting) period.

Should the sales price of interest-free non-bank bills maturing at sight be adjusted for tax purposes in cases where these bills were sold at the purchase price (i.e., below par)?

Answer: The issue under consideration is about interest-free bills issued by third parties, for which the terms of their issue do not provide for the payment of interest (coupon) income in the definition established in clause 4 of Art. 280 Tax Code of the Russian Federation.

According to paragraph 2 of Art. 280 of the Tax Code of the Russian Federation, income from operations on the sale of securities is determined based on the price of sale or other disposal of the security. Expenses for the sale of securities are determined based on the purchase price of the security (including the costs of its acquisition) and the costs of its sale. As a result of the ratio of income and expenses from the sale of a security, the profit or loss from the sale is determined.

In relation to securities not traded on the organized securities market and in the absence of trading on the securities market for similar (identical, homogeneous) securities, clause 6 of Art. 280 of the Tax Code of the Russian Federation establishes a special rule for determining the sale price of a security for tax purposes:

“...the actual price of the transaction is accepted if the specified price differs by no more than 20% from the estimated price of this security, which can be determined on the date of the transaction with the security, taking into account the specific conditions of the concluded transaction, the peculiarities of circulation and the price of the security and others indicators, information about which can serve as the basis for such a calculation. In particular, to determine the estimated price of a debt security, the market value of the loan interest rate for the corresponding period in the corresponding currency can be used.”

Thus, in order to accept for tax purposes the actual sales price (in the case considered in the question, it coincides with the acquisition price and is lower than the nominal price) as income from the sale of bills of exchange, it is necessary to determine as of the date of the transaction for the sale of the security:

— actual transaction price

— the estimated price of this security

— 20% of the calculated price of the security

- make a comparison: does the actual price fall within the range of “estimated price plus or minus 20% of the estimated price”

If the answer is yes, then for tax purposes the actual transaction price is accepted.

If the answer is negative, then by virtue of the requirements of paragraph 1 of Art. 40 of the Tax Code of the Russian Federation, the actual price of the transaction is also accepted, however, the tax authorities have the right to control this price in accordance with Art. 40 Tax Code of the Russian Federation.

In other words, the need to adjust for tax purposes the sales price of interest-free non-bank bills maturing “at sight” in cases where these bills were sold at the purchase price arises only if the actual sales price differs by more than 20% from the calculated price of this security, which must be determined on the date of conclusion of the transaction for the sale of the security.

5.2.4. Write-off of “overdue” bills

Question: Currently in circulation on the secondary securities market are previously issued but not presented to date promissory notes of JSC, the date of which is 1995-1998, which have payment terms of 360 days from the date of presentation. From time to time, enterprises holding bills of exchange turn to the JSC with a request to pay bills.

In this regard, the following questions arise:

1. Can a JSC reasonably refuse to pay bill holders due to the expired statute of limitations?

2. Can the JSC write off the debt on these bills of exchange as a financial result?

Answer: 1. In accordance with Art. 78 “Regulations on promissory notes and bills of exchange” (approved by Resolution of the Central Executive Committee and Council of People's Commissars of the USSR dated 08/07/37 N 104/1341) promissory notes for a period of so much time from presentation must be presented to the drawer for marking within the time limits specified in Art. . 23 of the Regulations (one year from the date of issue of bills). The period from presentation runs from the date of the note signed by the drawer on the bill. The refusal of the drawer to put a dated mark is certified by a protest, the date of which serves as the starting point for the period from presentation.

According to Art. 70 of the Provisions, claims arising from a bill of exchange against the acceptor are extinguished upon the expiration of three years from the date of payment. In accordance with Art. 77 of the Regulations, this rule applies in the event of a claim against the drawer of a promissory note, since it is not incompatible with the nature of the document.

If a promissory note issued for a period of “so much time from sight” is not presented for affixing a dated mark within a year from the date of its issue (from the date of preparation), then the payment period (360 days) must be calculated starting from the first day ( inclusive) after the expiration of the one-year period for presenting the bill to the drawer. For example:

a) a promissory note issued (drawn up) on January 3, 2002;

b) the payment period for the bill is 45 days from the date of issue;

c) within a year from the date of issue of the bill of exchange (from 01/03/2002 to 01/03/2003), the bill of exchange was not presented for affixing a dated mark.

In this case, the payment deadline for the bill will be 02/17/2003.

In accordance with Art. 38 of the Regulations, the holder of a bill of exchange for a certain day or within such and such a time from drawing up or from presentation must present the bill for payment either on the day on which it is due to be paid or on one of the next two business days.

Consequently, in the situation under consideration, the limitation period for a bill of exchange must be calculated from 02/20/2003. Accordingly, the limitation period for such a promissory note expires on 02/20/2006.

It is important to note that the statutory limitation periods for bills of exchange are preemptive. Thus, if, as a general rule (clause 2 of Article 199 of the Civil Code of the Russian Federation), the expiration of the limitation period serves as a basis for refusing a claim only in the case where the application of limitation is declared by a party to the dispute, then the expiration of the bill of limitations period, in principle, extinguishes the material the right of the holder of a bill to demand payment of a bill. The court applies this period regardless of the application of the party to the dispute (see, in particular, paragraph 22 of the Resolution of the Plenum of the Supreme Court of the Russian Federation and the Supreme Arbitration Court of the Russian Federation dated December 4, 2000 N 33/14 “On some issues in the practice of considering disputes related to the circulation of bills of exchange” ).

2. According to paragraph 18 of Art. 250 of the Tax Code of the Russian Federation, non-operating income taken into account when taxing profits includes amounts of accounts payable (obligations to creditors) written off due to the expiration of the statute of limitations or for other reasons. In paragraph 4 of Art. 271 of the Tax Code of the Russian Federation, the date of recognition for tax purposes of receipt of income in the form of accounts payable with an expired statute of limitations is not directly defined. Thus, the general norm for recognizing income established in paragraph 1 of Art. 271 of the Tax Code of the Russian Federation: “: income is recognized in the reporting (tax) period in which it occurred:”.

Since the Tax Code of the Russian Federation (in particular, Chapter 25 of the Tax Code of the Russian Federation) does not establish the procedure for determining in tax accounting “written off” or “unwritten off” accounts payable that cannot be recovered from the taxpayer due to the expiration of the limitation period or for other reasons, then according to Art. 11 of the Tax Code of the Russian Federation, accounting legislation must be applied.

As discussed above, the organization is obliged to write off debt amounts at the time of expiration of its limitation period. Thus, at the moment of expiration of the limitation period for repayment of JSC bills, for profit tax purposes, accounts payable for their payment must be written off as non-operating income.

When including accounts payable in non-operating income, one should take into account the amount of taxes (VAT, excise taxes) related to the supplied inventory, work and services, in payment for which the JSC’s own bills of exchange were transferred, as in the revenue part of the tax base by virtue of clause 18 of Art. . 250 of the Tax Code of the Russian Federation, and in non-operating expenses by virtue of clause 14 of Art. 265 Tax Code of the Russian Federation.

Since in the situation under consideration the bills of exchange were issued in 1995-1998, the statute of limitations for their repayment expired before January 1 of the current tax period. Therefore, when reflecting income in tax accounting, it is necessary to talk about the application of clause 18 of Art. 250 of the Tax Code of the Russian Federation, and clause 10 of Art. 250 of the Tax Code of the Russian Federation (income of previous years identified in the reporting (tax) period).

In relation to the specified type of non-operating income in sub. 6 clause 4 art. 271 of the Tax Code of the Russian Federation establishes the date of its recognition for profit tax purposes - the date of identification of income (reception and (or) discovery of documents confirming the existence of income).

This circumstance, in our opinion, indicates that in the tax return for the current year the JSC is obliged to reflect in non-operating income subject to taxation the entire amount of identified income in the form of accounts payable that have not been written off in a timely manner with an expired statute of limitations.

However, in the option under consideration, it may be more profitable for the enterprise to use the opinion of the Ministry of Taxes of the Russian Federation, set out in paragraph 5 of the Methodological recommendations for the application of Chapter 25 of the Tax Code of the Russian Federation (approved by Order of the Ministry of Taxes of the Russian Federation dated December 20, 2002 N BG-3-02/729):

"5. For the purpose of applying paragraph 10 of Article 250 of the Tax Code of the Russian Federation, if, based on the income of previous years identified in the reporting (tax) period, it is not possible to determine the specific period of errors (distortions) in the calculation of the tax base, then the specified income is reflected in non-operating income, then there are adjustments to the tax liabilities of the reporting period in which errors (distortions) were identified.

If, upon detection of errors (distortions) in the calculation of the tax base relating to previous tax periods, it is possible to determine the period of the errors (distortions), recalculation of tax liabilities is carried out in the period of the error in accordance with Article 54 of the Tax Code of the Russian Federation. In this case, the taxpayer is obliged to submit an updated Declaration to the tax authority. According to Article 87 of the Tax Code of the Russian Federation, tax authorities have the right to conduct on-site tax audits of taxpayers for three calendar years preceding the year of the audit. In this regard, for recalculation of tax liabilities associated with the identification of errors (distortions) in previous reporting (tax) periods before January 1, 2002, the taxpayer is obliged to submit to the tax authority an updated Declaration in the form established by Instruction of the Ministry of Taxes of Russia dated June 15, 2000 N 62 “On the procedure for calculating and paying income tax for enterprises and organizations to the budget.” If errors (distortions) are detected in reporting (tax) periods after January 1, 2002, the taxpayer submits an updated Declaration in the form approved by Order of the Ministry of Taxes of Russia dated December 7, 2001 N BG-3-02/542 (registered with the Ministry of Justice of Russia dated December 17, 2001 N 3084), taking into account the additions and changes made.”

In the case of structuring the occurrence of the expiration of the limitation period for the bills of exchange in question by year, it is possible that a number of amounts of accounts payable will be outside the time limits for tax control measures.

However, it is also necessary to evaluate the fact that in the case of filing updated returns for previous periods, it will be necessary to apply the income tax rate in force in the same periods. In addition, if updated declarations are submitted by the tax authorities, penalties will be charged on the tax amounts subject to additional payment.

Third party promissory note

When receiving a bill of exchange from a third party from the buyer before shipment of goods (performance of work, provision of services), accrue VAT at the time the bill of exchange is accepted for accounting (subclause 2, clause 1, article 167 of the Tax Code of the Russian Federation). This is due to the fact that a third party bill of exchange received from the buyer (customer) before the shipment of goods (performance of work, provision of services) is considered receipt of advance payment (advance payment (partial payment)). A third party’s bill of exchange is property – a financial investment in the form of a security (clauses 2–3 of PBU 19/02, clauses 1 and 2 of Article 38 of the Tax Code of the Russian Federation). Therefore (unlike its own bill of exchange) it extinguishes the obligations of the buyer (customer). A similar point of view is shared by the Russian Ministry of Finance in letter No. 03-04-08/77 dated April 10, 2006. Thus, upon receipt of a third party’s bill of exchange, the buyer’s (customer’s) obligation to pay for goods (work, services) is considered fulfilled. This follows from paragraph 2 of Article 153 and paragraph 1 of Article 154 of the Tax Code of the Russian Federation.

The accrual of VAT on an advance (partial payment) received in the form of a third party bill of exchange should be reflected as follows:

Debit 76 subaccount “Calculations for VAT on advances received” Credit 68 subaccount “Calculations for VAT”

– VAT is charged on the amount of the advance (partial payment) received in the form of a third party’s bill of exchange.

At the time of shipment of goods (performance of work, provision of services), deduct VAT accrued from the advance payment (partial payment) (clause 8 of Article 171 of the Tax Code of the Russian Federation). In this case, make the following entries:

Debit 90-3 (91-2) Credit 68 subaccount “VAT calculations”

– VAT is charged on proceeds from the sale of goods (performance of work, provision of services);

Debit 68 subaccount “Calculations for VAT” Credit 76 subaccount “Calculations for VAT on advances received”

– accepted for deduction of VAT on the amount of advance payment (partial payment) received in the form of a third party’s bill of exchange.

For information on calculating VAT on prepayments, see How to calculate VAT on advances received.

A bill of exchange as a safe element of tax planning

Methods for optimizing taxation using bills of exchange have always been of particular interest to tax authorities. Mainly because, by using these securities in calculations, unscrupulous taxpayers tried to obtain a VAT refund from the budget without paying the tax in real money.

Since 2006, thanks to changes to the Tax Code, according to which payment is not important for deducting VAT (Federal Law No. 119-FZ of July 22, 2005), the use of bill of exchange schemes for unfair optimization of VAT has lost its meaning. But since a certain stereotype has already developed, companies are still wary of using bills of exchange in business transactions. And tax authorities still pay close attention to those transactions of companies in which a bill of exchange is used for settlements. And they even put forward settlements by bill of exchange as one of the signs of a company’s dishonesty (for example, such a criterion was named in the letter “for official use” issued by the Federal Tax Service in the spring of this year*).

Practice opinion

Sergey Sazonov, head of the financial department of OJSC NizhegorodOblGaz: - In the early 90s, economists considered the bill as a panacea in the conditions of the non-payment crisis. But at the same time, the classic option of using a bill of exchange - as a debt security - was practically forgotten.

At that time, companies actively used trade credit when paying suppliers for raw materials using their own bills of exchange with subsequent acceptance for the goods. The scheme itself is not bad. However, it was discredited by the greed of bill issuers, who did not want to perceive their own bills (unconditional obligations) as equal to monetary obligations, trying to ship illiquid products for them at inflated prices. Accordingly, almost all commodity bills were not worth more than 60-70 percent of their face value and contributed to corruption in the enterprise itself. And their excessive release led to an increase in the share of non-cash components in revenue, a cash crisis. Therefore, all bill programs were curtailed and a strong prejudice developed against them.

Now the negative attitude towards bills remains. Tax authorities have classified almost all transactions with bills of exchange as suspicious transactions, and financiers and accountants (at least of most large companies) do not want to attract undue attention. Both are, of course, extremes. The bill of exchange has a number of very interesting features that can make its use impeccable from a tax and legal point of view and useful in business practice.

So, what is a bill of exchange now? How is it dangerous and how is it useful? Is it now possible to optimize tax payments with its help?

Legal ways to use a bill of exchange: in business activities...

Now bills of exchange are most often used for settlements between counterparties and as security for the fulfillment of obligations. In addition, urgent bank bills can serve as a tool for investing free money in a security with high reliability, high liquidity, but low interest.

Method 1.

Settlements between counterparties. The most common way to use third party bills is in settlements between counterparties. For example, receipt of bills as payment for goods. Buyers in this situation even benefit - when purchasing a bank bill with a maturity of 30 days, they earn a small discount, and in the acceptance certificates the value of the bill is indicated at par. As a rule, sellers agree with this practice. Firstly, they, in turn, can pay suppliers with such a bill of exchange also at par. And secondly, they can present the paper to the bank for payment at a convenient time with payment to the desired bank account.

Of course, if you do not wait for the bill to be paid, then if you repay it early, the bank will pay it at a discount. Nevertheless, due to the fact that the receivables of buyers with bills of exchange are actually repaid earlier than by non-cash transfer, by increasing the turnover of receivables, the seller saves on interest on a bank loan.

Practice opinion

Sergey Sazonov, head of the financial department of OJSC NizhegorodOblGaz: — Carrying out settlements with bills of exchange is often more convenient and faster than with cash. For example, when it is necessary to formalize transactions retroactively (which is impossible for any transactions with funds) or to carry out multilateral settlements, offsets, or close relationships at the end of the reporting period involving two or more counterparties. In addition, carrying out internal settlements of holding structures without the use of money has obvious economic advantages, since it significantly reduces the overall need for working capital, which, as is known, has its own credit price.

Maxim Domukhovsky, chief accountant of several organizations: - Payments with bills of exchange are simply necessary even in the case when the tax authorities have blocked the current account. If buyers transfer bills of exchange as payment, and the company uses them to pay suppliers, this will prevent the paralysis of economic activity.

Expert commentary

Svetlana Zadvornova, managing director for tax practice at BDO Unicon North-West LLC: - The use of bills of exchange as a means of payment when purchasing goods (works, services), property rights subject to VAT is currently becoming more unprofitable due to the fact that the buyer , who paid with a bill of exchange, will be able to deduct VAT only after paying the bill of exchange. This requirement of paragraph 2 of Article 172 of the Tax Code of the Russian Federation has remained unchanged, despite the fact that, as a general rule, the right to apply a VAT deduction arises regardless of the fact of payment. Thus, companies that use bills of exchange in mutual settlements find themselves in less favorable conditions compared to others. And if we imagine that the decision to repay the debt for purchased goods (works, services), property rights by transferring an unpaid bill of exchange is made after VAT has been accepted for deduction, then the payer will most likely have to restore the previously accepted VAT for deduction.

In addition, from January 1, 2007, changes made to paragraph 4 of Article 168 of the Tax Code of the Russian Federation come into force, according to which, when securities are used in calculations, the amount of VAT is paid to the supplier in cash by a separate payment order.

Official position

Olga Duminskaya, Advisor to the Tax Service of the Russian Federation, III rank, Department of Indirect Taxes of the Federal Tax Service of Russia: - Tax authorities pay special attention to situations when taxpayers use bills of exchange in payments for purchased goods (works, services). When using your own bill of exchange, the tax presented by the seller is considered actually paid and is subject to deduction only when the buyer pays his bill of exchange in cash.

If the taxpayer uses a third party’s bill of exchange for settlements, he has the right to deduct tax amounts at the time of transfer of the bill of exchange under endorsement in payment for the goods (work, services) purchased by him. But provided that the specified bill of exchange was previously received as payment for goods shipped, work performed and services rendered. In this case, the amount of tax to be deducted is accepted only within the limits of the cost of purchased (accepted for accounting) goods (work, services), which does not exceed the cost of the goods (work, services) shipped by this endorser to his buyer, for which he previously received a bill of exchange. If a third party’s bill of exchange was purchased as a financial investment and funds were actually paid for it, then the tax is deductible only to the extent of the funds actually transferred.

The specified deduction procedure was applied previously and is now in effect.

Method 2.

Ensuring transaction security. A bank draft can be used to secure transactions between parties who do not trust each other. In such a situation, an essential condition for the transaction is the simultaneous exchange of goods for money “from hand to hand” without any prepayments or delays. However, in this case, it is necessary to pay due attention to checking the authenticity, liquidity of bills, the correctness of execution of both the bill itself and the chain of endorsements, the absence of arrests, blockings, and entries in the stop lists of issuing banks.

Practice opinion

Sergey Sazonov, head of the financial department of NizhegorodOblGaz OJSC: - In the described situation, the bill acts as an officially approved replacement for cash, the settlement of which between organizations in large quantities is impossible. A bank bill is good because, unlike large sums of cash, it does not require recalculation, is easy to transport, and has a lower risk of counterfeiting. An alternative to a bill of exchange in such transactions can be a letter of credit, but this is a much more complex and expensive form of payment. A bank bill is a much cheaper and quicker instrument, although, of course, it also has its drawbacks, primarily associated with the risks of loss during transportation.

Alina Gurevich, Deputy Financial Director of OJSC Hotel Complex Oka: — On bank bills, as a rule, the telephone number of the bill department of the bank or its branch is indicated, which can be used to obtain confirmation of the issue of the bill. You should not approach this procedure formally - it is advisable to find out the phone numbers of branches yourself, since, despite the fairly high security of the bill forms of most banks, counterfeits still occur. So, in my practice, the details indicated the telephone number where the criminals’ accomplices were on duty; they introduced themselves as employees of the bill department of the issuing bank and confirmed the issue of these bills. It is also advisable to keep a copy of the bill for yourself to resolve possible issues in the future, although due to the fact that a copy is not considered a primary document, it is not necessary by law to keep a copy.

...and in tax planning

At the current moment, it is also possible to apply the bill directly in tax planning.

Method 1.

The transfer of profits from one company to another through a discount on a bill. In particular, this method is beneficial when making payments to an offshore company. For example, a holding company uses transfer pricing, leaving the entire markup in a preferential tax jurisdiction. To close the relationship, the financial center issues bills of exchange, sells them to a company that sells goods to external buyers, a trading company at par value for the amount of goods sold to it offshore. The offshore company accepts bills of exchange at a discount in the amount of the trade margin and presents them to the financial center at par. And with the proceeds he pays the purchasing company working with suppliers of goods (

).

A simplified option is also possible: an offshore company purchases a bill of exchange from a Russian organization at a discount and, after some time, presents it for payment. A discount on a bill reduces the taxable profit of a Russian company and is not taxed offshore.

Previously, such transfer of income was also used using internal Russian offshore companies, but now this is no longer relevant.

Official position

Alexey Kudryashov, tax service advisor, rank II:

— It’s no secret that shell companies are often used instead of offshore companies. Now that payment for VAT is no longer necessary, such a transfer pricing scheme has become even easier to apply. Therefore, the tax authorities are intensively working to combat fly-by-night scams, which should significantly limit the use of this method of minimizing VAT. Moreover, the new Article 93.1 of the Tax Code of the Russian Federation on counter audits, which will come into force on January 1, 2007, has expanded the capabilities of the tax authorities.

Practice opinion

Sergey Sazonov, head of the financial department of NizhegorodOblGaz OJSC: - Since a bill of exchange is essentially a product not subject to VAT, the markup on the purchase and sale of a bill of exchange (discount) is the cheapest tax-free (not leading to VAT) way of transferring income from one company to another. However, now bill income is not balanced, for example, with a loss from core activities; it is shown in the declaration as a separate line and has separate taxation. Therefore, this income transfer scheme is suitable if only the income needs to be transferred to companies that are not VAT payers, or do not have large VAT-related costs, or to individuals, or to an offshore jurisdiction.

Method 2.

Optimization of salary taxes. An individual purchases bills of exchange at a discount and subsequently resells them at par to another legal entity. In this case, the buyer of the bill does not accrue unified social tax. And an individual pays only personal income tax (13%) on the difference ( ).

But if the tax authorities can prove the interdependence of an individual and a company that regularly paid him fixed amounts, this is grounds for accusations that the company and the individual acted in bad faith and created a scheme to evade the Unified Tax.

Method 3.

Prompt redistribution of funds in the holding. This method provides tax-free grounds for the prompt redistribution of funds between companies included in the holding.

There are two most obvious ways to transfer funds from one organization to another without increasing the tax burden. This is an interest-free loan agreement and a bill of exchange agreement. Interest-free loans are convenient, but in accordance with paragraph 4 of Article 6 of the Federal Law of August 7, 2001 No. 115-FZ “On Combating the Legalization (Laundering) of Proceeds from Crime and the Financing of Terrorism” they fall within the scope of attention of the Federal Service for Financial Monitoring, which entails inconveniences associated with the obligation to submit a copy of the agreement to the bank.

On the other hand, funds under this agreement can be transferred in both directions. The movement of funds under an agreement for the purchase and sale of bills of exchange of third parties (for example, bills of exchange issued by a bill of exchange center), although deprived of the above-mentioned advantage of loans (which is decided by the signing of two counter agreements on the purchase of bills of exchange), however, attracts less attention from the FSFM.

Practice opinion

Sergey Sazonov, head of the financial department of NizhegorodOblGaz OJSC: - The widespread use of bills of exchange is dangerous because input VAT on general business costs must be distributed in proportion to revenue for different types of activities. This means also for bill transactions, if they are not of a commercial nature (for example, the purchase and sale of bills). Thus, the active use of bills of exchange for the redistribution of funds (without commodity turnover) is dangerous due to VAT losses for companies with a large number of VAT-containing costs. This problem can be solved by carefully monitoring the timely payment of bills upon their receipt by the company and monitoring the sources of their receipt.

Ilya Antonenko, financial director of the leasing group: — Interest-free loans are indeed subject to control by the Federal Service for Financial Monitoring, and therefore, in order to make payments under an interest-free loan agreement, banks, as a rule, require a copy of the loan agreement to be submitted, regardless of its amount. At the same time, the issue of the need for banks to notify the FSFM of cash flows on non-interest bearing bills is controversial. The agency itself has not developed an official position on this issue, which, however, does not exclude the possibility of introducing a requirement to provide such information on the basis of Article of Law No. 115-FZ.

Unfortunately, a unified arbitration practice has not been developed on the issue of the need to distribute input VAT on general business expenses in the event that the holder of a bill of exchange presents for redemption a bill of exchange of a third party (including a bank bill) received as payment from the buyer, as well as in the case of payment with this bill of exchange goods, works or services. On this issue, decisions are made both in favor of taxpayers (for example, resolution of the Federal Arbitration Court of the North-Western District dated June 10, 2005 No. A66-7746/2004) and in favor of the tax authorities (resolution of the Federal Arbitration Court of the Ural District dated March 15, 2005 No. F09-772/05-AK), which undoubtedly does not contribute to the popularization of bill payments.

Method 4.

Transfer of assets from one company to another. Now payment of fixed assets with bills of exchange will not arouse the persistent interest of tax authorities due to changes in the procedure for calculating VAT. In this way, you can change the “custodian of assets” in the holding even retroactively, ensuring all payments by the new owner of the property with bills of exchange.

Let's assume that the asset holder owes the parent company the value of those assets (this is often the case in holding structures). To secure this debt, he transfers his own bills. The parent company-creditor sells these bills to future asset holders, and for these bills, under a compensation agreement, they purchase assets from the drawer (

).

Method 5.

Accounts receivable management. Debt novation can be used as a way to manage accounts receivable through bills of exchange (Article 414 of the Civil Code of the Russian Federation). The debtor issues his own bill for the amount of debt for the purchased goods and transfers it to the creditor as security for the fulfillment of obligations. For the creditor, such security for an obligation is more profitable than debt under a contract, since in accordance with Article 5 of Law No. 48-FZ on bills of exchange, there is a simplified procedure for judicial collection of debt and shorter terms for consideration of a court case.

Practice opinion

Sergey Sazonov, head of the financial department of OJSC NizhegorodOblGaz: - The bill can still be used as a regulator of the accounting value of large transactions. When the actual selling price of a property differs from the accounting price, a bill of exchange is often used as a “blank item.” If the actual price is less than the accounting price, a bill with a zero actual value at par is transferred as an “add-on” when paying from the buyer to the seller. And in the opposite situation - as an “add-on” to the product. That is, if the buyer wants to increase the accounting value of the acquired expensive object, he pays the difference with bills that are actually worth nothing (for example, issued by a bankrupt). If the accounting price of the transaction decreases, in addition to the agreement on the acquisition of property, the buyer signs an agreement to exchange his bank bill for illiquid bills of third parties of the same denomination.

Thus, by artificially inflating the price of the property, the buyer will reduce his income tax and VAT, but will increase the property tax, and by lowering it, vice versa. Ultimately, in both cases, this method does not reduce the overall tax burden of the transaction - what one wins, the other loses. In addition, one of the partners is faced with the problem of further use of the illiquid bill. And of course, such a transaction (if bank bills were not used) will raise questions during verification.

* You can read more about this in the article “A new approach of government agencies to the integrity of PNP” No. 1, 2006, p. 18.

Tax authorities, out of habit, pay close attention to those transactions of companies in which a bill of exchange is used for settlements

A bank draft can be used to secure transactions between parties that do not trust each other

The active use of bills of exchange for the redistribution of funds (without commodity turnover) is dangerous due to VAT losses

The bill can be used as a regulator of the accounting value of large transactions

VAT on interest on a bill

As a rule, the buyer pays the seller with a bill of exchange, which provides additional income in the form of interest or a discount.

If the goods (work, services) for which the bill of exchange is received are subject to VAT, the interest (discount) on the bill of exchange increases the tax base (subclause 3 of clause 1 of Article 162 of the Tax Code of the Russian Federation). However, VAT does not need to be charged on the entire amount of interest (discount). But only from that part of it that exceeds the amount of interest calculated at the refinancing rates in force in the periods for which the calculation is made (subclause 3, clause 1, article 162 of the Tax Code of the Russian Federation).

Calculate the amount of VAT when receiving interest (discount) on a bill depending on the applicable tax rate as follows.

If the goods (work, services) in payment for which the bill of exchange was received and with which the receipt of interest (discount) on the bill of exchange is associated are subject to VAT at a rate of 18 percent, use the formula:

| VAT | = | Amount of interest (discount) on the bill | – | Interest amount calculated based on the refinancing rate | × | 18118 |

If the goods (work, services) in payment for which the bill of exchange was received and with which the receipt of interest (discount) on the bill of exchange is associated are subject to VAT at a rate of 10 percent, use the formula:

| VAT | = | Amount of interest (discount) on the bill | – | Interest amount calculated based on the refinancing rate | × | 10/110 |

Such rules are established in subparagraph 3 of paragraph 1 of Article 162 and paragraph 4 of Article 164 of the Tax Code of the Russian Federation.

In accounting, reflect the accrual of VAT on interest (discount) on bills of exchange of buyers (customers) by posting:

Debit 91-2 Credit 68 subaccount “VAT calculations”

– VAT is charged on interest (discount) on the bill.

This procedure is provided for in the Instructions for the chart of accounts.

If the goods (work, services) with which the receipt of interest (discount) is associated are not subject to VAT, do not charge the tax (clause 2 of Article 162 of the Tax Code of the Russian Federation).

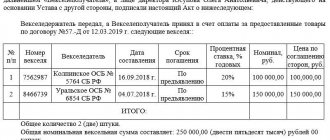

An example of calculating and reflecting in accounting VAT from a discount on the buyer’s own bill of exchange received by the seller as payment for shipped goods

On January 9, Alfa CJSC (seller) shipped a consignment of goods to Torgovaya LLC (buyer) for a total amount of 118,000 rubles. (including VAT – 18,000 rubles). Cost of goods sold – 90,000 rubles.

In payment for the goods, the buyer issued the seller a simple promissory note dated January 5 of the year with a face value of 130,000 rubles. The maturity date of the bill is January 31. On this day, the bill was presented for redemption and the entire amount was transferred to the seller’s bank account.

The discount amount on the bill is 12,000 rubles. (RUB 130,000 – RUB 118,000). The refinancing rate in January is 8.25 percent (conditionally).

For accounting purposes, Alpha's accounting policy does not provide for uniform attribution of the discount to financial results during the circulation period of the bill.

Alpha's accountant calculated the amount of the discount on which the selling organization needs to charge VAT. First, he determined the amount of interest based on the refinancing rate: 118,000 rubles. × 8.25%: 365 days. × 22 days = 587 rub.

The amount of VAT payable to the budget on the amount of the discount received on the bill is equal to: (12,000 rubles – 587 rubles) × 18/118 = 1,741 rubles.

In accounting, to reflect settlements with bills of exchange, the Alpha accountant opened a subaccount “Settlements on bills received” to account 62 “Settlements with buyers and customers”.

The following entries were made in accounting.

January 9:

Debit 62 Credit 90-1 – 118,000 rub. – revenue from the sale of goods is reflected;

Debit 90-2 Credit 41 – 90,000 rub. – the cost of goods sold is written off;

Debit 90-3 Credit 68 subaccount “VAT calculations” – 18,000 rubles. – VAT is charged for payment to the budget on proceeds from the sale of goods;

Debit 62 subaccount “Settlements on bills received” Credit 62 – 118,000 rubles. – the buyer’s own bill of exchange has been received.

January 31: